Not paying a debt or a loan sure seems enticing. But, if you had this opportunity, would you wonder if it is too good to be true?

In this article, I explain the intended and unintended consequences of wiping clean the student loan sleigh, the demographics involved, and some numbers that may upset you.

Insights You Need To Know About Wages, Rates, And Debt

I think this is one of the first things the Biden administration may do and it has been mentioned a lot in the news lately:

They're going to wipe the slate clean with student loan debt.

There are some pros and cons, and for you to be fully prepared in the future, you need to understand how this may play out. Not only the intended consequences but more importantly, the unintended consequences.

The American economy always starts with debt. Since 1981, we have seen a significant increase in the standard of living and wealth, especially for baby boomers. Their 401k and their home equity have gone parabolic, but…

How has this happened?

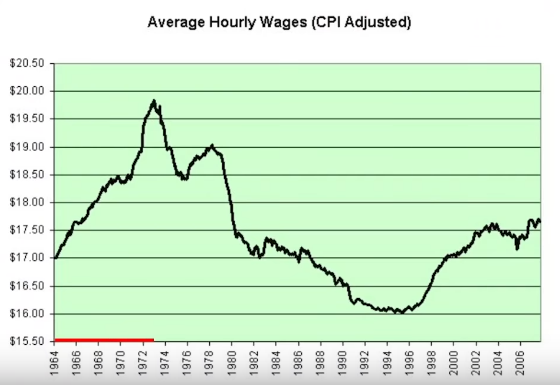

The chart below goes back from 1964 to 2004. It shows real average wages on the left, from $16 an hour up to $20 an hour.

In the 1970s, real wages were going up, the standard of living and the purchasing power for the average American was increasing significantly.

Right around 1974 it started to unravel when we got high rates of inflation because it exceeded the rate of the wage growth, so in real terms, wages went down.

This continued through the 1980s, the beginning of the 1990s, and down to 1994. Then, with the internet boom, it started to go back up, and we had some upward pressure on wages.

Jeff Snider would also argue because they most likely got aggressive in the Eurodollar market. It went up to 2000, we had the bust and then wages flatlined until where they are today.

Real wages today are under where they were in 1974. For more insights on why real wages have stayed low for so long I included a fragment from my recent interview with Real Vision's CEO, Raoul Pal:

- World War II: After World War II finished, the record number of people came into the labor force, so 76 million baby boomers into the US. By the time they were all getting into their thirties, much like the millennials are now, these people were competing against each other for wages.

- Bretton Woods: At the same time, we abandoned Bretton Woods, so that was another marker in this. But what happened was, when you put 76 million people into the labor force -at the time the population was much smaller- this was gigantic as a percentage, wages never went up again, ever, in real terms. So wages stopped going up in about 1974 in real terms. Then, if you wind forward a bit, that was nobody's fault apart from the silent generations' having too many kids, and that was a function of World War II.

- Credit boom: The next phase of this is cut to the credit boom that came out of the Reagan Thatcher years, what was that all about? Well, interestingly enough, credit growth offset the lack of wage growth. It's almost perfect when you measure all assets against it. So people did what they thought was the logical thing, “I'm earning less money in real terms, therefore I'll borrow to make up the difference”.

- Rise of technology: The next phase of this came with the rise of technology, the PC obviously in the eighties, but really by the nineties and the internet, this was a technological change that we hadn't witnessed before, it was feeding on itself, it was becoming exponential. So that was becoming deflationary as well because you could get more productivity out of a computer than you could out of a person.

- World Trade Organization (WTO): Then from '96 to 2000, we had that whole period of the WTO, and the WTO opened the playing field that everybody can compete on labor price. When China came in, that was it, done: Europe, US manufacturing industry completely holed out unless you were the best in class, which was Germany and Japan because they had great high quality so they can compete on price, everybody else got killed and wages just didn't go up.”

(End of transcript)

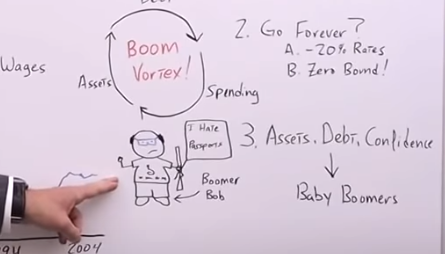

The question becomes, how on earth did baby boomers accumulate so much wealth during this time?

