Low-Interest rates Forever?

With 21 trillion dollars in debt and State & local pensions defaulting, can our government afford anything other than ZIRP without causing another Great Recession?

I see low-interest rates ‘forever’ on the horizon. How can they do anything else without causing chaos?

Can our government afford anything other than ZIRP?

Short answer: No, they can't even afford ZIRP. In fact, they can't afford the debt with NIRP.

The US government has to default on its debt.

Let me say that again, the US GOVERNMENT HAS TO DEFAULT ON IT'S DEBT.

Question is will they default the old fashioned way by renegotiating the debt or not paying, or will they default by paying the creditors back with dollars worth less than the dollars the government borrowed?

My guess is they'll pay with cheaper dollars.

In other words, they'll have to create inflation.

This gets at the heart of your point about interest rates being low forever.

Sure the short end of the curve can be low forever but the Fed doesn't have total control of the long end (10-year, 30-year.)

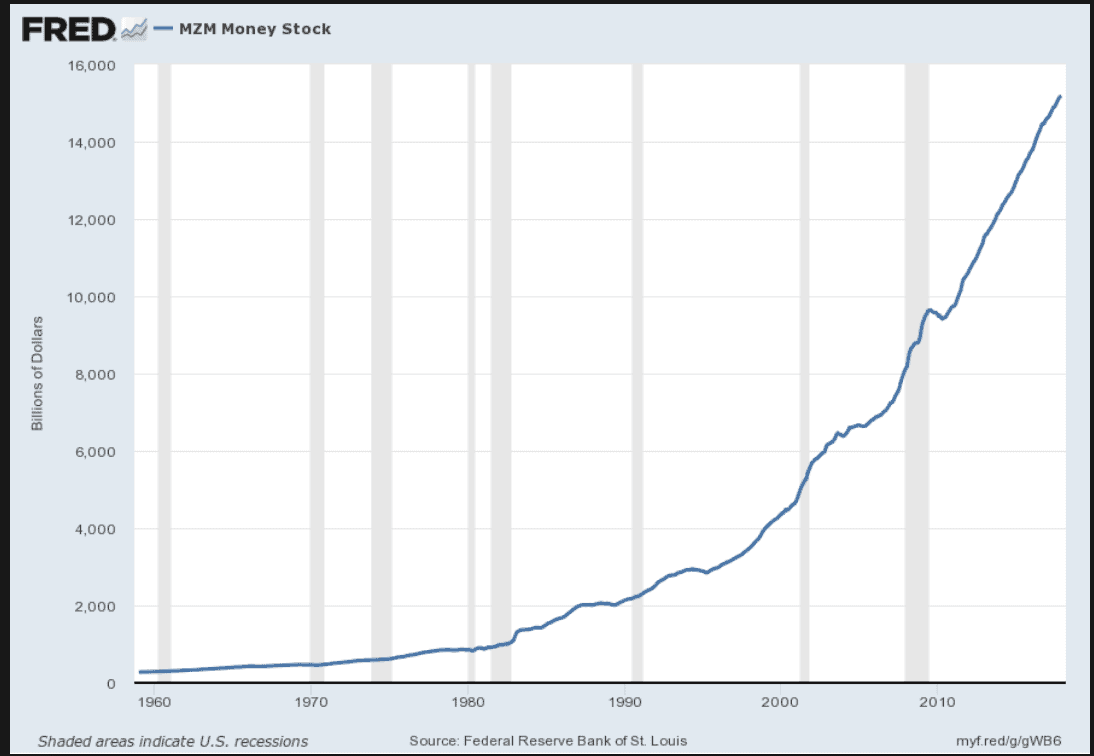

Central banks have suppressed the long end of the curve by buying those bonds but they have to “print money” in order to buy the bonds.

This is highly inflationary because you're dramatically increasing the money supply. See this chart of the US.

Why hasn't the world (US) seen more inflation?

It has.

It just hasn't shown up in the CPI but it's shown up in asset prices.

The point is, inflation is the only thing that can save the US from its fiscal issues, while at the same time, it's the catalyst that will most likely crash the US economy.

When inflation that the Fed's doing everything in its power to create, gets out of control, the US economy will be in serious trouble.

Let's think it through

Artificially low-interest rates create malinvestment (investments that wouldn't have been financially viable under normal market conditions/rates.

