Introduction

The main argument for the dollar crashing (losing 50+ % of its value vs. other currencies) is decreasing demand because foreign entities will “dump dollars.” This is also one of the main talking points for those who believe the US will lose reserve status within the next 10 years.

In my view, this argument doesn’t take into account the way the current monetary system is structured. Incidentally, the structure I’m referring to is why…

- Headline CPI in the US can go up to 9.1%.

- Government debt can increase from approximately 22 trillion in 2019 to 34 trillion today.

- Deficits can explode.

- Foreign central banks/governments can “dedollarize”.

All while the dollar appreciates in value vs other currencies and maintains market share in terms of use by global commercial banks and non bank entities.

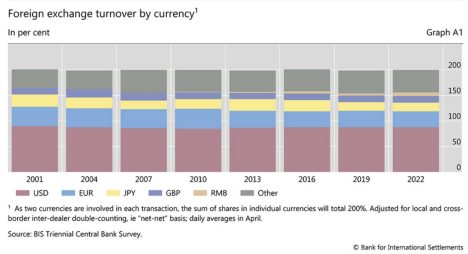

Please notice how USD reserves held by global central banks have decreased while bank use (FX transactions as a proxy) has stayed constant. I believe the latter is far more important in determining the dominant global currency because it reveals the private sector preference.

Monetary Mechanics

Let’s start by recognizing an undebatable fact, the banks create dollars by lending them into existence, they don’t lend dollars that already exist. This is a crucial distinction to make. Why?

Because when a loan is created it creates “money” and when the loan is paid off it destroys “money,” therefore the amount of money in the system is mostly dependent on the rate at which loans are created and paid off. This is especially true for the dollars offshore because such a small percentage are in the form of currency. Conversely, if a dollar that was printed (hard currency) is lent or paid back, the transaction doesn’t impact the money supply.

We also have to understand the number of dollars is always less than the principal plus interest (not enough money to pay off debt), so either velocity has to be high or more loans/dollars need to be created to avoid defaults. Additionally, if velocity decreases, or is low, more loans/dollars then otherwise would’ve been needed, have to be created to compensate for the lack of circulation of the dollars that currently exist. If not, entities that owe the dollars will have to sell assets (often other currencies) to make the debt payments. More on that later.

Dedollarize Narrative

The argument is foreign entities are going to start transacting in other currencies decreasing the demand for dollars, therefore the dollar value relative to other currencies will decrease. If dollar value goes down this will incentivize other foreign entities to “dump dollars” and it becomes a vicious downward cycle. All those dollars flood back into the US, causing extreme domestic inflation, which makes the dollar even less attractive to foreigners, and the doom loop is exacerbated.

What makes this narrative so enticing, to the point of it going “viral,” is it makes sense, the same way the Sun rotating around the earth makes sense because you can see the Sun moving during the day. The problem is the monetary system, like the solar system was during the time of Copernicus, is not only complex but very often counterintuitive. Therefore to properly assess the “dollar crash” we need a monetary telescope (shout out Steve Keen) which is simply a balance sheet(s).

