We know what has happened to the Stock Market with this Fed-induced Bubble. It just keeps going up and up, but what's more important to everyday people like you and me is Mainstreet. Not Wallstreet.

And you know just as well as I do, that when you're walking around and seeing all the restaurants and other businesses closed, that although Wallstreet may be going parabolic to all-time highs, Mainstreet and the real economy are really suffering.

The question I address during this article is:

Will the economy recover?

I offer a shocking answer and some solutions.

What Made The Economy Break?

What made the economy break in the first place?

There's a lot of misconceptions around this.

Most of you would say, “George, the economy was structurally flawed, to begin with. The coronavirus was just the straw that broke the camel's back.” I would totally agree, but I think we've got to dig deeper.

At the surface level, you can say the things that created this structurally flawed and very fragile economy were things like government spending, regulations, quantitative easing, and artificially low-interest rates.

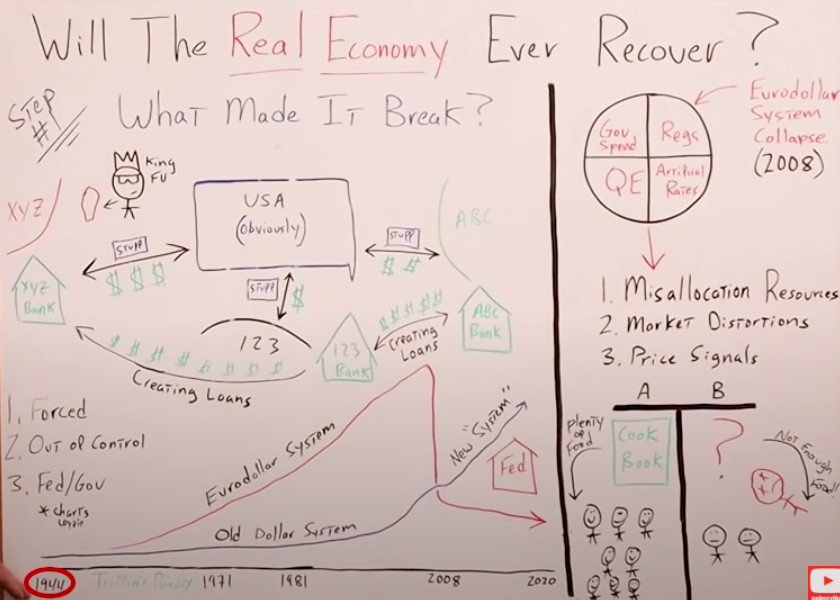

But if we keep digging deeper and really get to the core of the problem, I think Jeff Snider is right and it's actually a result of the Eurodollar system collapsing in 2008.

Because the central planners had to come in with the spending regulations, artificially low-interest rates, QE infinity, and all the money printing we know so well.

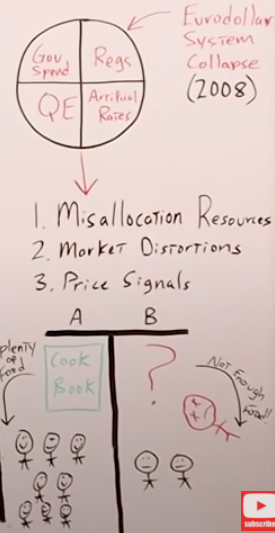

Look at the circle of doom I drew. I call it the circle of central planning doom with four quadrants.

We see this at surface level, but as a result of all of the central planning and tops down micromanagement of the economy, we have:

- Misallocation of resources

- Scarce resources with alternative uses, going right back to my favorite economist of all time, Dr. Thomas Sowell.

- Massive market distortions because there are no price signals.

The easiest way that I can describe how a misallocation of resources distorts the entire economy and makes it much more fragile and structurally unsound is by using the analogy of making food.

Look at the bottom example of the whiteboard I just showed. There is option A and option B. In option A, the people doing the cooking have a cookbook and limited resources.

Let's say the recipe is Pizza and there is a limited amount of flour, cheese, tomato, and sauce. Therefore, we have to maximize every single ingredient we have because it's a scarce resource.

If we have a cookbook, we know that every single pizza we try to make is going to come out really good and we are going to have plenty of food to feed all of the people.

But if we have no cookbook whatsoever, meaning we don't have any price signals from the free market, because of the distortions the central planners are creating by micromanaging the economy, it's just like trying to cook without that cookbook.

Therefore, we have a lot of pizzas that we try to make but we don't know what we're doing so we have to throw most of them away.

There's not enough food and we get fewer people fed.

The bottom line is if you have individuals at a local level making decisions on a daily basis, buying and selling goods, creating more goods and services based on what they see is demand in the marketplace, and pursuing their own self-interest and those of their families, you're going to utilize those scarce resources very well.

It goes back to the example that Milton Friedman always gave us on the pencil. Remember that?

How many people have to cooperate and how many resources are used just to create one simple pencil?

If we don't have those price signals, if the central planners are distorting everything and misallocating resources, then, we're not going to have enough food.

Resources are going to get wasted. The only way we can fill the gap is instead of feeding people, just have the Fed come in and feed them pure sugar. That's really the best example I can give you.

But let's move over to explaining the Eurodollar system so you can get your head around it and understand when it broke.

This is going to give us a key piece of the puzzle to answer the question:

Will the economy ever recover?

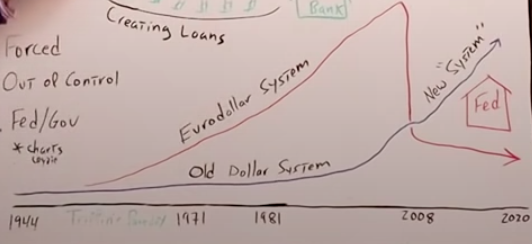

Look at the left bottom of the whiteboard. I drew a chart that starts in 1944, all the way to 2020. It's not entirely accurate, but visually you get the idea.

1944 is an important date, why?

You guys know, just as well as I do, that's when we had Bretton Woods. The dollar officially became the world reserve currency, but that created Triffin's paradox.

Triffin's paradox happened when the US had to create enough currency units for the global economy to function at a hundred percent capacity.

Therefore, if the United States wasn't creating enough currency units to satisfy the globe, we would have had a deflationary kind of death spiral.

If the United States creates enough currency units, then all of a sudden it's detrimental to the US economy because we have to run all of the trade deficits and it hollows out manufacturing.

It sounds familiar, doesn't it?

In the beginning, the United States wasn't exporting enough dollars, so the Eurodollar system took over. It really operated in the shadows.

This is how the Eurodollar system actually works. It sounds complicated, but it's not. Look at the whiteboard where there is a square representing the USA.

What happens is the United States imports a lot of stuff from other countries.

We'll call them countries “ABC” 123″, and “XYZ”, and a little island country on the left, I have no idea what the name is, but we'll say the leader of the country is King FU, the little guy with the crown.

I had to bring back everybody's favorite stick figure, King FU, the guy that gives the middle finger to the Fed all the time.

King FU needs some dollars for his corporations and his companies, but unfortunately, they're not getting enough dollars coming out of the United States.

Remember that when we have a trade deficit, there's more stuff going into the United States, being imported into the United States, than being exported to other countries.

Therefore, we run a trade deficit. What that means is the balance or the difference between what we import and export are currency units.

If we have $1 billion of imports, but we only have $500 million of exports, that means we have to come up with an additional $500 million in currency units to export out.

