It’s true the market has crashed, but have we reached the bottom yet? My short answer is “NO”.

To determine how much more downside is in the stock market, we have to ask ourselves if the stock market is cheap or expensive, historically speaking.

Is it the already the perfect time to buy? Many are asking. Well, let’s dive in and see!

In this article, I will start by analyzing the stock market capitalization to GDP ratio to determine if the overall market is undervalued or overvalued compared to a historic average.

I’ll also analyze the CAPE ratio to comprehend where we’re at today and explain the math behind buying cheap and buying expensive.

Stock market crash analysis part I: Market cap to GDP ratio

In order to determine the downside of the stock market, we need to examine, as I said if it’s cheap or expensive by having a historical context.

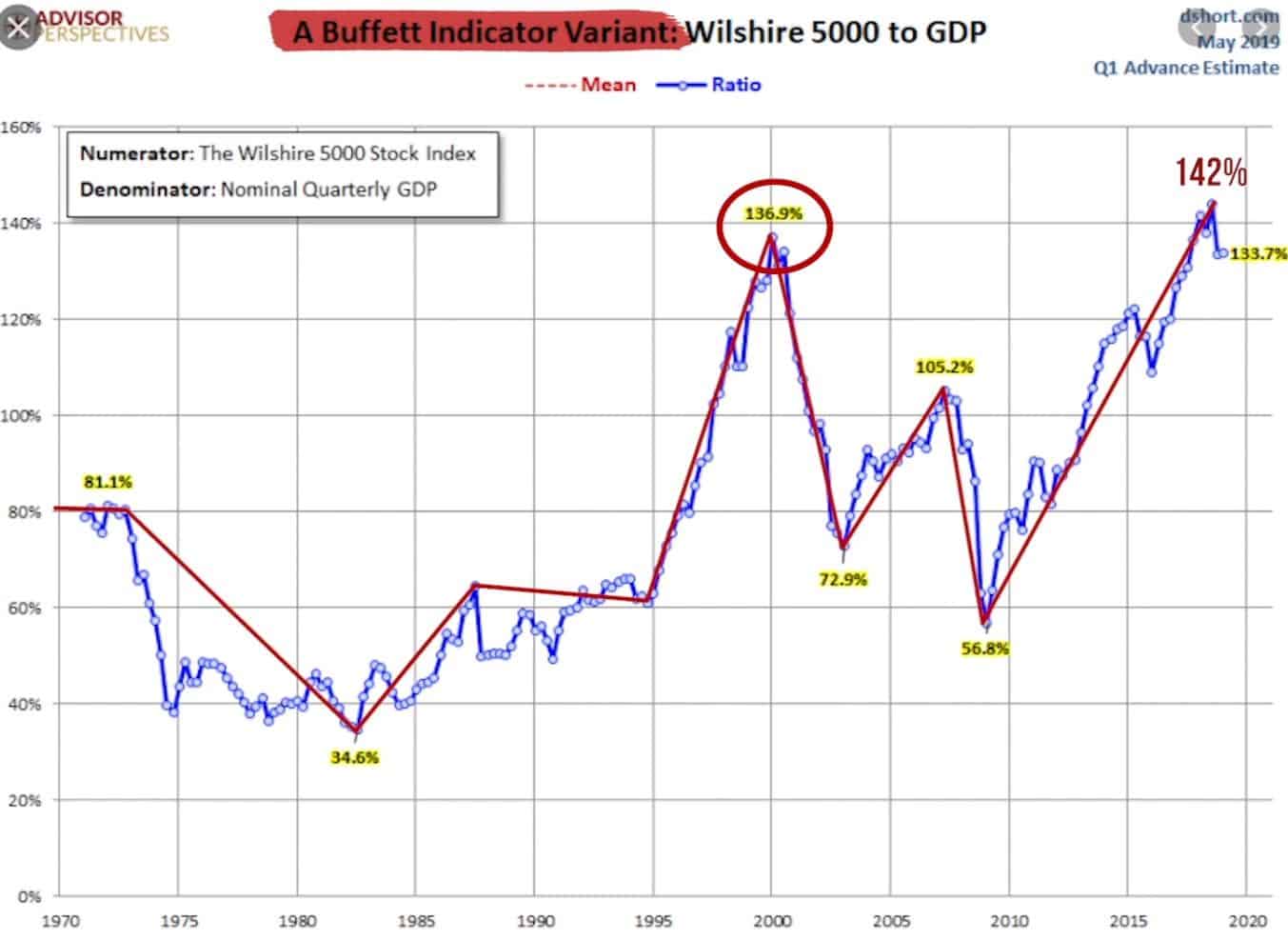

To do so, look at this chart. Keep in mind I’ll be talking about the broad market as a whole.