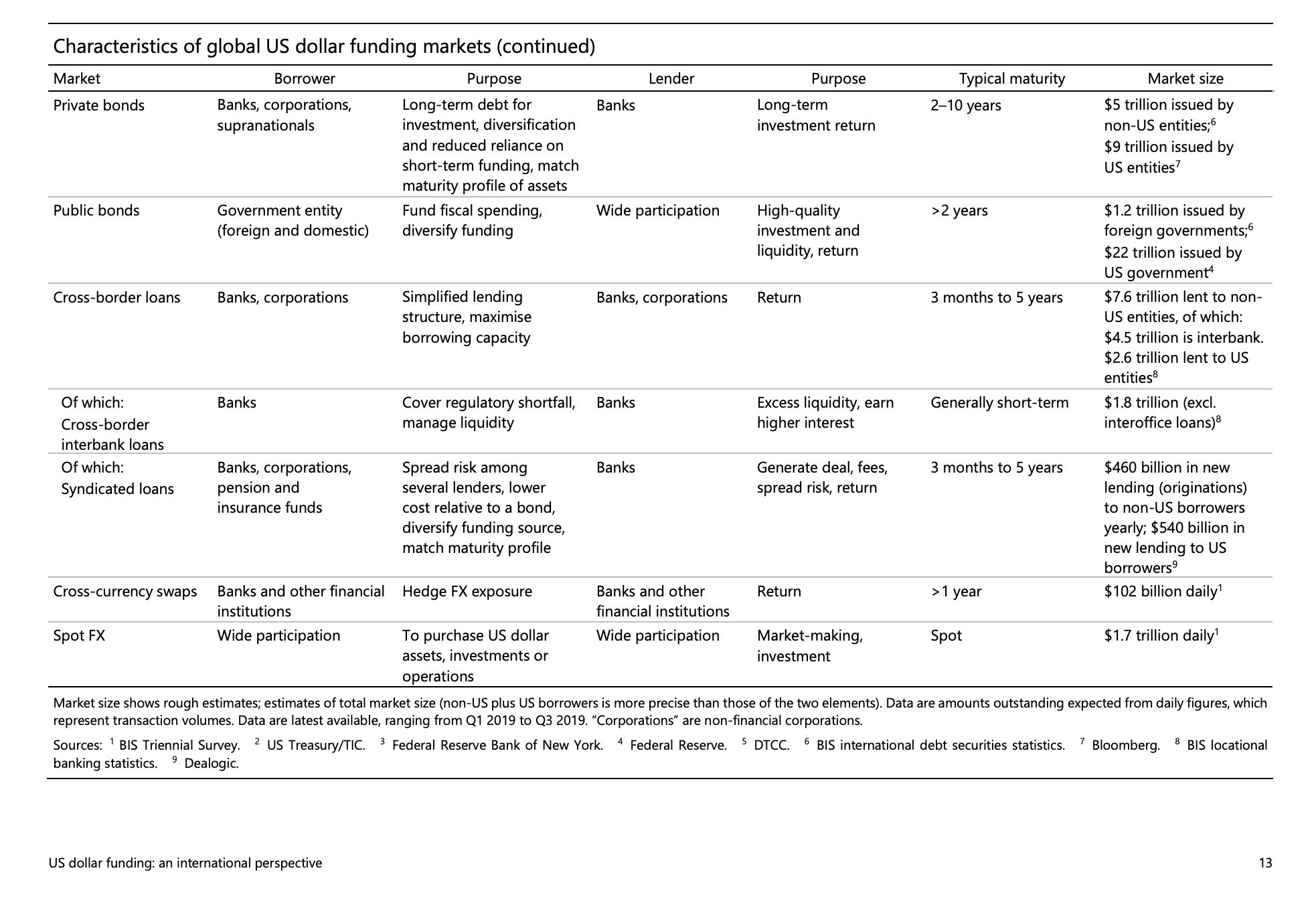

Aggregate Balance Sheet

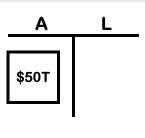

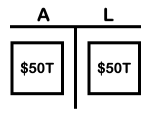

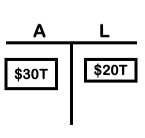

Assume there’s $50 trillion total outside the US. Said another way, the aggregate balance sheet has $50 trillion in dollar cash assets.

Those $50 trillion were lent into existence so the aggregate balance sheet outside the US would also have $50 trillion of dollar denominated debt as an offsetting liability. (more considering interest but we'll just focus on principal to keep it simple).

