Are We In Another Real Estate Bubble?

Anyone who tells you the RE market is insulated because lending standards are tighter doesn't know what they're talking about.

Ignore them. Additionally ignore anyone who tells you anything along the lines of “don't wait to buy real estate, buy real estate and wait.”

Most RE investors just don't understand macro risk and rationalize it away because they're emotionally and financially invested.

Calvin’s outline of current conditions was excellent, I can't improve on what he said but I might be able to expand on it to give you an even clearer picture, and some actionable advice.

Many reference news headlines over the past few years claiming we're in another housing bubble.

Their point is everyone’s been saying it and it hasn't happened so the yield curve inverting is just another doom and gloom predictor that will come and go.

Comparing the yield curve inverting to other news headlines is like comparing the advice given by a homeless person and advice given by Warren Buffett.

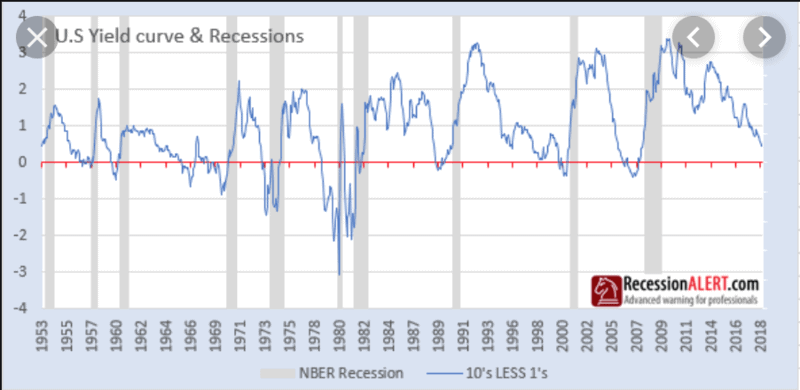

FYI, the yield curve is Warren. Let's look at a chart to put things in perspective.

Please note: the current yield on a 1 year is 1.72 and the current yield on a 10 year is 1.52. This has literally predicted every recession since 1953.

Nothing is ever certain, we have to look at probabilities.

Based on the chart above the probability of the US going into recession is extremely high.

But so what. The US has been through recessions before w/o real estate prices being affected.

We need to first understand what 3 things now drive the US economy:

- Debt

- Confidence

- Asset prices

Just picture a US economy with half the debt. What is the USD backed by other than confidence?

Consumer spending (70% of the economy) driven by confidence.

How about asset prices? What does the US economy look like if housing, stocks, bonds all take a 50% haircut?

So why are the risks so great? What are most investors missing as they whistle past the graveyard?

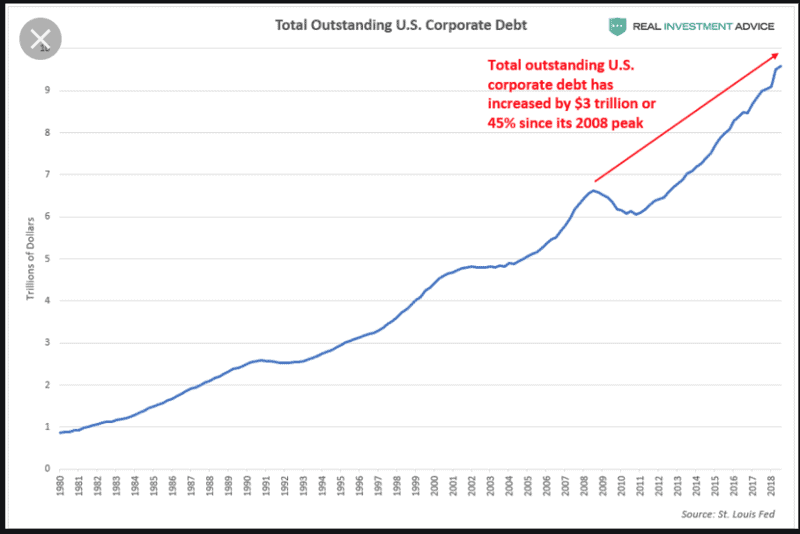

First and foremost corporate debt.

Artificially low interest rates create malinvestment.

Everyone knows this. After the dot com bust artificially low rates were vital to creating the housing bubble, which was a credit bubble (malinvestment.)

While it is true, we don't have a consumer debt bubble as we did in 2007, although there's a strong argument for auto/student loan debt being the next consumer shoe to drop.

But this isn't likely systemic like the housing debt bubble was in 2007.

