Initial Public Offering: The Mechanics Of A Scam

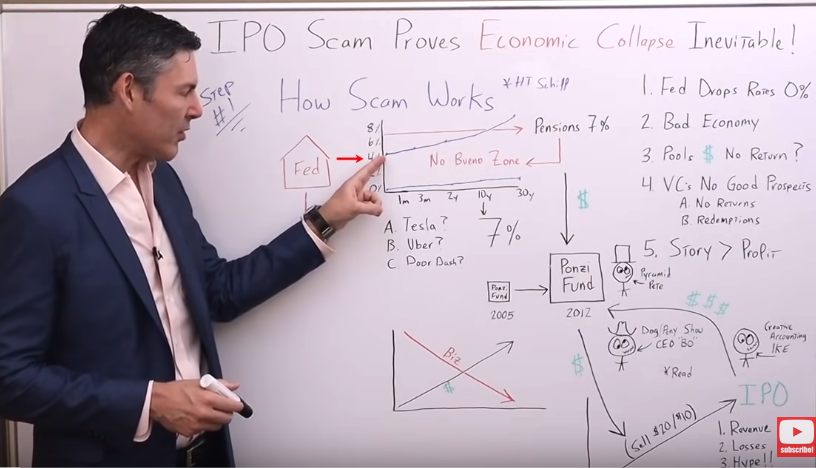

As you would imagine, it all starts with everybody's favorite entity of central planning, the Federal Reserve. They dropped rates down to zero and completely distorted the yield curve.

The image above shows an example yield curve of the treasury market, which goes from one month to 30 years. On the left, it goes from 0% to 8%. Before the Global Financial Crisis (GFC), rates were far more normal.

At the bottom of the graphic, I will assume the overnight rate was close to 4%, and as the maturity increased, the interest rates went up.

This makes sense because the longer you lend your money to the government, the more they should pay you, as you risk being paid back in cheaper, devalued dollars.

The increase of interest rates worked well for pension funds and large pools of money that needed a 7% return to meet their obligations.

The government could just go in and buy 10-year treasuries, and they would be good to go, but when the Fed came in and dropped the whole curve down, they could only get 1.5% for those 10-year treasuries they bought.

A big delta between 1.5% and 7%, which is the percentage they need to meet their obligations. This takes the government right into the “No Bueno Zone”, where they are underfunded. Big problem.

So what do they do?

They have to go further out the risk curve. They have to take more risks to get the same return they were getting before just by buying 10-year treasuries.

So, this leads us to the question:

Would we even have companies today, like Tesla, Uber, and DoorDash -the most recent debacle- if it weren't for the Fed dropping interest rates artificially low?

If the big pools of money, like pensions, could have sat back and got the 7% return with no problem…

Would they have taken all the risk required to not only fund these companies but continue to fund them as they burn through cash?

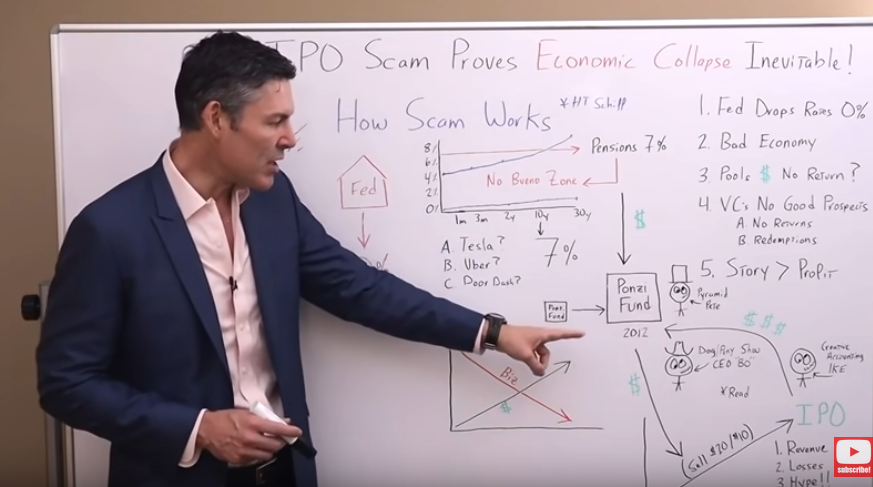

It's an interesting thought experiment, but what the pensions did was go to venture capitals. To explain it better, I want to introduce you to a new character on my whiteboard, his name is Pyramid Pete, and he is a venture capitalist fund manager.

