Is your money safe in a bank? Have you asked yourself that question?

In this article, I'm going to go over the secrets of bank reserves, and reveal all of them to you. This is also a reaction article to Mike Maloney's video on how the Fed took reserve requirements all the way down to zero.

That's right, banks are no longer required to have any reserves whatsoever.

One of the biggest areas of confusion for the average person is how bank reserves actually work. So in this article, I reveal the following:

1. How most people see the banking system (it’s wrong).

2. How the banking system and reserves actually work.

3. Why would the Federal Reserve eliminate the reserve requirements in the first place?

4. What’s their motivation?

I'm sure you want to make better financial decisions in the future, and it’s imperative you understand how the banking system works, and it all starts right now!

How People Think The System Works

We see banks as having big vaults with cash in them, just like they did in the old days where they had currency, paper notes, and gold.

People usually think “it's just somewhere like a safe deposit box where you go and put your stuff.”

Nowadays, the banks might not keep track of all this physical “stuff”, but they just do it electronically, meaning they have your dollars in electronic format.

So we as people, the general public, the average Joe and Jane, see things the exact same way as they were back in the day.

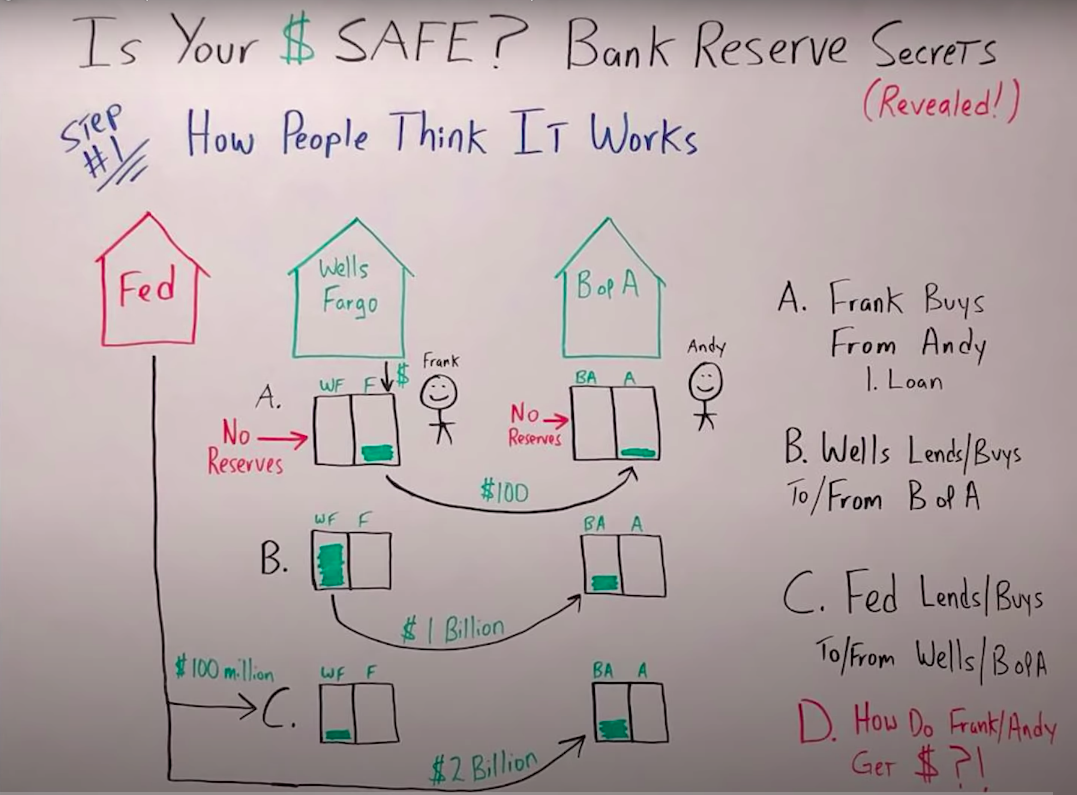

Here is an example of how it works with 2 well-known banks:

I drew Wells Fargo on the left, and Bank of America(B of A) on the right. The way most people see it is Wells Fargo and B of A have bank accounts just like they have safes.