Maturity Matters…A lot

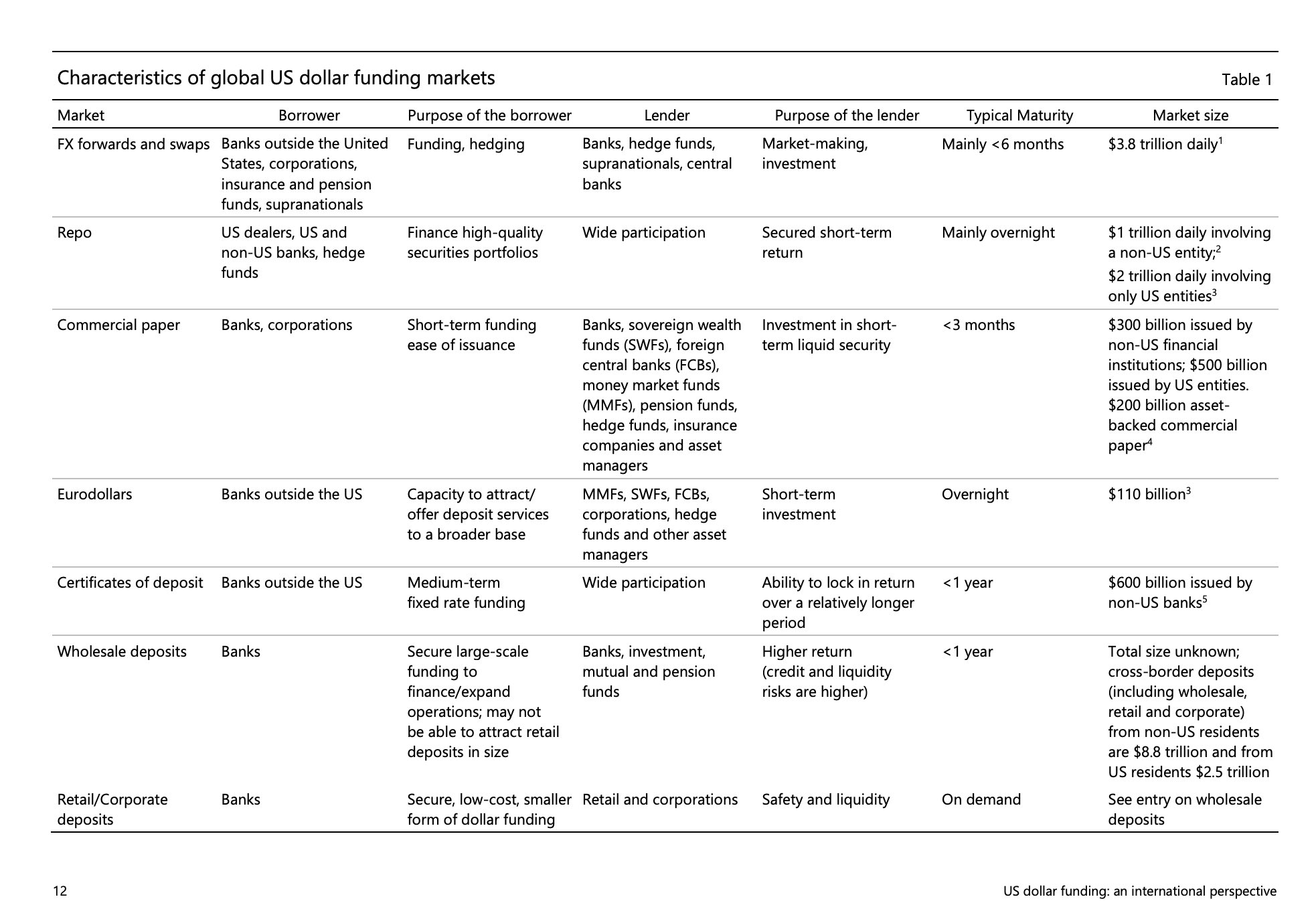

Before continuing I’d like to point out, although it’s impossible to get exact numbers, I think we can assume much, or even most, of the dollar debt outside the US issued by banks is short term. See BIS data on global dollar funding markets, specifically the field titled “typical maturity.”

Keep in mind, not all lenders are banks, which would still apply to demand for dollars to pay dollar debt, but wouldn’t apply to dollars being created or destroyed by the lending/paying loan process. Why?

Banks are the only entities listed who are actually creating new dollars when they lend, the non bank entities are only lending dollars that already exist.

Another tool for determining average maturity of dollar debt outside the US is good ole fashion common sense. What are the main categories of direct bank lending?

1. Consumer (home, auto)

2. Corporate/Commercial

3. Interbank

I think we can safely say very few dollar denominated consumer loans are being created outside the US and tend to be longer term. I’d assume most corporate borrowing is less than five years and most interbank lending is less than one year, so overall short term.

Possible Actions To Dedollarize

1. Sell dollars for currency xyz. Those dollars are purchased, but if the number of sellers outweighs the number of buyers, the dollar's value relative to the other currencies goes down.

Notice: did the aggregate balance sheet change? No. In other words, even though the dollars have changed hands there is still $50 trillion cash assets and $50 trillion of liabilities, at some point the dollars will be in demand by the entities who owe the debt. Although demand can decline, it can’t go lower than the outstanding debt.

Now is when the maturity of the debt matters. Why?

Let’s assume all the debts are balloon payments for the sake of keeping it simple. If the maturity is ten years, the demand for those dollars won’t come for a long time. This means the new dollars created by the loan have plenty of time to circulate and create downward pressure on the value.