On the left, the percentages go from zero to 160% market cap to GDP, and it starts in 1970 all the way to 2020.

In 1970 it went down around 8%, but then it came crashing to an all-time low in 1982 where it was very cheap, reaching 34%.

After this, it went up a little in 1990 and it stayed flat until 1995 when it went parabolic to the huge dot com bubble we had in 2000.

It crashed again and went back up when the Fed inflated a bubble. This bubble deflated and came down in 2009 to 56%, again, very cheap.

Yet, the Fed came with quantitative easing, ZIRP, money printing and so the stock market went up to an even higher level than when it was in 2000, it went up to 142%.

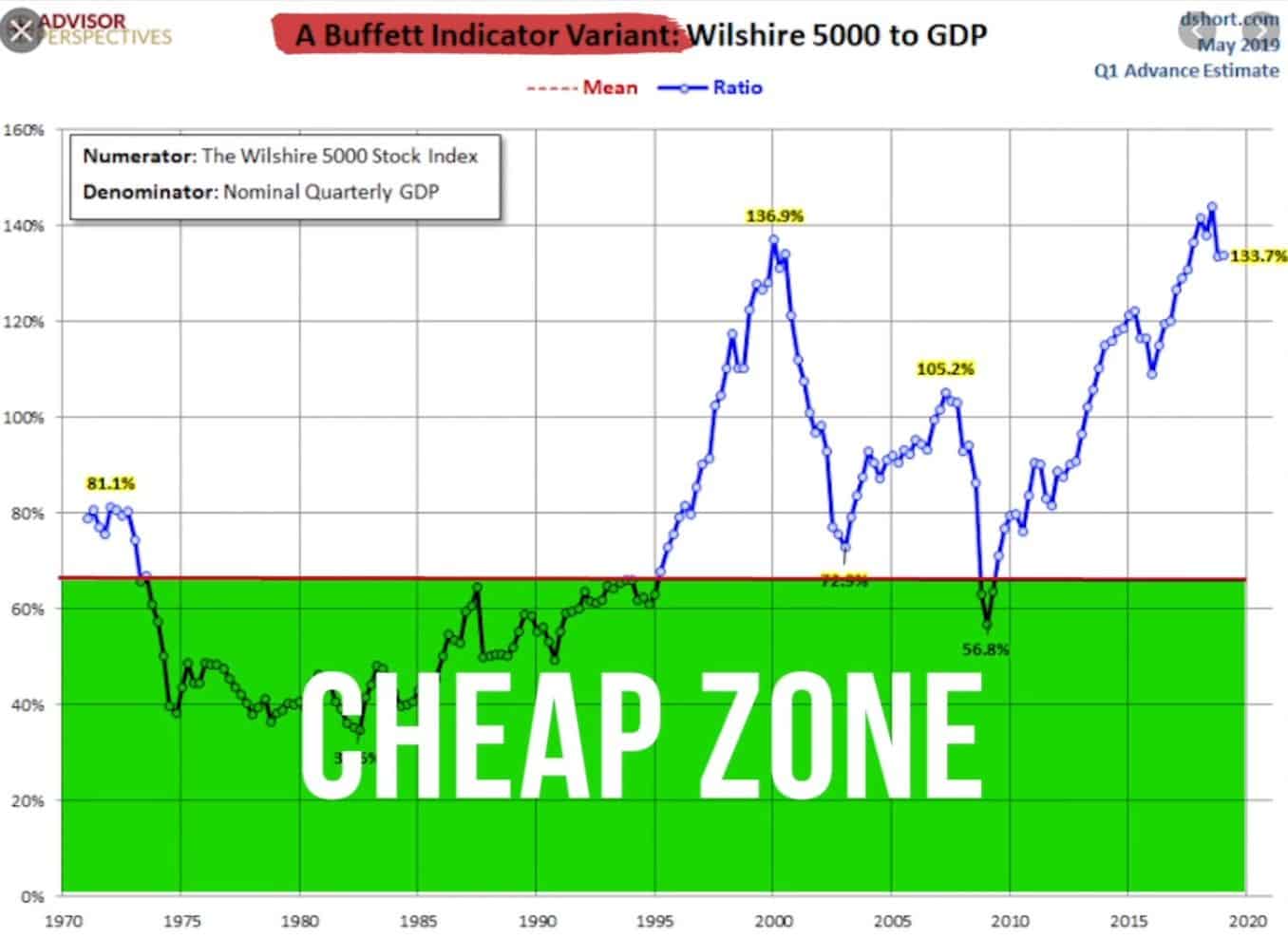

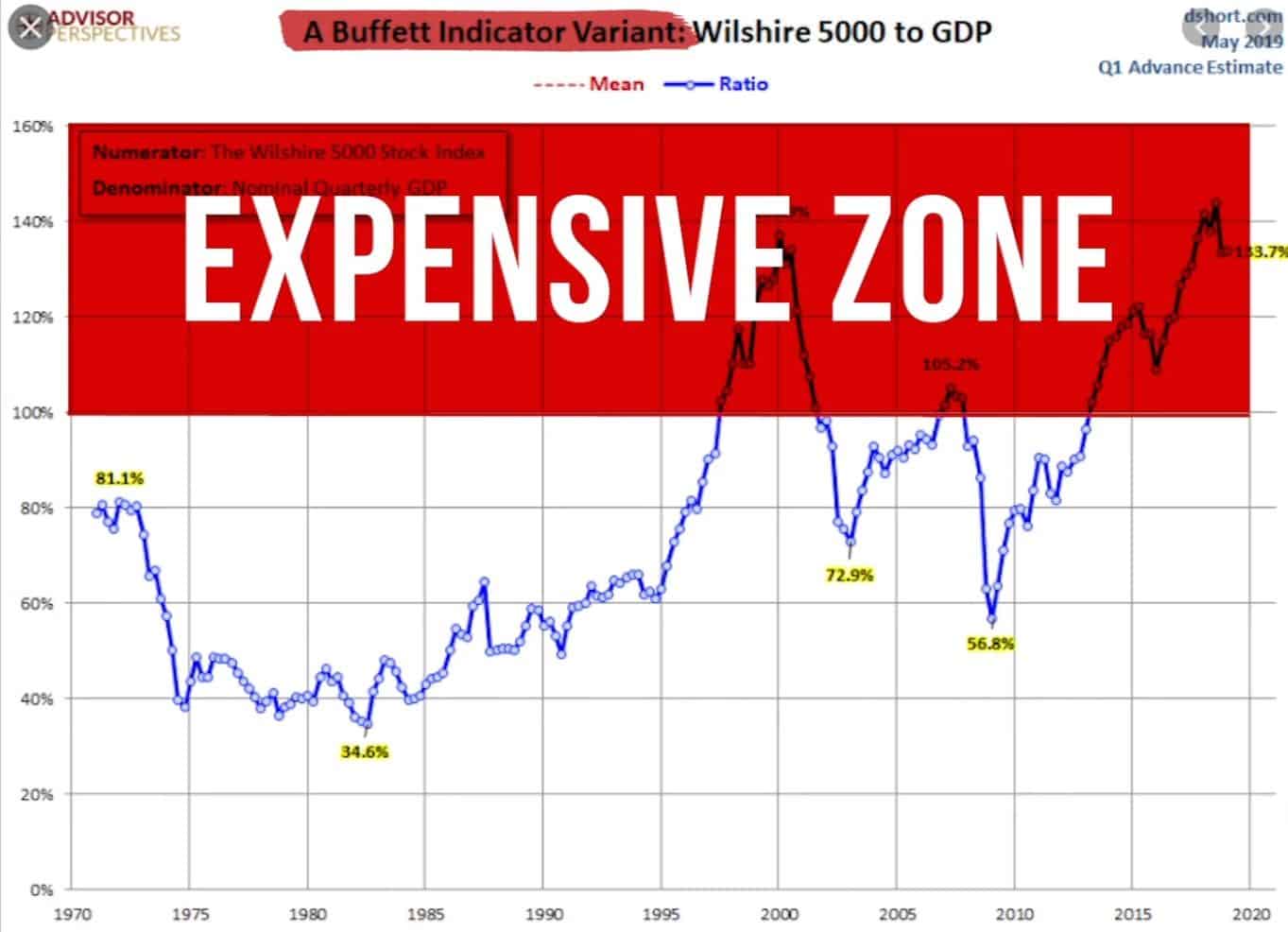

To understand what I mean by cheap and expensive, look at these divisions. Anything below the line shown in the image, it’s the cheap zone.

Anything around 100% and higher, it’s the expensive zone.

Also, anything above 120%, in my opinion, is in the “no bueno zone” because it means we’re in a bubble.

Being in an all-time high, or maybe, in an all-time low, doesn’t necessarily mean and individual stock or asset, is cheap or expensive, remember we’re talking about the broad market.

