Inflation expectations and interest rates are going through the roof. And as a consequence, home affordability will be affected. Will inflation cause home prices to go down, or will they continue increasing?

How do inflation expectations and interest rates affect home affordability and housing prices?

If the government continues to deficit spend the way it has been, and the M2 money supply continues to increase, then we will see inflation expectations continue to rise as well.

If inflation expectations continue to rise, then so will the 10-year treasury and 30-year mortgage rates. Today's markets are incapable of absorbing ever-increasing interest rates.

Also, the behavior of copper and 10-year treasury rates are also signaling a future price hike.

Copper prices

The price of copper has been steadily increasing over the past year. Copper is a required ingredient in many consumer goods, so it makes sense to follow copper. If copper is increasing in price, then expect products containing copper to go up as well.

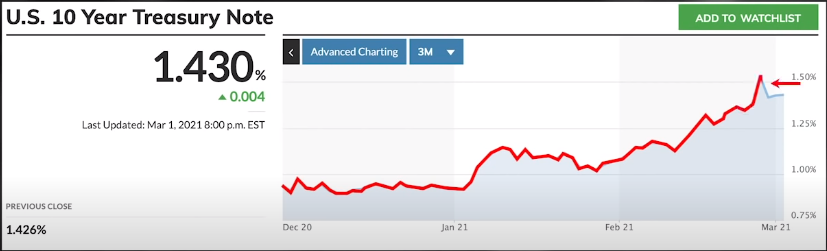

10-year treasury rates

10-year treasury rates have increased dramatically from January to March of this year (2021). The rates have gone up from 1.0% to 1.5%, as shown below.

What happens to mortgage rates when the 10-year treasury rate increases?

During the same timeframe – from January to March – mortgage rates also increased from 2.64% to 2.82%. When the 10-year treasury rate increases, so do mortgage rates. In terms of percentage, the rate increase is definitely substantial at 6.8%.

Inflation expectations trigger an upward move in 10-year treasury and 30-year fixed-rate mortgages

Mortgage rate increases put pressure on home prices and home affordability.

The Fed has two options:

- Allow interest rates to continue increasing and risk a housing market crash along with the entire US economy, or

- Try to manhandle interest rates by creating more bank reserves, which could have other unimaginable and unintended consequences.

Purchasing power and the ability to afford a monthly mortgage payment become an issue when the cost to borrow increases. The higher the interest rate, the lower the purchasing power. If purchasing power decreases, then expect demand to decrease as well. Housing prices will have no choice but to adjust in an effort to meet market demand.

Manhandling interest rates (option 2) will come with strings attached. The Fed risks losing control of the fed funds rate, and every interest rate along the yield curve.

In September of 2019, the repo rates spiked to almost 10%. According to George, this proves the Fed momentarily lost control of the overnight fed funds rate.

mortgage rates could also explode higher if repo rates rise

On the other hand, Prime Money Market Funds (MMFs) provided 66% of the liquidity of the repo market in March of last year. If the MMFs are not there to provide the liquidity, and we still have the same demand, then 66% of the cash needed in the repo market will be unavailable.

66% of the cash needed in the repo market could disappear

Money Market Funds could exit the repo market due to negative interest rates. If you recall, a money market account was once a popular savings vehicle at your local bank. It typically had a slightly higher yield than a traditional checking account.

Your bank loans to financial entities in the repo market. The rate they pay you is less than the cost to borrow, so they pocket the spread and make a profit on your money market account. This is no longer the case.

With rates at near zero, no one in their right mind would park cash inside a money market account. Imagine what would happen if rates went negative?

Repo Market Borrowing Costs set to explode

Assume for a second, that Money Market Funds exit the repo market, as soon as yields turn negative. So what happens to the price of money when 50+ percent of the liquidity vanishes? The price of money would go through the roof.

And again, If repo rates go up, so do mortgage rates.

If the Fed comes in and tries to peg mortgage rates, they’re going to have to print more bank reserves.

Printing more bank reserves could take treasury bills negative. And if treasury bills go negative, then so will rates on Money Market Funds, which could lead to another repo market spike.

Make sure to click play on the video above for a deeper understanding of inflation expectations, interest rates, the repo market, and how it all affects the housing market.