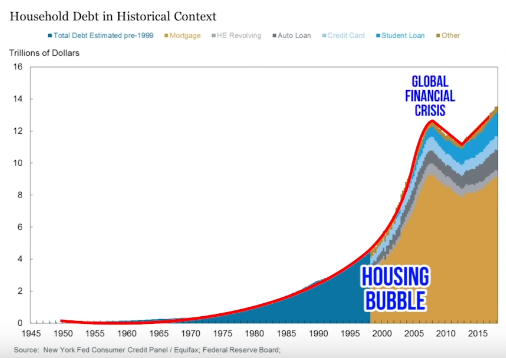

This takes us not to a doom vortex today, oh no, today we have a boom vortex! That's when the increased amount of debt increases the amount of spending, which increases the number of asset prices, which increases the amount of debt available.

It's a positive feedback loop that sends asset prices higher and higher. This is visible on the following graphic, which starts in 1950, and goes to 2015.

On the left, there is the amount of household debt from zero trillion dollars -believe it or not at one time it was almost that low-, up to 16 trillion. It flatlines until we get to 1990, and starts to go up significantly when we had the housing bubble in the early 2000s.

It comes back a little when the balance sheet of the average consumer is being rebuilt during the Global Financial Crisis, but since then it's gone to all-time highs.

This would explain how the baby boomers have such a large 401k and have so much home equity and wealth. It isn't a result of them producing more goods and services, it's just a result of more debt and higher asset prices.

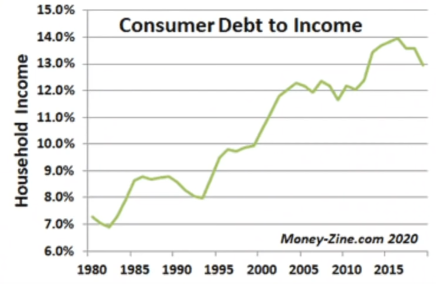

I also want to point out that consumer debt on almost every metric has gone Buzz Lightyear, to infinity and beyond, as shown on the chart above. The ratio of debt to income has gone straight up as well as the debt per capita.

I made some calculations of my own using an inflation calculator with the numbers represented in the debt per capita chart. So even when you adjust for inflation and the size of the population or the population increase, debt in the United States has gone parabolic since 1981.

How can Baby Boomers take on this much debt if their wages are pretty much going down or at best flat-lining?

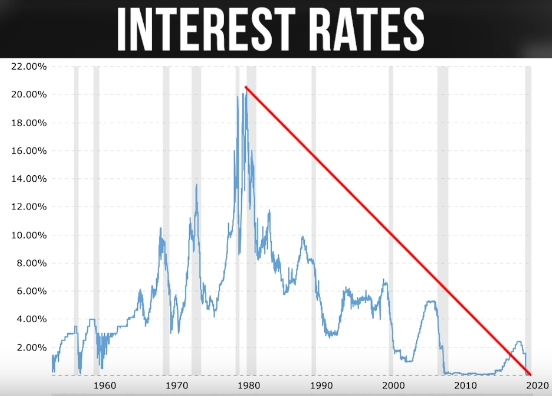

It is because interest rates have gone down since 1981, and this brings us to interest rates and fed funds. In 1981, interest rates were close to 20%.

Can you imagine?

We know what's happened since then, we've come down to where we are today at 0%.

If interest rates go down, that means the amount of the monthly payment for a mortgage, let's say, go down as well. So you can afford more housing, and have more purchasing power although your wages haven't increased at all.

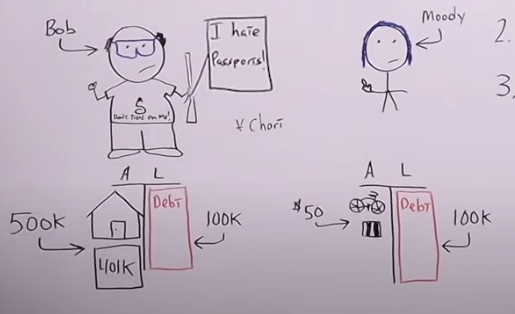

Now the character Baby Boomer Bob steps in and says, “Wait a minute, George, I think you're missing something very important”.

He is really angry at the government and is wearing a shirt that says, “Don't tread on me, government. I have my rifle right here, and I have my sign that says, ‘I hate passports', because I'm a patriot, and if anything happens here in the United States, I'm going to stay here and fight. That is right”.

Bob is saying, “George, you are wrong. If all of this financial engineering from the government has helped me get rich in the greatest country in all of the world.

Why can't they just continue doing it for the next 20, 30, 40 years to make asset prices go up forever?”

