Repo market bailouts Continue

The Fed continues to commit to different and larger amounts of money on term and overnight repos, and recently announced the reopening of the Primary Dealer Credit Facility (PDCF).

My purpose with this blog is to explain each one of these situations and give you a general overview of the economy along with several serious questions about it.

To do so, I will start by putting the cards on the table and explaining where we are today.

Repo market bailout

First, let’s go over the numbers, which are a lot!

These number I’m about to mention are the amounts the Fed is committing to, it doesn’t necessarily mean they will do this amount in repos, it all depends on the demand, but their commitment level is astronomical.

So far, just in term repos, they’ve committed to $6.45 trillion, which they said will go back down on Friday, March 23rd, to only $175 billion.

On overnight repos, last week alone, meaning Wednesday, Thursday and Friday, they committed to $1 trillion a day.

For the next month, or ending April 13th, they’ll go to $7.2 trillion of commitment in overnight repos, and If we add that to the term repos they’ve agreed on, the result is $13.65 trillion.

Insane numbers, right? That’s half of the national debt!

After analyzing these numbers, I ask myself, where would they even get this many treasuries?

I understand they’re doing mortgage-backed securities as well, but this is truly repo infinity.

This is how the Fed is currently bailing out the repo market and the financial system along with it, but this isn’t all. The Fed recently announced the reopening as I said, of the PDCF.

In order to go further into it, I would like to remind you how the repo market works.

Repo market explained

The Fed has set up several commitments, which I already mentioned above.

Those commitments are made to the primary dealers alone, and I want to clarify this because I’ve seen many people are confused thinking the Fed injects money right into the stock market or the corporate bond market.

This is not how the repo market works.

The Fed doesn’t go into the repo market or any other market, they just make transactions directly with their primary dealers.

It works like this: The Fed goes to its primary dealers A, B or C and gives them reserves in exchange for their collateral, usually, treasuries or mortgage-backed securities.

Those reserves become liabilities on the Fed’s balance sheet, but of course, the treasuries and mortgage-backed securities become assets.

So, those $13.65 trillion the Fed committed to, if they truly spend them, will go into the primary dealer’s reserves only, and it would be up to the primary dealers to go into the repo market, or any other market, and turn those reserves into deposits.

This is how the reserves are actually injected into the system.

My point with this is if the primary dealers don’t do anything with the reserves and they just sit at the Fed, it would be like if someone took those $13.65 trillion and hid them under their mattress.

It literally wouldn’t matter, they would just be adding reserves to the system while the real need is to get them out to the system to bail out financial institutions, and hedge funds among others.

Fed’s bailout and the Plunge Protection Team (PPT) scam

The PPT scam started with the reopening of the Primary Dealer Credit Facility (PDCF) that was created by the Fed to, in my opinion, make an open-ended bailout.

To better understand what I mean by this, look at the Fed’s term sheet first because I want to point out several things.

You can read the full document right here.

As you can see, the eligible collateral of the term sheet says they can, not only take the treasuries and mortgage-backed securities they take in the repo market, but they’re also able to take “investment-grade corporate debt, international agency securities, commercial paper, municipal securities, mortgage-backed securities, and asset-backed securities; plus equity securities”.

It also says, and I want to emphasize on this bullet point: “Additional collateral may become eligible at a later date upon further analysis”.

This means that if the CEO has a collection of baseball cards, as an example, or an old 67 Corvette in his garage, the Fed will take that too!

The Fed will take whatever they would want to throw up, and give them money for it instantly, more likely a hundred cents on the dollar.

The loan’s term will be 90 days, but I’m sure they’ll be able to roll it over and get a rate of basically zero.

“Loans will be limited to the amount of margin-adjusted eligible collateral pledged by the dealer and assigned to the New York Fed’s account at the clearing bank”.

So however much they have, the Fed will take it and give them trillions or quadrillions of dollars, it just doesn’t matter.

But, when we get to the end of the document, we’re able to see the most shocking affirmation: How long will be program last?

“The PDCF will remain available to primary dealers for at least six months, or longer if conditions warrant”.