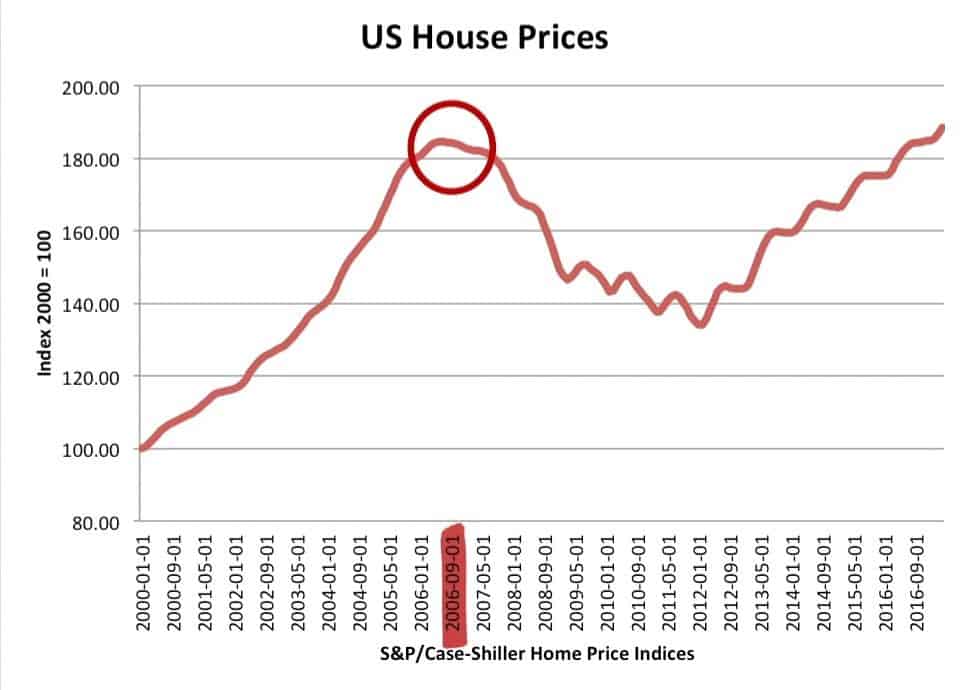

For example, the top of the real estate bubble was in 2006, and it bottomed out in 2012, but, if anyone could’ve had a 2012 type of deal in 2006 or 2020 when the market was just as high, you should have pulled the trigger, immediately.

Likewise, if we were in 2012 and saw a massively overvalued property, it doesn’t mean the individual asset was a good deal just because the market was “cheap”, “expensive” or even in a bubble.

See where I’m heading with this?

Now, taking this example one step further to prove another point, let’s look at this chart where you’ll see home prices peaked out in 2006 when we were in a massive bubble.

No one would dispute we were in a bubble, yet, prices in 2020 went up just as high, if not higher than in 2006. So if we were in a bubble in 2006, how are we not in a bubble today?

The exact same thing applies to the Buffett indicator.

If we were in a bubble in 2000 and no one would deny it, how were we not in a bubble, two months ago, when the market cap to GDP was even higher than it was in the dot com bust?

Jim Chanos from CNBC puts it this way.

“Every idea stands on its own merits, and valuation is an important part of it.

So if valuations are down, then we’ll be less likely to do something.

Having said that, as I said at the outset of our conversation, there’s a lot of situations where the valuations are still excessive and kind of shockingly so.”