That's how the countries were supposed to get the dollars they need, but these countries were growing a lot faster than that, so they had to come up with a solution.

What the banks did in all of the countries was say: “Listen, we have dollar deposits and we can get rid of this fractional reserve thing. It really doesn't make too much of a difference because we need to generate tons of dollar-denominated loans. So since we have these dollar-denominated deposits, we'll go ahead and just create dollar-denominated loans.”

Effectively they're creating dollars outside of the system, again in the shadows. Nobody knows how many dollars they're creating, how exactly they're doing it, nor who is getting those dollars.

The dollar-denominated loans go back and forth from country to country, from corporation to corporation, and bank to bank. From ABC to 123, from 123 to XYZ, and back. On the board, the little dollar signs are representing US dollars.

There are only five of them coming out of the United States through the trade deficit, but there are a lot more dollars that have been created outside of the United States through the Eurodollar system and because of Triffin's paradox.

Now, this really goes into hyperdrive going back down to my timeline in 1971, when the dollar is removed from the gold standard. In my mind, I see it this way.

The blue line represents the old dollar system, and we'll call it M2 money supply or broad money. This line goes up and there is a little bit of a plateau in the GFC, but then it goes parabolic.

But the red line, the Eurodollar system grew much faster. It went up because it was picking up all the slack from the dollars needed that aren't coming out of the United States, so it's going up.

Once we got to 1971, it really started to get crazy. But in 1981 when we had a peak in interest rates, it created a lot of financialization, but now we've got a down cycle in rates for 40 years.

The financialization of the entire economy can happen because we're not on a gold standard. There's nothing restricting the amount of base money that we can create.

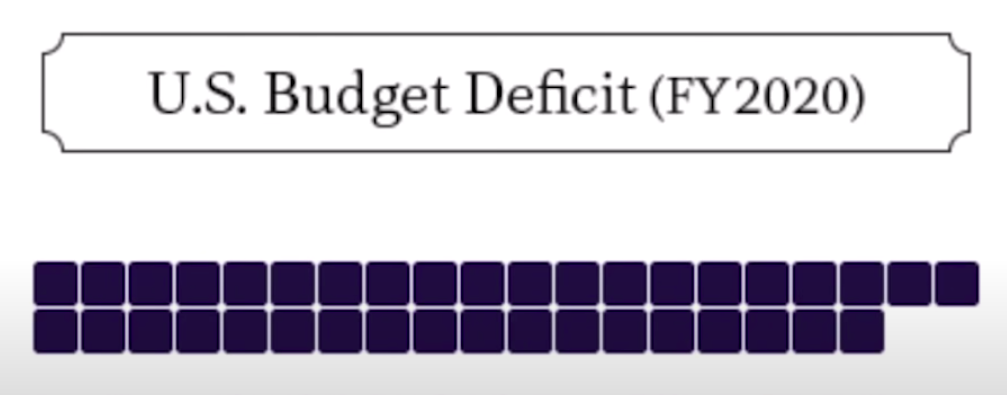

The Eurodollar system goes hog wild because they have nothing restraining it and we come up with all of these derivatives. Look at these amazing images from the Visual Capitalist.

This is a really cool visualization of the world's money and market.

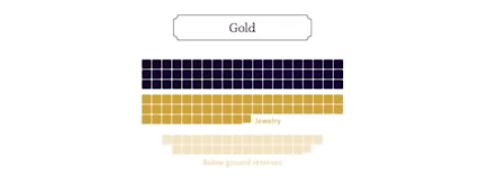

1. Silver

Start off by looking at how much silver is in the world, illustrated by one square, it says each one of the squares is worth a hundred billion dollars.

So there is about a hundred billion dollars worth of silver in the entire world.

2. Budget deficit just for 2020

That's a staggering amount, isn't it?

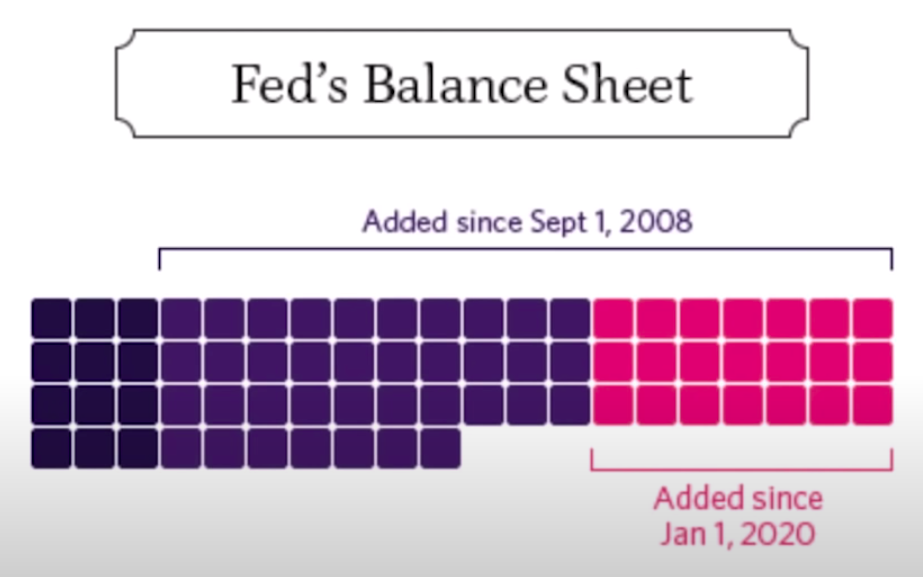

3. The Fed's balance sheet

I think it is really interesting that these pink squares show just how much has been added since January 1st of 2020. It's really mind-blowing when you think about it.

4. The amount of gold in the world

5. Global stock markets

5. Global stock markets

This is how they look as represented by a hundred billion dollar squares.

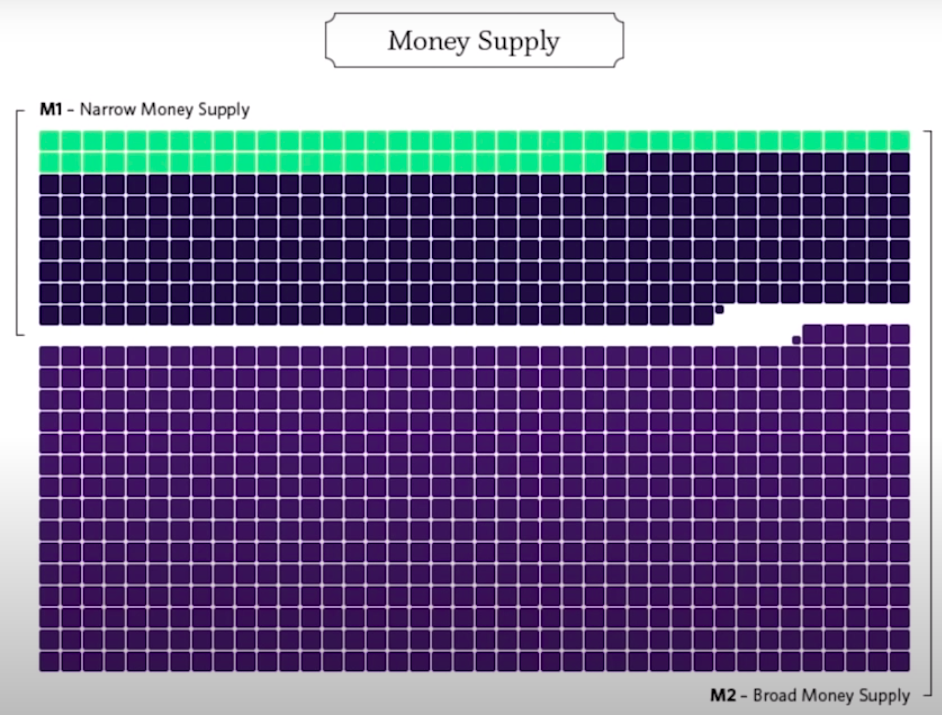

6. Money supply in the entire world, M1 and M2

Now, this is the way they measure it, and I would argue this isn't even close because of the Eurodollar system working in the shadows. At least prior to 2008, when it was functioning well.