As I said, this is basically an open-ended bailout or a way for the Fed to buy stocks and corporate bonds, but two things could be happening, first and foremost, Peter Schiff tweeted he thinks this is a bailout for the primary dealers.

The Fed just announced bank bailouts 2.0. Loaning money to banks and accepting corporate and muni bonds, plus equities as collateral, so the banks don't have to sell those assets at huge losses, is a bailout. In 2008 I warned the next bank bailout would be even more expensive!

— Peter Schiff (@PeterSchiff) March 18, 2020

If it is a bailout, how would it work?

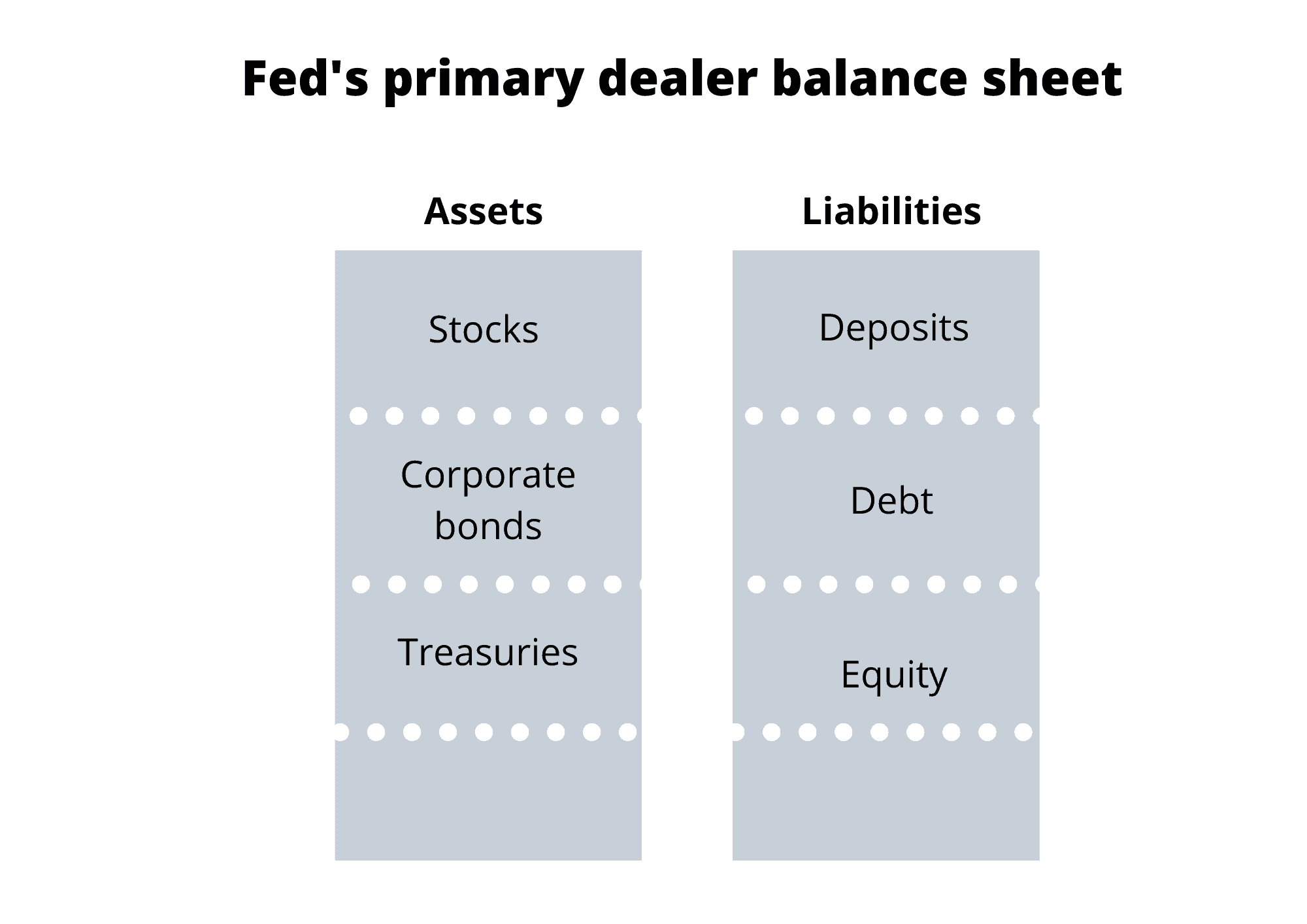

Let’s assume the primary dealer’s balance sheet looks something like this:

They have stocks, corporate bonds, and treasuries on the asset side, but on the liability side, they have deposits, debt, and equity.

