What is a debt jubilee and what does it mean for a country like the United States? Is it a solution where debt disappears, or is it a crazy invention leading to economic collapse?

First, we need to understand how we look at assets and liabilities.

Sometimes we think of assets and liabilities as something tangible. But are they really?

Aren't they ultimately just electronic digits on someone's balance sheet?

And how about treasuries?

Treasuries are simply the debt of the government. And it's crucial we understand this to see if a debt jubilee could ever work for the US.

In this article, George explains the idea behind a debt jubilee, its implications, and the real problems it can create.

Also, this article is a repurposed video transcript. In an effort to keep it simple, it's written in the first person.

Debt Jubilee Explained

Is debt jubilee a simple solution to a massive debt problem or could it trigger a system collapse?

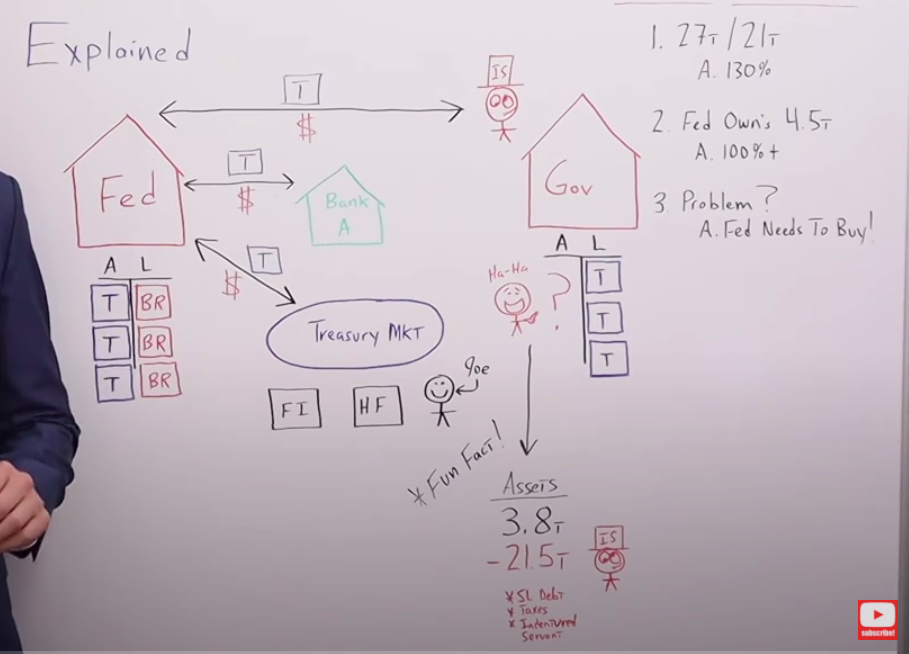

To start digging, let's look at the whiteboard.

The Federal Reserve is on the left and the government is on the right.

This example starts with your drunk insolvent Uncle Sam, as it usually does.

I always say, “He is insolvent”, and you may ask yourself, “why?”. Keep reading…you're about to find out.

So, the Fed needs to accumulate treasuries onto its balance sheet. But…

Remember, treasuries are simply debt of the government.

…the Fed buys treasuries directly from the government through a shell game, thereby monetizing the debt. They also buy from the banking system and the open market.

All those treasuries go onto the Fed's balance sheet. Usually, the open market consists of financial institutions, hedge funds, pension funds, and everyday people.

All the treasuries that go on to the Fed's balance sheet, are now assets of the Fed but liabilities of the government.

We usually look at assets and liabilities as tangible things that we can hold, like a bar of gold. But for the most, they're really just electronic digits on an account somewhere.

All the FED would have to do is come in one morning and hit the delete button on the asset side, which would go to zero, and then on the government's liabilities side of the government balance sheet, and just simply, puff, it goes to zero.

But, you have to ask yourself this question…

Would anyone know if the Fed forgave the debt?

It's an interesting question that I'm going to explore later in this article, but before we get there, let's go over some hard numbers.

