Markets are still going crazy, stock market, oil, and spending keep going down while humanity wrestles to avoid Covid-19 and its consequences.

I’ve explained how all of this impacts the entire economy in my previous blogs, so if you’re interested click here, but today I will be getting into the repo market and how its crisis can affect you.

In order to get to the bottom line and how this is important, I need to give you a full context.

Repo market overview

The demand and the number of repos are starting to go up and up.

Last Thursday’s overnight repos closed at $103,100 billion, and the Fed is committing to doing up to 175,000 billion in overnight repos.

14-day term repos had $45 billion in transactions, but there was a demand for $87,1 billion, which means on the 14th day the market was oversubscribed by $42,1 billion.

On 25-day term repos, there were $50 billion in transactions and $82,6 billion in demand with an oversubscription of $32,6 billion.

Altogether there was a total of $74,7 billion of oversubscribed repos, and this is just a slice of the overall repo market which today is at 2 trillion dollars in repos a day.

The $74,7 billion work as a proxy for the oversubscribed, or the repo fails in the broader market, and whenever the Fed sees the market falling, it intervenes and prints more money.

On March 12th, the Federal Bank Reserve of New York said the Desk offered $500 billion in three-month term repos, and the next day they offered another $500 billion in three-month term repos and another $500 billion for one-month term repos.

Along with this, as I said previously, they also committed to $175 billion overnight repos, yet, there’s more.

The Fed is currently buying 60 billion dollars worth of T-Bills every month, in addition to what they’re already doing in the repo market.

They’re also transitioning to buying T-Bills to all maturities of treasuries, this is important because they’re buying and admitting to buying all maturities, which means they’re doing QE4.

But, what’s the real problem with all of this?

To answer this question as a whole, there are a few things you need to understand:

How the repo market provides liquidity, how companies and entity balance sheets work, and why is liquidity so important.

Repo market explained

Liquidity is the key to keeping the entire house of cards from collapsing on itself.

To understand why it is such an important factor in the economy I will give a series of examples of companies and entity’s balance sheets and how they get liquidity on a daily basis.

The Fed is the primary liquidity dealer of the banks, it delivers them cash in exchange for the bank’s treasuries, their pristine collaterals or their mortgage-backed securities, then the Fed deposits the money they print out of thin air into their reserve accounts.

The hope of the Fed when depositing the funny money into the reserves is the banks will use it to lend money into the repo market to other financial institutions, this way they’ll have access to the liquidity they need.