They have one bank account for themselves, the Wells Fargo account, and they have another bank account for their customer. In this case, it's a guy named Frank, so he's Wells Fargo Frank.

B of A also has its own bank account and they have one for their customer, whose name is Andy.

Let's go through a couple of scenarios of transactions and see how most people think this works.

-

Scenario A:

Frank buys something from Andy for 100 dollars. He tells Wells Fargo, “I'm going to use my ATM card and I'm going to swipe it with my buddy, Andy,” Or, “I want you to transfer the money over to him via Zelle.”

Or maybe he's going to wire it or write a check, but he's going to instruct Wells Fargo to take the 100 dollars from his checking account and transfer it over to Andy's checking account at B of A, simple.

Wells Fargo subtracts $100 from Frank's account and B of A adds $100 to Andy's account, pretty straight forward. Just like they would have done it in the old days if it was actual paper currency notes, gold coins, or silver coins.

-

Scenario B:

Wells Fargo lends or buys something from B of A. In this case, they're buying treasuries or mortgage-backed securities or mortgage-backed sausages as I like to call them.

Wells Fargo says, “Listen, B of A, we'll buy those mortgage-backed sausages for you and we'll give you a billion dollars.” B of A says, “Fine, we'll do the transaction.”

Wells Fargo takes a billion dollars from their checking account, of course, because they have their own account, and are going to transfer the billion dollars over to B of A's checking account.

-

Scenario C:

The Fed lends money to Wells Fargo and then they buy something from B of A, again maybe treasuries or mortgage-backed sausages.

So let's say the Fed lends 100 million dollars to Wells Fargo. They go to their discount window, Wells Fargo calls them up and says, “Fed, we need money ASAP.”

The Fed sends them 100 million dollars, puts it right back into their checking account, and they're good to go.

Then, the Fed says, “Listen, B of A, we'll buy those assets from you for $2 billion.” B of A says, “Fine, let's do the deal.”

The Fed transfers the $2 billion into the B of A's checking account, which of course they have because they are a bank.

Just like in the old days, they would have a giant safe and the Fed might send them over some paper currency notes in a Brinks truck, or maybe some bars of gold, something physical.

So, B of A would take the stuff, whatever they borrowed or whatever they've received from the Fed, and they would keep it right there in their physical bank, safe and secure.

Now, let's remember the banks aren't required to hold any reserves whatsoever, so in their checking accounts, they could have zero goose eggs.

What happens if Frank or Andy go down to their local bank and try to get 100 dollars from the ATM machine?

In the future maybe they're not going to be able to get the 100 dollars because Wells Fargo and B of A aren't required to have any money whatsoever in their accounts.

This is the one the way most people see the system and how it works, and this is completely and entirely wrong.

