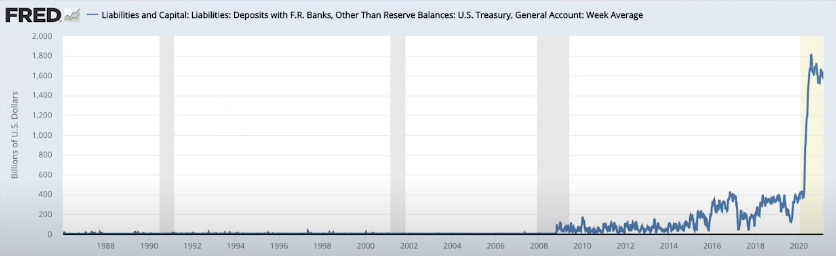

Janet Yellen – The United States Secretary of Treasury – recently announced that she will be drawing down the Treasury General Account (TGA) by $1.1 Trillion over the next four months.

Could this be an economic time bomb in the making?

This decision could lead asset prices, like homes, and 401ks, to correct by over 50% while creating an inflationary scenario never before seen in the US. All of this, according to George Gammon.

$1.1 trillion is the equivalent of $250 billion per month out of the Treasury General Account.

Where will TGA funds flow?

These funds will be spent on additional quantitative easing. Mind you, the Fed is already spending $120 Billion per month on QE.

What is Quantitive Easing?

According to Investopedia, Quantitative easing (QE) is a form of unconventional monetary policy in which a central bank purchases longer-term securities from the open market in order to increase the money supply and encourage lending and investment.

Buying these securities adds new money to the economy, and also serves to lower interest rates by bidding up fixed-income securities. It also expands the central bank's balance sheet.

To add more context, QE was meant to be an extreme, emergency counter-measure intended to keep the financial economy safe.

Eighty-Billion dollars per month in QE was once considered extreme. Janet Yellen's TGA contribution puts QE at $350 billion per month.

A question best reserved for a psychiatrist, but why does the Government and the Fed always seem to think their unorthodox manipulation of markets can keep everyone safe?

Janet Yellen Creates Additional Liabilities For Banking System

Janet's additional $250 Billion per month not only creates additional bank reserves but also creates additional liabilities in the commercial banking system.

Why does an additional $250 Billion Per Month Cause Additional Liabilities in the commercial banking system?

These additional reserves eventually end up on the commercial bank's balance sheet as assets. And with respect to the Fed's balance sheet, these same reserves are liabilities.

Since the Fed Funds rate is near zero, there is no way for the commercial banks to earn a yield on these ‘assets'. To add insult to injury, these banks still have to service and maintain their account holder's accounts.

If Moody-The-Millenial's account over at Chase earns a yield, regardless of how small, then the bank still has to pay it. If there are fees associated with managing Moody's account, then those fees will have to be absorbed by the bank.

These banks are essentially providing banking services for free when holding onto reserves generated by Janet Yellen.

Banks Must Get Creative Or Else

The banking system needs to figure out a way to earn extra returns.

They'll likely visit the Repo market, or get creative with derivatives, and use re-hypothecation.

Re–hypothecation occurs when the creditor (a bank or broker-dealer) re-uses the collateral posted by the debtor (a client such as a hedge fund) to back the broker's own trades and borrowing. This mechanism also enables leverage in the securities market. – Wikipedia

However, to take these actions, commercial banks need to use their bank reserves to buy up as many T-bills (treasuries) as possible.

If banks are soaking up the T-bills supply, in an effort to lend more in the Repo market, or create derivatives, and re-hypothecate, then what does this do to T-bill interest rates?

T-bill interest rates will go negative, while prices go up, due to increased demand

Interest rates are used to incentivize purchasing. If no incentivizing is necessary, then expect those incentives to turn into disincentives (negative rates).

George believes this process could blow up the entire monetary system, especially hedge funds, sovereign wealth funds, and those countries that depend on treasuries having at least a 0% interest rate.

George also believes that the Fed would have to intervene and increase interest rates on US treasuries, which presents another problem: Higher interest rates translate into higher interest rates in the real economy. This would destroy asset prices, including the stock and housing market.

The US economy is built on three pillars: Asset bubbles, debt, and confidence.

As soon as asset prices crash so does the American economy.

The Fed knows that when prices crash, it creates economic devastation. So the Fed needs to peg the yield curve. That means doing anything in their power to bring the interest rates down to where the economy can handle it.

To institute yield curve control, the Fed needs to do more quantitative easing, which was their initial problem. More quantitative easing takes the US economy deeper into a doom loop.

In conclusion

George is convinced there is a way of protecting your wealth. First, understand the crack-up boom cycle.

The crack-up boom is a consequence of credit expansion and price increases that result in distortion of the economy. The central bank attempts to sustain the boom indefinitely without regard to consequences, such as inflation and asset price bubbles.

When the Government continuously pours more money into the economy to give a short-term boost, it eventually triggers a fundamental breakdown in the economy.

To prevent any downturn in the economy, monetary authorities continue to expand the supply of credit and money at an accelerating pace until it's too late.

George thinks this is exactly what Janet Yellen and the central planners are doing today.

For you to be prepared financially, you need to click on the video above to have a deeper understanding of how interest rates and the Treasury General Account work.

Make sure to watch all the way to the end for actionable content that you can use to protect yourself.