Is money printing set to explode? The short answer is yes. I don't even think most people understand the magnitude of how much it's going to explode.

But, what I find is most people really don't understand what money printing actually is. They really don't even understand money.

So before you can figure out how money printing is going to affect your financial future, you have to understand how it works.

I'll explain it to you in seven simple steps in the form of a series of articles named: Is money printing set to explode? This is part 1 of 7.

Do you want to take your investing to the next level? Check out my new Online Investing Forum! I have partnered with Lyn Alden and Chris MacIntosh to bring you the BEST Investment Tool on the Internet Today – Rebel Capitalist Pro! Check out our 7-Day Trial Membership Promo for only $1! Visit GeorgeGammon.com/rebel-capitalist-pro. Are you positioned to profit from the 2020 Election Cycle? Watch for Free: Election Cycle Investing with Lyn Alden and George Gammon.

Banking Mechanics: Spending And Transfering Money

How does it work when we actually spend or transfer money?

I call it “Fugazi”, just like Matthew McConaughey does in the movie Wolf of Wall Street. Here is a transcript of his explanation:

Matthew McConaughey: It's all a Fugazi. You know what a Fugazi is?

Leonardo Dicaprio: Yeah, Fugazi. It's a fake.

Matthew McConaughey:Yeah. Fugazi, fugazi. It's a wazy, it's a woozie. It's fairy dust. It doesn't exist. It's never landed. It doesn't matter. It's not on the elemental chart. It's not real. Right?

Leonardo Dicaprio:That's right.

(End Of Transcript)

“Money in your bank account” is just like Fugazi. It doesn't even exist. It's not there. It's like pixie dust, and I'll show you what I'm talking about.

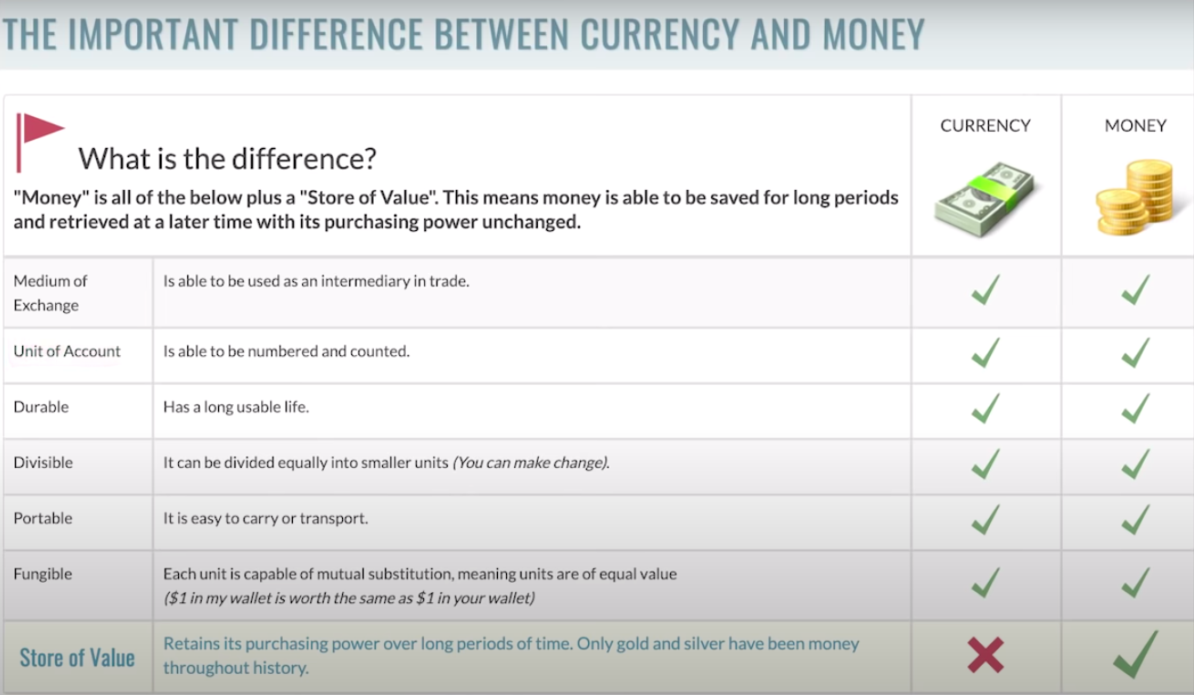

When I mention money, I'm not referring to the classic definition that Mike Maloney as an example would use.

Store of value, medium exchange, durable, divisible, portable, fungible, unit of account. I'm not referring to that.

I'm referring to just the average definition that the person walking on the street would give you, “Oh, it's just the money in my bank account.”

Also, as we move on, we're going to reference a fantastic blog post from my partner in Rebel Capitalist Pro, Ms. Lyn Alden.

I'm going to reference that periodically. I would strongly suggest reading that when you're done reading this article.

It really dives into the nitty-gritty of money printing, quantitative easing, and how it works with the consumer, the banks, the fed, and the treasury's balance sheet.

The mistake most people make when they think this through is they see the banking system as this entity that's just holding on to something physical you have.

As an example, you're going down to the local Wells Fargo to set up an account and you're taking a bag of silver or a bag of gold, or maybe a box of green pieces of paper and you're just giving it to them.

The average Joe thinks the bank just takes that physical stuff and puts it in a vault.

Then when you want to spend your physical stuff, it just goes from your vault to the bank of whomever you just paid, but that's not how it works at all.

The only thing we're doing when we're transferring money or spending it with a business is we're just transferring IOUs back and forth.

That's all it is.