Well, because what brought asset prices so high had a lot to do with interest rates going down by 20%. Right now we're at the zero lower bound, meaning interest rates are at zero, so if we want to create the same financial engineering we had from 1981 to now, we have to take interest rates from zero down to negative 20.

I don't think that's likely, although if we go to a FedCoin and a central bank digital currency, who knows. One more thing I'd like to point out about Baby Boomer Bob is even though he is quite chatty, he's going to stand up and fight tyranny, as he owns 486 guns.

“They'll take my lead before they'll take my gold” is what he always says, but…

What was Baby Boomer Bob doing to fight tyranny back in March of 2020, when the government quite literally locked him in his own house?

The only fighting he was doing was locking the front door, polishing his guns and sitting down every day and watching eight hours of Fox News.

So my point is not to make fun of Baby Boomer Bob, but it's to point out that, Bob, you're most likely not going to fight any government or police state at the age of 70, so go out there and get yourself a darn passport.

There's no downside to it. That's the best way, the most realistic way that you and every one of us, as far as Americans, can increase our freedom and liberty in the future.

Remember what I always mention: The United States economy, and especially the balance sheet of baby boomers, is dependent upon asset prices, debt, and confidence.

Baby Boomers Vs. Millennials: Will Student Loan Forgiveness Result In An Economic Boom?

We have Baby Boomer Bob here again with his blue blockers, his gun, and his sign that says “I hate passports”, and my good old character, Moody the Millennial.

Bob's balance sheet has a lot of debt as I pointed out in the beginning. For this example let’s assume his debt is about $100.000, but he also has several assets and they're worth a lot of money. His home and his 401k are worth $500,000, so Bob is doing quite well.

Where Moody, on the other hand, has the same amount of debt, $100,000 in student loans, but his balance sheet on the asset side only has a bicycle and a backpack. Between his bicycle and his backpack, he only has $50 in assets compared to $100,000 in student loan debt.

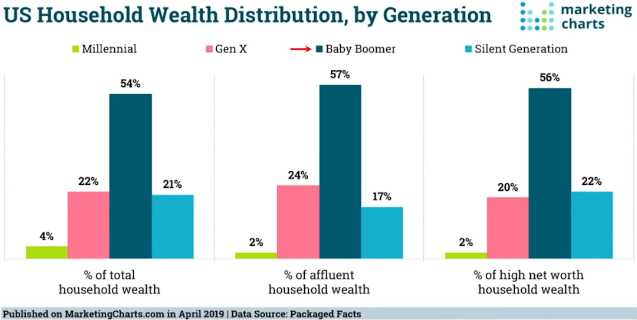

The two groups represent a huge percentage of the overall population, there are 68 million Baby Boomers and 82 million millennials.

If we extinguished all student loan debt, we could see a boom in an economy where 70% of GDP is a result of consumption.

To illustrate this further, here is a chart showing appropriately the balance sheet problem that millennials have.

Regarding the percentage of total household wealth, baby boomers have 54% versus millennials, who only have 4%. As you would expect, when you look at more affluent groups, the percentage of household wealth represented by the millennials goes down significantly, by 50%.

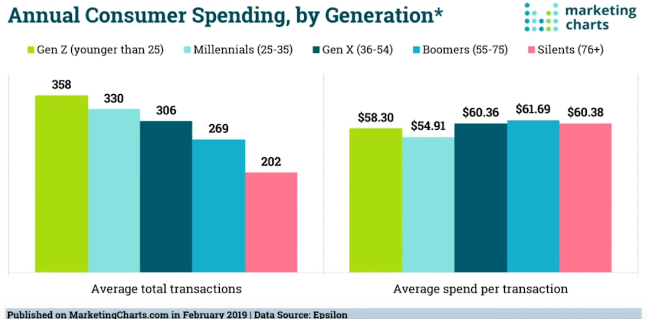

Let’s keep in mind that young people have a higher propensity to consume. The chart below describes exactly what I'm referring to, annual consumer spending by generation. Gen Z, which is the youngest generation, spends a lot more than the silents, which is the oldest generation.

So, Moody the Millennial has a mortgage and a mortgage payment, but he doesn’t have a house. As shown in the image above, he has a much higher propensity to spend. So if we were to give him, we'll call it a Moody Jubilee instead of a debt jubilee, where we wipe out all of the student loan debt.

What is he going to do?