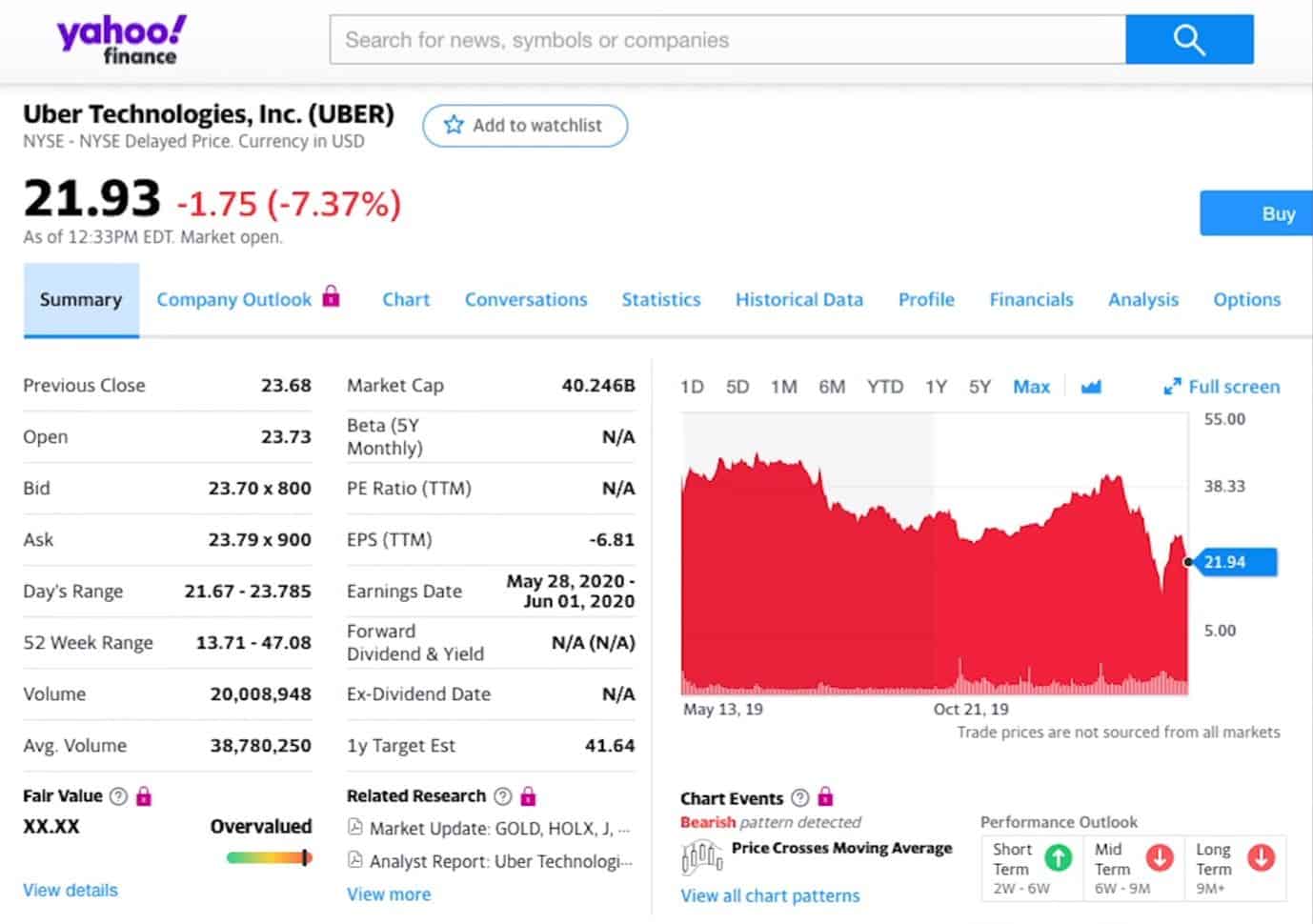

To understand what Jim Chanos is saying, I’ll give you an example with Uber, look at its chart.

Last week, their stock was trading around $21.93, about half of its all-time high.

You may think because it has come down a lot, now it’s cheap, however, please take a look at its earnings per share.

It’s minus $6.81! And if we look at their earnings, they had $14 billion of revenue in 2019 while losing $8.5 billion.

How is it possible to incinerate that much money?

Even though this company has lost a massive amount of money and will most likely struggle to go into a recession or depression, we still see the market cap is $40.24 billion.

How is it possible for a company to have such a market cap, when in 2019 they made the most revenue ever, lost over $8 billion, and will most likely struggle for the next six months?

Uber is an example of an individual asset that didn’t go cheap even though the share price and the market went down.

