I‘m trying to make sense of the complete insanity of 2020. People are buying stocks, equity in bankrupt companies, and equity of companies that have never made revenue with their unemployment checks.

The speculative mania is truly remarkable! Can we better understand asset bubbles, in general, to get our heads around what’s happening today and use that understanding to make solid financial decisions for the future?

Yes, we can. During this article, I explain the structure of an asset bubble and its phases, its key components, and the psychological attributes that come with it.

At the end of the day, it’s one thing to know why the market is behaving irrationally, but we also want to position ourselves to profit from the madness!

Structure Of An Asset Bubble

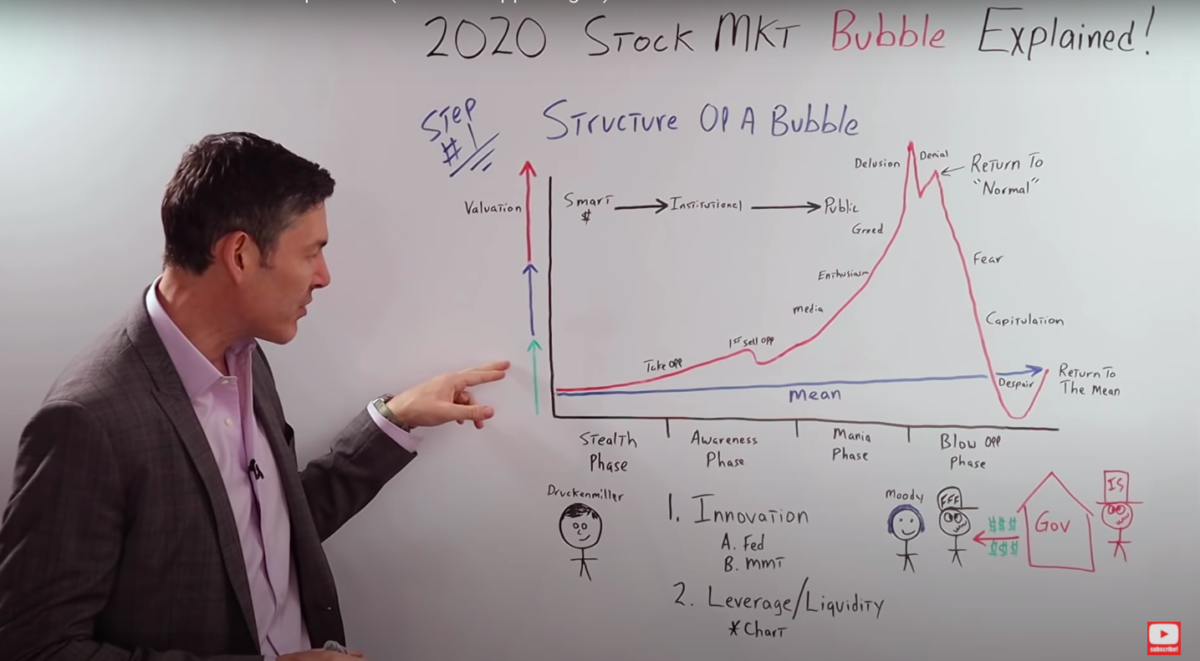

Usually there are four phases for an asset bubble, which I drew in this whiteboard.

On the left, you can see valuations. They start very cheap, but then it goes mid-range and eventually it gets insanely expensive.

-

Phase #1: Stealth

It starts when the smart money comes in and starts to buy. This is where guys like Stan Druckenmiller see and value things that other people just can't see.

-

Phase #2: Awareness

It starts when the institutional investors start to see what the “smart money” saw long before. In this phase, prices go up.

Then we get to our first sell off, the bear trap, but the fundamentals are still good so it goes up.

-

Phase #3: Media

It starts when they see the story and announce it to everyone. You see it on CNBC, Bloomberg, and in The Wall Street Journal. The public starts to understand what's going on and you get this enthusiasm phase.

Greed sets in but then complete and utter delusion comes. This is the phase when you hear phrases like “It's a game changer, a paradigm shift, it's a whole new world,things are different this time.”

Then of course, reality sets in. Fundamentals start to take over. The market rolls over and it goes back down, but all the Joe Public's that bought on the way up, are in complete denial.

They've been told over the last two decades that you always buy the dip. You see it on Instagram, YouTube, and Twitter.

So Joe Public maxes out its credit cards, takes its unemployment checks and goes right back in and buys because that's what “smart” investors do.

