@Michael Ealy Interesting question,

“Is stupid money chasing millennials in your market.”

The Fed has created an environment of artificially low-interest rates which starves several groups of yield.

As we all know, it makes it much more difficult for managers of large pooled groups of money to provide an acceptable return to their investors.

These starving groups include hedge funds and private equity funds.

Most would respond with “boo hoo,” the poor billionaires, what will they do.

Stupid money is coming from yield-starved public and private pension funds

But the further you dissect the problem you see it's not just billionaire run hedge funds, but public/private pension funds, insurance companies, teachers unions, etc.

All of these groups, and more, are starving for yield and they'll do almost anything to get it…including going out much further on the risk curve than is prudent.

Adding fuel to the risk curve fire are the funds in Europe and Japan where rates are not just artificially low, they're negative.

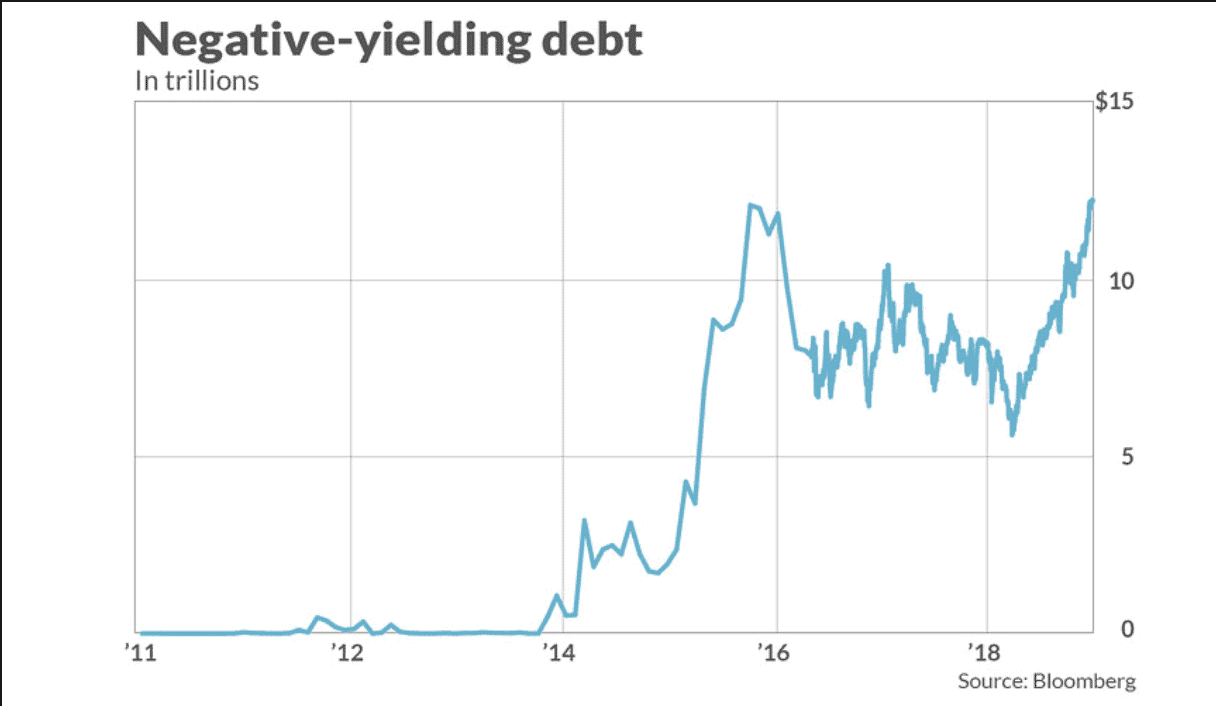

That's right, believe it or not, there are 13 trillion dollars of negative-yielding sovereign debt (and recently European corporate debt), floating around the worldwide financial system, formerly the bedrock of most funds portfolios.

In other words, there's upwards of $13 trillion that is no longer able to buy bonds. See chart

So what do you do if you're a fund manager? Go to cash? Do you think your investors will continue to pay you 2% and 20% management fees to be in cash?

They really have no choice but to be fully invested.

Bonds are not an option so do you go into stocks? Maybe, but where?

US market is at all-time highs and in the longest period without a recession in US history.

European banking (Deutsche Bank) is shaky at best and Australia/Canada are on the verge of having their housing bubbles pop.

My point is all things considered if you have to put large amounts of money to work, multifamily with a 6% cap looks pretty darn good.

Which by no means implies there's little risk, or all the “professionals” working for them know something you don't.

It simply means they have no choice but to go further and further out the risk curve.

Just because they go further out the risk curve doesn't mean it's less risky! 😉

IMO this may have something to do with Millennial housing preferences but it has much more to do with interest rates being at 5000-year lows and $13 trillion in negative-yielding sovereign debt.

My suggestion would be don't compete with them, there's far greater downside than upside.

If you have to buy US assets, buy them with 30-year fixed-rate debt. It's cheap and not available to hedge funds and private equity.

30-year fixed-rate mortgages are by far, the biggest edge small investors have based on current market conditions.

George.