Five months ago, oil crashed and we experienced chaos worse than 2008. The markets were going crazy, and it was just a bloodbath out there. So much so that I had to wear my good old red Prada loafers that day.

In this article, I explain how it started, what happened with the credit markets, and how I thought the endgame would be.

The hashtag for this article is going to be #SDT and you all know exactly what that means.

The Price Of Oil

I'll start by explaining all the past chaos. It started with not only COVID-19 but the oil price.

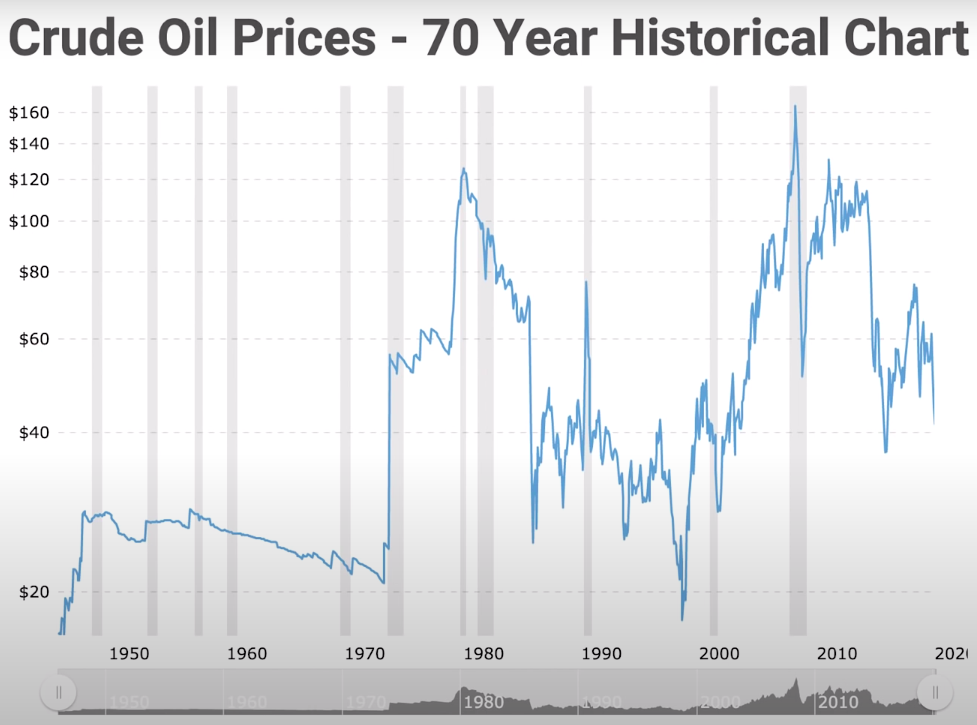

Look at this chart that goes back to 1970 to 2020, and it shows the price of oil on the left going from 20 dollars up to 140. This is adjusted for inflation.

I also drew it for you to make it more clear.

In my drawing, you can see one thing that always stays consistent with the oil market, and that is massive volatility.