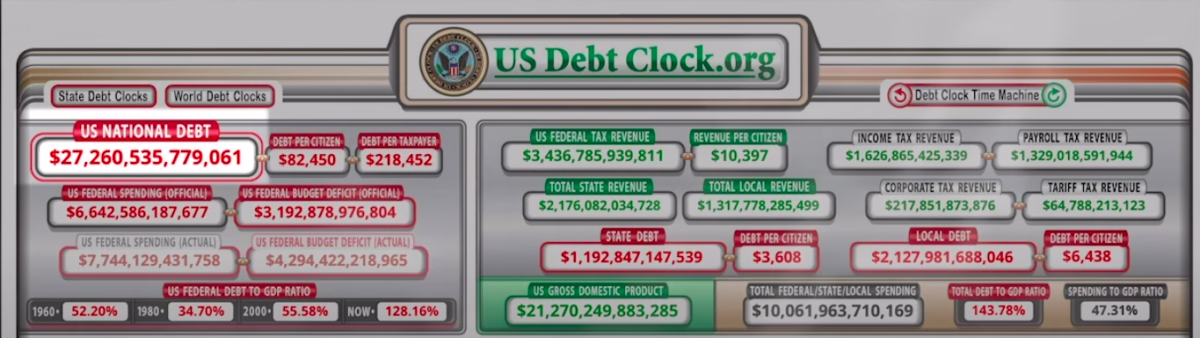

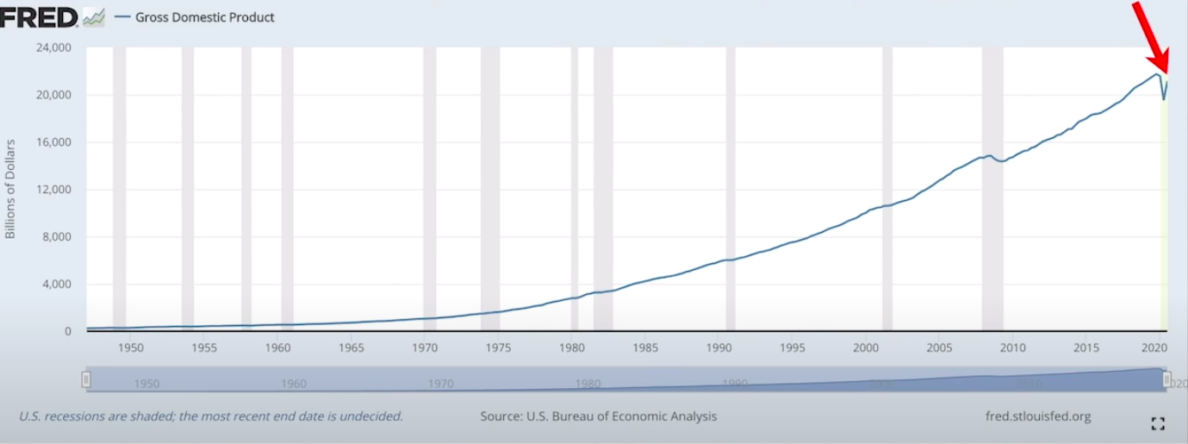

Right now, the government is 27 trillion dollars in debt, but nominal GDP is only 21 trillion. Now the government has almost 130% debt to GDP.

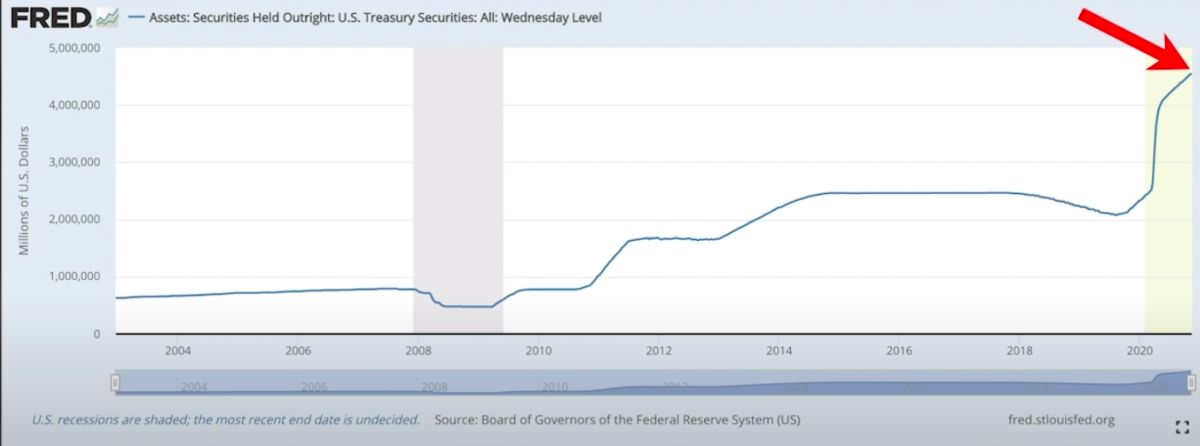

Currently, the Federal Reserve owns about $4.5 trillion in treasuries.

So, even if we had a debt jubilee right now, the same type of debt jubilee I just described would only take the government's debt down to about $22.5 trillion.

It's extraordinarily high. In fact, the debt to GDP ratio would still be over 100%.

The big problem debt represents, if interest rates were to go back up to normal maybe around 5% or 6%, is that it would be very difficult for the government to service the debt through tax receipts alone because almost all the money coming in from the tax payments would go to service the debt.

So, where are they going to get the money for all the other government expenditures?

They would have to monetize the debt and the release valve would most likely be the United States Dollar.

But if we put that problem aside for just a moment, if we wanted to get a debt jubilee that would really matter, the Fed would have to buy a lot more treasuries than they already own.

