If you want to know how to analyze the market, when to sell or buy assets, find the anomalies and catalysts behind each process, you need to read this article. You may not be able to foresee the future, but you will learn when to act upon them and be prepared.

Jim's Secret Techniques For Analyzing The Market

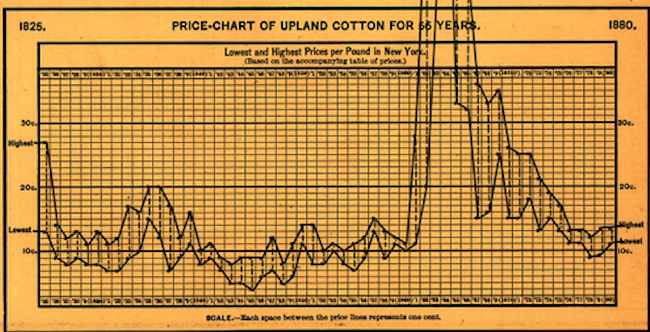

The image below shows a chart of cotton going from 1825 to 1880. On the left side, it went from a whopping 10 cents up to 30 cents. This is one of the coolest charts I have ever seen. I almost wanted to make a screensaver for my cell phone.

This is old school, and right here on the George Gammon blog, I check out all the data and have no recency bias going back five or 10 years, just like Jim Rogers, I take it back to the 1800s.

In 1825, the prices of cotton were around 12 cents, then they went down a little bit, came back up to 20, then they came down a penny, a half a cent. Later they came back up to their 10 cents historic trend line, and then prices went parabolic, even off the chart.

I've never seen a chart where the prices go off the chart. They were proper Buzz Lightyear prices to infinity and beyond. After that, they went back down to about 15 cents and pop back up in 1880, right back where they started about 10 or 11 cents.

The question becomes…

What on earth drove prices from half a penny up to who knows because we can't even see the prices on this chart?

With my research, they went up to probably $1 or $1.20, but to dive into this further, and to understand how we can use this specific chart to decode the current-day debate of inflation versus deflation, I examined an extract from my full-length interview with the man himself, Jim Rogers:

George Gammon: So let's go back to your days at Columbia and try to use this as more of an instructional question. I know back then you would have your students look at charts.

I know you're not a big fan of technical analysis or anything like that, but you would have them look at charts and see anomalies going back to the 1800s, I think even further back than that and different commodities and stocks and markets, and then you'd have them try to figure out why the anomaly took place and what could they have done to foresee it happening.

-

Do you still think that's a good approach for someone trying to learn how to invest in today's day and age?

-

Would you have them do the same type of thing?

Jim Rogers:

I did not have them look at charts as chartists. I had them look at the chart to get the historical perspective so that they could see, Oh, there's this stock or this whatever shot up at such and such a time.

Why did it shoot up? What caused that and how would you have figured it out?

If you go back and look at cotton in 1861, it went from half a cent to a dollar in six months. Now I was not long, I wish I had been around for that.

Then a fantastic boom for anybody who had the good sense to foresee what was coming and that's this kind of thing I said, Okay, I got to look it up and see what happened.

George Gammon:

The key to Jim's first technique can be summarized like this:

- Look at historic charts and look for anomalies.

- Then, ask yourself what happened, what drove this price to move higher or lower.

- Next, you need to figure out how you would have predicted the specific price movement given the information they had at the time.

- Use that knowledge to build a framework for today and what may happen in the future, regardless of whether it's the price of cotton, the price of oil, the price of gold, or whether we're going to see inflation or deflation.

The techniques we can learn from Jim Rogers to become better investors don't stop there, as you will notice reading further.

Jim Rogers:

You look for a chain, you look for something expensive, and often if you get it right, something will go from dirt cheap to a bubble, or certainly very overpriced for years, and everybody gets excited.

I think you probably know what overprice looks for. Everybody's talking about it. Everybody says it can never go down.

Everybody says, “Oh, don't you know, this time it's different.” Very dangerous words. George as you know, when they say, “This time, it's different.” You don't understand.