They have stocks, corporate bonds, and treasuries on the asset side, but on the liability side, they have deposits, debt, and equity.

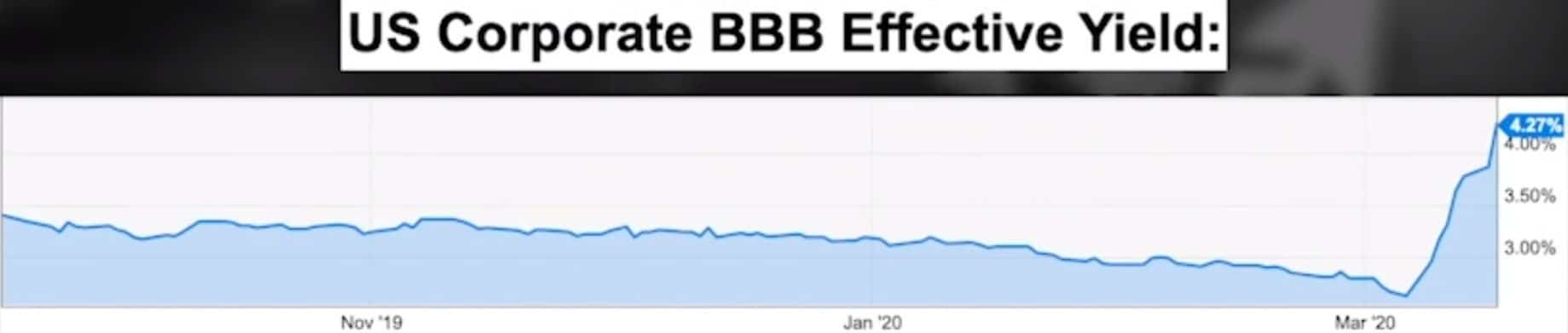

Now, we all know the market has tanked over the last 30 days, and interest rates in the corporate bond market are going through the roof as shown:

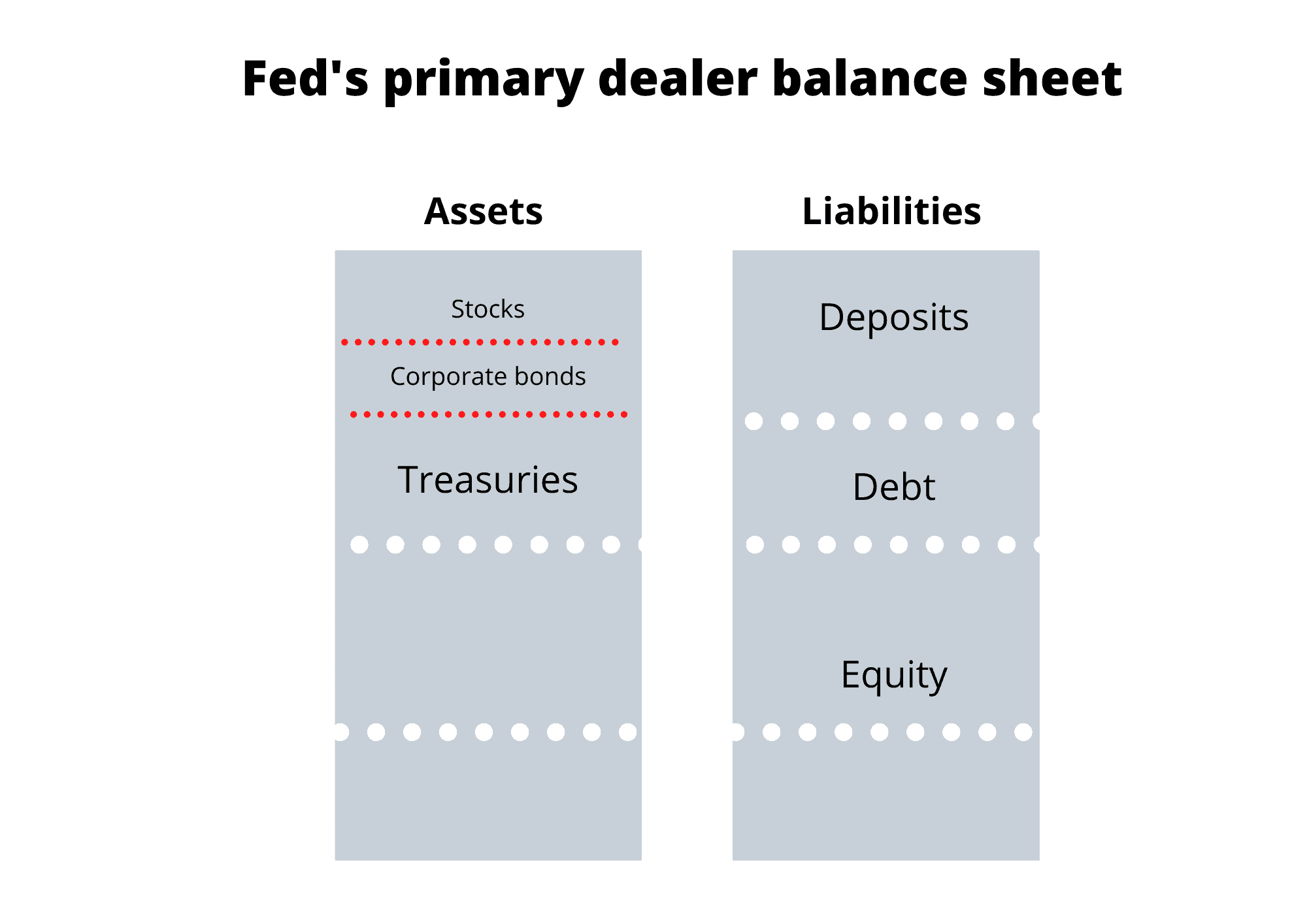

This means the value of corporate bonds is going down, and it also means the reality of their balance sheet isn’t as the one presented in the image above, but rather like this one:

Why?

Why?

Because the stocks they had, have gone down in value and so did the corporate bonds, I highlighted them in red to illustrate this.

So what the Fed does is take their devalued assets off their balance sheet and put them into theirs in exchange for the reserves.

Assuming, at a hundred cents on the dollar as of 30 days ago.

This way the primary dealers don’t absorb the loss they would’ve otherwise taken if they would’ve sold those assets into the open market.

Here’s an example to better grasp this.

If you want a house that costs $100,000 and take a mortgage for $100,000 to buy that home, your balance sheet would have a $100,000 home in the asset side and in the liability side, a $100,000 mortgage.

Let’s assume the house goes down in value by 50%, so now it is only worth $50,000.

The Fed would come to you, take that house off of your balance sheet and give you $100,000, so instead of having negative equity, you’re made whole.

This is exactly what they’re making with the primary dealers.