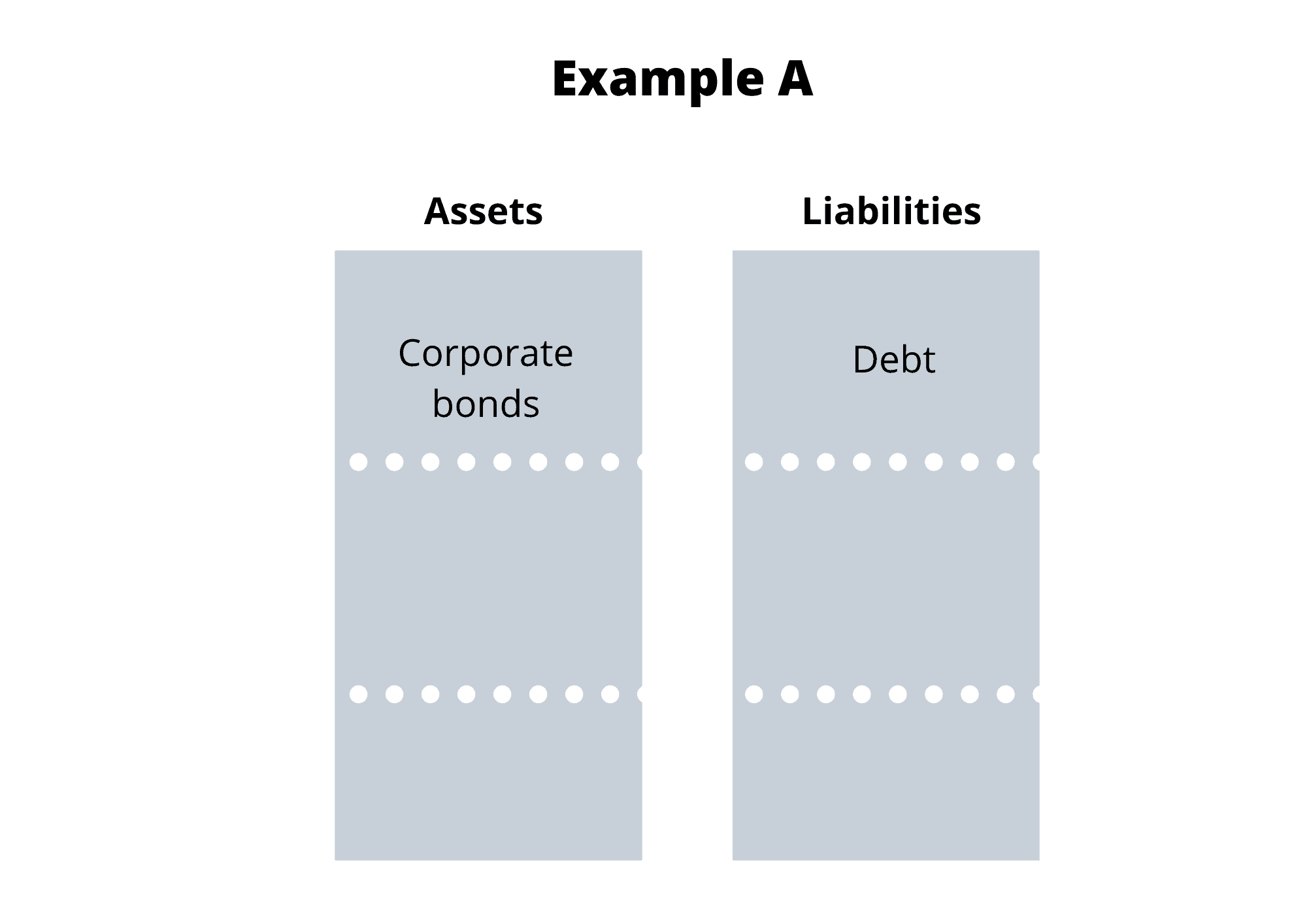

In order to have a better grasp of this and of the actual biggest problem of liquidity, I will explain example A.

Here we have a hedge fund balance sheet, they only possess corporate bonds as assets and debt as liabilities.

They can’t take their corporate bonds into the repo market because in order to trade in the repo market you need pristine collateral, preferably T-Bills, which is why they would usually go to a bank and swap corporate bond for a T-Bill.

They can’t take their corporate bonds into the repo market because in order to trade in the repo market you need pristine collateral, preferably T-Bills, which is why they would usually go to a bank and swap corporate bond for a T-Bill.

If the hedge fund proceeds in this manner, their debt will stay the same, they’ll have fewer bonds, but they’ll now have the treasuries needed to go into the repo market to get liquidity and pay their liabilities while still having a positive asset value.

The problem is when the corporate bond market crashes, meaning interest rates will go up and prices down, their balance sheet will collapse because of the value of their assets.

What’s even worse is they will be left with only one option: sell their corporate debt at any price to buy the T-Bills they’ll need to trade in the repo market.

This example allows us to understand the importance, not only of the cash side of liquidity but of the collateral side.

Here’s another example.