Those sides are pretty common. They happen all over the world and all markets when something gets overpriced.

You'll know if it's expensive, you'll know if there's wild enthusiasm, and then if you see something changing for the negative, you start to act. At least that's how I try to act and how I try to sell.

Likewise, when things are cheap back in Germany in those days, well, I mean, Russia, I was negative on Russia for decades, but for a variety of reasons, I concluded that there was a change taking place in the Kremlin. I can tell you why I think it, but who cares?

I think that I see change taking place for a hundred years in Russia, they didn't like capitalists. They didn't like rich people. They shot you or put you in jail, took your money, and then put you in jail. But I think I see vast changes in the Kremlin and the psyche of the people, it was very cheap. That's why I decided to invest in Russia, that's the sort of thing you look for.

(End of interview)

The second key technique to understanding when you should buy an asset or when you should sell is to look for a catalyst.

-

Is there something significant that happened that will most likely drive the price up or drive the price down?

-

What happened in 1860 that drove the cotton prices literally off the charts?

Of course, it was the civil war. The South produced the majority of cotton for the United States, so when war broke out supply plummeted and the prices went to infinity and beyond.

Now, let's use what we've learned from Jim Rogers to try to predict whether or not we're going to have inflation or deflation.

Inflation And Deflation Anomalies

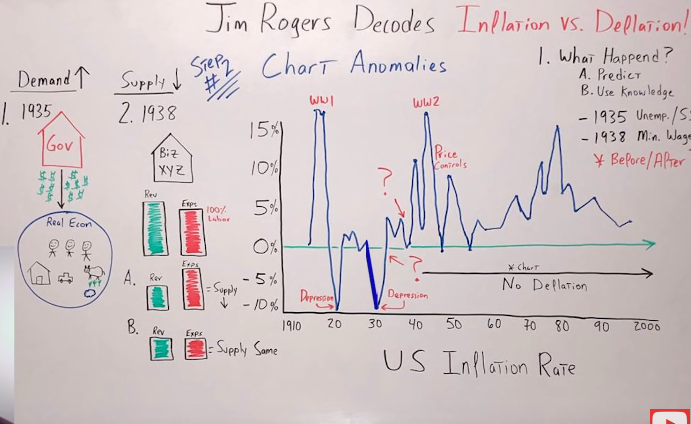

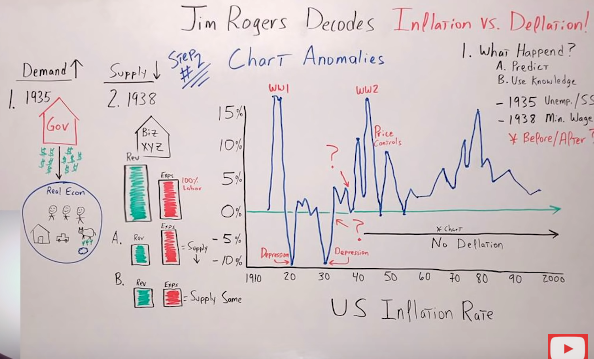

The graphic below depicts the US inflation rate going back from 1910 until 2000. It went from negative 10% to a positive 15%, so inflation skyrocketed, World War I came crashing down in 1920.

Most people forget we went through a severe depression in 1920 and 1921. When you look at the front line numbers such as deflation and unemployment, it was worse than the 1930s, but it goes right back up roaring twenties, where inflation was pretty stable.

We know what happened in 1930. Deflation kicked in, and again, went down to 10%, and in the middle of the decade, it went back up. Then we had World War II and price controls, and that was when inflation came back again, the 1950s stabilizes to the 1970s.

Then we had price controls again. We went off the gold standard, several different contributing factors, and then we had high inflation throughout the 1970s, as most of us remember.

In 1980, of course, Volcker came in and smashed inflation by jacking rates up close to 20%, then inflation came back down. Since then, it's been rather tame if you believe the government's CPI numbers, but for this purpose, we'll assume they're accurate.