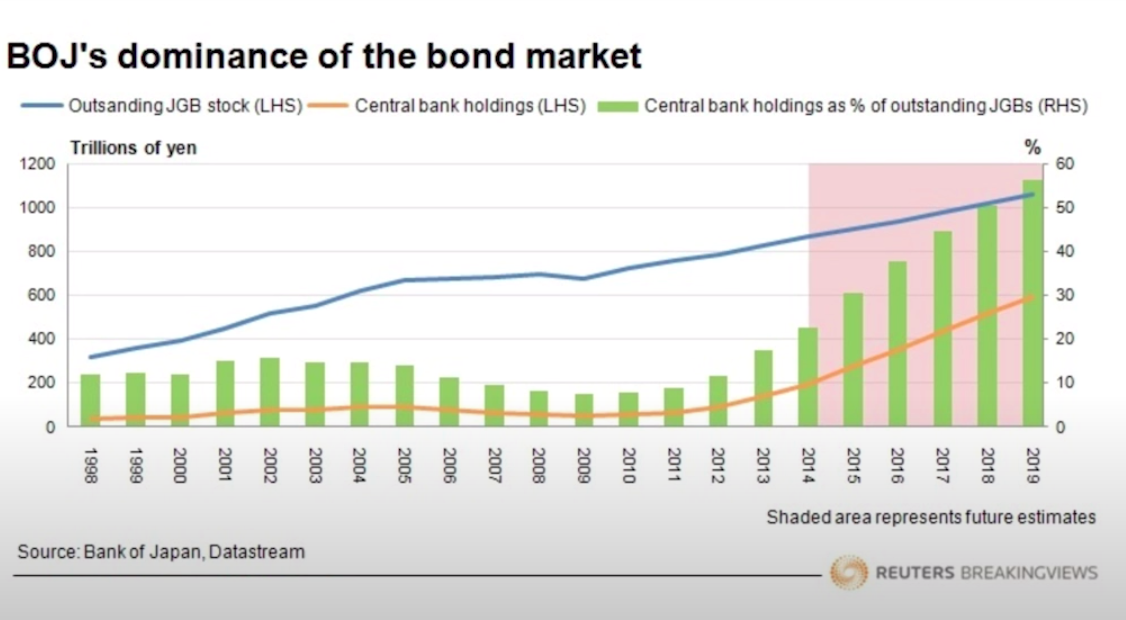

We'd need to get the debt to GDP ratio down to 80%, 60%, or maybe even 50%. To do that, the Fed's balance sheet would need to look a lot more like Japan's.

In this chart, you can see they own almost 60% of the government debt outstanding.

But, if that were the case, let's explore the problems that may occur as a result of the Fed trying to buy more and more treasuries. But first, I want to give you a quick fun fact.

You may have noticed the asset side of the government balance sheet has a big question mark on the right…

-

How much does the Federal government actually own?

-

What does their balance sheet really look like?

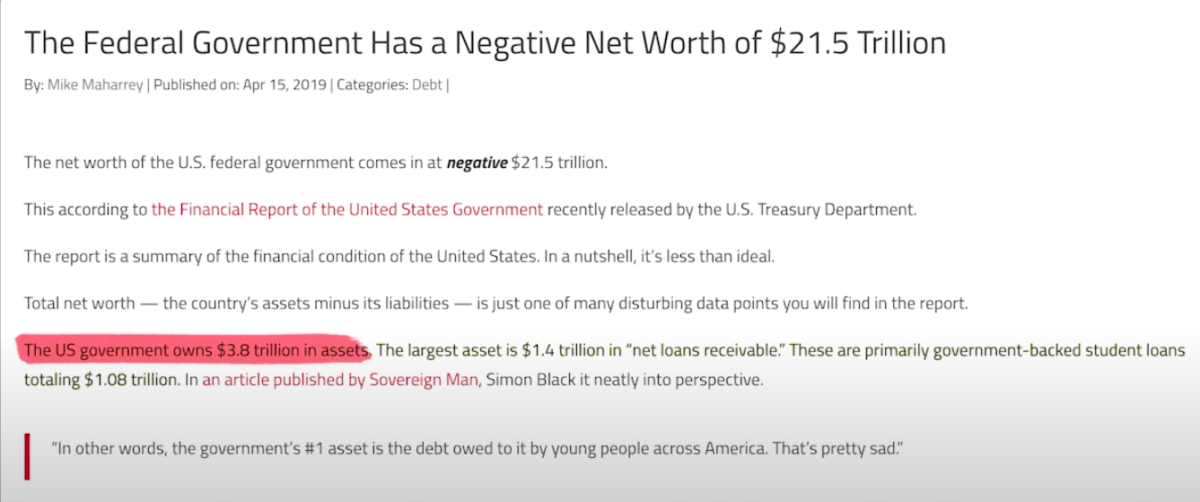

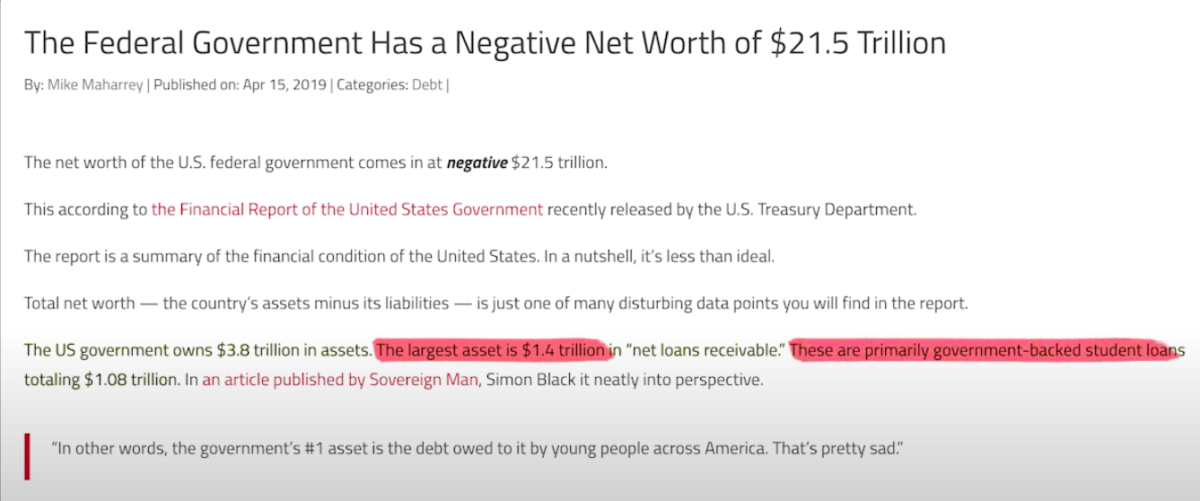

We know the liabilities side has over $27 trillion, but you may be shocked to find out that the asset side of the government's balance sheet has only $3.8 trillion.