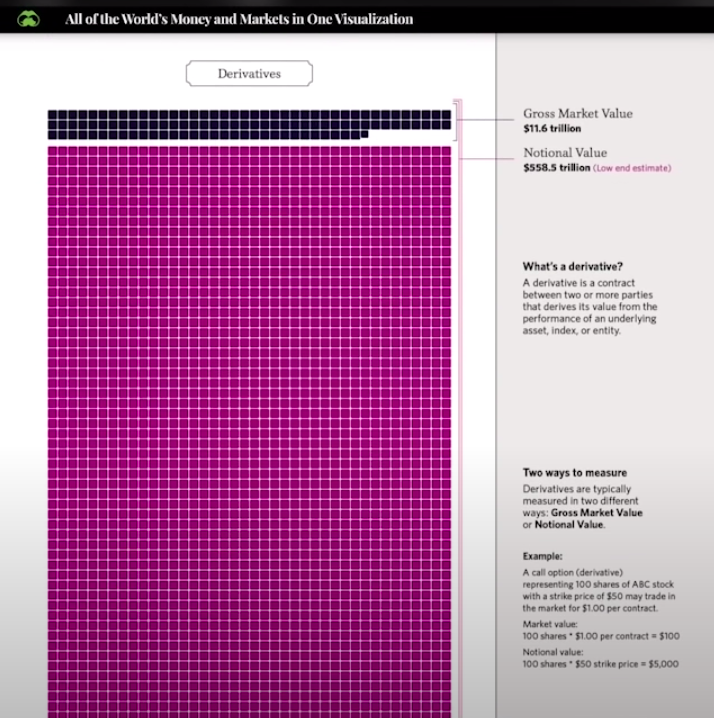

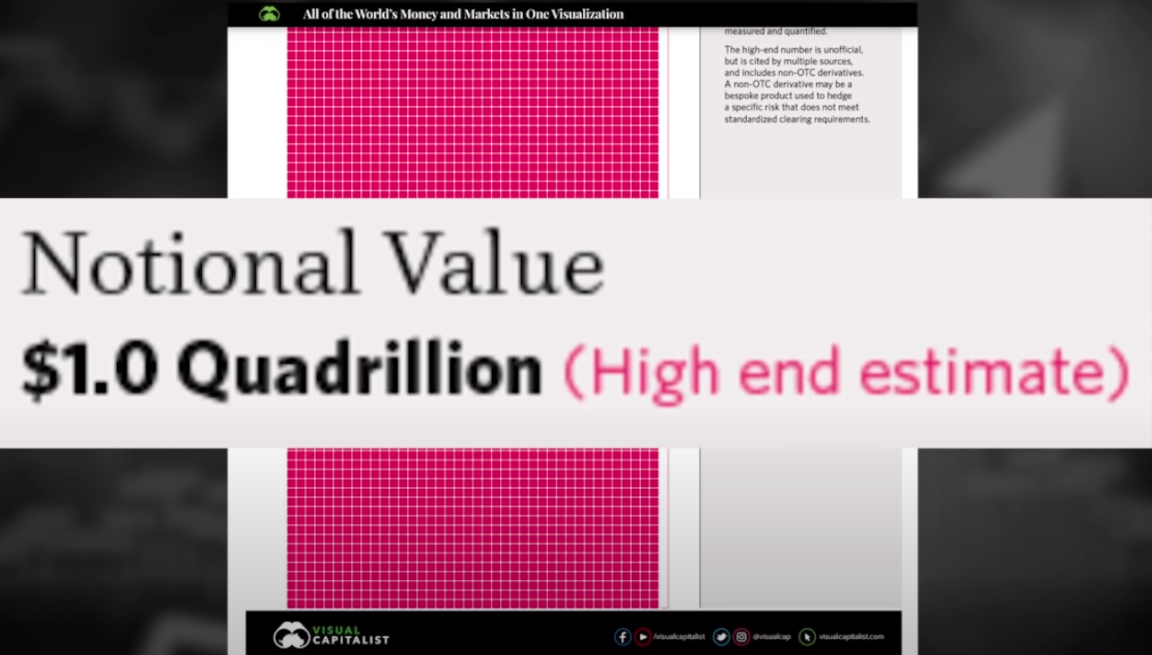

7. The derivatives market

In my opinion, this was the result of the Eurodollar system going completely haywire.

You saw a visual of approximately how much money is in the world, but look at the amount of derivatives.

The visual represented by these hundred billion dollar squares just keeps going and going. It never stops. You can keep scrolling down for five minutes before you get to the end.

You might ask: How much could this possibly be, George?

They say the notional value is one quadrillion dollars. Let that sink in for a while.

If I'm correct to assume these derivatives that led to the 2008 global financial crisis were a result of the Eurodollar system functioning the way it was prior to 2008. So, now, we can connect the dots and it takes us all the way back to 1944.

It shows us such a perfect example of why central planning and politicians, and the decisions they make, never seem to work out.

Because they can never get their head around the future unintended consequences that occur as a result of their good intentions in the present.

That is assuming their intentions are good and not malicious, and that's a completely separate whiteboard article that I'm sure would get me in hot water with all my new “best buddies” over at the BBC.

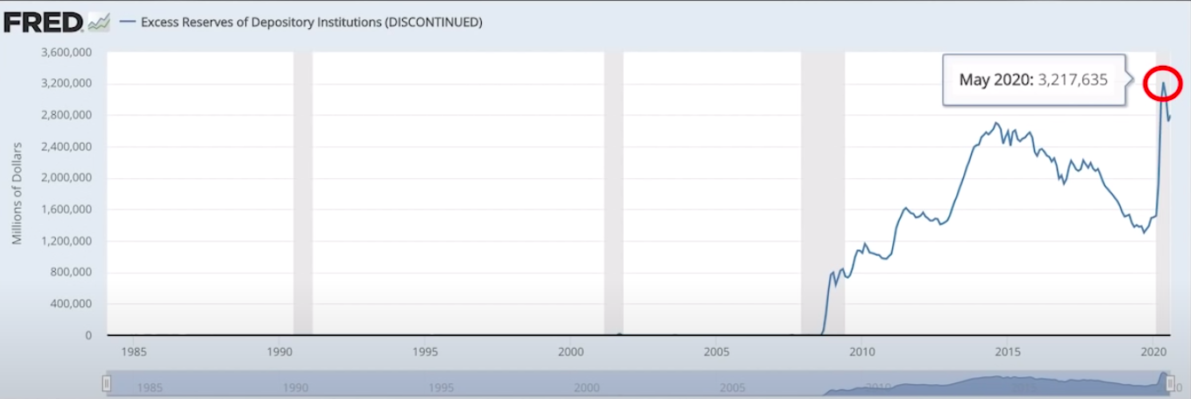

I also want to point out that the old dollar system was very efficient, and we can see this by looking at the excess reserves of the entire banking system in the United States held at the Fed.