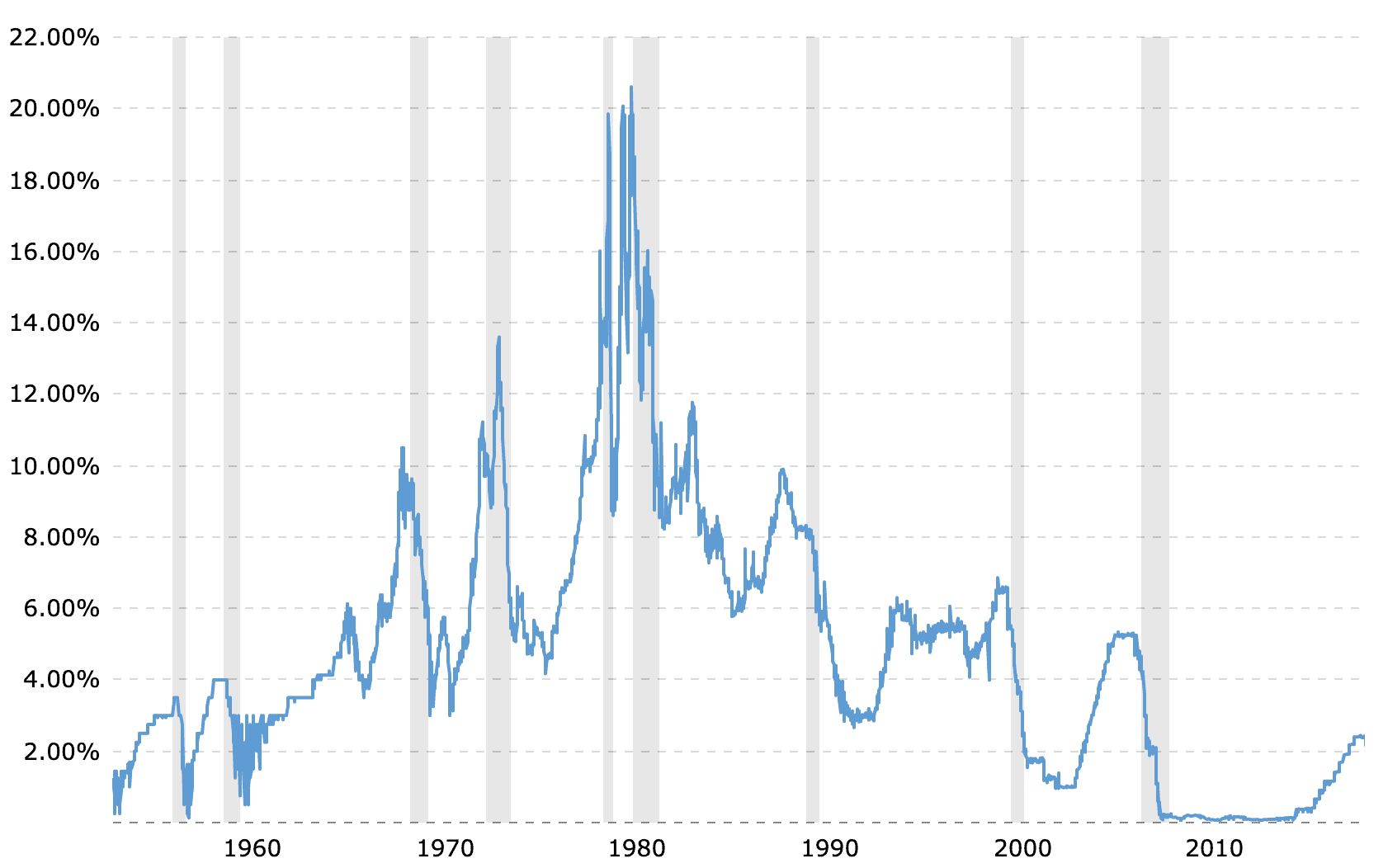

Remember fed funds rate average about 5%+. See chart)

If the fed funds rate is 5% and we have a steepening of the yield curve, where does that put the 10-year or mortgage rates? Maybe 7.5%?

How about commercial loans on all these multifamily complexes being built? Maybe 8.5%?

Think about how many investments have been made since the GFC and ZIRP…how many would be able to service their debt if they had to roll it over at 8.5%?

If that were to happen the Fed would most likely do more QE to bail out the economy but that creates more money, which adds fuel to the inflationary fire.

The only solution then is Volcker style crushing inflation with 20% interest rates.

Unfortunately, this time around that won't be possible because the US couldn't afford the interest payments on the 23 trillion in on-balance-sheet debt.