How The System Really Works

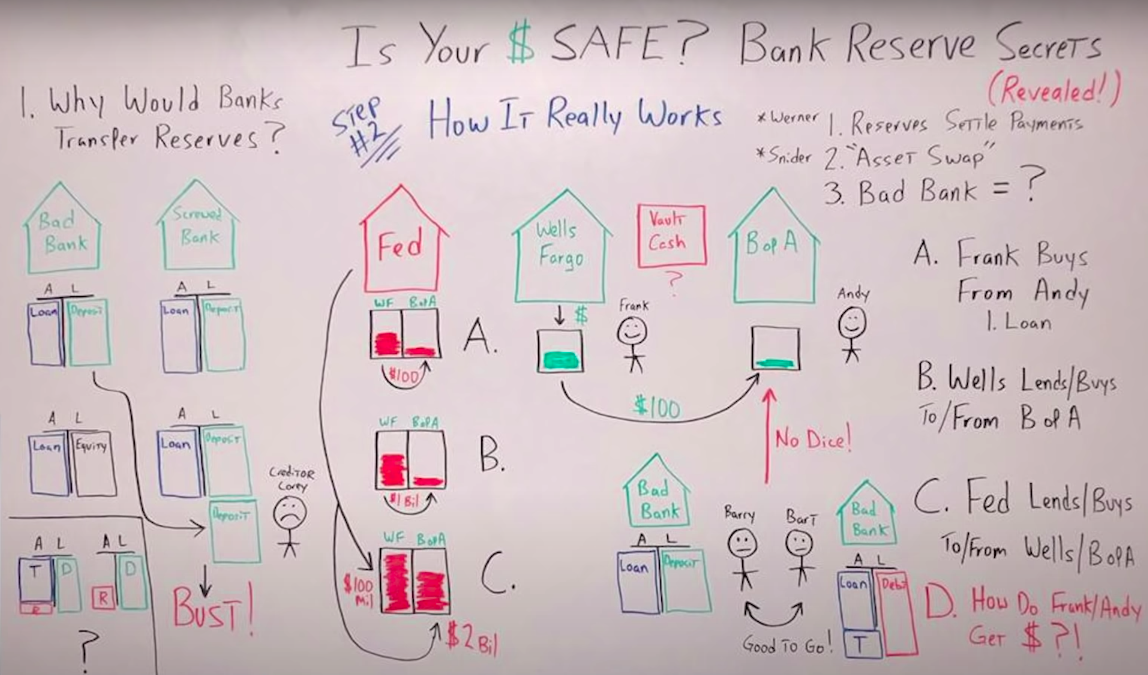

Look at the next whiteboard and let's walk through the exact same scenarios here.

First and foremost…

-

Scenario A:

Frank buys something from Andy. What happens is Wells Fargo transfers the money from Frank's checking account to Andy's checking account even if it's a loan. If it's a loan, Wells Fargo just credits an additional $100 to Frank's checking account.

This is actually the same, but where it gets a lot different is simultaneously Wells Fargo would have to transfer $100 worth of reserves from their account held at the Federal Reserve to B of A's account held at the Federal Reserve.

Notice I'm emphasizing that last point. Now, let's check out the next transaction.

-

Scenario B:

Wells Fargo lends or buys something from Bank of America. So Wells Fargo would just transfer a billion dollars to B of A's reserve account held at the fed.

Notice, with that transaction nothing happened in the “real economy.”

In fact, nothing happened outside of the Federal Reserve, there were no deposits transferred.

There was no deposit that went from Wells Fargo to B of A, that's why in my drawings I colored the reserves in red and I made sure the deposits were green.

Technically, they are both considered dollars, meaning bank reserves and deposits, but in practice, they're a lot different.

That's why Jeff Snyder always says that when banks buy stuff from each other and when the Fed prints funny money to buy treasuries, it's not really creating money supply, it's only an asset swap.

Meaning the Fed is just trading bank reserves for treasuries or mortgage-backed sausages, and the banks do the exact same.

As long as it stays within the financial system or the banks under the Fed's umbrella, the transactions only occur through bank reserves, they don't occur through actual deposits going back and forth.

-

In scenario C:

The Fed lends or buys something from Wells Fargo and Bank of America. For this example, I'm using transactions of $100 million and 2 billion.

In that case, the Fed would print funny money or bank reserves and would lend Wells Fargo 100 million by adding 100 million to their reserve account held at the Fed.

The same thing for B of A, if they purchased billions in T-bills from them, they would just deposit an extra $2 billion worth of bank reserves in their account.

What determines whether or not Frank and Andy can get their money?

It's not necessarily the amount of reserves in the system, it's really all about the vault cash.