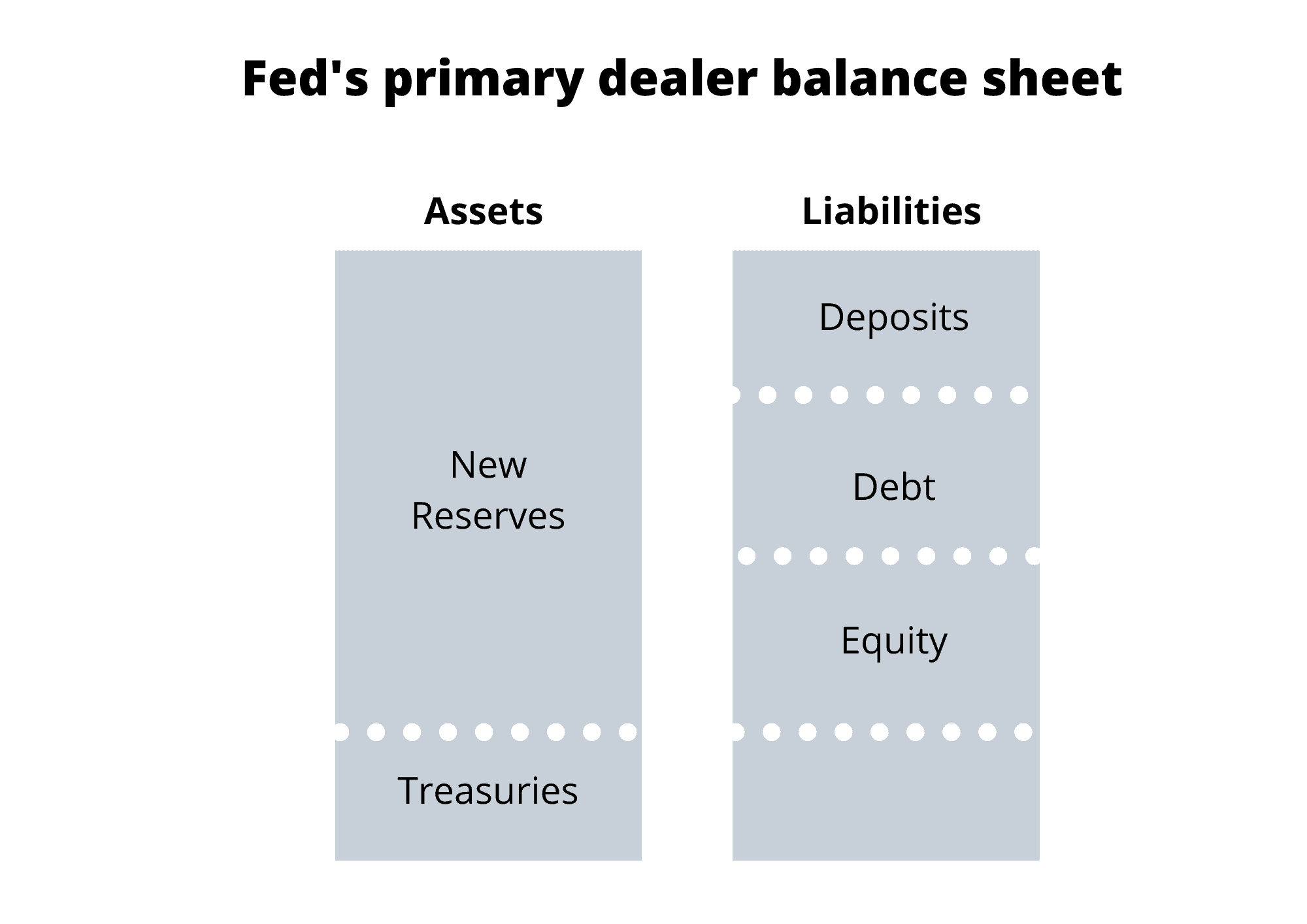

So, having understood what the Fed’s doing, I have a third balance sheet to show you.

As you can see, the primary dealers, instead of having all that garbage, that isn’t worth much, including the treasuries, now have brand new reserves to match up the liability side of their balance sheet.

Also, let’s not forget the primary dealers and banks under the Fed’s umbrella already have $1.5 trillion in excess reserves, prior to the most recent collapse and the PDCF opening up.

So if they have even more excess reserves right now, what’s to stop them from going into the stock market, buying stocks, then to the corporate bond market and buying new bonds just to prop those markets up?

Those assets go into the primary dealer’s balance sheet, but the Fed buys them again, takes them off of their balance sheet and puts the money in their reserves after this exchange.

This allows the primary dealers to buy as many stocks and corporate bonds as they see fit.

It’s truly the Plunge Protection Team (PPT).

Endgame questions

Usually, I conclude with an endgame where I connect all the dots, but right now the data is changing so quickly, and there are so many different variables that’s very hard to know exactly how this is going to play out or even venture a guess.