This chart starts in 1985, but nothing happened until 2008, and that's not because there weren't excess reserves in the banking system.

That's because there was so little compared to today, we can't even see it on the chart.

Going back to 2005, as an example, you can see that the entire system functioned very smoothly with only $2 billion in excess reserves.

There's more than $2 billion in Jeff Bezos checking account that he forgot about. Can you imagine that? Look at this little teeny blip in 2001?

You can guess what that is. That was 9/11 when they “flooded” the system with reserves and it got them up to a whopping $20 billion.

Compare that to today, 2020, where we have $2.7 trillion, $2.7 trillion. Unbelievable.

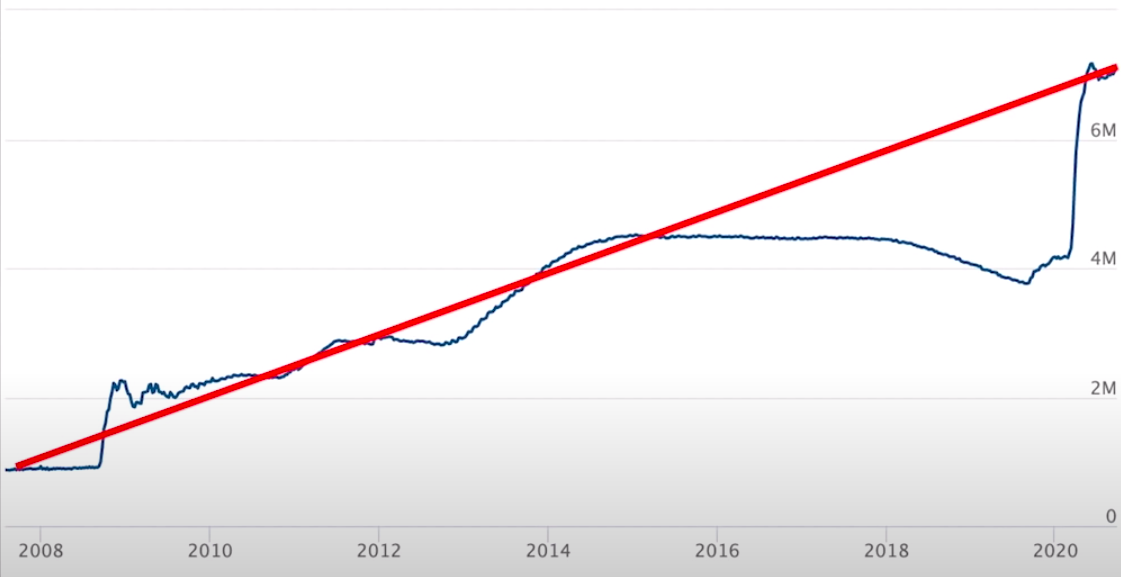

This is a perfect visualization of the Eurodollar system collapsing and the fed coming in to try to fill the void with all of their monetary sugar and heroin.

You can see that in 2008, the Eurodollar system had a Wile E. Coyote moment where they just ran right off the edge of the cliff and kept going until they looked beneath them and saw that there was nothing between them and the ground.

That's exactly what happened to the Eurodollar system that those politicians created all the way back in 1944, or maybe inadvertently created. We'll give them the benefit of the doubt.

Then the Fed comes in and tries to create a new system, or at least fill the void of the old system by money printing, creating additional bank reserves, taking their balance sheet from 800 billion all the way up to seven trillion where it is today.

You and I both know that's just a temporary fix. They're just kicking the can down the road while at the same time they're making the underlying economy that much more unstable.

Peter Schiff has the perfect analogy. It's the drug addict that goes into withdrawals, and you just give them more drugs to get them to buy. But you're not fixing the problem.

In fact, you're making the underlying issue that much worse. At the end of the day, you only have two options, either pay the fiddler or change the entire system completely.

Why The Problem Will Get Worse

What it boils down to is what my good buddies, Emil Kalinowski and Jeff Snider, always say on their podcast “Making Sense.”

The central banks aren't central. That's a key point.

Another thing that Lyn Alden, my partner in the rebel capitalist pro always likes to point out, and which I think is extremely true, is that central banks are very good at crushing the economy and inflation just like they did in 1981.

Volcker took rates up to 20%, but they're very bad at building the economy. So they can crush it, but they can't build it.

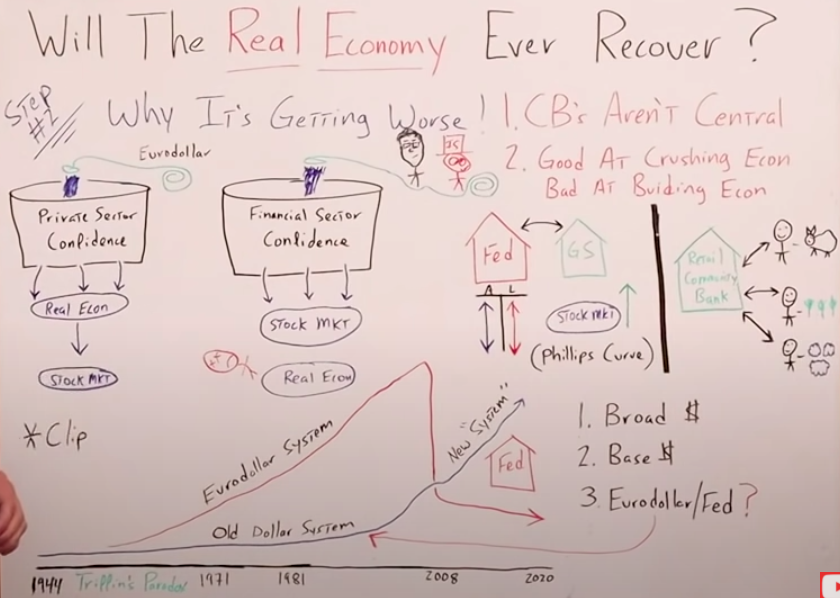

Check out this diagram:

To be very clear, this is just a visual timeline. It doesn't represent any amount of money supply or any amount of Eurodollars in the system outside of the United States.

It's just a visual that I drew so you could understand what I was referring to.

I was talking about the old dollar system and then the new dollar system, but I think it's a lot easier to get our heads around it if we think of this time, prior to 2008, as the time where the monetary system was focused on the broad money supply.

In other words, the money that was in the real economy, chasing goods and services, and the money that was being created by the commercial banking system, to fund productivity.

To fund entrepreneurs that were going out there to take risks and create more businesses, goods, services, and jobs.

Now that the system is broken, we've moved to the Fed coming in and trying to recreate the same productivity just by focusing on base money, bank reserves, and the Fed's balance sheet, not necessarily the balance sheet of the commercial banking system.

And it gets more nuanced than just the two balance sheets.

You have to ask yourself this question:

This Eurodollar system would have gotten out of control with the derivatives if the Fed wouldn't have come in the late 1980s, early 1990s, and started propping up the market with the Fed put?

Regardless of whether it was real or just psychological, it gave the market confidence to take more risk.

I definitely think there's an argument that the Eurodollar system wouldn't have gone that out of whack if it wasn't for the intervention of the Fed and the central planners.