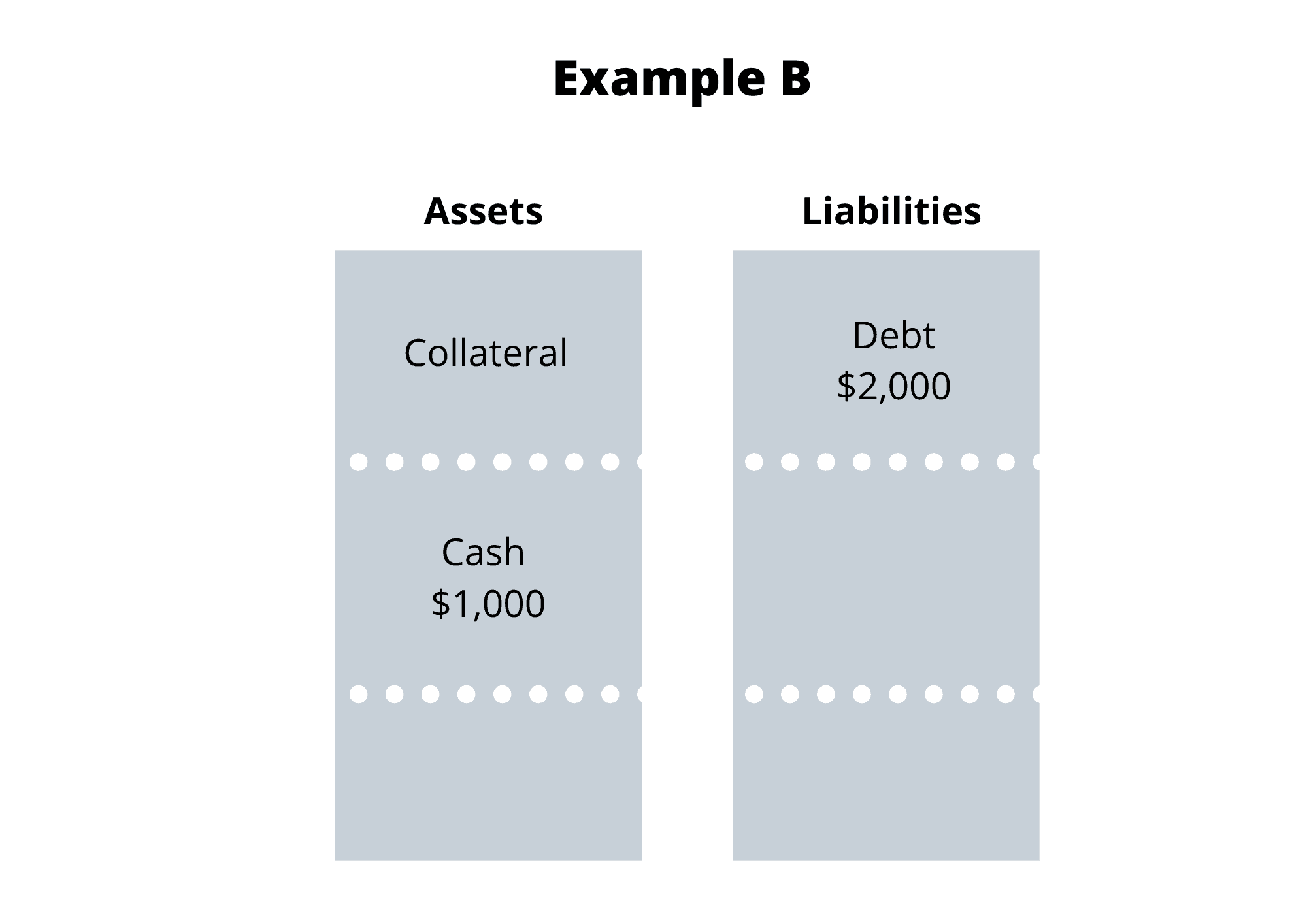

Example B

We have a typical business balance sheet, a very simple one with two sides: the assets side and the liabilities side. The first one, for this example, includes collateral, $1,000 in cash, and the second one, a debt payment of $2,000.

Let’s pretend this business has a customer who owes them a thousand dollars while they have a coming $2,000 debt payment.

If the customer doesn’t make the payment in time, to meet this liability the company has to go to the repo market and borrow $1,000, in other terms, liquidity, in exchange for their collateral.

This way they would have the liquidity needed to make the debt payment, so when the customer makes the payment owed to the business, the company will go to the repo market again, pay the $1,000 and take the collateral back.

This is the ideal scenario. The opposite, and bad one would be if the company only had a thousand dollars and there was no liquidity available for them, meaning they wouldn’t be able to make the debt payments, and in the long run, potentially go bankrupt.

In other words, if there’s no liquidity for the businesses, the financial institutions, hedge funds or banks, they’ll all go bankrupt very quickly.

This example, different from the first one, shows us the importance of the cash side of liquidity, where a company isn’t able to access the money needed to meet its liabilities.