I think that was one of Mike's main points, and again, if you didn't see that video, it's awesome. I totally suggest it.

Now the question I almost guarantee you're asking yourself is, “George, if there aren't any reserve requirements going back to transaction A where Frank buys something from Andy, why on earth do the banks have to transfer reserves back and forth?”

There are no reserve requirements.

To dive into this a little further let's read exactly what Richard Werner has said.

If banks create money, they do not need to raise deposits to lend or sell (Werner 2014). Still, they must avail themselves of the cash and reserves necessary to guarantee cash withdrawals from clients and settle obligations to other banks emanating from client instructions to mobilize deposits, to make payments and transfers.

-Richard Werner (World Bank Blogs)

That's just a very fancy way of saying, If Wells Fargo transfers deposits or money for whatever reason to B of A, they also have to transfer the reserves.

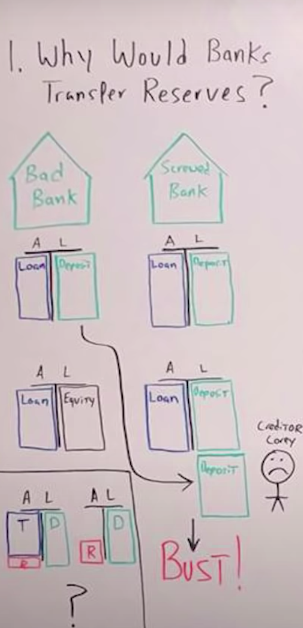

Let me explain this even further by using an example on the whiteboard.

On the left we have the “bad bank”, they don't want any reserves and they're trying to figure out a way to take advantage of the system that doesn't require reserves.

On the right, we have screwed banks. They have problems, you can tell already.

The bad bank says, “I know what we'll do. If we don't have to transfer any reserves to the screwed bank, we'll go ahead and send them all of our deposits because the deposits are actually liabilities on our balance sheet. If we can get rid of our deposits, all of a sudden we'll have loans, assets, and equity. We'll be instantly rich because we have no more liabilities.”

But then what happens to screwed bank? Well, of course, they have loans on the asset side of their balance sheet and they have deposits that equal out, so they're solvent.

If the bad bank sends them all of their liabilities, now all of a sudden they have way more liabilities than they have assets. In other words, they have negative equity, they're insolvent, or what we like to say, they're bust.

Let's remember that the depositors, people like you and me who have bank accounts at your local bank, whether it's Wells Fargo, B of A are actually a creditor of the bank, an unsecured creditor.

If the bank goes bust, guess who gets screwed? That would be you.

In this case, it's the little guy I drew in my whiteboard named creditor Corey.

If those were his deposits and screwed bank said, “We have to close our doors, we just went bust,” creditor Corey who had deposited with the bad bank of course wouldn't get his money.

To answer the question is your money safe at your bank? You have to start by focusing not just on the reserves but more importantly the on the balance sheet of the bank you're doing business with.

Let's look at another simple example…

In this case, I drew a balance sheet of a bank that has 30% reserves compared to their deposits, but doesn't have anything else.

They're completely out of business, they're bust. Compared to the bank on the left that has deposits as liabilities.

They didn't have as many reserves but they had additional assets, let's call them treasuries. The bank on the left is solvent, they're fine.

While the bank on the right is actually out of business, in other words, the creditors, you, the depositors might not get the money back.

Let's go through another thought experiment.

Imagine there's a bank that has no reserves whatsoever. We'll call them the second bad bank. All they have are loans on the asset side of their balance sheet and deposits on the liability side.

They have two customers, Barry and Bart, but what happens if Barry wants to transfer some money and buy something from Andy?

Well, they can't do it because the second bad bank doesn't have any reserves.

Now, they could sell some of their assets or borrow against their assets, but just to keep things simple if they didn't have any reserves held right now at the Fed, technically they really couldn't transfer the deposit to Andy for Barry to make the purchase.