In 2005, his fund, the Ponzi fund, was very small, and he looked for companies that had profit potential (a very antiquated model, I know). So, all the pension capital was flowing into the Ponzi fund, which had tripled or even quadrupled its size, but… Pete had a problem.

As the money that was coming into his fund increased, the amount of profitable businesses, or the amount of good business opportunities out there to invest were decreasing.

The Global Financial Crisis has shown us that there are structural flaws in the economy which were never fixed, they just got papered over. As a result, those business opportunities out there are far and few between.

Since there aren't any businesses that can make a profit or there are very few relative to the amount of money that Pete has to put to work, he has to come up with an idea.

What does he do?

He says, “I'm going to forget about businesses that make a profit. I'm going to focus on businesses that have a fantastic story. I'm going to have to dump a ton of money into businesses, but when they go public, I'm going to be paid back in spades.”

The problem here is, when they go public, Pete has to have a lot more money from that IPO than he would need if it was just a profitable business that was going public to expand their profitable operations.

To dive into this further I included a transcription from my good buddy, Peter Schiff, who gave me the idea for this article. He compared Microsoft to DoorDash and Airbnb. It's a fascinating story:

“Microsoft went public in 1986, but when they went public, they were making a lot of money. It was a very profitable software company, and in that IPO in 1986, Microsoft raised $61 million. That's it. Now, let's compare that to the IPOs for Airbnb and DoorDash.

Each of these companies raised approximately -I don't remember the exact amount- but each of these companies raised about three and a half-billion dollars in their IPOs. Three and a half billion. Microsoft only raised 61 million.

Now, I know there's been a lot of inflation since 1986. If you take the CPI, which is the government's version of inflation, I agree understates it, but let's just use the government numbers for this analogy.

In 1986, this Consumer Price Index was at 110. Today, it's at 255, so if you adjust the Microsoft IPO for the CPI, for Airbnb or DoorDash to have raised an equivalent amount of money that Microsoft raised, their IPOs would have been 140 million.

Instead, they're more than 20 times that. They're not raising 140 million, they're raising three and a half billion.

What are they going to do with the money?

Other than subsidizing their existing losses because they're hemorrhaging money, Microsoft wasn't losing any money. It was making money.

Microsoft needed that money to expand, to take a viable business model that had proven to be successful, and to expand it into a much larger company by tapping into the public markets to raise capital.

DoorDash and Airbnb don't need to tap into the public markets to raise money. They've already raised billions in the private VC market.

That market didn't exist in the Microsoft days. It exists now, and in reality, the only reason that we have IPOs today is so that the VC investors can cash out.

It is not so the companies can raise new money to expand. They've already raised all the money they can. They've expanded the businesses as much as they can, and now they want to payday, but the one thing they haven't expanded is their earnings because they don't have any.”

(End of transcript)

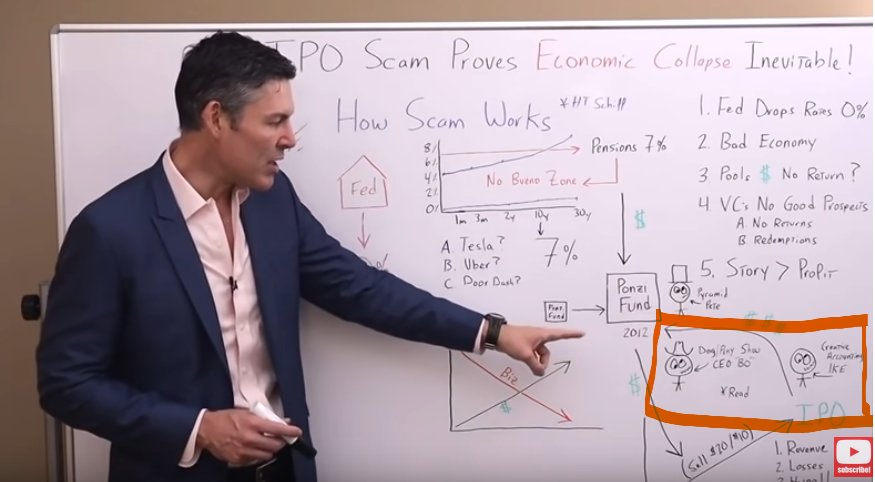

Once Pete finds a company with a good story, he has to hire a couple of other individuals to create all the hype required for a huge IPO, so he looks for his buddy, dog and pony show, Bo. He is the CEO and he can sell ice to an Eskimo.