But what if the maturity is one week? Now the entities who owe the dollars must earn, buy, or borrow them ASAP assuming they don’t already have the dollars on their balance sheet. Let’s remember. This is happening in an environment where the world is dedollarizing so it’s safe to say banks will be less incentivized to roll over the borrowers debt because the costs now outweigh the benefits and it will be harder for the entity to earn dollars because everyone is now using the new XYZ currency so the risk of default increases. And of course, if the world goes into a recession or has some sort of crisis the banks willingness to lend will go down further along with the entities total revenues, exacerbating the problem.

So what if the borrowers can’t roll over the debt and they don’t have the dollar cash flow? Then they have to sell whatever other currency is on the balance sheet to get the dollars they need, which reverses the original action of dumping dollars because now the other currencies are being dumped to buy the dollars. Those dollars are then used to pay off the debt which decreases the supply of dollars…more on that in a moment.

What if the borrowers can roll over the debt? This buys them time but may increase the risk of default due to dollars being used less and less and the high probability interest rates would go up based on what we’ll discuss in #2.

So the main takeaway from Action #1 is if entities dump dollars it may decrease value of dollar vs XYZ currency temporarily but only in so far as the debt doesn’t come due soon. And demand can only decrease to the level of outstanding debt. As a reminder, the debt which created the dollars outside the US is short-term for the most part, so the impact of selling dollars for XYZ currency would likely be minimal and short-lived, especially if the global economy was slowing due to recession, war, black swan etc.

2. Use dollars to buy US assets.

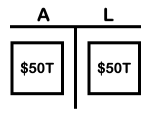

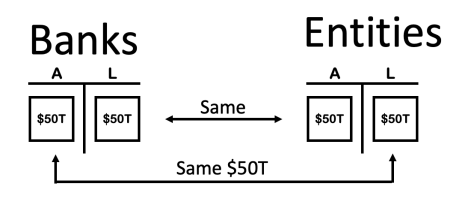

Let’s look at the 50 trillion dollar aggregate balance sheet outside the US again and add the aggregate balance sheet inside the US, say $20 trillion for easy math.

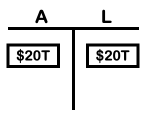

Suppose $10 trillion comes flooding into the US to buy stocks, real estate etc., how do the balance sheets change? Outside of the US there are now $40 trillion cash assets and $50 trillion of debt liabilities and in the US there are $30 trillion and $20 trillion.

As a result, there’s an undersupply of dollars outside the US relative to demand to pay debt and oversupply inside the US. Adding insult to injury the maturity of the debt inside the US is likely much longer giving the oversupply more time to put downward pressure on the dollar vs. US domestic goods and services.

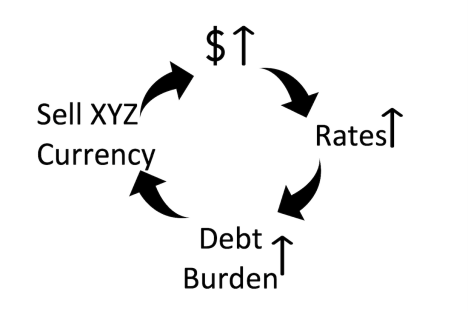

Because of the undersupply outside and shorter maturity of debt (that’s key) the value of the dollar would likely shoot higher vs. other currencies. But that’s not all, odds are Jerome Powell would raise rates to combat the growing inflation due to dollars flooding into the US. As a result, even if the entities outside the US could roll over their debt it would be at a higher interest rate making the debt burden even more overwhelming. And let’s remember while this is happening the dollar is increasing in value relative to the currency of the cash flow they’re receiving (assuming it isn’t dollars) or the assets on their balance sheet, so they’re having to sell more and more XYZ currency (XYZ currency asset) to buy the number of dollars they need, and the amount they need is increasing due to the higher rates. This creates a positive feedback loop where the dollar goes continually higher, a short squeeze.

1. Dollar shoots higher vs. XYZ currencies.

2. Powell raises rates which likely would impact front of the curve.

3. Debt burden increases:

a. Because higher rates = more dollars owed (demand).

b. And because higher dollar = more xyz currency to get dollars needed to pay debt.

Unfortunately, it gets worse. What we haven’t discussed yet is the asset loan that was created by the banks when the entities borrowed the dollars and received the cash asset and the loan liability. These loan liabilities of the entities are assets of the banks and deposit liabilities of the bank are assets of the entities.

