Jean Racine once said there are no secrets that time does not reveal, and George proved him right.

Against popular belief, one of the secrets the Fed doesn’t want you to know is deflation is actually good for society. It means lower prices for consumers.

Inflation on the other hand is bad since it causes consumer prices to increase, while asset inflation gives a false sense of security. Not to mention, the upper middle and upper class folks typically own assets like stocks and a 30-year fixed rate mortgage, while the poor and lower-middle-class do not.

The government loves inflation because it allows them to pay back their fixed-rate debt with devalued dollars.

The Fed and Government are also guilty of protecting banks with bailouts. In other words, they socialize losses and privatize profits.

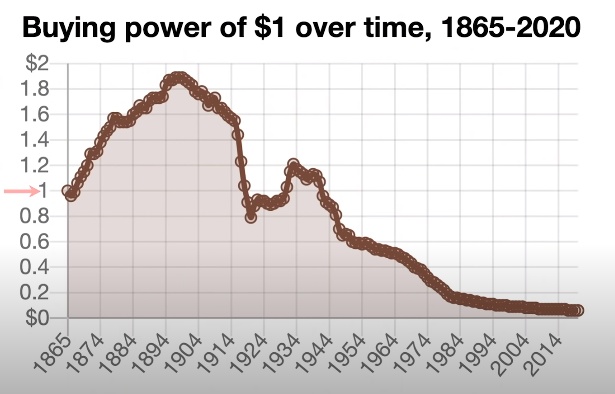

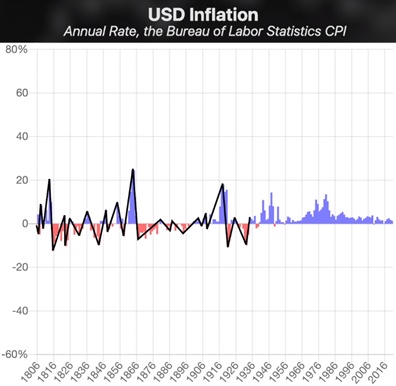

When the Federal Reserve was created in 1913, the dollar started losing its purchasing power. The dollar also went through steep declines each time hot a hot war reared its ugly head.

The Fed: fund wars and create inflation

Before the US Federal Reserve came into existence, the American economy was experiencing deflation. The dollar had a higher purchasing power and the market was highly efficient.

In the late 1800s, The United States was truly a free market without any micromanagement by the US Government. Wages increased, while work hours per week decreased.

Deflation is not the boogeyman. The way the US economy is structured is.

– George Gammon

If asset prices, debt, and confidence weren’t the base of the US economy, deflation would eventually increase demand, which is good.

Between 1865 and 1903 (before the Fed) the cost of goods and services dropped by 1.88% per year, as the GDP doubled in nominal terms. And that was normal! This is what happens in a free and efficient market: Income rises while expenses go down over time.

Despite what the Fed would want us all to believe, inflation is bad. George believes the US Government and the Fed have conditioned unsuspecting tax payers to believe that inflation is actually good, when it's clearly not.

Until 1934, inflation and deflation worked like a heartbeat, with regular ups and downs. After 1934, it was constant inflation.

What does high inflation mean for the US economy?

Even though wages have increased over the years, if you adjust for inflation you'll see that purchasing power has actually decreased. As a result, savers are forced to speculate in the stock and housing markets.

If tax payers don't speculate, then they won’t get ahead financially. Ever.

Inflation creates an environment where it's difficult to save money. Back in the 1800s, people could save money for their retirement. Today, the value of savings is always going down.

In a deflationary environment, savings are good and debt is bad. In an inflationary environment, savings are bad because you lose purchasing power.

Long term, fixed rate debt (like a 30-year fixed rate mortgage) is also good in an inflationary environment because you are essentally shorting the dollar over 30 years. Not to mention, there are tax benefits when owning real estate.

The rich get richer

The people benefiting from today's economy are the ones who own assets. The rich get richer because there is no free market or sound money. You have to be self-educated and willing to take risks.

George also affirms the Fed doesn’t want you to know who owns it. According to institutional investor Citibank, JP Morgan, Goldman Sachs, HSBC, and Deutsche Bank are the Feds biggest shareholders.

These Fed owners profit from the Fed’s money printing because it pushes investors into higher-risk investments. Investment banks became immune to the pandemic because of stimulus checks, quantitative easing, and other measures that sent the markets to all-time highs.

Break Glass In Case of Emergency

The Fed no longer believes in free-markets. Jerome Powell has broken the emergency glass and is reading from an emergency playbook that's not planted in reality.

This playbook is 100% disconnected from any free market activity and requires constant Fed manipulation, which ironically, only makes things worse.

However, insane profits have been generated for investment banks.

In conclusion, investment banks have a very big upside and a very low downside with respect to risk/reward. The Government and the Fed print money and make investment banks “too big to fail”.

Make sure to click play on the video above for a deeper understanding of inflation, deflation, and the twisted mechanisms created by the Fed to run the US economy.

Comments are closed.