Then, the last piece of the puzzle is a creative accountant, in this case, Ike, as shown above. He can fudge the numbers and create new metrics that make the company seem like it is wildly profitable. However, when you look at their bank account, they are incinerating cash.

It's a very neat trick. Bo and Ike go on their dog and pony show, create the hype needed, and Pete just keeps pumping more money into this company that is selling $20 bills for $10.

As you can imagine, their revenue is skyrocketing. The media buys this hook, line, and sinker. You throw in some social media echo chamber, and all of a sudden, they have a huge IPO, plenty of money to cash out and make Pete a very rich person to pay off those pension funds that need the 7% return.

Again, none of this would have happened if The fed hadn’t had dropped rates down to 0%. Please keep that in mind.

Another IPO example is WeWork, which almost went public but didn't make it, and then completely collapsed. I delved into this article from Bloomberg written just before WeWork's IPO collapsing in on itself:

The New York-based company will test public investors' appetite for cash-burning startups. WeWork lost $1.9 billion last year. Uber, however, lost $5 billion in just the second quarter. More than just its cash-burning ways, WeWork's IPO will test investor tolerance for made-up accounting metrics as well. You might recall Community Adjusted EBITDA, the gauge WeWork devised to measure net income before not only interest, taxes, depreciation, and amortization but also building and community-level operating expenses.

What they're doing is adding back the majority of their expenses, and somehow claiming them as equity to make it seem as if they were not burning through billions of dollars. This is a great example of creative accounting.

How Do Retail Investors Play Along With The Game?

You're probably asking yourself, “Well, if Pyramid Pete is creating these story companies that don't make any money…

Doesn't the retail investor see through the charade?”

When we check out specific companies like DoorDash, you may ask:

How can anyone invest in this company that is just burning through money?

The data from Yahoo Finance below displays what I am referring to, but when you look at their competitors, such as Uber, it doesn't get much better, they lose a lot more money. Then Grubhub, their direct competitor, incinerates money as well.

-

So how does the average Joe character fall for this nonsense?

-

Why does he go in and buy companies hemorrhaging money?

If we think about what influences him today, it starts to make a lot of sense. For the last couple of decades, it's been ingrained into his head there is a Fed put, “so always buy the dip, and you'll make money.” He turns on the TV, he sees CNBC, and all he hears is, “Buy, buy, buy.”

Then he looks at the government, and they are saying, “Don't go outside. Don't open your business. Don't walk on the beach. There's danger everywhere. We want you to lock yourself in your house, and we'll pay you to stay there, so whatever you do, don't go out and start a business. No way, that is way too risky.”

He looks at the real economy and sees very few opportunities. It's not like it was in the good old days, where you could go out there, work hard and get ahead.

Now, the only way to get ahead is to buy assets and hope they go up in price. He then looks at his Instagram account, and everyone he follows is getting rich buying stocks.

He's looking at their Lamborghinis, their travel lifestyles, and wondering why on earth he isn't doing the same.

Then, he looks at his other social media accounts, and of course, he follows people that have the same belief system he does, so it creates an echo chamber, where he doesn't hear anything outside of the facts that he wants to hear.

This generates tremendous FOMO -fear of missing out- and all the people that he follows say not only, “Buy the dip,” but, “You should buy XYZ asset. You should buy Uber. You should buy DoorDash. Buy Airbnb, and you're going to get rich just like me.”

Lastly, DoorDash is one of the brands that so many of the young retail investors right now have experience with. Think about it. They're locked inside their house, they can't go to the store without putting on a hazmat suit, so of course, they're going to get the food delivered. The delivery driver shows up in a Prius, working for DoorDash.

Every single time you get food, you see the brand, therefore, the average Joe thinks the brand is huge and printing money.

To go further into it, I examined an extract from Jim Cramer in a CNBC clip that can shed some more insight on the psychology of what's going on with the average Joe and the IPO scams, as DoorDash:

“But look, the one thing is certain, Carl is that this newer brand of investors I've been profiling on may have money, have a lot of capital. A lot of people say:

“Well, where did it come from?”

I don't want to even ask that. I just say they like things, and when they like things and they use things, actually the old Peter Lynch model from Magellan Fund for a long time at Fidelity, they're willing to keep buying. Look at Snowflake.