The market goes back up and everyone takes a sigh of relief. They think “Thank goodness. We're going right back to normal.”

But all the buyers have blown their low. There are no more buyers left. So the market rolls over again and completely plummets.

It can retrace 50%, 60%, even 70%, but finally, the fundamentals take over. It falls out of bed.

-

Phase 4#: Blow Off

We get the fear phase where everyone is freaking out because they've lost all this money but the market continues to go down to capitulation.

This is when people are saying, “I want nothing to do with this stock market or this XYZ asset class. I was crazy to buy it. Why did I do this? I've lost so much money. I'm never going to buy stocks again for the rest of my life, everyone knows that stocks always go down”

It's hard for us to even imagine Joe Public saying that right now, but it takes me back to 2012 when I first got into real estate investing. That year was the absolute bottom of the real estate market.

I went almost all in with rental properties in the Midwest and everybody was telling me that I was crazy.

They said, “George, don't you know anything about investing? The real estate market is going to go down for the next decade. You have to be a fool to buy real estate. Everybody knows that real estate prices always go down.”

A great example of capitulation, but usually prices continue to go down.

As you can see on the right side of the chart, they get into a despair phase and that's when the smart money guys like Druckenmiller come back in and start to buy from all the dumb money that sold on the way down, and the cycle repeats itself.

Components Of An Asset Bubble

There are two key components that we've seen throughout the history of asset bubbles going all the way back to the tulip craze.