When you look at the asset side of their balance sheet and realize there's only $3.8 trillion compared to the $27 trillion-plus they have on the liabilities side it shocks.

I even drew that kid from the Simpsons, the Nelson bully kid that always says, “Haha!.” It's us looking at your drunk insolvent Uncle Sam doing the exact same thing.

When it comes to stuff like this, you have two choices, you can either laugh or you can cry, and I always try to laugh.

This article is based on 2019 information and hat tip to Simon Black at sovereignman.com.

He pointed out that back in 2019 the government had negative equity, or they were upside down by $21.5 trillion.

Now, you know why I not only refer to him as your Uncle Sam, but you're drunk, insolvent Uncle Sam.

Think about it this way. The next time you go out and see a homeless person standing on the street begging for change realize that individual is over $21 trillion richer than the government.

But what really gets scary is when you start to look at what's included in the $3.8 trillion.

The largest asset of the Federal government is student loan debt.

When you think about how much taxes are going to be going up in the future and you combine that with the understanding that student loan debt is the only thing that you cannot wipe out in bankruptcy, it becomes crystal clear that today's young people, the millennials, the kids in college right now, are really indentured servants of the government.

I think we can now all understand why Moody the Millennial is so moody.

Downside Risks Of A Debt Jubilee

What are the downside risks and the potential disasters that could occur from a debt jubilee?

It's actually a lot harder to figure out than you'd think.

As an example, here is a transcript from one of my favorite podcasts: The End Game with Grant Williams and Bill Fleckenstein. They try to think through what on earth would happen if Japan did a debt jubilee.

Grant Williams: There are two wildly different outcomes at either end of the spectrum, but there is the same number of dots you can take from the start to each of those outcomes.

It could go this way, one, two, three steps, massive inflation, currency collapse. One, two, three steps in this direction, deflation, yields go down.

Bill Fleckenstein: You can't really get to deflation, because they took their debt to GDP from 400% to 200%. I mean, they have the bonds. They won that round.

Grant Williams: No, I agree.

But what's the mindset in Japan?

The big problem they have is that big deflationary mindset.

Bill Fleckenstein: But now all of a sudden, if you were worried about deflation because you had too much debt and then you didn't have too much debt anymore.

How would you worry about deflation?

Grant Williams: As long as you can get the Japanese to go and borrow, which, I mean, I'm guessing ultimately you could.

But the problem is if you're Japanese, you haven't been able to inflate your debt away as everybody else can.

Bill Fleckenstein: No, but they don't need to inflate it away. They bought it.

Grant Williams: No, no, no, I'm talking about the new debt, because presumably once you get there, you then start lending again, you build up the debt again. The whole idea of expunging it is, so you can create it again.

Bill Fleckenstein: Right, right.

Grant Williams: That's the whole point of doing it.

Bill Fleckenstein: That's right, that's why I keep asking people, what will it look like on the other side of that? Because it seems like that's where we're going. Anyway.

Grant Williams: Well, I'll ask some of my buddies in Japan who we should speak to.

(End Of Transcript)

I don't know if I can give Bill or Grant any specific answers, but I can go through my thought process, because I've really been trying to figure this out myself, and maybe that can help them out when they do get that pro that understands the Japanese market on a future episode of The End Game.

The first thing that they actually discussed in this episode is that rates could skyrocket.

The reason is that all the individuals that are left holding the rest of the bonds that weren't on the bank's balance sheet or the central bank's balance sheet, in this case, the BOJ, would immediately want to sell their bonds because they might think that they're next.

In other words, if the government and the central bank are willing to go to these extremes maybe they'll cancel all the debt and whoever is holding those bonds is going to be left holding the bag.

The bottom line is it creates more uncertainty so those people would be incentivized to sell.

The more selling, the more supply, and if prices go down, interest rates go up.

One effect of a debt jubilee they didn't go over in the podcast that I've been thinking through extensively is the central bank wouldn't be able to reduce the size of its balance sheet.

Assuming the Bank of Japan controls interest rates the same way as the Fed, through something called IOER (Interest On Excess Reserves), they would have a mechanism to control lending or try to reduce the amount of lending if inflation ran hot, but they wouldn't have that other tool.

To explain this further, look at this whiteboard.

Let's go into the potential issue of the central bank not being able to reduce its balance sheet. Here's how it works.

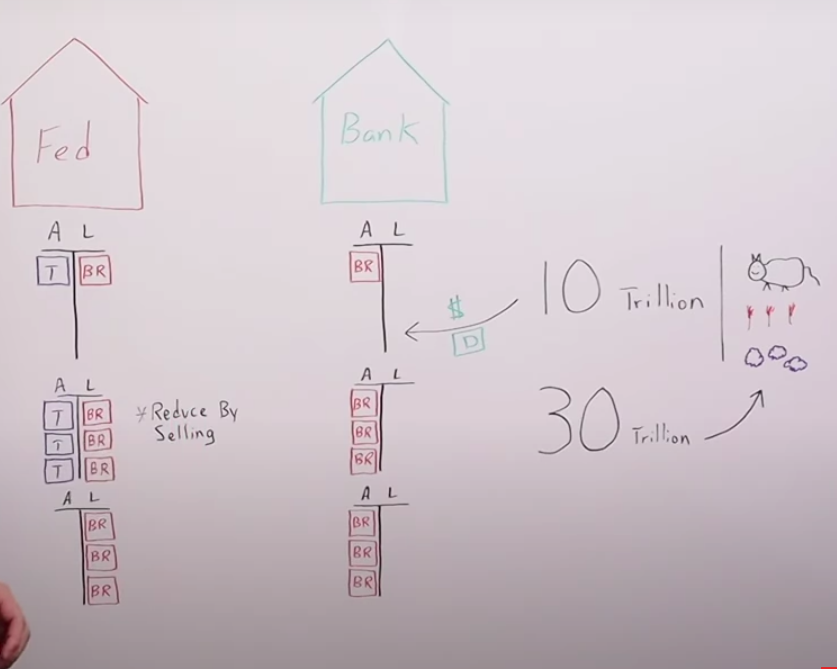

On the left is the Fed, but this could be the BOJ or any central bank, and then there is Bank A or XYZ on the right.