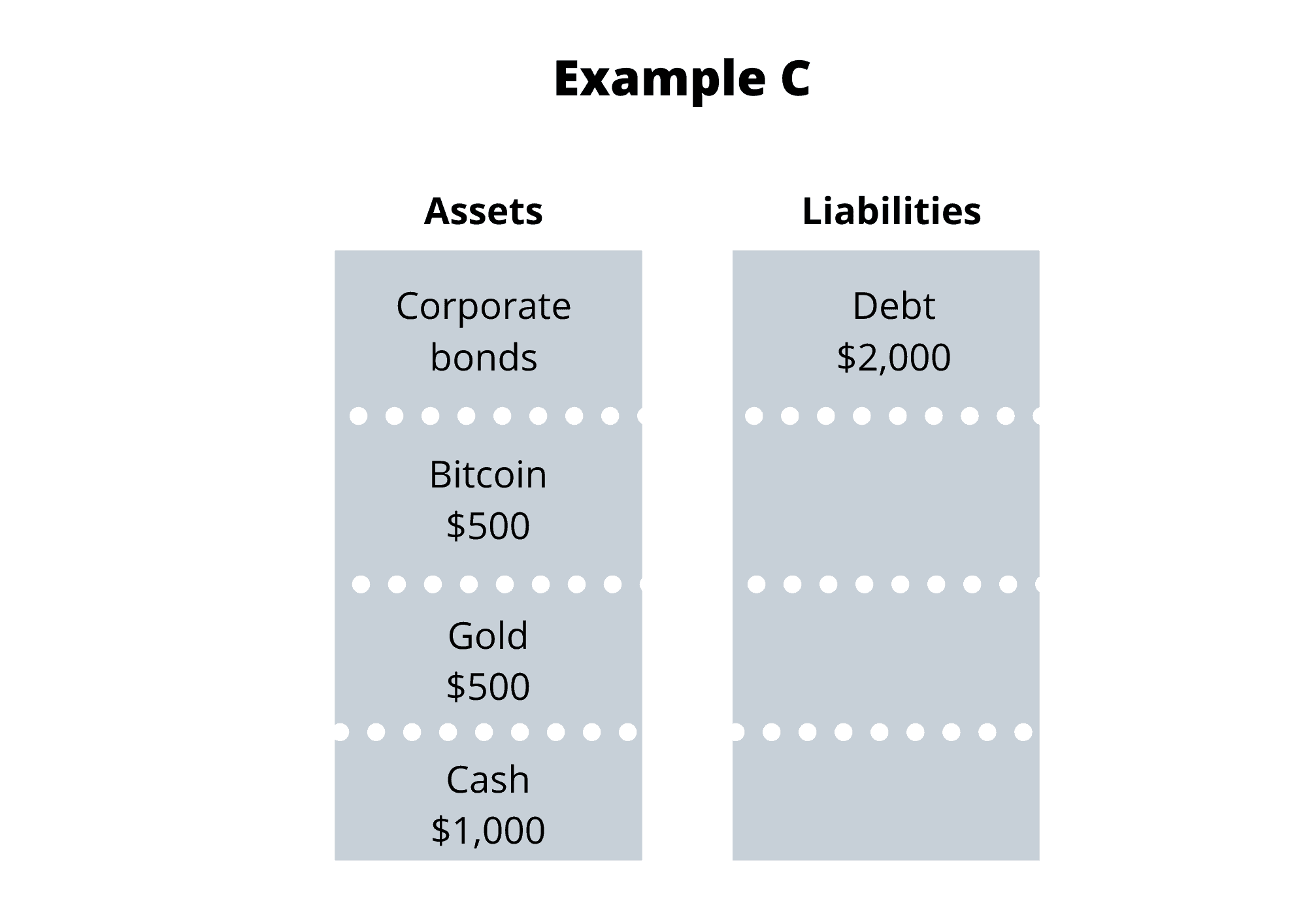

There’s one more illustration I want to use to explain why in the midst of this crisis, gold and bitcoin, even though they’re liquid assets, have tanked.

Example C

We have an entity owing $2,000 of interest payments, but their assets include corporate bonds, which we now know are persona non grata because the corporate bond market has collapsed, $500 in Bitcoin, $500 in gold and $1,000 in cash.

This means they need an extra $1,000 of liquidity to make their debt payment, to do so they’ll have to sell off their Bitcoins and gold in exchange for cash, and with it buy T-Bills for the repo market.

This means they need an extra $1,000 of liquidity to make their debt payment, to do so they’ll have to sell off their Bitcoins and gold in exchange for cash, and with it buy T-Bills for the repo market.

Why not just use the cash they received when selling their liquid assets?

Because believe it or not, T-Bills are more flexible and valuable than cash.

If the entity goes into a negative equity position, with the T-Bills they won’t have to lose them into the repo market, because the collateral stays on the balance sheets of the borrower, not the lender.

The net result at the end is, because of all the additional buying of treasuries and selling of Bitcoin and gold, T-Bill prices will go up while the rest of the mentioned assets go down.

Now, before I continue to answer our main question, we have one more thing to understand and that’s liquidity.

Repo market and its liquidity

In the previous examples, I illustrated two problems of liquidity, which are its main components: cash and collateral.