-

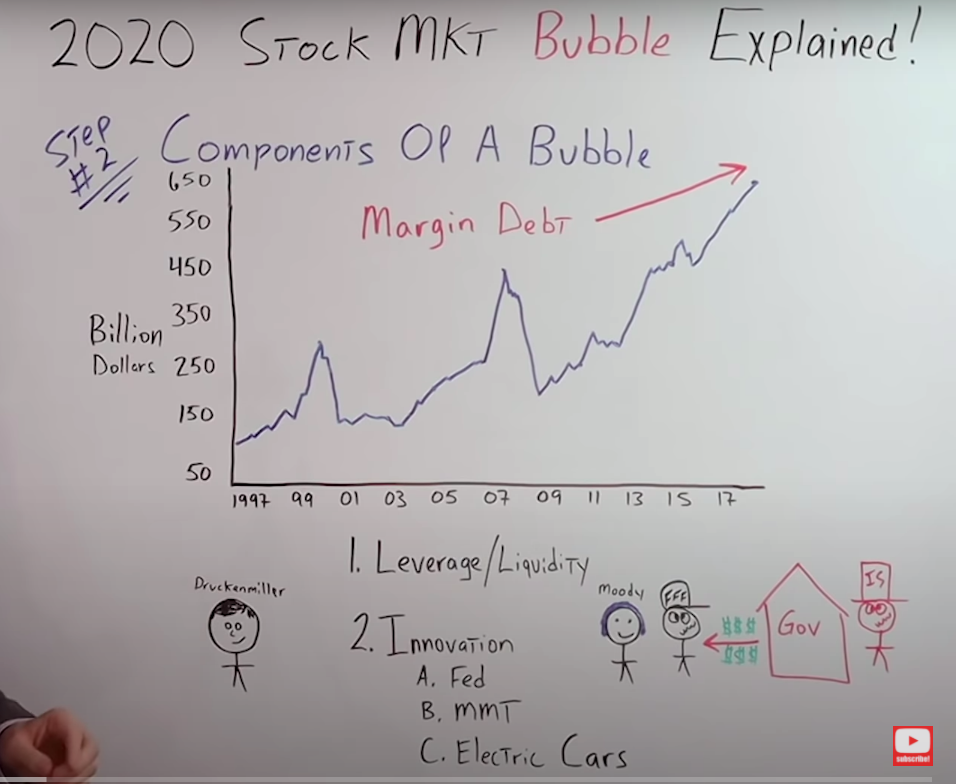

Component #1: Leverage and liquidity

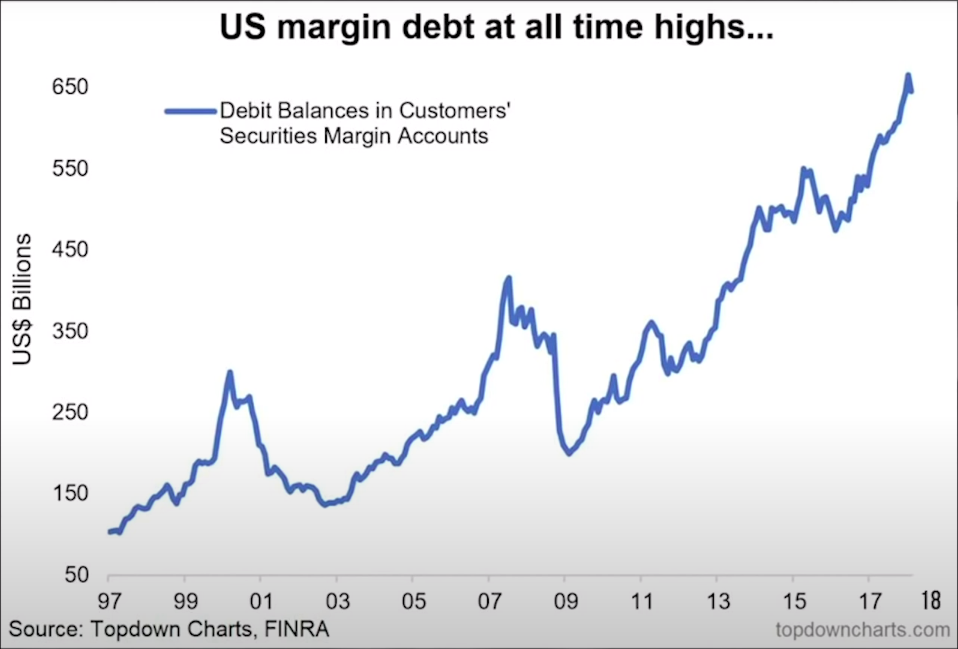

Here is a chart going back to 1997, and all the way to 2018.

On the left, it goes from $50 billion up to $650 billion. In 1997 it started off at about $75 billion and then gradually went up until it got to 1999 where it went parabolic as you'd imagine during the dotcom boom.

It came all the way down and started to go up again in 2003 until it reached 2007 where it went parabolic again before the next crash.

The global financial crisis hit and then it came down. During 2009-2010, it started going up and didn't stop growing until an all-time high that it had in 2018.

Since then, I'm sure it's even higher. As far as margin debt or leverage in the stock market, we can definitely go ahead and check that off the list. But there also needs to be excess liquidity.

Look at the following whiteboard and notice your drunk insolvent Uncle Sam on the right.

He is spending trillions of currency units into the real economy in the form of stimulus checks. That money is going to people like your friend and family member Fred, and of course, to Moody, the millennial.

What are they doing with these stimulus checks?

They're going right into the stock market. As an example, look at what CNBC says.

Many Americans used part of their coronavirus stimulus check to trade stocks.

-CNBC

That's the headline, we get that. But check out the bullet points from CNBC.

-

“Trading stocks were among the most common uses for the government stimulus checks in nearly every income bracket, according to software and data aggregation company Envestnet Yodlee.”

-

“People earning between 35,000 and 75,000 annually traded stocks about 90% more than they did just the week prior to receiving the stimulus check.”

Just like leverage, I think it's extremely safe to go ahead and check liquidity off the list as well.

-

Component #2: Innovation

The second component is some sort of innovation or at least what the public perceives to be innovation. I think there are three things that could fall into this category right now.

A) Believe it or not, first and foremost, the Fed

The Fed saved the day, or this is what society believes and what the media and politicians would lead you to believe.

They came in the 1990s with the “Greenspan put”, Bernanke came in and saved the day! The.com bubble? That's nothing to worry about.

Greenspan dropped rates and the housing market crashed. Bernanke came in and they started quantitative easing. They started printing money. They figured out a way to solve the problem.

They were innovative and if we would just place our faith in the monetary mandarins, as Jim Grant says, and the 900 PhDs led by Jerome Powell, if we would've just done that earlier, then we would all be rich.

Because we never would have hesitated to go into the market and buy the dip because we know the “Fed put” is real. It's an innovation created by central banks.

B) Along the same lines: MMT

This is what the market says:

“What on earth were those Austrians worried about for so long? They always complain about their crazy inflation. It's the boogie man hiding under your bed like a little kid.

Look at how much money we've printed since 2008, we haven't had a speck of inflation. We don't have to worry about it anymore. There's absolutely no downside to printing money and inflation is dead.

If we just released the shackles that we've been under for so long worrying about inflation and move on to an enlightened state when we all just realize that the government can print their own money.

If the government can print their own money, it solves everything. We can eradicate poverty. We can have asset prices continue to go up and up and up for eternity.