What we can do is ask ourselves the right questions.

how big is the Fed’s balance sheet going to be when we’re done with this crisis?

When we started our last crisis in 2007-2008, the Fed’s balance sheet was around $800 billion and it got up to $4.5 trillion.

Today, we’re over 4 trillion dollars, so what would the next step be? Where would it be in the next three or six months?

Will it go to $10 trillion, $15 trillion, $20 trillion?

As I read through my Twitter feed last week, I read many people think the Fed’s balance sheet could exceed $10 trillion.

What I think is they would take that and notch it up a few levels now that they’ve introduced the $1 trillion a day repo and the bailout with the PDCF.

How?

It starts with government deficits and it’s not just about the limitless bailouts they’re going to do in the next few months or the fiscal stimulus packages, it’s also about interest rates.

The Fed has to keep interest rates low along the entire yield curve or else, the government isn’t going to be able to afford to issue new bonds and roll over the existing debt.

This is something nobody’s talking about, and the people that build the models in the Fed only assume the interest rates go down in a recession, but what happens if they go up?

Peter Schiff makes a great point regarding this:

“When the Federal Reserve does this stress tests I think they’re engineered so all the banks pass. They’re not really putting them through the type of stress they need.

What are the circumstances that what they’ve never tested was: what happens if there’s a recession, but interest rates go up? That’s never one of their assumptions, they always assume that if there’s a recession, interest rates will always go down.

Well… What if they go up? What if long term rates go up? No bank can withstand that. If we would have stagflation, and that’s where we’re headed to, I think there’s going to be a currency crisis.

The reason the dollar didn’t collapse in 2008 because of QE1 and 2 and all the tarps and bailouts was because everybody believed it was temporary and that the Fed could unwind the balance sheet and normalize interest rates, but none of that happened and now the balance sheet is blowing through the roof and it’s going to be much bigger than it was before.

Now, no one is going to believe they can normalize rates. I mean, they couldn’t do it last time, how are they going to do it this time, especially since we have so much more debt now?

The more debt you have, the harder it is to normalize rates”.

So if we get a stagflation type of scenario where interest rates want to go up, and the market is naturally pushing them up, the Fed will have to counter that by buying those bonds and pegging the yield curve just like they did in World War II.

Where would that take their balance sheet? It goes way north of $10 trillion.

Yet, we haven’t talked about social unrest, which is not part of the mainstream narrative right now, but I think it’s very important.

Think about this: If the Federal government comes in with all these bailouts we’re going to see something like Occupy Wall Street times a hundred.

People will be angered and taking their pitchforks to the street.