The Fed has assets and liabilities and so does the bank, that's their balance sheet. On the assets side, they have treasuries or any government debt, and on the liability side, bank reserves.

Those liabilities are assets of the banking system, and the bank reserves are what gives the banks themselves balance sheet capacity to create loans.

Just the easy way to think about it is the more bank reserves they have, the more loans they can create. It's not to imply they loan out the bank reserves.

Just to get your mind around it, the more of these reserves they have, the more loans they can create in the real economy if there's demand, and the banks see opportunity.

For the sake of the example, let's say that with one block of bank reserves, the banking system can lend out $10 trillion. If they create $10 trillion of loans, they're creating $10 trillion of money supply.

Stated another way, they're creating $10 trillion of bank deposits or bank liabilities in the commercial banking system that is there to chase goods and services in the real economy, like cattle, wheat, or cotton.

If the Fed does quantitative easing or whatever they do to create more bank reserves, that gives the banking system additional balance sheet capacity to create more loans.

If they added another two blocks of bank reserves, whatever that represents, then theoretically, the banking system could create $30 trillion worth of loans.

$30 trillion worth of bank deposits or liabilities and $30 trillion of money supply chasing the goods and services in the real economy.

Let's think this through. The way the central bank reduces the supply of bank reserves in the system is by selling assets.

They take those treasuries, sell them back to the bank, and then they go ahead and delete those bank reserves. So the bank is using the bank reserves to pay for the treasuries effectively.

But if there are no treasuries, if there is no government debt because they do a debt jubilee, then they can't reduce the number of bank reserves in the system.

That would mean they can't reduce the balance sheet capacity of the banking system and they would have no way to control all the additional loans that could be created or all the additional money supply going out into the real economy chasing goods and services.

I'm not saying that this would be catastrophic, especially in a place like Japan, where they've really battled deflation, but what I am saying is this would be an effect of a debt jubilee that we need to think about.

Maybe the pros out there that know a lot more than I do can take this idea, run with it and give us some potential outcomes where we could look at it, weigh the probabilities for ourselves, and determine what happens if the government tries a debt jubilee.

I think the next issue that would arise would be a moral hazard.

If you wipe out the government's debt or a percentage of that, all the politicians are going to think that there's free money just growing on trees and they could just spend to infinity and beyond, Buzz Light year style …

And, there is going to be no downside whatsoever and it will distort the economy. But also, I think especially with today's societal narrative, they'd probably try to wipe out consumer debt.

Now, that could have some positives, but there's always a cost-benefit analysis, and what you'd be doing is creating a lot more M2 money supply.

Why is this?

Because when consumers pay down debt, it destroys debt. If there was no debt to pay off, any additional debt created would increase the money supplier currency units that were in the real economy, and this could be highly inflationary.

And just to make myself clear, when I say inflationary, I'm talking specifically about consumer prices.

Now, let's go ahead and pull it right back to the United States. I want to discuss debt consolidation and how we need to think about this in terms of the repo market.

That's really crucial when you're thinking through the dollar funding markets and how this could differ from a scenario in Europe or Japan. For those of you who haven't seen all my repo market articles, I'd highly suggest checking them out.

We were doing them last year around September, for obvious reasons, but we'll go through a quick review.

The collateral used in the repo market by hedge funds, financial institutions, and banks are usually treasuries and mortgage-backed securities. Prior to 2008, it was not a big deal because banks were accepting mortgage-backed securities as collateral for repo transactions the exact same way they would the treasuries.

But post-2008, that was no longer the case. I mean, think about it.

If you're a bank wanting collateral, do you want anything to do with mortgage-backed securities?

I don't think so.