The cash component is the one on which everyone’s focused on, including the Fed, and the collateral is the component nobody’s paying attention to.

When we look at the repo market we see there are two assets being traded from counterparty to counterparty, not just cash but also the collateral.

The Federal Reserve could print trillions, even quadrillions of dollars and deposit them into their primary dealer’s reserves, but, if there’s no collateral in the system, there still won’t be any liquidity in the system, it will be stuck with the Fed.

There are a lot of smart people on Macro Voices and Real Vision who think the collateral is the real problem of liquidity.

They’ve even pointed to charts of pristine collateral where it's evident the price has continually gone down over the past two weeks.

Look at this pristine collateral chart of three-month T-Bills:

Also, it’s important to mention there are two types of treasuries we need to be cognisant of: On the run and off the run.

In George Goncalves' words, professional bond strategist, the on the run treasury bonds are the most liquid, the most actively traded.

They’re usually issued every month or on a quarterly basis, and they’re usually the liquidity premiums because they’re traded very quickly between parties.

The price of the on the run bonds is higher and the interest rate is lower compared to the off the run treasury bonds, which are held in portfolios of private individuals. These two generally have a spread of 14 basis points.

But, again, why is all of this so important?

Back in 2008, when Lehman Brothers failed, the basis points spread between these two types of bonds spiked all the way above 60 basis points.

This tells us there was a huge premium for the treasuries that was the most liquid because there was a big demand for them in the repo market.

Taking this back to today, we would have to ask: What was last week’s spread between the two with all these problems?

Answer: 50 basis points.

Almost as high as the spread was when Lehman Brothers collapsed.

Because the liquidity premium was so high, they were able to notice the massive amount of demand for the most liquid asset on the run treasuries.

If we now analyze the Fed’s actions, we can also see they’re also extremely worried about a lack of collateral, because as I said before the Fed is currently buying $60 billion worth of short term T-Bills per month.

Aside from this, they’re also supposedly buying short term, overnight and term repos, but the purchases of the T-Bills are being parked on their balance sheet. This means the Fed is taking all the best collateral of the repo market.

They finally realized, in my opinion, the unintended consequences and came out last week with the announcement they are transitioning from short term T-Bill purchases to the entire yield curve.

In other words, the Real Vision and Macro Voices guys, along with Jeff Snider weren’t the only ones worried about this, but the Fed as well.

The liquidity problem is not just about cash, it is even more so about a lack of collateral.

Finally, we’re one step ahead of resolving the question of how does all of this affect us and the answer is in the solution.

Repo market solution = A bigger problem

The Fed can only create reserves, it can’t create additional collateral. The only entity able to do the job is the government.

Insolvent uncle Sam can create all the additional T-bills needed for the repo market but only by doing deficit spending into the real economy, in other words, we get into MMT and helicopter money.

Also, we know well inflation equals the money supply plus velocity, but there’s one thing I haven’t talked about and that’s Coronavirus. This crisis could reduce the money supply dramatically.

But even if velocity goes down or remains consistent, if the amount of money supply is going down at a faster rate, we still could see price inflation.

The yield curve is what the Fed and the government have to pay a lot of attention to because there’s a distinct line in the sand they can’t cross.

They can’t allow the 10-year treasury’s interest rate to exceed the line because if it goes that high it wreaks havoc on the economy.

The 10-year interest rates will start to go up because of the inflation created by the government spending money into the real economy through MMT and helicopter money.

But, that’s not all, the government is also the largest subprime borrower in human history and he doesn’t have a 30 year fixed rate loan, rather it has an adjustable-rate mortgage, so most of their debt is very short term, meaning they would have to roll it over and over on a yearly basis.

Today they have 23 trillion dollars in debt, but with their deficit spending, it will go from 23 trillion to 30, 40 or who knows how high it would go, and it will require for the Fed to keep rates in the short end of the yield curve as low as possible so the government can continue to roll over the debt without imploding.

The takeaway is the Fed would not only have to buy the short end of the curve, but they would have to buy the entire curve taking their balance sheet from 4,5 trillion to 10 trillion and to infinity and beyond.

The bottom line, and the answer to our main question (finally), is in the next three to six months we’re most likely to see prices of things such as food, going up, prices on higher ticket items like cars going down, and prices of assets, including treasuries, going down.

There are no certainties, only probabilities, but in my opinion, this is what’s most likely going to happen.

For more articles like these and to go further into what's happening to our economy, take a look at my previous blog.

See you on the next one!