But going back to a more nuanced look of the two systems, one focused strictly on base money and the other focused on broad money in the real economy, or the balance sheet of the Fed, however you want to look at it.

Now we have a system where the Fed goes back and forth with the primary dealer banks and the banks under their umbrella, we'll call it Goldman Sachs.

They're doing quantitative easing and all of this financial engineering that increases the size of the Fed's balance sheet.

Again, they're hyper-focused on base money because they think that will trickle down into the real economy and create productive broad money growth, but we're seeing that's not happening at all.

The only thing that it's doing is trickling down into the stock market creating asset bubbles.

What they're trying to do through…

- Money printing

- Quantitative easing

- Artificially low-interest rates

- The creation of additional bank reserves

- And taking their balance sheet to over seven trillion

Is have a positive effect on the real economy, but there's a distinct line in the sand. There's not a very good transfer mechanism.

On the left side of the line, there's the retail community bank that should be the driver of growth, they should be the focal point for a healthy economy. They're the ones that fund all the people out there.

I call them farmers in this very simple economy I always use. The guys that are growing cows, corn, and cotton. That's what the retail banking system should support.

That's the broad money that's being created in the real economy that's supporting all of this productivity, goods, and services. That's what we want.

But what we're seeing is the real economy isn't being supported at all. The only thing that's being supported is the financial economy, and you know this is a house of cards.

To understand what we may see in the future, as far as the Fed actions, you have to try to see things through their eyes, as difficult as that may be.

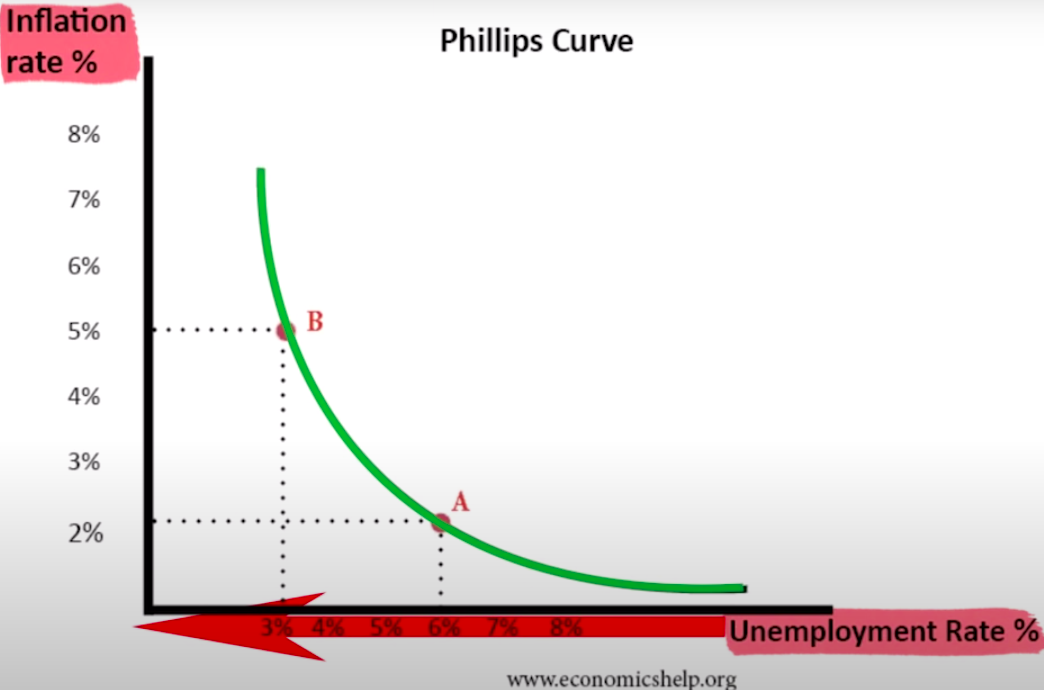

To do so you have to understand something called the Phillips curve editor.

The Phillips curve it's pretty much the lens through which the Fed and central banks view the world.

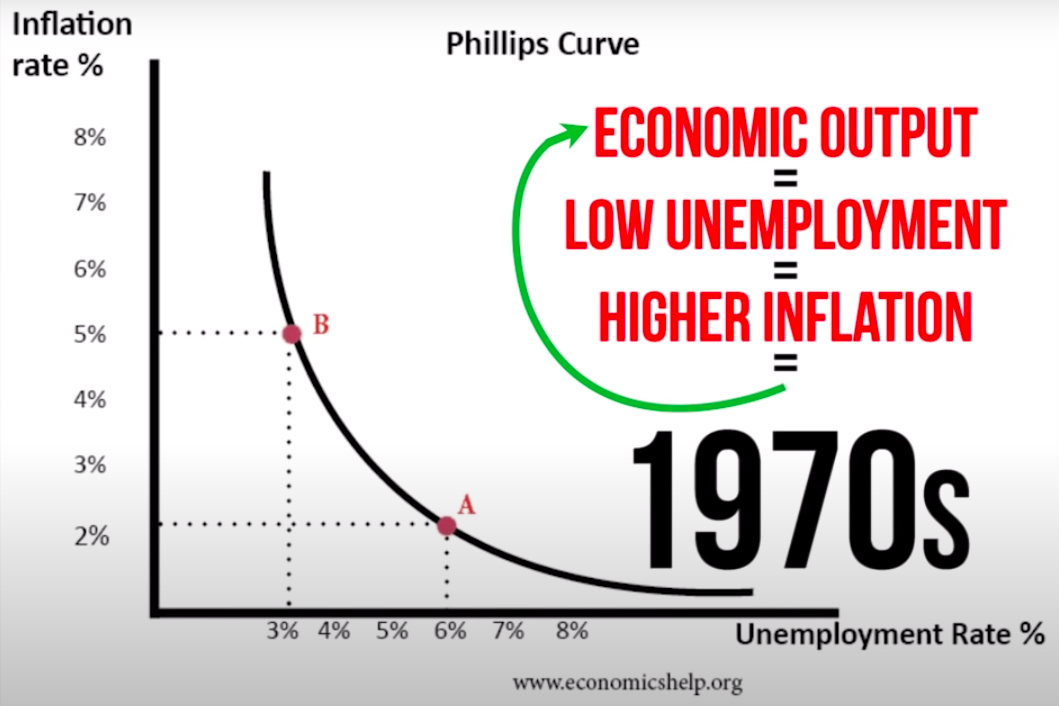

It has a pretty straightforward inflation rate on the left, and an unemployment rate on the right. As the unemployment rate goes up, the inflation rate goes down, and as the unemployment rate goes down, the inflation rate goes up.

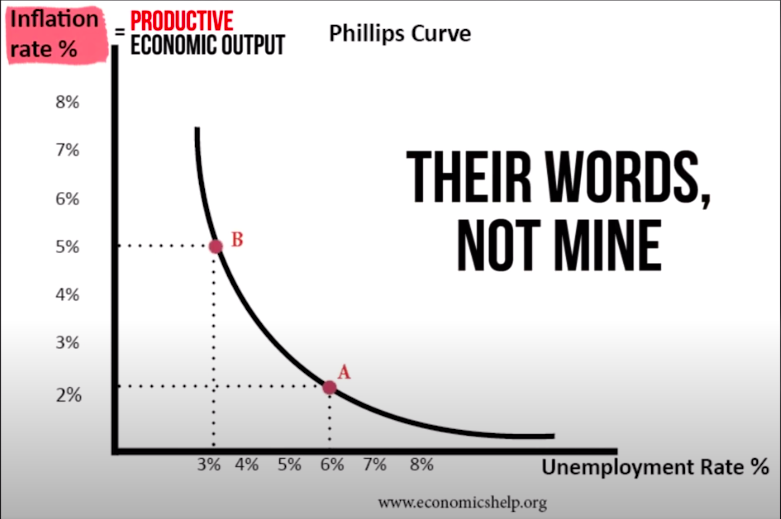

In the Fed's mind, if economic output equals low unemployment, and low unemployment equals higher inflation, then you can assume that higher inflation must equal economic output.