Using what Jim Rogers taught us, I checked out the chart below to find any anomalies or interesting things. The first point that comes to my mind in the 1930s, is an entire decade of deflation where prices went down further.

The only thing that saved us from declining prices was World War II, but the chart tells a different story. At the beginning of the decade, yes, prices did go down. However, once we got to 1934 and 1935 prices went back up higher than they were throughout the 1920s.

We almost got up to a 5% inflation rate in 1935 and 1936. And for the latter part of the decade, we didn't have deflation at all. In fact, contrary to popular belief, we had pretty substantial price inflation.

Another thing I'd like to point out is since the early 1930s, the United States hasn't seen another bout of significant deflation. Pretty much all inflation since the early 1930s.

These two questions need an answer:

-

What happened in the mid-1930s that could have changed everything?

-

What anomaly took place that we need to be aware of so we can determine going into the 2020s if we're going to see inflation or deflation?

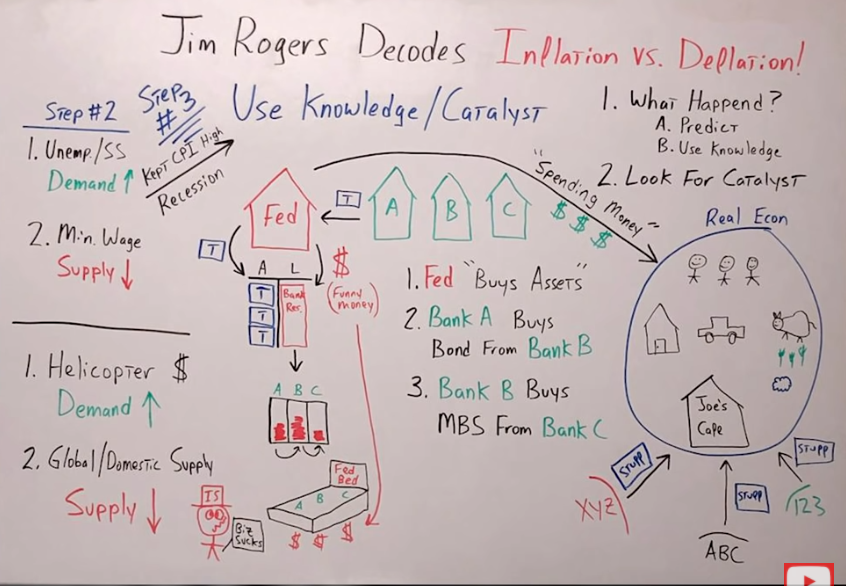

Well, in 1935, they passed the Social Security Act, which included unemployment benefits. Also in 1938, they passed the first minimum wage. The following chart of inflation-deflation in the United States makes it evident:

Before 1935 and 1938, we had bouts of deflation inflation, just going back and forth. After this period, we have seen nothing but inflation.

You may be saying to yourself, “Okay, George, I get it. I understand that we implemented social security, unemployment, and a minimum wage, but I'm not connecting the dots.”

How does that play into the United States having almost constant inflation for the next eight decades?

First, in 1935 when the United States implemented social security and unemployment. To be clear, social security payments didn't start going out until 1940, but the bottom line is it increased demand in the real economy.

Back in 1935, the United States government didn't have a way of transferring money directly to the people for them to go out and spend, but through unemployment benefits and social security.

Now, all of a sudden the US government was writing checks directly to the everyday person out on the street. Therefore, they had more money to buy homes, cars, cows, corn, or cotton.Moving onto the supply side, it got a little more complex.

In 1938, they instituted a minimum wage. From a standpoint of a business where 100% of their expenses are wages, if you have business XYZ under normal conditions, their revenue is slightly higher than their expenses, as shown below (revenue on the left, expenses on the right side)

So they had a bit of a profit there. They were good to go, but if we went through a recession or a depression, their revenues would significantly decline.

If they didn't have flexibility in their wages because of a minimum wage, they would have gone out of business. Therefore, the supply went down dramatically because this business wasn’t even functioning anymore.