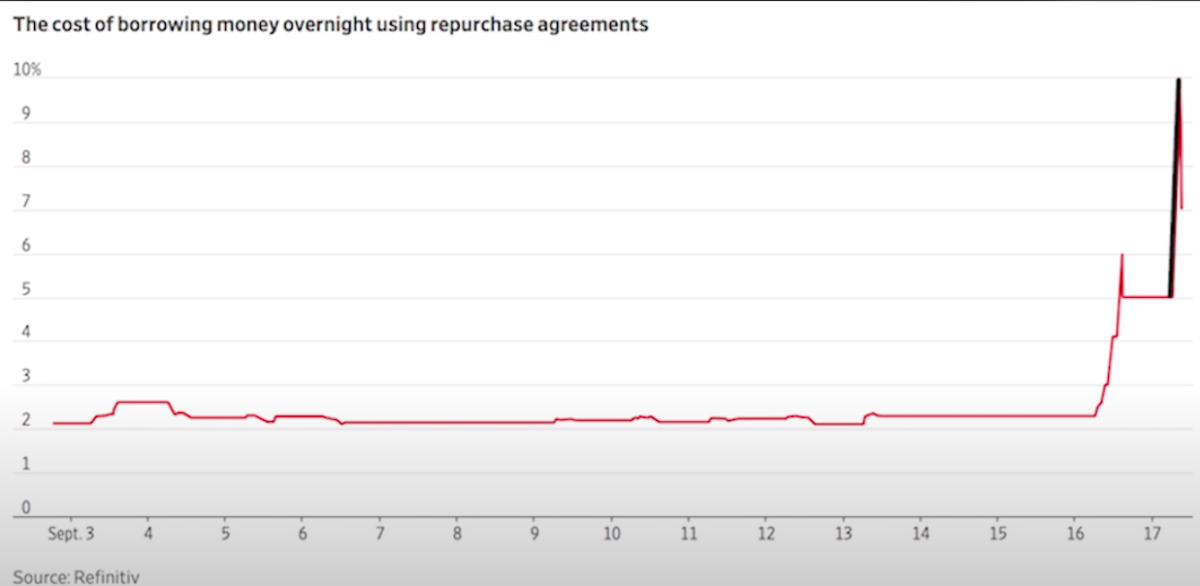

Back in September of 2019, for a variety of reasons, there was a bottleneck where the banks that needed overnight funding, needed cash and they needed it quick.

They didn't have anything other than these mortgage-backed securities to offer as collateral. I'm getting all this from my conversations with Jeff Snyder, just FYI. This isn't my idea. I am deferring this one to Jeff.

The banks had these toxic mortgage-backed securities, and maybe some of the banks themselves were toxic.

Maybe those counterparties looked at them and said, “No, I don't want anything to do with Deutsche Bank or HSBC.”

But as a result of there not being enough collateral or a bank being insolvent, or just this bottleneck within the system, the interest rates skyrocketed up to 10%.

Why was that really bad? Because it brought all the interest rates up, including the Fed Funds Rate.

So momentarily, the Fed lost control of all the interest rates, including the all-important Fed Funds Overnight Rate.

And to solve the problem, which was of course not a solution, only a band-aid, the Fed came in and did another round of quantitative easing.

But whatever you do, don't call it quantitative easing. Remember Jerome Powell, he was reprimanding us.

He said, “You Austrians, people on FinTwit, shut your mouths. I don't want to hear you call this quantitative easing.”

This is not QE. In no sense is this QE. This is nothing like it at all.

Jerome Powell

What he was create bank reserves to buy treasuries from the banking system. But you'll remember that initially they started off buying T-bills, short term treasuries.

But going back to my conversations with Jeff Snyder, you know that the most pristine collateral in the repo market is? T-bills, the exact same thing that the Fed was buying.

The banks went to the Fed, said, “Whoa. Whoa, whoa, timeout. You can't buy any of these T-bills because you're exacerbating the problem.”

What did the Fed do?

They started buying treasuries that were further out the curve, meaning the maturity was longer, so they started buying 5,10, and 30 year treasuries instead of these short-term ones that the repo market needed to function well without interest rates spiking again, causing the entire system to collapse.

You may be saying to yourself, “Okay, George, I get the repo market”.

But what does that have to do with a debt jubilee?

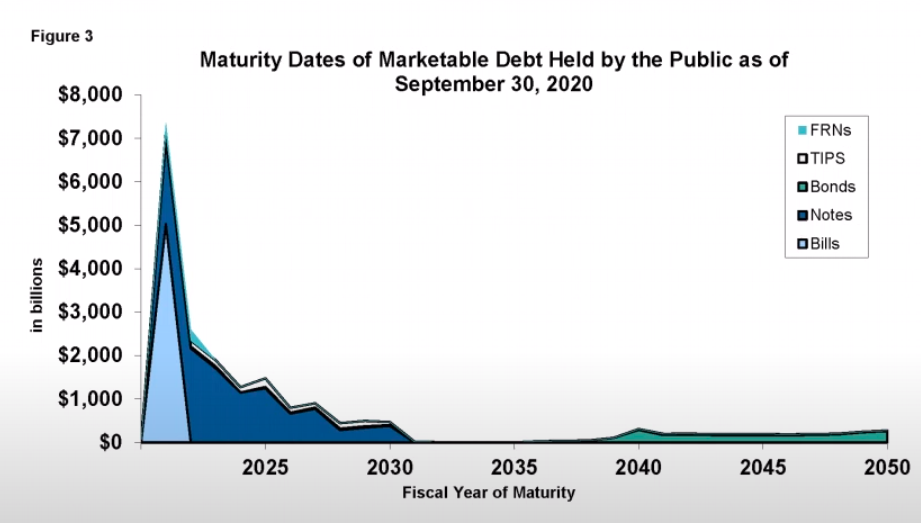

This takes us to our next chart.

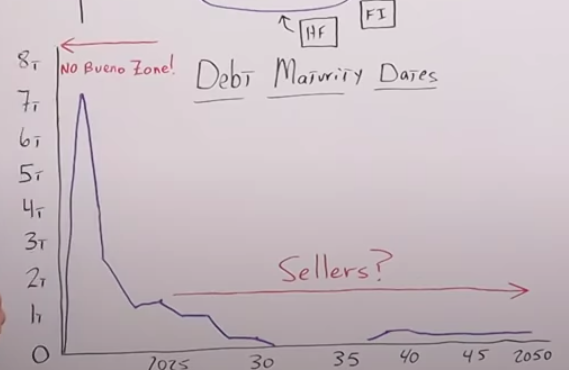

It starts off today, in 2020, and goes to 2050. This represents the debt outstanding for the Federal government as far as the maturity.