To say that out loud, it sounds kind of silly, especially when we have the 1970s to look back on, but these are the type of models that the 900 PhDs working at the Fed completely depend on.

They've removed logical thought and common sense from the equation and get hyper-focused on these models.

If the model tells them to do this, then that's exactly what they do and they expect to get a specific result.

If they don't get a specific result, they don't come to the conclusion that the model could be flawed, they just come to the conclusion that they didn't do enough of what the model told them to do.

Just to review again, they think the inflation rate equals economic output, productive economic output. Therefore, all you have to do is create inflation and you create positive economic output, real growth in the real economy.

Now let's look at this in a slightly different way to make sure we are on the same page.

I think it is crucial you fully comprehend what's going on so you can build wealth and thrive in a world of out of control central banks and big governments.

I'm just going to explain the process in a way that's a little different.

I've been using an analogy I got from Jeff Snider and Brent Johnson. It's the analogy of a bucket. There are two buckets and in the middle is Jerome Powell. I didn't draw it very well, I'm a bit disappointed with my stick figure because my black pen is running out of juice.

Anyhow, next to Jerome is your insolvent Uncle Sam, who obviously is drunk. We can see his smile kind of to the side and he's cross-eyed.

They have a hose and they're filling up the bucket with water, but the only way water can get out of the bucket to support whatever is below it, is if entities other than the Fed poke holes in it and kind of direct the water.

What happens is the private sector looks at who is filling the bucket up with water, and in this analogy, we'll assume the water is the creation of money, whether it's base money or broad money, and they see that it's really the Fed and the government.

They don't have a lot of confidence that's going to support the real economy so the only sector that has confidence in the creation of this new water from the Fed and the government is the financial sector.

All the water gets directed exclusively to the stock market and none of it flows down into the real economy.

Which gets worse until it's just DOA, as the red guy in the middle of my board that has passed out ready for the ambulance to come to pick him up.

You contrast that to the way it was before with this Eurodollar system, and the private sector had a lot of confidence in the Eurodollar system creating the additional money supply.

As the money was coming into this bucket, the private sector has a lot of confidence so then they take control of where the water, or the money in this place, actually flows.

On the left bucket, it goes to support the real economy. Then, since the real economy is flourishing and the stock market should be a reflection of the real economy, that water, or the money trickles down, and the stock market goes up at the same rate that the economy goes up.

But, on the right bucket, we have a situation where there's a total disconnect. The only thing going up is the stock market and the stock market is just a reflection of the stock market.

It has no correlation whatsoever to the real economy.

Now we have a whole bucket filled with distortions, misallocation of resources, no price discovery that's making the underlying fundamentals of the economy worse and it's destined to come crashing down.

There is no way to fix the real economy without changing the entire system. That's the problem.

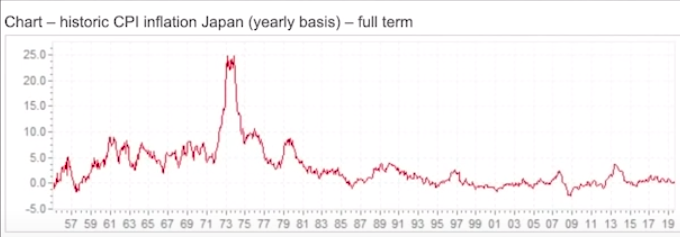

We can't continue to do more and more of the same and expect different results. As an example, here are a couple of charts of Japan and Europe.

They've tried to create this “inflation” by looking at the Phillips curve, like I mentioned before, and you'll see that both in Europe and Japan haven't been able to create inflation at all.

It's just been nothing but disinflation for the last couple of decades. But this isn't just my opinion. To explore this further, here is part of a recent interview I had with experts, Jeff Snider and Lyn Alden.

George:

Is it possible to fix the US economy without fixing the Eurodollar system?

Jeff Snider: No, I think it's not. We can get it working a little bit here and there as we saw in 2014 or 2010, it seems to progress a little bit, and then it sputters again, and it's even worse in the rest of the global economy.

If we're talking about a long-run solution, I think we need to replace the system. We need to replace the Eurodollar system.

I would prefer to see one that isn't entirely bank centered because obviously, we've seen the downside of what happens when it sputters and when it doesn't work right.

We need to find a system that works on all levels and does so predictably in a long-term fashion.

(End Of Transcript)

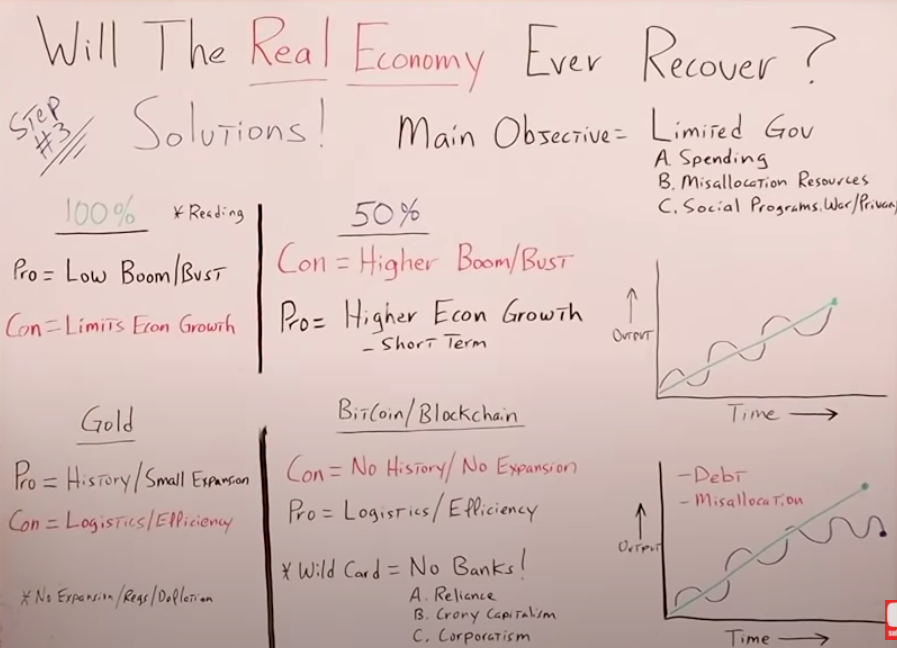

The solutions

We already discovered that because the global economy has been built on a very volatile eurodollar system, in order for it to truly recover and be structurally sound and anti-fragile, we need a completely different monetary system.

To go over the solutions we always have to remember that our main objective is the limitation of government.

Specifically, government spending because this is a misallocation of scarce resources with alternative uses, and this means limiting social programs.

A lot of people on the left, the liberals or the progressives, whatever you want to call them, not that they're right or wrong, but they always get fixated on social programs being cut back.