He is going right out to buy his first house, a car instead of a bicycle, and he is going to go out to restaurants, bars, and especially right now when we're getting crushed by Covid-19 and all of the lockdowns. The businesses that are being most affected are most likely the businesses where Moody would spend the most money, but if we were to wipe out the student loan debt, this could definitely result in an economic boom.

However, there is no free lunch. These are the intended consequences, but now we need to go over the unintended consequences.

The Longed Answer: Is Student Loan Forgiveness Going To Be An Economic Boom Or An Economic Bust?

We have to remember what Henry Hazlitt and Frederic Bastiat taught us: In economics, what differentiates a good economist from a bad economist is the good economist not only recognizes what is seen at the surface level but also recognizes the unseen. To find more insights on this topic, click here.

So what are the second, third, and fourth layer effects of a certain policy?

Let's go through this process with student loan forgiveness and see if we can come to some conclusions:

What makes a society rich?

Let's pretend we have our character -average Joe- on an island, surrounded by water, the only thing he has is a palm tree with a couple of coconuts and a chest full of a billion dollars.

I want you to ask yourself a question, is Joe rich, or is he poor? Most of you would argue that Joe is poor because regardless of how much money he has, he only has access to three coconuts, maybe some sand and some saltwater. It's the same for the United States or any country.

The amount of wealth that the country has over the longterm, isn't represented by how much currency units they have or how many it can produce, but it's represented by the number of goods and services they can produce, the productivity of society at large.

Right now, your friend and family member, Fred, is probably saying, “Yeah, George, I get it, but the whole reason we don't produce that many goods and services are because we don't have any ‘good' jobs.”

Okay, but it goes right back to what Hazlitt and Bastiat taught us. One of the main reasons we don't have any “good jobs” is because we have a huge trade deficit that's hollowed out our manufacturing base. That was a result of Triffin's paradox, which was a result of Bretton Woods in 1944.

So one of the reasons Moody the millennial can't find a good job goes back to 1944 and an agreement between 44 countries and governments that never would have imagined that pegging the dollar to gold and then pegging other currencies to the dollar would result in Moody not being able to get a job to where he can afford to pay back his student loan in 2020.

This beautifully illustrates what Hazlitt and Bastiat are trying to tell us. We need to think through things from A to Z, it's not just about the seen, it's about the unseen.

Let's take it another step and think about the millennial generation, what their productive capacity is right now. Based on the education they've received and therefore the debt they want to extinguish.

This article from ranker.com shows us the top 10 or 15 most useless degrees. The way they're defining useless is when you get done with college and it's extremely difficult to get a job where you can pay back your student debt.

The reason I associate this with a younger generation or the generation that has the most amount of student debt right now is that when I was considering college back in the early nineties, I don't think they even had these majors, at least not that I can remember, so let's go through the list of useless degrees here:

- Gender studies

- Peace studies

- Disruption

- Dance

- Golf management

- Renaissance studies

- Religious studies

- African-American studies

- Fine art

- Feminist theory

I'm not here to say that no one has a degree that will help them produce more goods and services, therefore creating a wealthier society. I am saying that a much higher percentage today have these degrees that are “useless”. Degrees that don't involve any science or math.

It might make us feel good, but it's not going to make our society as a whole any richer, it's going to make us poorer in the long run.

My point is, even if we wipe out all the student loan debt, it doesn't make our society any more productive. The only thing we can do is spend more money, so even if we see a boom, the boom is only going to be temporary. At the end of the day, the structural flaws with our economy still exist.

If we go through a process of forgiving all student loan debt, most likely in the future we'll go to a society that has “free” college. Of course, nothing is free, but that's what they'll be calling it, and if we go to MMT, we will most likely have a jobs guarantee program.

So, if all young people can go to college for free, they'll never have student loan debt, and when they get out of college they're guaranteed a job at feminist studies, dance or golf maintenance at Topgolf, whatever it is, we're going to have fewer young people studying things like math and science that will allow our society to produce more goods and services, making us more and more wealthy.

Although the short-term effect of student loan forgiveness may be a boost in spending so we get higher nominal GDP, over the long run we produce less stuff, therefore, our society becomes poorer.

Let's remember if we're producing less, that means our trade deficit will increase, which means the amount of “good” high paying jobs that we have, again, will decrease. It comes full circle. So to answer the question,

Would student loan forgiveness be an economic boom or an economic bust?

If we're thinking about this like Hazlitt and Bastiat, the conclusion I think you have to come to, and again, there are no certainties, only probabilities, is that short term we would have a boom, but long-term we would have a bust.

Comments are closed.