On the left, it went from $1 trillion all the way up to $8 trillion. This chart tells us the majority of the debt outstanding is very short term.

If the Fed wanted to execute on this debt jubilee in a way that would actually matter, they'd have to own a higher percentage of the outstanding debt.

They would have to start by buying longer maturity bonds or treasuries.

Why?

Because they found out the hard way that if they buy short-term T-bills, that's going to create the same problem we had back in September, interest rates are going to spike and the economy is going to collapse.

Any of the outstanding bonds in this area, the short-term T-bills, are in the no bueno zone, for sure. The Fed cannot buy because they need them circulating out in the economy and in the repo market.

Think this through, they really can't buy any of the longer maturity treasuries either because…

Who's going to sell?

First of all, you don't have that many out there, and…

Are you going to buy them from the pension funds, from the insurance companies?

No, they need them in their portfolio. So the Fed's really stuck.

The government really can't do an effective debt jubilee unless the Fed just buys all of the future debt issued by the government, when we take our debt to GDP up to 200% or 250% where Japan is now.

And that takes us to our final question that I addressed back.

-

Does the debt jubilee even matter?

-

If it's just electronic digits on two balance sheets, would anybody even know?

Maybe there is a free lunch.

What Is The Real Problem With The Debt Jubilee?

What I mean by this is everybody, when they look at a debt jubilee or the negative ramifications, is looking at what may happen in the future, myself included.

I think, after I've thought this through for a long time, we shouldn't be asking the question of, what would happen in the future if there's a debt jubilee?

We should be asking ourselves:

What happened in the past?

Like I mentioned earlier, the accounting of a debt jubilee is very simple, It's just electronic digits.

You click a delete button on the liabilities side of the government's balance sheet and another delete button on the asset side of the central bank's balance sheet, and, poof, it's gone.

If you didn't make an announcement, no one would really even know. Everyone wakes up the next morning, and business is as usual. But…

Does that mean that there's free money the government can just wipe out and continue to spend like drunken sailors and we're off to the races?

Absolutely not, because all of the damage was done in the past, all of this economic catastrophe that we're looking for with interest rates going up, inflation going up, a huge debt deleveraging, or a deflationary downward spiral into oblivion. It all happened before.

It all happened as the debt was being accumulated. Here's what I mean.

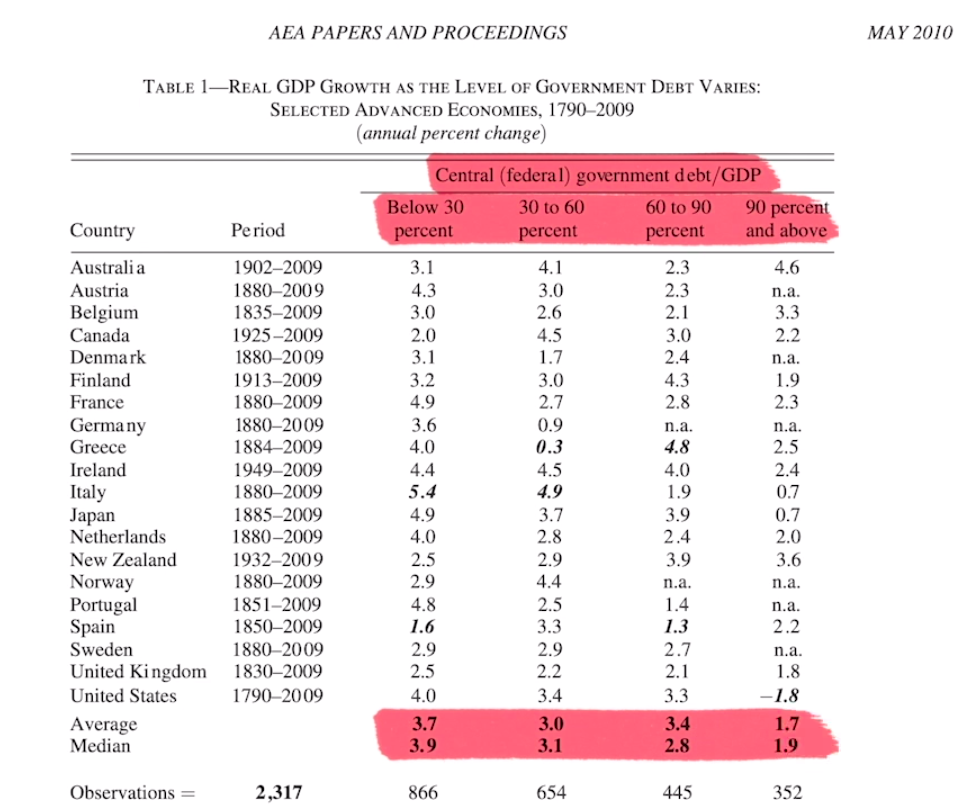

If we look at the 2010 study from Reinhart and Rogoff, Dr. Lacy Hunt, one of my favorites, references this all the time, and it shows that as government debt goes up, real GDP goes down.

This makes a lot of sense if you just think of it very simply in these terms.