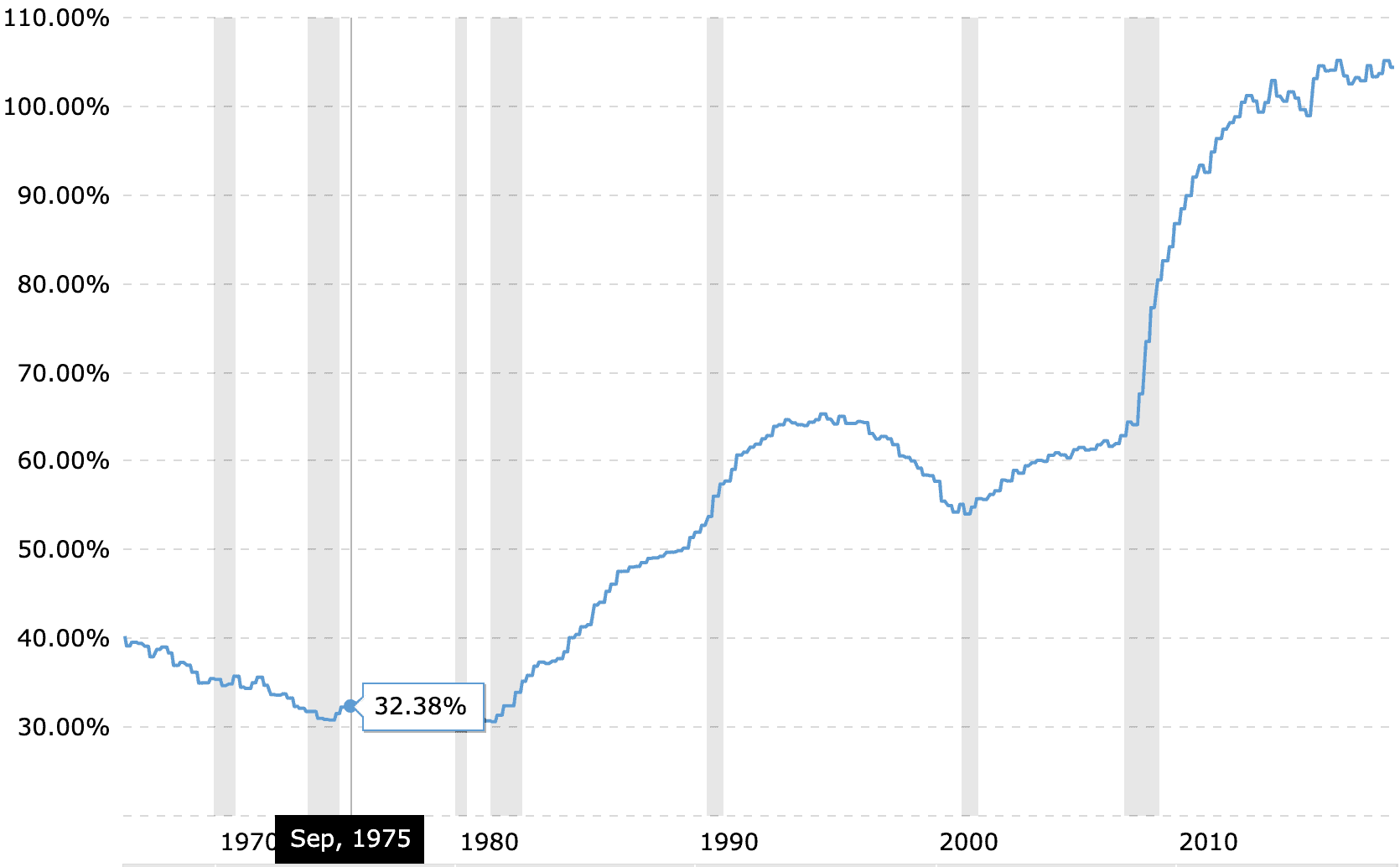

Compare our current debt to GDP ratio to 1980. See chart

The US currently pays about 500 billion a year in interest, and at a 2% interest rate. At 10% it would be 2.3 trillion, and let's not think about 20%. 😉

How would the gov pay for the massive deficits?

By issuing more bonds, but more bonds increase the money supply putting more upward pressure on rates. You can see the vicious cycle.

So the short answer to your question is the Fed doesn't have total control of the long end of the curve. The long answer in the next decade, the Fed might not have control of any part of the curve.

Most people's rebuttal is the US will be Japan, interest rates will be low forever.

What I preach till I'm blue in the face on BP is you have to look at probabilities NOT possibilities.

Is it possible the US turns into Japan? Sure, but is it probable?

And let's not forget, the US becoming Japan is our BEST CASE SCENARIO.

In other words, the most optimistic outcome is a 30-year depression.

Those who make the Japan rationalization, are usually people who'd be crushed by higher rates, and rarely have studied the similarities (other than they had a big crash too) or the differences.

I could go on and on about the differences, but let's look at one major metric.

Japan has been the largest creditor nation in the world 28 years running.

The US is the largest debtor nation in the history of the world. Let that sink in…

How can Japan have a 230% debt to GDP and be the largest creditor nation?

Their public debt is owned by the central bank and other various institutions.

So they own a lot of other country's assets and owe very little to other countries (even though they owe a staggering amount to themselves.)

The US is the opposite, it owns almost no foreign assets and owes foreign countries more than any nation in the history of the world.

This means all those dollar assets held by foreigners can be sold fast if the conditions are right, creating the velocity needed to create inflation when combined with the massive expansion in our money supply.

Foreigners don't own any Japanese assets to it would be much harder to create a rush of selling needed to increase velocity and/or inflation.

And this is just one difference between Japan and the US.

Please don't get me wrong.

Japan has got problems, HUGE problems, but problems are significantly different than the US.

Which takes us back to probabilities. There's a 100% chance of 1 of 3 outcomes over the next decade.

- Inflation (1970's)

- Deflation (Japan)

- Nothing (the US stays locked at this moment in time forever)

Let's just assume there's a 33.3% chance of each outcome.

That means there's a 33.3% chance many on this thread go bust.

And a 66.6% chance things get really bad, BTW what happens to pension funds if the US turns into Japan for the next 10 years? Answer…they go bust.

The bottom line is investing in the US right now is extremely dangerous, especially for those whistling past the graveyard needing ZIRP forever to stay in business.

If your business model requires ZIRP, you are part of the malinvestment.

Don't build your investment framework around ZIRP. 😉

Comments are closed.