The big problem is, all that consumer debt we had in 07 has moved to corporate balance sheets. See chart

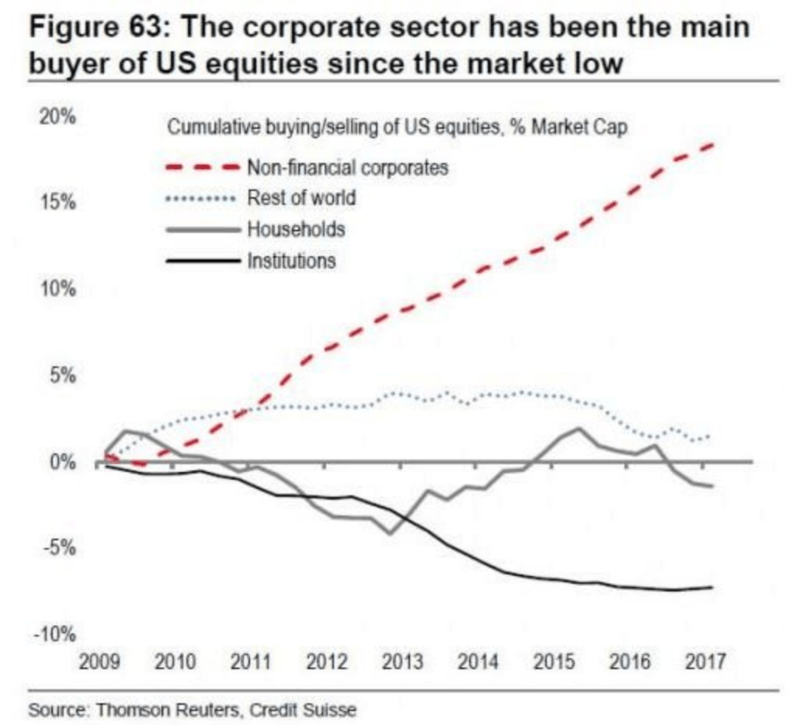

So what's the big deal? The reason this is such a problem is what the corporations used the debt to purchase. See chart

Corporations didn't use the money to build more factories or become more competitive, they used the debt to buy back their own shares.

Also note: institutional buying, where did the institutions go?

Into the corporate bond market in search of yield because the Fed dropped rates to zero.

Are you starting to see the iceberg in front of the titanic? 😉

So corporations borrowed a ton of artificially cheap money (more debt) to buy back shares and artificially increase their share price (higher asset prices) making the stock market go up and give the illusion of prosperity (public confidence).

Remember, the economy is driven by

- Debt

- Asset prices and

- Confidence.

What happens if stocks go down for more than 6 months?

Step 1 – Corporate balance sheets deteriorate because so much of their balance sheets consist of their own stock.

Step 2 – The corporate debt gets downgraded because of deteriorating balance sheets.

Step 3 – Institutions have to sell the downgraded corp debt because by law they can't own “junk” or high yield debt.

Step 4 – No buyers for stocks or corporate debt.

Step 5 – A massive negative feedback loop where lower stock prices create lower debt prices and lower debt prices create lower stock prices.

Then debt seizes, stocks get cut in half (which is where they would likely be without the corp buybacks), and confidence goes to 2009 levels if not worse.

Also, think about what happens to retiree's pensions, if stocks and bonds go down by 50%…pensions go bust. It gets ugly fast.

What are the likely side effects for RE investors?

1. Much higher interest rates on the 10 year, so mortgages. If you can get a loan which will be tough because the credit markets will be near frozen. That means lower home prices.

2. Unemployment will skyrocket putting downward pressure on rents. Usually higher unemployment would mean more renters, but not if unemployment goes into double digits and people are struggling to find work.

3. Rolling debt over at much higher interest rates so positive cash flow props will go negative.

I could go on but you can see how we don't need a consumer credit bust or housing problem to create a massive housing problem.

Please note: These are probable outcomes, not certain outcomes.

As an example, the Fed would possibly drop the fed funds rate into negative territory and do a massive round of QE 4 to bail out the corporate bond market.

An MMT democrat could take the white house and print trillions to bail out consumers.

But something has to give, there has to be some release valve.

That release valve would most likely be the USD. Which in turn means the 1970's 2.0, high inflation, high unemployment, and high long term interest rates.

I'd encourage everyone reading this to stress test your RE portfolio using the 1970's metrics… 9%+ unemployment, 10% inflation, and double-digit interest rates on the 10 year.

How would it do? My guess is not well.

My point is, anyone brushing off the yield curve doesn't know what they don't know.

Don't fall into this trap and ignore the fact if we have even a small recession the US has HUGE problems, far greater than 2007.

I'm not saying US RE prices won't go up. US could be the next Japan and have ZIRP for years. What I am saying is it's less probable.

Use the info in this post and a few other very astute posts on this thread to make a decision based on facts and economic reality, not emotion and ignorance.

Actionable takeaways:

1. If you buy now, use 30 year fixed rate debt <60% LTV.

If the USD is the release valve you'll make a fortune. If it's not you can refi at lower rates, there's almost no downside.

2. Buy starter homes under the cost of construction with 1% R/V ratios in great neighborhoods.

It's the most you can do to limit your downside.

3. 5%-10% of your portfolio in gold.

4. Consider investing in RE outside the US in markets where there is very little debt in the RE market.

The world is drowning in debt, this will have to be written off or inflated away. Both scenarios favor non-leveraged RE markets.

Hope that helps,

George.