All we have to do is realize the innovation of Fiat currency and money printing.”

Again, this is the market saying this, not George Gammon. You guys know that.

C) Lastly, Electric cars

I'm not saying they aren't the future, I'm just saying that right now, the general public is way ahead of reality, just like they were with the internet back in the 1990s.

A great example of this is a company called Nikola, a complete rip off of Tesla.

Basically what they did is they couldn't even come up with an original name, first and foremost, but they saw all the millennials and all the investors that are unsophisticated piling into Tesla, driving up the stock price.

They said, “Well, we'll just do the exact same thing. In fact, we'll use the exact same name.” They're riding on Elon Musk's coattails.

They don't even have a product or a concept car, nor do they have revenue.

According to the Markets Insiders:

Nikola Motor Corp, has yet to sell a single car, has $0 in revenue, and doesn't expect to generate revenue until 2021.

Let me repeat. I didn't say they don't have profit, I said they don't have $1 of revenue, not even a penny and this is a company that has a market cap of $30 billion. With a B.

They have a higher market cap than Ford Motor Company and they've never generated a penny in revenue.

Combine this with Joe Public taking their unemployment checks from the government directly into the stock market, on margin levering up, and becoming day traders by buying the equity of companies like Hertz that have already filed bankruptcy.

Put all these things together, and if they're not clear signals of a stock market bubble, I don't know what is.

5 Psychological Attributes Of An Asset Bubble

These are the five psychological attributes of an asset bubble. This is courtesy of a fantastic article from Tech Crunch.

-

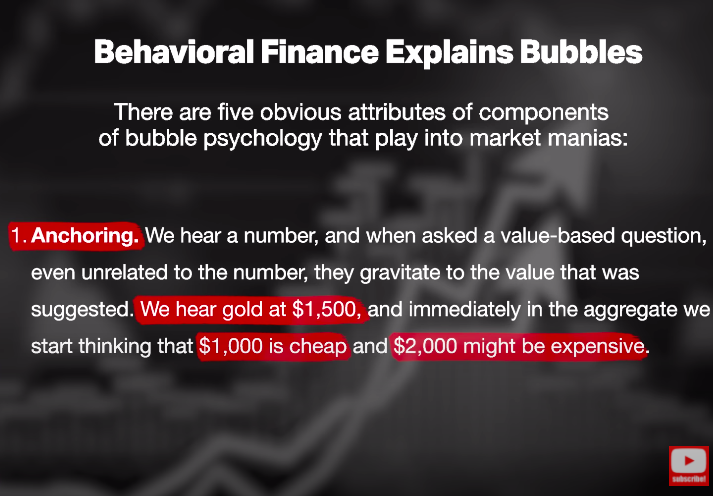

Attribute #1: Anchoring

They use an example of gold, but I think it's a lot better to use an example of the stock market as a whole. So, let's just replace the word gold with the S&P.

People heard the first week of June 2020 that S&P was at 1,500, the second one it was at 1,000.

They automatically assume it's cheap and if next week they hear the S&P has gone to 2,000, they automatically think it's expensive.

Their analysis is strictly focused on price instead of value.

This is something I preach until I'm blue in the face. You guys know that I'm constantly talking about value instead of price.

-

Attribute #2: Hindsight Bias

“We overestimate our ability to predict the future based on the recent past.”

Boy, oh boy, that is ever true.

-

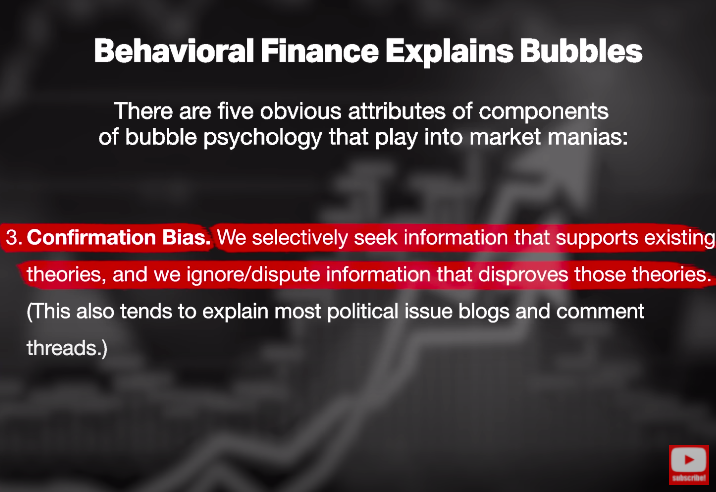

Attribute #3: Confirmation Bias

“We selectively seek information that supports our existing theories and we ignore/dispute information that disproves those theories.”