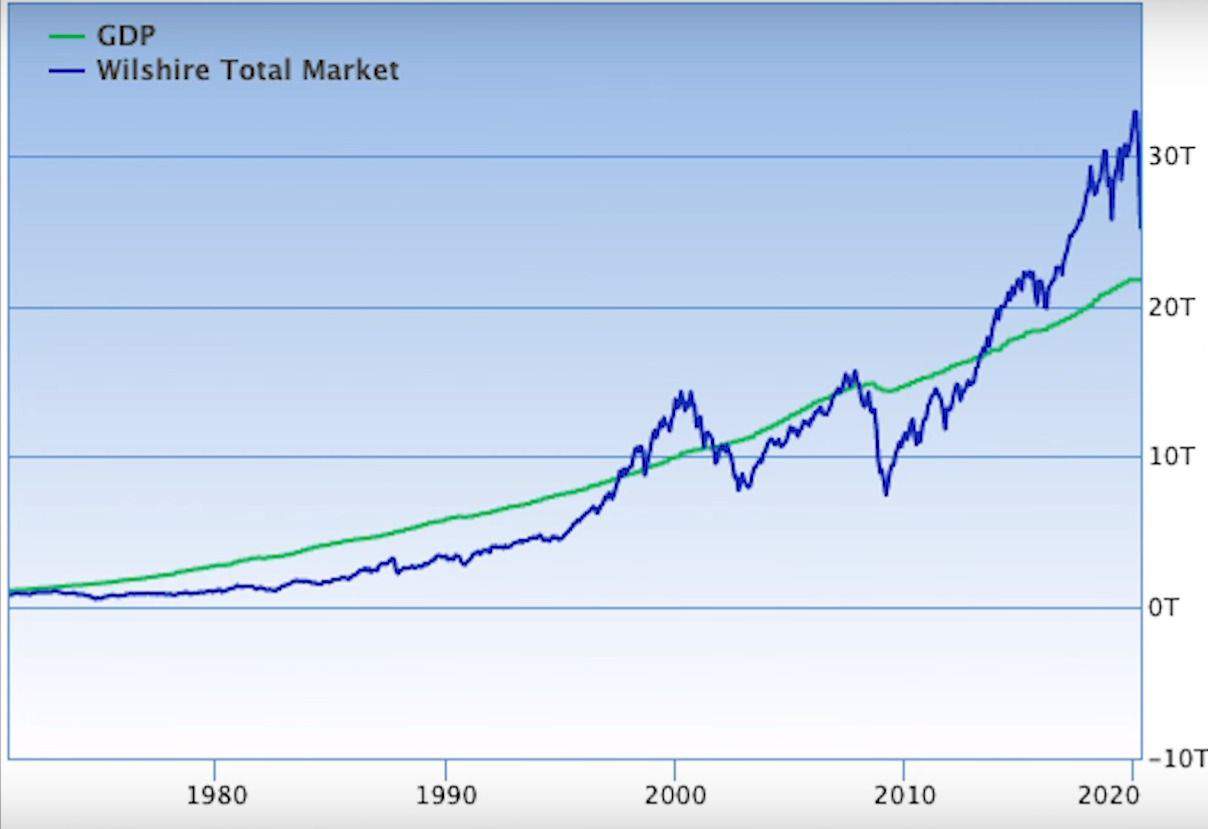

After this being said, I want to show you another way of looking at the Buffett indicator.

Notice instead of seeing a percentage in this chart, we see two lines. The green one is the GDP, and the blue one is the market cap of the stock market.

When the market cap is below the GDP, its usually cheap or at least reasonably priced, but when the market cap exceeds the GDP substantially, it means we’re in a bubble.

So far we have analyzed the market cap to GDP and learned new ways of looking at the indicator, but, where are we today? What’s our current situation?

Look this image.

As you can see, we are at 116%, still not anywhere close to cheap. In fact, according to the website Gurufocus, the stock market is still significantly overvalued.

If we look at the current market cap to GDP of 116% and extrapolate it into the future, to see what are the expected returns over the next decade, it’s likely we’ll only see a return of 1.5% a year from this valuation, including dividends.

As pointed out by Warren Buffett, this chart “is probably the best single measure of where valuations stand at any given moment”, which is why it’s very important we have this historical context.