If we have a limited government, we reduce the amount of war and we increase the amount of personal privacy. Something that any liberals, or anyone for that matter, should be in favor of.

Try to shelf that just for a moment because I'm going to come back to it. We just need to remember that is our number one priority.

Because remember, as Dr. Thomas Sowell says, “There are no solutions only alternatives.”

Let's look at a couple of potential things we could do to restructure the current monetary system.

On top, you can see the first option.

Solution #1

We could go to 100% backing or 50% backing. This takes us all the way back to the gold standards, and, of course, there are pros and cons of each.

To dive into them deeper and really understand them, look at what I found on mises.org.

The first idea we need to contend with is the ability for the money supply to expand to maximize economic growth.

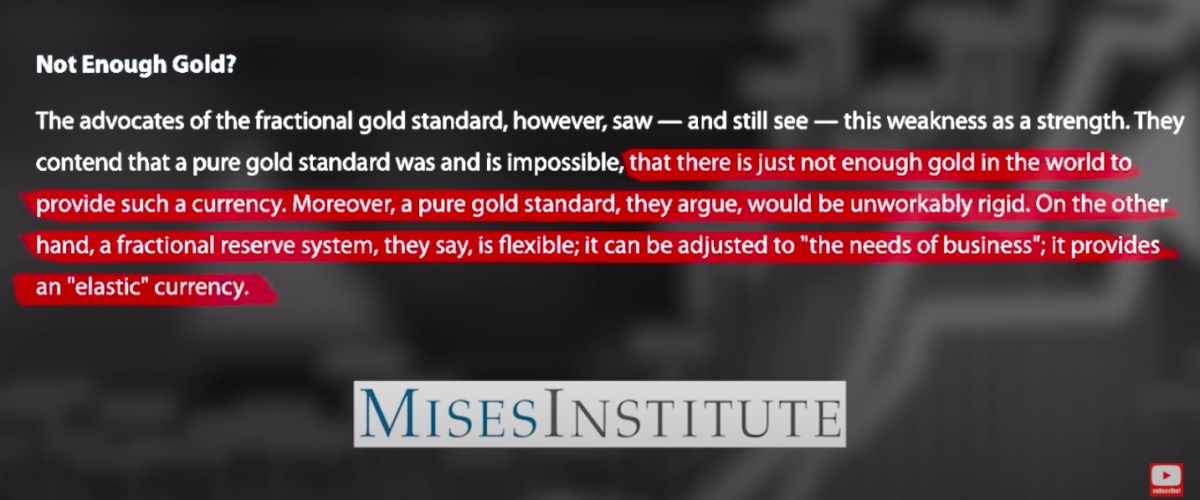

People who argue against a 100% backed currency, such as a 100% gold standard, argue that there is just not enough gold in the world to provide such a currency.

Again, the benefit here is that the currency and credit can expand to facilitate maximum economic growth.

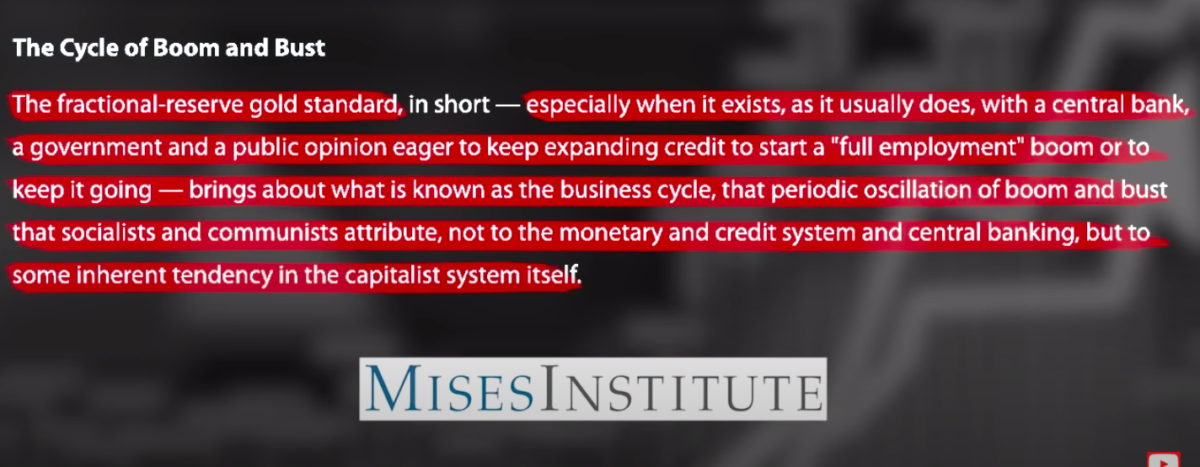

Unfortunately and as it is said in the quote: The fractional reserve system has drawbacks.

Especially when it exists, as it usually does, with a central bank, a government and public opinion eager to keep expanding credit to start a “full employment” boom or to keep it going, brings about what is known as the business cycle, that periodic oscillation of boom and bust that socialists and communists attribute, not to the monetary and credit system and central banking, but to some inherent tendency in the capitalist system itself.

Obviously, this really resonates with what we're seeing in the world and in the United States, more specifically today.

You may be saying to yourself, “My gosh, that is so true. This must have been written in the last week or maybe the last month, or at the most, the last couple of months.”

But when we go to the top of the article we see that this was written by none other than Henry Hazlitt in 1979.

Truly precious words from Henry Hazlitt and the Austrians about how the boom and bust cycle can lead to socialism and communism.

If you look around us in the world today, you can see this playing out right in front of our eyes.

Just as a recap for this solution: We have a 100% reserve system and a fractional reserve system of we'll call it 50%.

The pro over the 100% is it produces far fewer boom and bust cycles if any at all.

The con is that it potentially limits economic growth because you can't expand the money supply to keep pace with the needs of the private sector trying to produce more goods and services more efficiently.

On the fractional reserve side, the con is that it has a higher propensity to create boom and bust cycles, but it does allow additional money growth and the expansion of credit to facilitate higher economic growth.

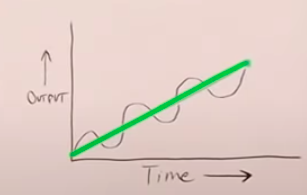

Although I would argue that usually, this is only short term. As an example, I drew a chart.

On the bottom is time expanding or time increasing and on the left is the output increasing.

The green line represents a 100% reserve system.

It goes up very slowly, it's kind of a turtle's pace, but it just chugs along and goes up and up. Now, the high flyer, the rabbit in the story, the fractional reserve system (50%), in the short-term, it goes up a lot faster.

But of course, we get ahead of ourselves as human beings. We have a bust cycle and it goes down, but then it goes back up, and back down again. But at the endpoint, we still have the same amount of economic growth.

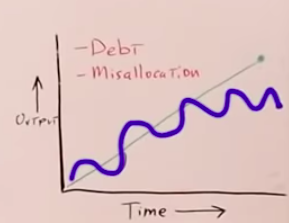

Although this makes sense, it might not be true. I would argue that the fractional system over time increases the overall debt burden.

Also, it allows the government to get involved and create this misallocation of resources by lowering interest rates, as an example, to artificially low levels.

We all know what that's done, and let's not even talk about quantitative easing.

In the beginning, yes, the blue line and the green line do go up the same amount, just at a different pace. But over time, the blue line, because of this debt burden and because we're misallocating resources, it starts to plateau.