But this is where it gets interesting. Let's say that Barry wanted to buy something from Bart and they're both customers of the bad bank.

No problem there because the bad bank can transfer the deposits within its own balance sheet from one person to the next.

The balance sheet doesn't change at all, there are no reserves required if the transactions are going from customer to customer. The problem comes if the bank has to transfer the deposits to a different bank.

So, the bad bank is looking at this situation and saying, “My gosh, why on earth do we want these customers in the first place, they're kind of a nuisance?

If we can have no reserve requirements, why don't we just borrow money from the repo market or even from the Fed and use it to buy assets and create loans?

Then we eliminate the stupid customer and the pain in the neck that's involved with transferring all the reserves back and forth all the time, we can do much bigger deals.”

So, the bad banks look less and less like retail banks and start to look more and more like investment banks, just like Goldman Sachs or JP Morgan.

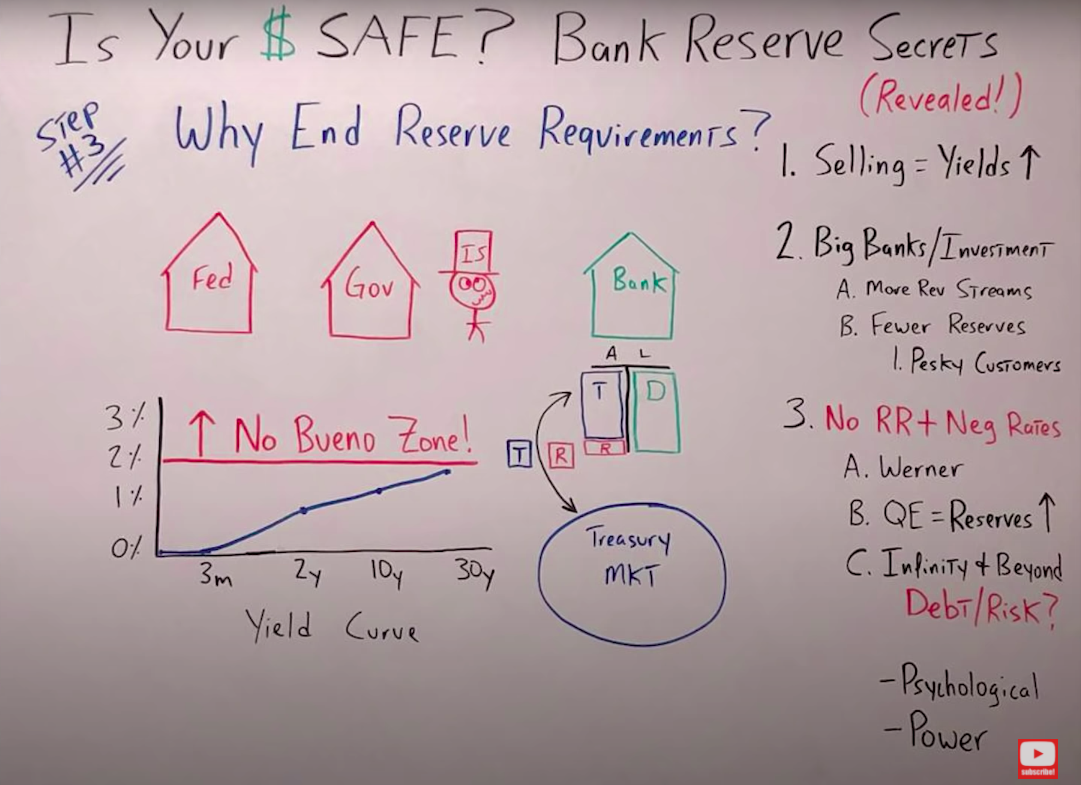

Why Would The Fed End Reserve Requirements?

If we know the retail banking system has to have reserves going back and forth, if customers want to transfer money, make payments, buy and sell things, why would the Fed come in and end reserve requirements?