In a free market system that doesn't have a minimum wage, revenues would go down, but their expenses would too. They would just reduce wages and, therefore, they would still be able to produce their product.

Granted, they might be producing less than they were before the recession or the depression, but they wouldn't completely be out of business. So what we have here is demand going up because the government is now transferring payments directly to people in the real economy and supply potentially being restricted.

After all, if we have a significant downturn in the economy, we have a lot more businesses shutting their doors instead of just lowering wages.

Let me be very clear. I'm not claiming that unemployment benefits, social security payments, and the minimum wage, are the only reason we haven't seen big bouts of deflation in the United States since the early 1930s. What I am saying is they most likely were significant contributing factors.

Inflation and Deflation: Using Our Knowledge To Find A Catalyst

We know that unemployment and social security benefits increased demand and the minimum wage decreased supply. Therefore, since the early 1930s, whenever we've had a downturn in the economy or recession, it's kept the Consumer Price Index (CPI) artificially high.

In other words, it's kept inflation higher than it otherwise would be. I included here a fragment from a recent interview with Dr. Lacy Hunt and my good buddy, Eric Townsend, from Macro Voices. Dr. Hunt delivered one of the best arguments I have ever read on deflation and hyperinflation:

“The first-round effects may appear to be appealing. I mean, wanting to bail people out in a time of crisis, people get a check. They think that's good. Then, the problem is in economics is that they're the unseen effects. The second, third, and fourth-round effects.

I don't like to use the term good or bad, but there's a little exercise that folks can do. If you graph government debt to GDP on one axis and the long bond yield on the other axis, and you do that for the United States. What you'll see is that there is an inverse relationship that is as the government debt levels go higher, the bond yields decline, and the logic here is that you are triggering the law of diminishing returns and you're, you're reducing saving to weaker and weaker levels that preclude physical investment. By the way, if you do that exercise for Europe, Japan, and now China, you'll see that the inverse relationships hold.

What we're talking about is understanding the economics and the economics suggest that if we pursue this policy, we're going to get weaker growth and lower inflation, and a prolonged period of low-interest rates. Unless of course the central bank, Federal Reserve is allowed to print money.

Then, in that case, we will not improve the growth rate one iota. The growth rate will probably even get worse because we will have a severe decline in productivity. In extremely high inflation, people do not hold financial assets. They spend time converting the financial assets as quickly as possible into commodities.

Then they trade those commodities with other people who have things if they want to. In other words, you have to have a double coincidence of wants, which is extremely inefficient. And so productivity will fall and the economy will lapse into an even deeper morass than it is now. So the money printing is a horrendous option. It may be used though, and if it does, you'll see a change in my forecast.”

(End of transcript)

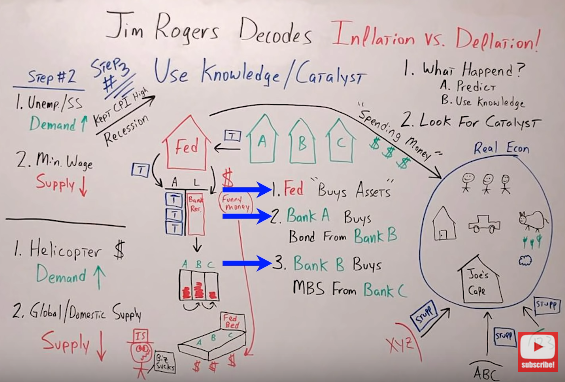

The catalyst Dr. Hunt refers to is the difference between the Fed buying assets and spending money or printing money. In real life The Fed is connected to the primary dealer banks, A, B, and C you can see in the whiteboard.

When the Fed buys assets, they usually buy them from one of these primary dealer banks or a bank under the Fed's umbrella. So in this case, bank A, bank B, or bank C are selling treasuries directly to the Fed.

The Fed takes the treasuries and puts them onto the asset side of their balance sheet. On the liability side of their balance sheet, they print up funny money or bank reserves that it deposits with the account of the bank that sold them the treasuries.