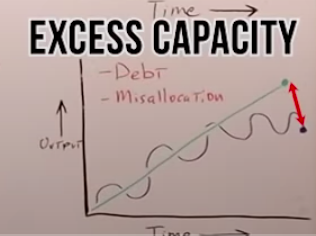

Then what happens?

The Keynesians, the central bankers, and the government come in and say, “Look, we have a Delta between what the economy is producing and what we should be producing. There's excess capacity in the system. So we'll just create more money and more debt, that will fix the problem.”

But you know, as well as I do that exacerbates the problem.

So, initially, it starts to plateau, but then once we get all of this central planning, artificially low-interest rates, money printing, and excess of debt, it makes it lower and lower.

As the economy and the private sector decline, government spending as a percentage of GDP gets higher and higher.

We'll take that to its logical conclusion where the government spending accounts for 100% of GDP, and we go right back to where we started with Henry Hazlitt, that we're now at socialism or communism.

Ideally, we would have a system that would allow for sufficient monetary and credit expansion to keep up with the pace of the private sector, creating more goods and services.

But as Dr. Thomas Sowell says, “There are no solutions, there are only alternatives.”

Because I understand that we're imperfect creatures in an imperfect world, I'm always going to favor the 100% reserve system.

That said, I'm more than open to new technologies creating a system in the future that will solve the problem of us being human beings and needing that additional expansion of money, supply, and credit.

Solution #2

But let's take it to the next step. Imagine we have 100% reserve backing or even a fractional reserve backing it, but it's backed by something.

Do we back it by gold, old school, or maybe something like Bitcoin, a cryptocurrency, and blockchain technology?

Let's walk through the pros and cons.

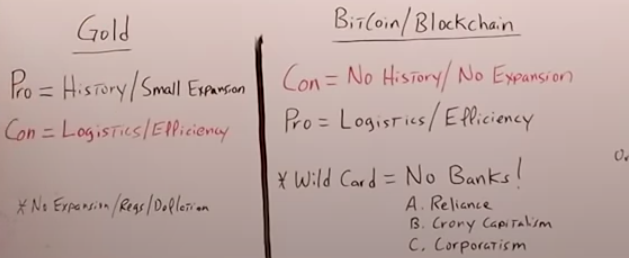

The Pros of gold

Gold has a 5,000-year history. That's for sure. We don't have to worry about people having confidence in gold, or gold maintaining its purchasing power. Definitely a store of the value we can all count on.

I would also add that it does allow for small amounts of expansion in money supply and credit because every single year there's more gold produced.

The Cons of gold

The con is that logistically it's very cumbersome and it's not efficient to have to move physical gold from the United States to Japan, South America, or Europe, to wherever around the world.

In 2020, with the global economy we have, we need things moving quickly to maximize our productivity.

That takes us over to the Bitcoin, cryptocurrency, blockchain side.

Cons of Bitcoin

t has no history whatsoever and it's very volatile. At least no history considering the 5,000 years we have with gold.

There is no room for expansion in the monetary supply. Many of you would argue this is actually a feature, not a bug.

To a certain extent, I would agree over the long-term, but we need to analyze this further.

Pros of Bitcoin

The main pro, logistics are seamless. It's very efficient to transfer Bitcoin or any cryptocurrency around the world instantaneously.

Also in the future, Bitcoin or another cryptocurrency could be payment in and of itself, instead of just used as backing another currency.

But right now we don't have the technology because there are so many payments and transactions that happen on a daily basis. But there's always that possibility in the future when technology advances.

The wild card is this technological option could give us the opportunity to get completely outside of the banking system, to where we didn't even need banks at all.

We would have complete reliance on ourselves, not the banksters. We eliminate crony capitalism and corporatism that's always blamed on free-market capitalism.

It's not just me saying this, the experts are thinking about this as well. As an example, let's go right back to my interview with Jeff Snyder and Lynn Alden.

George: Jeff, you were saying that we can't really fix the system as is right now and have a permanent solution because it's predicated upon the banking system and that is inherently volatile.

So, preferably we'd have a system outside of the banks.

-

My first question would be, what does that look like?

-

If we can transition to a better system smoothly, is there a way to do that?

Or the only way to transition is if the whole thing collapses and we rebuild it like the phoenix coming out of the ashes.

Jeff Snyder: I hope not. I hope that's not the transition. But it's a difficult thing, and it starts with recognizing the problem as it is and recognizing that there is a problem.

If we wait for politicians to get their heads out of their asses and say, “Okay, we need to do something,” then maybe that's what we're left with doing that.

That the next big crisis is what finally convinces them they need to do something.

Where do we go from here? I think we transition to a world, hopefully, that is based in some way on digital currency, blockchain. Whatever it might be.

I don't necessarily believe that it might be Bitcoin, but I think there's value in the Bitcoin technology. There's definitely value in blockchain technology, maybe an iteration or two down the road.

There is definitely a way to do a currency system that is non-bank centered.

If you really think, if you use blockchain as a payment space to account for all the payments that flow throughout the economy, we don't even need banks anymore.

We can have a bank-less monetary system that I believe would function, assuming that we could set it up in the right manner. The right manner is a loaded term that opens all sorts of Pandora's boxes.

But I think there's a way to do this, a digital currency way, so that it can be dependable, predictable, and operate in a sustainably steady fashion that solves a lot of the basic issues with your analysis.

I don't think it will necessarily be perfect, but we can't let perfect be the enemy of good here.

(End Of Transcript)

The more decentralized we can make our monetary system, the more this limits the government. Our main objective.

Before all you crypto guys and girls start celebrating and saying, “Yes, George is finally seeing the light.” There is something else we need to explore that might tip the scales back in the favor of good old fashioned gold.

To think through how a Bitcoin standard or a cryptocurrency standard would work, let's go back and revisit the good old fashioned gold standard.

On the right, I drew the United States, and we have a country named XYZ. Of course, the USA is running a huge trade deficit, which means that there's more stuff being imported into the United States than is being exported.

What that means, if we were on a Bitcoin standard, is the United States would have a net decrease in the amount of Bitcoin it has in circulation.

Country XYZ, that had the trade surplus would have an additional amount of Bitcoin circulating within their system. So this creates an additional money supply.

Technically, we would have inflation in country XYZ, meaning consumer prices going up.

In the United States, we would have consumer price deflation, but not as a result of more efficiencies and more goods and services being produced, but a lowering of the overall money supply.

Back in the days, when wages were flexible, there was no minimum wage, very little credit in the system and the economy wasn't built on debt and asset bubbles, the deflation wasn't a big deal.

Because money goes down, prices go down and everything else goes down with it, so you have this equilibrium.

But in today's economy, where wages are very sticky, there is an excess of credit in the system. Everyone's levered to the hilt, and we have an economy that's built on debt, asset bubbles, and confidence.

If we had a deflationary spiral due to a lower money supply, that would be completely catastrophic.

The main takeaway is that, although I favor a 100% the reserve system and a system based on the technology could be very interesting in the future, it may allow us to limit the size of government even further. Also, reduce crony capitalism and corporatism. But it might not be realistic in today's day and age.

Why? Because if we transfer to either of the systems overnight, it would completely collapse the economy because of what we went over in the last diagram.

We'd have to go all the way back to the late 1800s where we had limited government, no central bank whatsoever, low regulation, and low taxes. The probability of that is extremely low.

A hybrid system, maybe 50% reserve, or a system backed by gold that does expand slightly, could be better for what we're dealing with today, the way the economy is currently set up.