I mean, I might speak to Frank Slootman. He's not sure exactly who his investors are, but he knows a lot of them are retail investors. DoorDash is used by a lot of younger people, both in the suburbs and in the cities, so I think that you're going to see incredible enthusiasm. I wish that people would use limit orders, but that is parlance, Carl, that they don't understand. They don't get that.”

(End of transcript)

Along with the dog and pony show with Bo and Ike that I mentioned earlier, we also need to remember that…

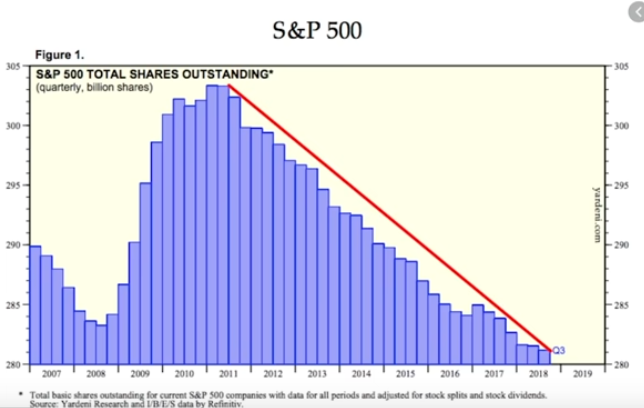

Since 2008, the banks have been expanding their balance sheets almost exclusively to lend to big corporations. Then they go out, take that money, go into the stock market, and buy their shares back.

This chart of shares outstanding for the S&P 500, has gone straight down since 2011 as Corporate Debt has climbed to all-time highs.

There is one more piece of information I added here, and it tells its own story:

People whose Facebook friends experienced a five percentage point larger house price increase over the past two years, are 3.1 percentage points more likely to transition from renting to owning and will pay 3.3% more for a given house, make a 7% larger down payment, and buy a 1.7% bigger house.

This shows us how outside influences dramatically impact our decision-making process when it comes to investments, and it gives us insight as to why the average Joe is so susceptible to buying into the IPO scams.

Natural Selection Applied To The Economy

I'm sure you're following along with everything I mentioned earlier, but you might be scratching your head, saying, “George, okay, I get it, but…

How do IPO scams lead to an economic collapse?”

Here's how I think it happens:

Just like natural selection in the evolutionary process, the strongest survive. Their genes continue onto the next generation, making the species as a whole, a lot stronger. It's the same thing in free-market capitalism and the economy about profitable businesses that create goods and services.

I want to go back to some of my more recent articles where I've outlined what exactly is wealth.

Is it just green pieces of paper?

No. Wealth in society is the number of goods and services that society produces.

So, if we are funding companies like Doordash, WeWork, or Airbnb, instead of strong companies, we are funding the weak businesses that don't produce any goods and services.

They might just produce them temporarily, or they can only produce them if they're subsidized. What companies like these do well is create great stories, but at tremendous losses.

As we continue to prop up and fund businesses that can't produce goods and services sustainably, the only thing they produce is a $20 bill they sell for $10.

Over a specific time, we have fewer companies out there producing goods and services that create the wealth of society. It's just like the giraffes, the savanna, trying to eat leaves from the trees. What we're doing right now is funding the short, fat giraffes, when we should be funding the tall, thin giraffes with the long necks, that over a long period, will be able to survive.

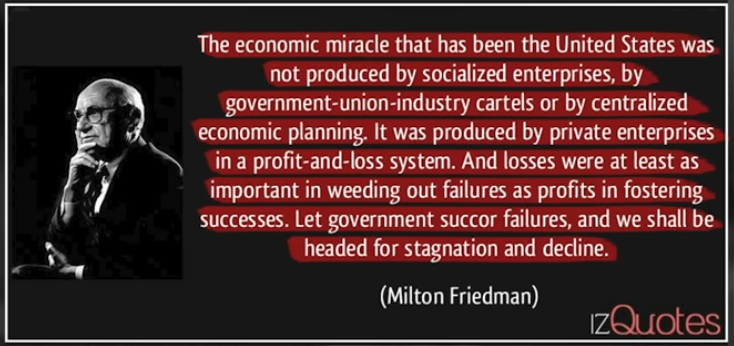

This whole process works in reverse, and what we end up with is, instead of a strong economy, we have one that over the long-term becomes weaker. No one points this out better than Milton Friedman himself:

Comments are closed.