Let's remember the liability side of the Fed's balance sheet are bank reserves that look just like bank accounts or checking accounts we have with Wells Fargo, Chase, Bank of America, or whatever bank.

The primary dealer banks have these checking accounts with the fed. So primary dealer bank, A, B, and C, they all have checking accounts. So when the fed prints funny money or bank reserves, they go into one of the reserves accounts for the banks.

Another way to look at this is to pretend you have $10,000 and you stuff it under your mattress, it's not going anywhere. It's not going to create more demand in the real economy.

Why?

Because the money's under your mattress.

Let's just assume for a moment the Fed has a bed and a mattress. We'll call it the Fed bed. On the Fed bed, there are three different sections, one section for primary dealer bank, A, B, and C.

They're taking the bank reserves, and stuffing them under the Fed bed, bank A is putting it in their area, same as bank B and bank C, but it never leaves the mattress, it stays under the Fed bed forever.

Why is this?

Let's go through three different scenarios:

- First scenario: The Fed buys assets or treasuries from one of the banks. The treasuries go onto their balance sheet, and the funny money goes under the Fed's mattress.

- Second scenario: Bank A buys a bond from bank B. In that transaction, the treasury would go from bank A's balance sheet to bank B's balance sheet, but all they would do to pay for the transaction is transfer bank reserves held at the Fed from bank A to bank B.

- Third scenario: Then, bank B, let's say, buys mortgage-backed sausages from bank C. The only thing that happens there is bank B takes its funny money from their side of the mattress and moves it to bank C's side of the mattress.

Again, regardless of which one of the three transactions you look at -the reserves or the funny money- has never left the Fed. Contrast that to the Fed spending money.

I will use Dr. Hunt's words. What he refers to is, if the Fed, instead of buying an asset from one of the banks, goes in and pays for a bridge to be built, or maybe universal basic income, the money goes directly into the real economy.

This creates more demand for houses, cars, commodities, and it creates more demand for restaurants. I’ll use the character Joe's cafe as an example. The cafe also has big problems, remember they have to deal with the minimum wage.

So if we went through a recession, they would have a hard time staying in business because they can't drop their wages very much. Yes, they could hire fewer employees, but that also reduces supply.

While the Fed is creating additional demand, spending money into the economy, regardless of what you want to call it, whether it's helicopter money, MMT, UBI, or printing money, it's creating more demand.

This is happening at the same time when we could be seeing a reduction in supply because wages aren't flexible. They're very sticky. But let's also remember with Covid-19 we could see a lot of the global supply chains being disrupted.

Most of the stuff we consume in the United States isn't produced in the United States, it's produced by in-country XYZ, ABC, and 123, so if we have fewer countries producing stuff for the United States, it also decreases supply.

Also, remember the government, represented by your drunk, insolvent Uncle Sam, is competing with businesses for their employees by substantially increasing unemployment benefits to the point where most employees are making more money staying at home than they are going into work and producing more stuff or increasing supply.

Today, the catalyst we need to look for is the Fed increasing demand in the real economy by spending money directly into it instead of just creating bank reserves. They would do that through MMT, helicopter, money, UBI, whatever you want to call it, or just by monetizing the government's debt directly.

The government comes in, spends money on an infrastructure project, and issue bonds. Then, the Fed buys those bonds directly from the Treasury, or just in a roundabout way through the primary dealer banks.

Despite everything, this increases demand substantially, and it's exactly what Dr. Lacy hunt was referring to. On the supply side of the equation, we need to pay attention to how many businesses are going bust.

These are the questions you need to ask yourself:

-

What's happening to the supply chains?

-

What's happening with the political narrative of de-globalization?

-

How is it playing out with unemployment benefits, keeping people from going back to work, creating goods and services we need in the economy, reducing the supply?

Then it's just the simple equation of what is going down and what is going up.

If demand is going up while supplie is going down, you're going to see inflation. If demand is decreasing at a faster rate than supply is decreasing, then you're going to get deflation. Those are the catalysts we need to look for.

Comments are closed.