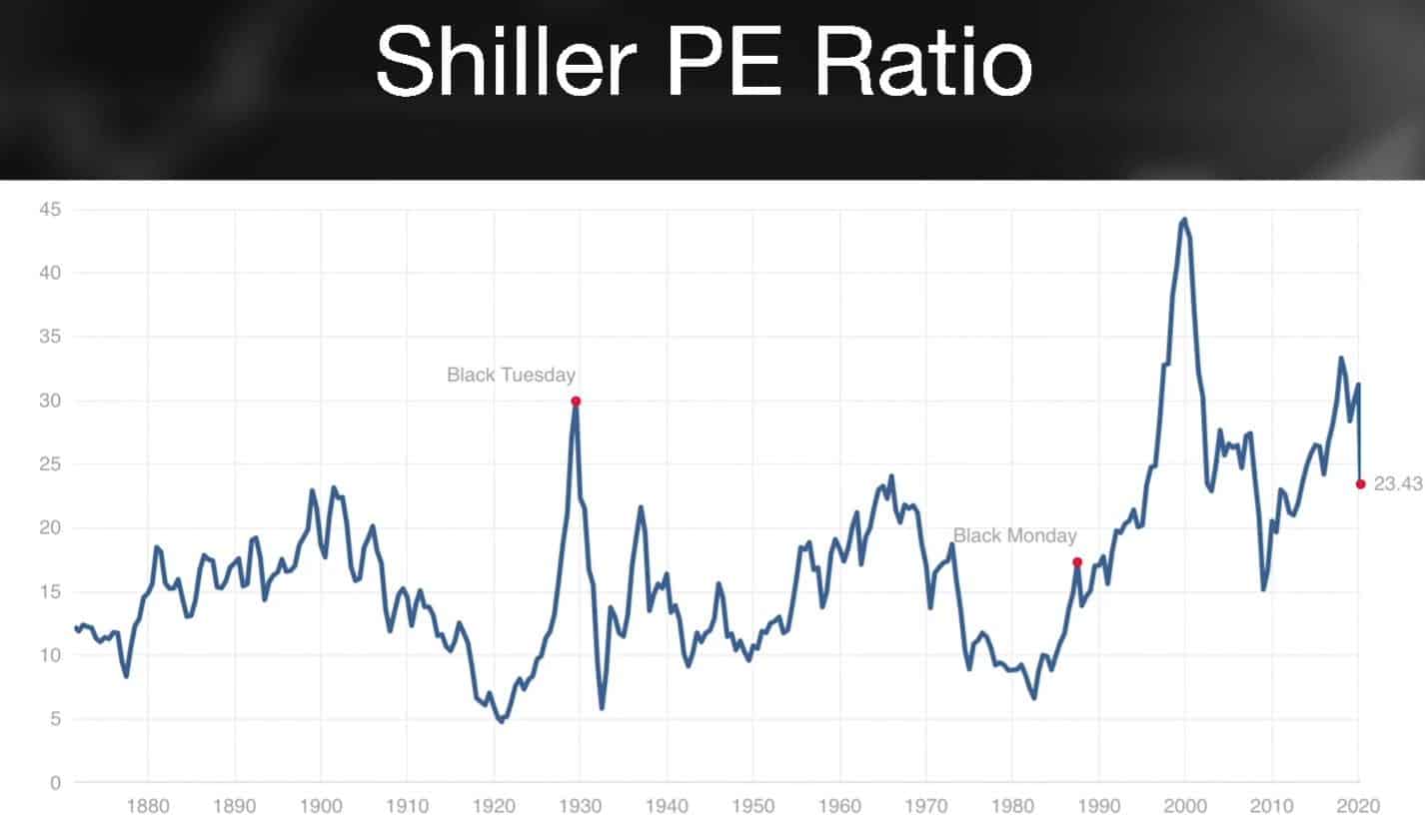

The stock market crash analysis part II: The CAPE ratio

I know we’ve examined many charts, but it’s extremely important we continue to do so, especially this one because it adds a lot to our thought process when looking at the market cap to GDP ratio.

Here I present to you, the CAPE ratio.

On the left side, the price to earnings ratio goes from 0 to 40, and it starts in 1880 all the way to 2020.

Anything above 15 or 16 is most likely getting into the expensive zone, and anything below its cheap. This means around 17 its okay, but once it’s above 20, it starts to get expensive, and above 30 its a bubble.

On the flip side, if it’s around 14 it’s not as bad, but once it gets down below 12, it’s very cheap, and if it gets anything below 10, we need to back up the brinks truck.

Today, we’re at 23.8 which is definitely expensive, but keep in mind this is all the way down from plus 30 back at the peak, so it has come down dramatically, however, 23.8 is still expensive.

We’re nowhere near cheap, but I think the business climate will be far less friendly because we’ll have a lot more regulations in the business environment.

What do I mean by this? Jim Chanos explains it very well.

“I think the gig economy companies are going to come out of this harmed, not enhanced. I know there’s a body of thought that everybody will just do food delivery, take Ubers and no one’s going to buy a car again. But, I think the flip side of it is the labor pool issue for the gig economy companies is going to loom very largely, coming out of this crisis.

Keep in mind we as taxpayers are paying the unemployment benefits for a lot of drivers of Uber, Lyft, GrubHub, and so on, but the reason we’re paying it is the companies themselves never paid into the unemployment pools.

It’s the whole idea of keeping people as independent contractors rather than employees.

I think both political parties are going to be looking at it coming out of this crisis to enhance corporate responsibility in lots of different ways.

Whether it’s keeping employees as independent contractors or its restricting buybacks.

There are a lot of issues we haven’t thought through, yet, I think it will make a difference to U.S. businesses”.

We’ll have a lot more regulations in the business environment and there will be fewer buybacks, which was the main driver of the stock market getting to an all-time high since 2010.

So the question now is, once we go through six months, or a year of dealing with the pandemic, how many individuals are going to want to go out, take their savings, start a business and risk it all?

It’s the SMEs who drive this economy.

Maybe a lot less than we had in 2019, which means we’re going to be in a much less dynamic economy, making the 23.8 on the CAPE ratio seem even more expensive.

Stock market crash analysis part III: Is it time to buy?

We know the stock market is still extremely expensive, and we most likely haven’t seen a bottom, but, does buying things when they’re cheap matter?

To find out I invite you to read one of my blog posts from 2019 called Actionable 100 Year Analysis Of S&P 500: What's the best.

The article is about a study I made where I compared buying in the market when it was cheap, and buying when it was expensive.

The numbers I crunch are a compound annual growth rate, not the annual rate of return.