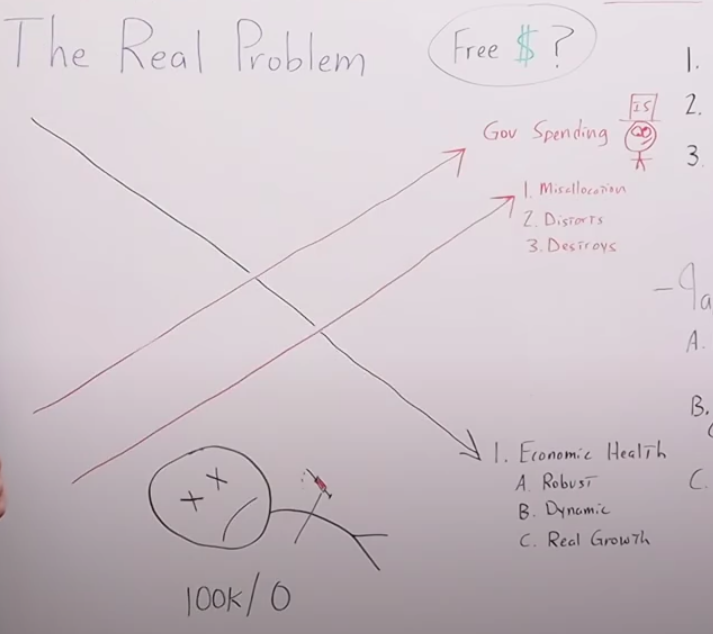

As the government spends more and more as a percentage of GDP, it misallocates more resources. It distorts the economy, and continues to destroy it.

So, government spending goes up, misallocation of resources and distortions go up at the same rate, while economic health goes down and deteriorates.

The economy becomes less robust, less dynamic, and as they showed in their 2010 report, real economic growth goes down.

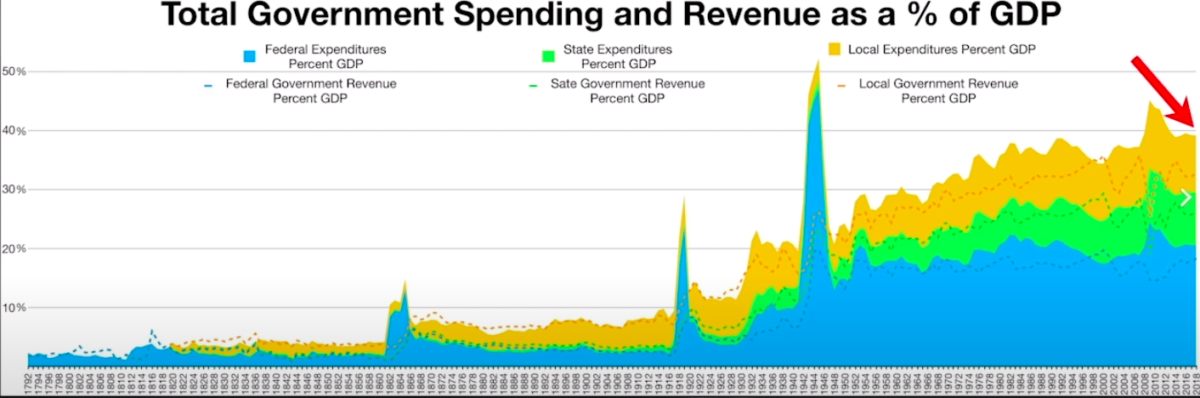

Let's not forget that back in 2019, prior to the coronavirus, government spending was about 40% to 45% of GDP.

I would say government spending is almost at 60%, meaning the private sector's only responsible for 40% of economic output in the United States.

Also, to give you some alarming facts, let's look at the deficit for 2020. It's about $5 trillion.

You could say, “Well, big deal, George.” But, let me give you some context.

Between 1776 and 1996, the first 220 years of the existence of the country of the United States, It racked up about $5 trillion in debt. So we'll accumulate just as much debt this year as we did in the first 220 years of the United States.

Think about how many resources are being misallocated, how wildly the economy is being distorted and destroyed in 2020.

But I think the easiest way to look at this is taking an analogy from my good buddy in Puerto Rico, Peter Schiff.

When the government spends more and more as a percentage of GDP, the economy gets addicted to the spending, just like a drug addict gets addicted to heroin.

Look at this example:

This guy is passed out on the sidewalk, most likely in San Francisco, and he has his needle leaking out, or whatever it does.

Let's say that he accumulated $100,000 in debt buying drugs to become a drug addict. But we came in and gave him a debt jubilee.

We took his debt all the way down to zero. Now, the drug addict can get up off the sidewalk and go buy another $100,000 worth of drugs.

Is he any better or is he actually worse off?

It's the exact same with the government, the damage was done while they were accumulating the debt that needs to be written off in the debt jubilee.

The only thing that will do by wiping the slate clean is to give them more ammunition to buy more and more drugs and make the economy even worse than it already is.

What's the solution for Japan?

Of course, it's to reduce the size of government. It's to do the opposite. It's the increase of free-market capitalism. Let businesses fail, for heaven's sakes.

Don't micromanage the economy, whatever you do, don't fix prices. We know this doesn't work with goods and services.

So why should it work when we try to fix the price of money itself?

Money is one-half of every single transaction, so when you fix the price of money, in other words, interest rates, what you're doing is you're manipulating the price of every good and service that's sold within the economy.

Stop fixing interest rates, get rid of the central bank, and let Schumpeter's destruction, the free market, and the individuals in the real economy, the average Joe and Jane just like you and I get the shackles of the government off their shoulders.

Let us go out there, create goods and services, increase the standard of living for everyone involved, and create a healthy, robust, thriving economy.

Going back to our original question… The debt jubilee may be a simple solution, but it's evidence of a system collapse.

It might not necessarily be the catalyst of a system collapse. But to know for sure, we'll probably have to wait for that future episode of The End Game with Grant Williams and Bill Fleckenstein.