In other words, we get into this echo chamber and refuse to hear anyone talk that isn't aligned with exactly what we're saying. This is extremely dangerous, but we see it all the time in bubbles.

-

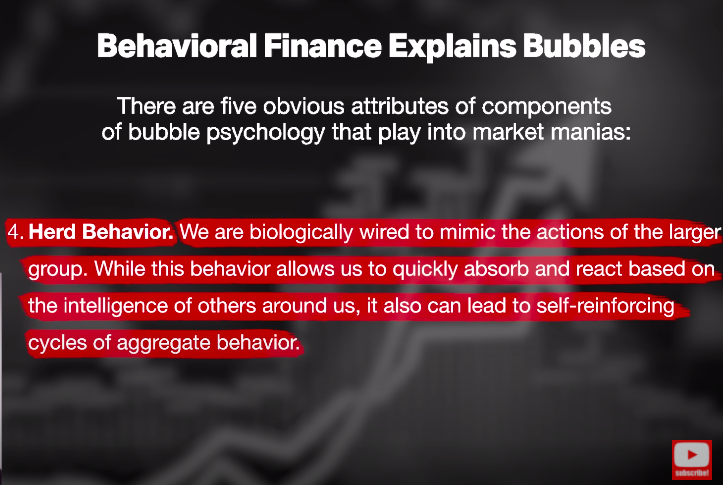

Attribute #4: Herd Behavior

We are seeing that to an extreme right now with all the people taking their unemployment checks and buying the dip.

“We are biologically wired to mimic the actions of the larger group. While this behavior allows us to quickly absorb and react based on the intelligence of the group as a whole, it can also lead to self-reinforcing cycles of aggregate behavior.”

This, I think, is the core reason why asset bubbles exist.

-

Attribute #4: Overconfidence

“We tend to overestimate our intelligence and capabilities relative to others.” Boy, do I agree with that.

The article sums things up beautifully.

“Ironically, the combination of these traits predictably leads to these four words: it's different this time.”

Because of those attributes and human psychology, I'm under the belief that the market will always hurt the maximum number of people.

Look at the chart going back to the tech boom.

We know that everyone was piling in, the taxi drivers, the construction workers, and the teachers. Everybody was buying tech stocks. The market lures them in with that greed and then it completely collapses.

The exact same thing in the housing bubble, everybody was getting rich with real estate.

The shoeshine boy, I guess that might've been the 1920s.

You'd go to cocktail parties and your friends were talking about it. You'd go to dinner and the waiter would have just purchased a condo and already made $100,000 on paper.

You would get into that Uber ride and sure enough, your drivers talking about how they just made a killing in real estate.

Again, the market draws everyone in through that FOMO and then collapses.

But you also have to look at the flip side of the coin.

-

What if we're not in a bubble right now?

-

What if we're at the beginning of a bull market?

Well, if this were true, then all Uber drivers, the construction workers, the millennials, and the high school students would have to be right and people like Warren buffet, Stanley Druckenmiller, and Chris Cole would have to be wrong.

I'm not saying that's impossible, but go back in history and ask yourself: At what point in time was the shoeshine boy, the Uber driver, or the construction worker, right?

When did they get hyper-emotional about the market?

They lever up. They max out their credit cards. They do crazy things like taking their unemployment checks and going into the market.

-

When did that work out?

-

Did that work out in the '90s at some point in time?

-

Did that work out in the 2000s?

It has never, ever, ever worked.

If we're at the beginning stages of a bull market now, all those people, the average Joe's that are incredibly emotional, driven by emotions and not thinking facts, data, and fundamentals are going to get rich.

If we're at the beginning stages of a bull market.

What is the probability of that coming true?

In other words, what are the chances that 50 years from now, we look back at the history books and it says, “In 2020 high school students across the United States got rich by opening up a Robinhood account and buying equity in Hertz, a company that has already filed bankruptcy.”

I always say there are no certainties. There are only probabilities, but if I had to bet on one thing being certain, I would definitely bet that you won't be reading that in future history books.

I'm sure most of you are saying, “Yeah, George, I get it. I understand. We're in a massive stock market bubble right now in 2020. But what am I supposed to do about it? I need solutions.”

For that, I got you covered. Don't worry about it. But you're going to have to stay tuned until the next article where I dive into my very best investment advice.

Comments are closed.