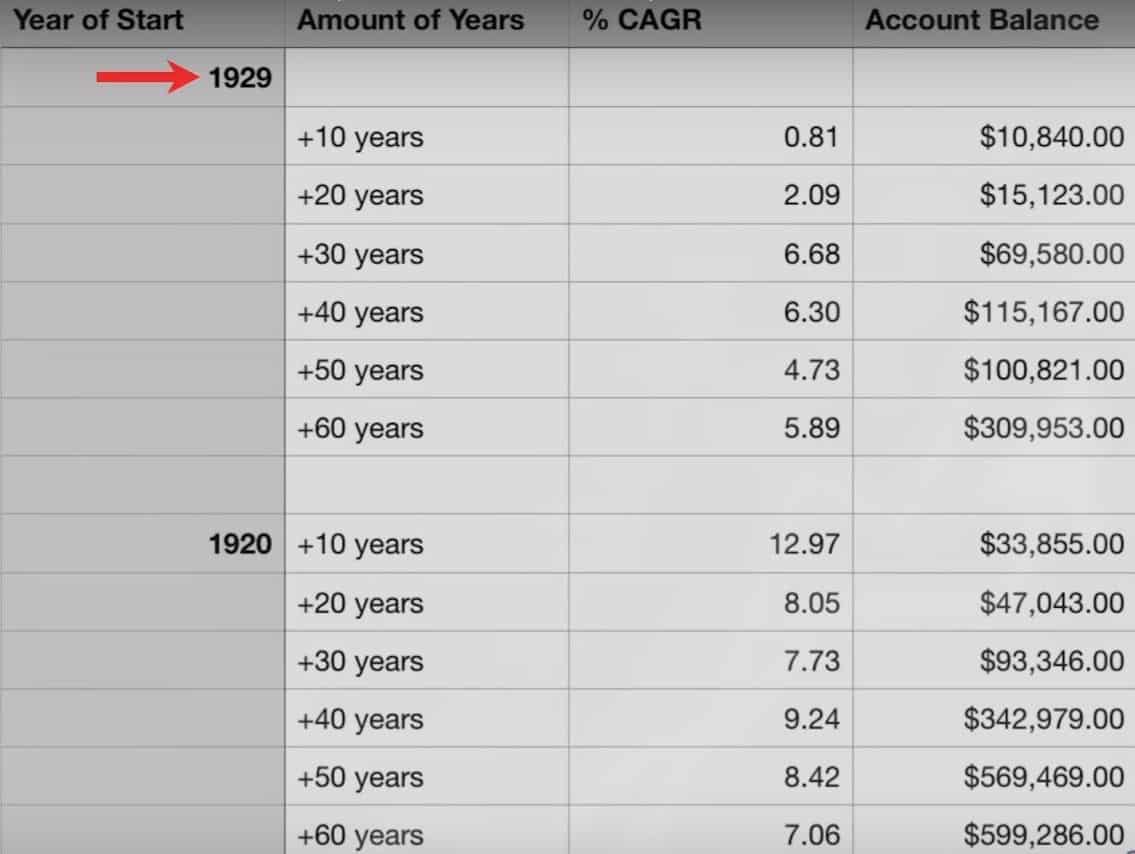

I analyze this spreadsheet starting in 1929 where it’s assumed someone invested $10,000 adjusted for inflation and it adds dividends at the end of 10 years.

In 1939, the compound annual growth rate would’ve been 0.81% and the total balance, $10,840.

You can see how it changes from decade to decade, and at the end of 60 years, there will be $309,953.

Doing the exact same thing but starting in 1920, which was low on the CAPE ratio, instead of one of the all-time high, after 10 years, the compound annual growth rate would’ve been almost 13%.

The original investment of $10,000 would have grown to $33,855, and the compound annual growth rates would’ve been much higher if you compare them to the 1929 case, which was when the market was extremely expensive.

At the end of 60 years, instead of having $309,953, they would’ve had almost $600,000.

This is just one example of when its better to buy low and sell high than to try to buy high and sell higher.

So if you have a diversified portfolio where you don’t have all your eggs in one basket, and buy things when they’re cheap, most likely in the long run, you’re going to do well.

In conclusion, whether you’re buying in the broad market or an individual asset, make sure you’re buying things when they’re cheap and selling them when they’re expensive.

The overall market, right now, is extremely overpriced, so in my opinion, we haven’t seen the bottom in this bear market.

Yet, keep in mind I could be completely wrong! The Fed could come, buy every single stock in the entire S&P500, buy every mortgage and bond, and prop up the price to infinity and beyond.

Let me know what you think in the comments below.

See you on the next one!