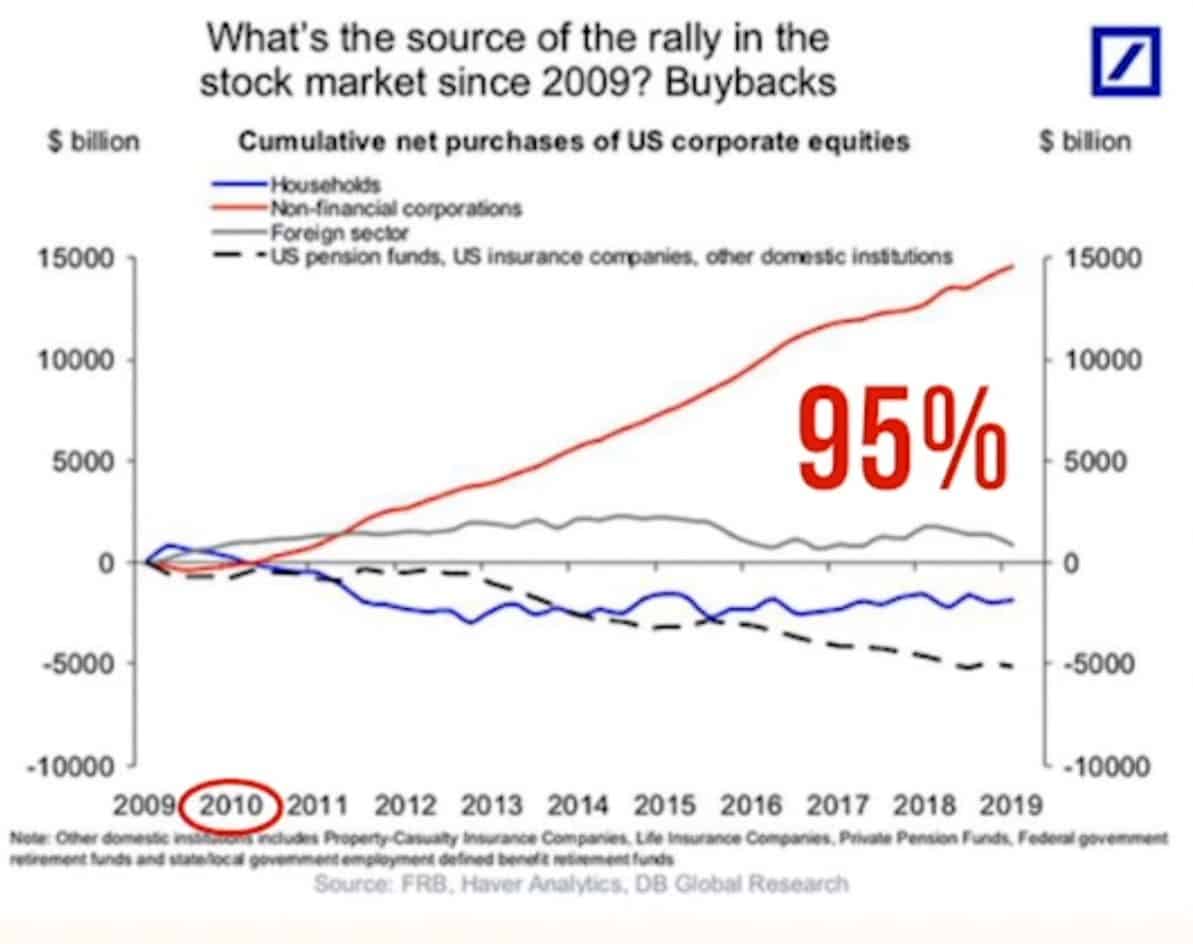

In my opinion, the buybacks on a moving forward basis may be banned, if they don’t do so I think they’ll limit them someway with a new type of Dodd-Frank bill, but remember, the buybacks contributed to almost 95% of the stock market gains since 2010.

If we limit or ban those buybacks, I’m not saying we should, how will the stock market recover? How do people’s 401(k) recover?

They don’t, and that’s my point.

how much will the Federal Reserve have to buy in stocks and corporate bonds, to make sure people’s 401(k)’s aren’t half of what they were thirty days ago on a moving forward basis?

The bottom line is the Fed is going to have to come in and prop up these markets.

How?

By printing money, and again, expanding their balance sheet even further.

The problem is they would now have these two cross-currents or tailwinds to their balance sheet:

1. Peg the yield curve.

2. Print trillions of dollars to keep that yield curve low if market forces push interest rates up so that the federal government can issue more bonds, pay for all of these programs and roll over their existing debt without going bankrupt.

In addition to this, they’re going to have to buy stocks and corporate bonds. I personally see this going north of even $20 trillion.

My next question is: How long would this last?

Dr. Chris Martenson says it’s all about herd immunity, and even if we’re able to cap this in the United States and across the world, it still leaves us in a very vulnerable position going into the fall where we don’t have enough people that have built up that immunity by getting the Covid-19 in the first place.

The takeaway is we might not be done with this until we get a vaccine.

How long would that take?

Most likely 12 to 18 months.

This means that if the Fed has to maintain these operations for a year or 18 months, their debt will go to 20, maybe $30 trillion.

This is not a prediction, I’m just saying if all these circumstances play out, we could see this happening.

Lastly, if the debt goes up to $20 or $30 trillion due to the Fed’s action of creating deposits in the real economy, we might see inflation.

But, will we actually experience all of this?

Keep on reading my blog posts in order to answer those questions.

For more content like this, click on my previous blogs on the oil crash and the repo explained.