If rates go up the value of the banks loan assets go down if they’re not hedged properly (Silicon Valley Bank as an example). A bank whose assets are decreasing in value faster than their liabilities will have a hard time not going bust. That means creation of new loans and velocity of existing dollars will decrease making it even harder for the entities that owe dollars to find liquidity. And remember, the dollar cash assets of the entities are simply liabilities (or IOUs) from the banks, so if they go bust the dollar cash assets of the entities disappear.

This would create massive deflationary pressures, potentially a deflationary bust because let’s not forget all currencies, even the currencies held by the entities that sold dollars are liabilities of a bank. If the banks with dollar debt assets go bust they’ll likely bring down other banks with no dollar debt liabilities. Why?

The global monetary system is simply a network of banks and financial institutions that deal in many currencies, are highly levered, and don’t usually settle in cash or bank reserves but in IOUs (from bank A to bank B, from bank B to bank C and bank C to bank A.) Due to the fact it’s highly interconnected the assets of one bank are the liabilities of another and vice versa.

(On a side note, this would likely lead to the central planners moving the commercial bank deposit liabilities onto the balance sheet of the central banks (aka CBDC) to avoid the deflationary bust).

The banks and financial institutions understand these dynamics very well which reduces the probability of the dollar losing reserve status to begin with. In other words, oddly, the potential level of devastation caused by the global dollar monetary network fracturing makes it stronger.

Obviously, I’m using extremes to illustrate how the system works. It’s doubtful that $10 trillion would flood into the US at once or within the span of a month, but the same dynamics would apply to $1 trillion, only to a lesser degree.

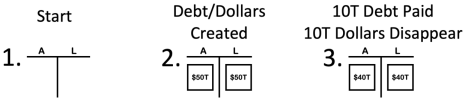

3. Pay down/off dollar debt. Assuming more debt was being paid off than was being created (which seems likely if the world is dedollarizing), the decrease in demand for dollars would decrease the supply of dollars. Why?

If dollars were created when the loans were originated then dollars are destroyed when the loan is paid.

I’d also like to highlight something my good friend Mike Maloney discusses in his series “Hidden Secrets of Money,” there’s always more debt (principal + interest) than dollars to pay the debt. This is especially true in the Eurodollar system that creates dollars outside the US because, for the most part, it’s cashless and reserveless.

So this means as more debt is paid than is being created and the supply of dollars decreases, there’s always a tail risk of lower velocity. If velocity decreases as the number of dollars are decreasing this means defaults will increase because there’s not enough dollars to pay existing debt and the dollars that do still exist aren’t circulating to the entities that need them to make the loan payments. Again, short squeeze.

It’s important to look at the probabilities of velocity decreasing through the lens of debt maturity. Remember, if maturity is shorter, it would put downward pressure on velocity at a time when there’s an increased need for higher velocity due to negative net loan issuance (dollars being created is negative).

Example: Colombia corporation has $1 million of cash assets and $1 million of debt liabilities. If they don’t have to pay the debt for five years, they may choose to invest the cash (higher velocity) in adding machinery to produce more widgets. They realize the additional productivity will likely return to them more than $1 million over the next five years, then they can pay their debt and have more cash left over. But if they have to pay the debt in 2 weeks, they’ll keep the money in the bank (zero velocity) because they don’t want to risk not making the payment to the bank. So if the supply of dollars is decreasing as a result of loans being paid off, or net dollar loan issuance is negative, this could put further upward pressure on dollar vs. XYZ currency. In other words, dollar demand decreasing (assuming Action #3) would likely lead to dollar appreciation, as counterintuitive as that seems.

Conclusion

The dollar crash narrative is popular because it intuitively makes sense.

Less demand relative to supply and the value should go down, we’ve all seen pictures of past hyperinflations where people were carrying all the unwanted currency around in wheelbarrows.

But the way the current dollar monetary system is structured makes all the difference in the world. The vast majority of dollars aren’t printed, they’re lent into existence, therefore demand controls supply. Especially if the maturity of the debt, which created the dollars, is short-term.

If entities want to dedollarize, there are 3 possible actions they could take.

1. Sell dollars for XYZ currency

2. Use dollars to buy US assets

3. Pay off debt

When we walk through the mechanics of each of these options it becomes clear, the probability of the dollar crashing is very low. However, as counterintuitive as it may be, the higher probability outcome is the dollar increasing in value relative to other currencies.