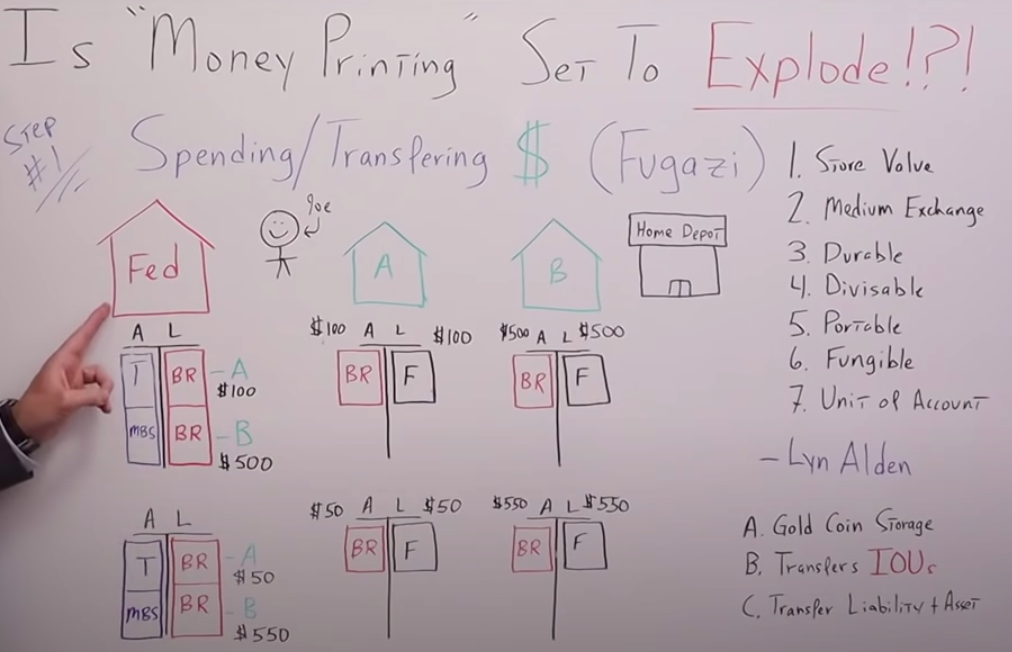

On my whiteboard, I drew the Fed, bank A, and bank B. Let's say the average Joe has an account with bank A and home Depot has an account with bank B.

The fed's balance sheet has assets, liabilities, assets treasuries, mortgage-backed securities, liabilities bank reserves. Bank A also has assets and liabilities. On the asset side of their balance sheet, those are the bank reserves.

The same bank reserves that are assets for the banks are a liability for the fed. On the liability side is the deposit account with Joe and the deposit account for Home Depot.

A deposit account is a very misleading term because there's nothing in here.

Again, it's all pixie dust. There's nothing. It doesn't exist, it's up in the air. All this really is, if it's anything, it's just an IOU.

Bank of America or bank A will say that it's like saying, “Joe, we owe you $100.” Therefore, when you look at your deposit slip, it's not a record of how much money you have in your account. There's nothing in your account.

Your account balance is just a record of how much money the bank owes you.

But, think this through. If Joe goes down to the local Home Depot to buy a hose and a rake, he spends $50. He doesn't give Home Depot $50, all he does is he transfers $50 of his IOUs when he swipes his debit card.

$50 IOUs go from his account to Home Depot's account.

Let's say we start with $100 and this isn't $100 in Joe's account, there's nothing in there, remember, it's Fugazi. The only thing that Joe has is $100 of IOUs.

He pays Home Depot and $50 of those IOUs get subtracted from his account and get added to Home Depot's account.

Now, bank B owes Home Depot $550 instead of the original $500. You see what's happened. No money has exchanged hands, the only thing that's gone back and forth are IOUs.

IOUs from the banking system to entities, individuals, or businesses in the private sector. But let's keep in mind, the IOUs going back and forth are liabilities of the bank.

Just like if you owe your friend $100. You have that liability, and that IOU to your friend would be an asset.

Since bank B has an additional $50 of liabilities, bank A has to send them some form of asset to back up that $50.

Because let's take it to an extreme, let's say that Joe spent a trillion dollars with Home Depot. Those trillion dollars of IOUs or liabilities would go from bank A to bank B.

If all bank A did was transfer a trillion dollars of liabilities to bank B, bank B would be bust. They'd be insolvent with negative equity.

So, what has to happen is that the asset has to go along with the liability for the bank's balance sheet.

What is the asset?

Bank reserves.

Now, I want us to go through the balance sheets one more time so we are all on the same page.

Bank A starts with $100 in bank reserves, $100 in, I hate to call them deposits because there's nothing there, but I'll call them $100 in Fugazis. Bank B starts with $500 in bank reserves and $500 in Fugazis.

After Joe spends the money with Home Depot, or basically gives Home Depot $50 IOUs, those IOUs go onto the balance sheet of bank B.

Now, the balance sheets have $50 in bank reserves for bank A and $50 in liabilities. Bank B has $550 in bank reserves and $550 in Fugazis. The Fugazis got transferred, but which is a liability.

The bank reserves got transferred as well. Those are the assets.

What happens to the fed's balance sheet?

The bank reserves that are assets for the banking system are liabilities for the fed.

So we started with bank A having $100 in bank reserves and bank B having $500 in bank reserves.

After the transaction, bank A now has $50 in bank reserves and bank B has $550.

Why, you may ask?

Because when the $50 in Fugazis went from Joe's account to Home Depot's account, bank A had to transfer the equivalent amount of bank reserves from their account at the fed to bank B's account with the fed.

The liabilities are transferred over, therefore the Fed's assets had to transfer over as well.