Let's see if we can go ahead and connect some dots.

First and foremost, take a look at a bank's balance sheet that needs to come up with additional reserves.

What will happen? Well, they have assets on the left, most likely treasuries, and they need additional reserves because they don't have enough.

Again, this is going back to a situation where there was a 10%, 20%, 30% reserve requirement.

At the end of the day, they would have to sell some of their assets and treasuries to get the reserves they need to meet the reserve requirement.

If they're selling treasuries what does that do potentially to treasury yields? It increases them because there's more supply, there's less demand, the rates or the yields go up.

This takes us right back to the Fed and the government, your drunk insolvent Uncle Sam, who is always spending money like a drunken sailor.

He has so much debt and the Fed knows that they can't allow interest rates to get above a certain level or your Uncle Sam might actually go bust.

But it's not just Uncle Sam, it's the consumers, the states, the corporations, all of them have a massive amount of debt.

The Fed cannot allow interest rates to get above a certain level, and I always call it the “No bueno zone”.

If interest, especially the 10-year, got into the no bueno zone and kept going higher, this would crush the economy, local governments and it could crush the federal government.

Ending the reserve requirements could be a strategy the Fed is using to try to prevent entities from selling their treasuries and keep interest rates artificially low.

Let's remember the big banks, especially the investment banks have a lot of advantages.

- They have many more revenue streams through financial engineering, not necessarily issuing loans to customers to buy cars, homes, et cetera.

- They don't need as many reserves as a percentage of their overall balance sheet because the transactions they're doing are a lot different, and most of the transactions are exclusive to the financial economy.

- They don't have those pesky customers transferring money back and forth with their deposits, which means the bank themselves have to keep reserves to make sure that they can transfer the reserves to match up with the deposits of the customers going back and forth.

What nobody's talking about is what happens if you combine no reserve requirements with negative interest rates, this is what we really need to think through.

To start, let's go right back to Professor Richard Werner.

The policy of negative interest rates is thus consistent with the agenda to drive small banks out of business and consolidate banking sectors in industrialized countries, increasing concentration and control in the banking sector.

The Bank of England, may further increase its own power and accelerate the drive to concentrate the banking system if bank credit creation was abolished and there would be only one true bank left.

– The Band of England

(End of quote)

What am I talking about specifically?

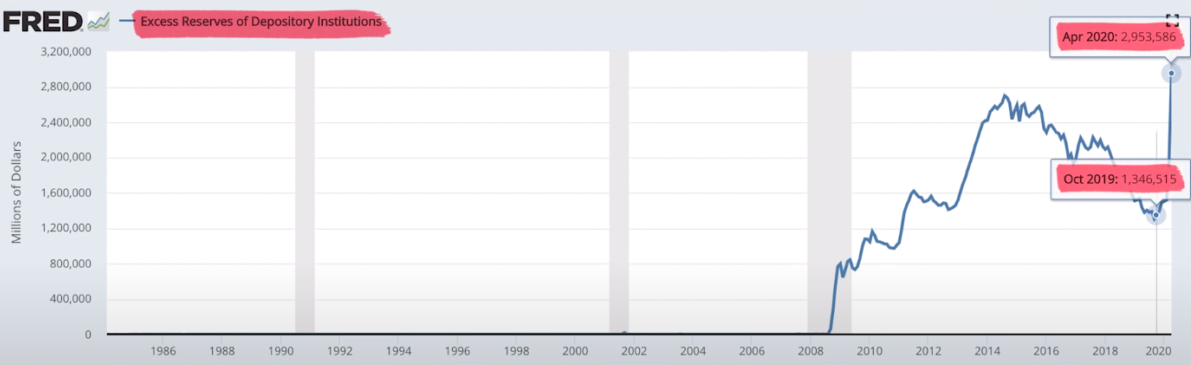

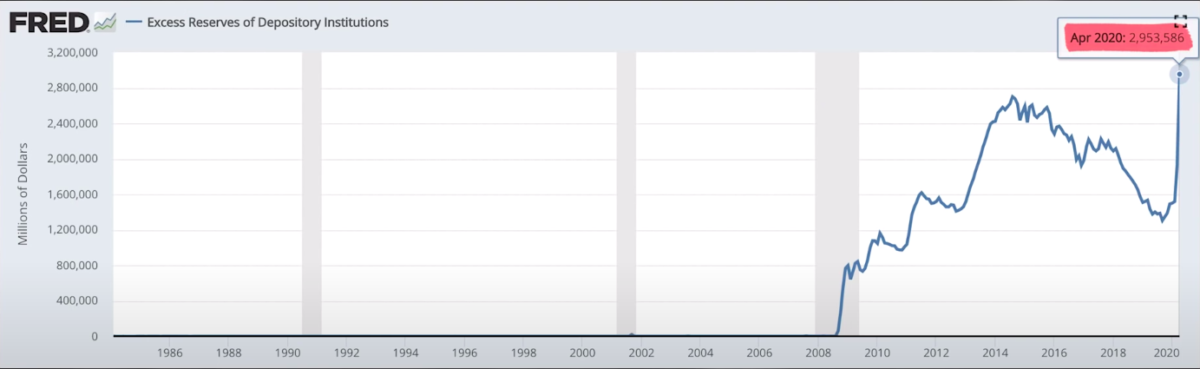

Here is a chart of the excess reserves right now of the banking system held at the Fed.

Just since October of 2019, the excess reserves the banks hold with the Fed have gone from 1.3 trillion all the way up to almost $3 trillion.

This is a staggering amount, and yes, the Fed is paying them interest right now on this excess reserves, but if interest rates go negative then the banks will have to pay the Fed for these excess reserves.

If you wipe out the reserve requirements what that most likely means in practice is the huge banks, and especially the investment banks, will only have to have maybe 1%, 2% of reserves.

While normal retail banks and smaller banks will have to have at least 10% regardless of the reserve requirements because they have customers making these transactions back and forth.

Think about this, the burden of the $3 trillion in reserves held at the Fed, the majority of that will be on the shoulders of all of the retail banks.

This is going to put pressure on them, most likely putting a lot of them out of business. It goes right back to what Richard Warner was saying…

Is this a plan for the central banks and maybe the investment banks to consolidate power?

Just to make sure we're on the same page the game plan could be, increase the amount of reserves in the system by doing QE infinity, this doubles it, taking it from 1.5 trillion up to 3 trillion.

Then create negative interest rates so the entities holding onto those reserves have to pay us. In other words, it becomes an expense for the entities that have the reserves.

This is a one-two punch that puts more pressure on them, forcing them out of business.

There also could be a cycle technical component to this and I'm guessing this is what Jeff Snyder would argue. He thinks the Fed is completely incompetent, as well most central banks.

There's no way they could pull off a plan that is as intelligent as increasing QE, the amount of reserves dropping interest rates negative just to consolidate power.

I don't want to put words in his mouth but I'm guessing that's what he would say.

But, dropping the reserve requirements could be the Fed's way to try to convince the market place there's going to be inflation in the future, therefore, increasing the velocity of money while at the same time M2 is going parabolic.

This increases the rate of inflation and an increase in inflation decreases the debt load in the entire system.

Regardless of why the Fed got rid of reserve requirements, whether it was to allow banks to take debt to infinity and beyond, remove the need to have physical cash on their location, or it was something far more sinister.

Maybe they were trying to consolidate power within the banking system, or the Fed's just a bunch of idiots trying to play psychological games with the market to bail out your drunk, insolvent Uncle Sam.

The bottom line is getting rid of the reserve requirements is a bad thing and it makes the entire system far more risky.

Comments are closed.