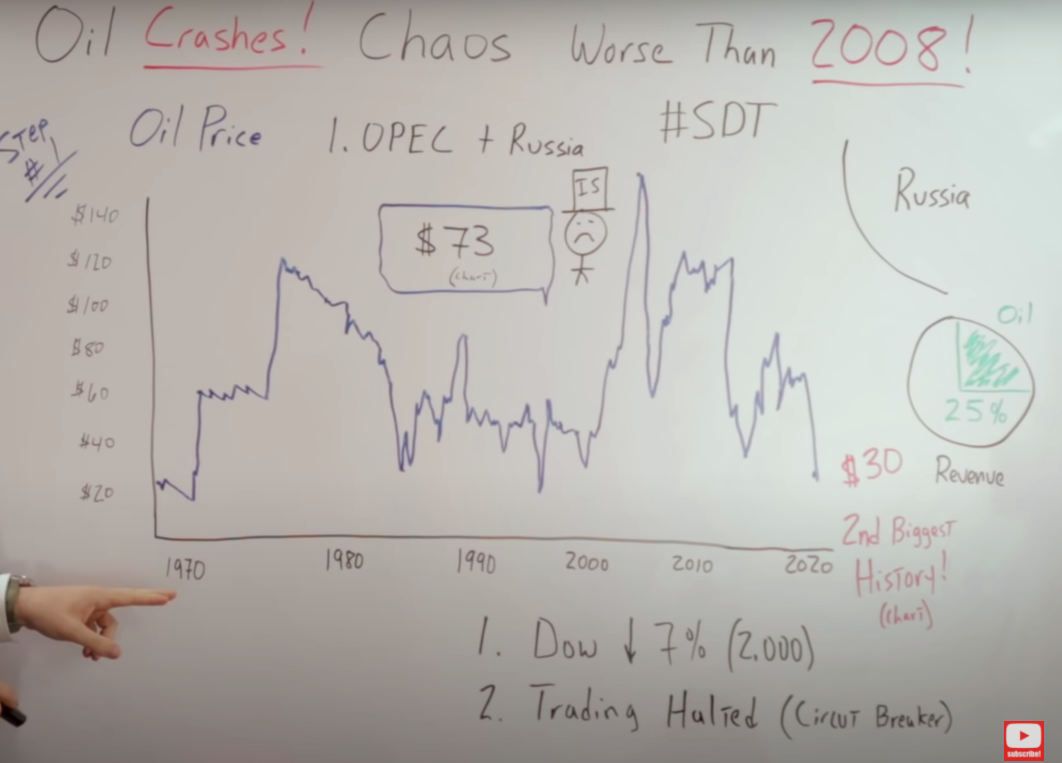

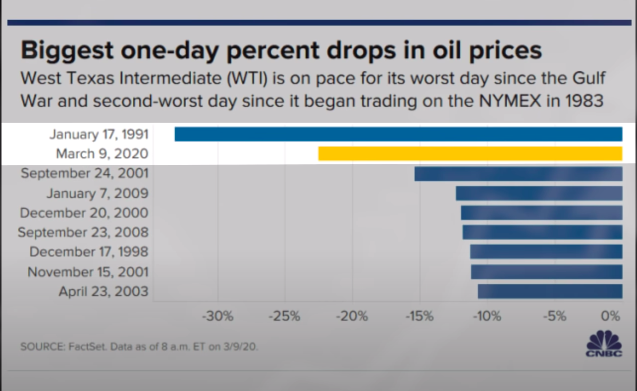

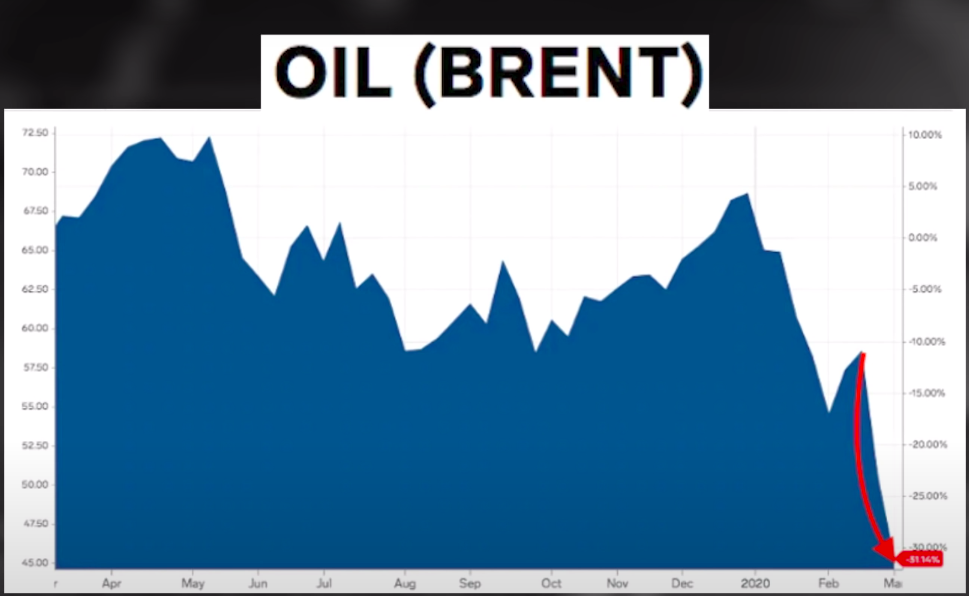

Taking it all the way to the day where I saw some reports, the price of oil on the futures market got sub $30.That drop was the second biggest in history.

Taking it all the way to the day where I saw some reports, the price of oil on the futures market got sub $30.That drop was the second biggest in history.

Oil price crashes 30% as markets open.

Global stocks hit with US crude ar $30 a barrel as Saudi tactics spook traders

– Financial Times

And you may have asked yourself, how on earth did we get here?

Well, it all started in the first week of March when the OPEC met with Russia.

The price of oil was plummeting as a result of COVID 19, and they came together to potentially agree to reduce production and artificially bump that price.

The media outlets headlines were mostly like this:

Russia was not playing ball. One of the reasons is they're a country where a good percentage of their GDP is a result of oil production.

So they said, “We can't afford to reduce the amount of production because we need dollars coming into the country.”

The OPEC got pissed, more specifically, Saudi Arabia, and they said, “Fine. If you want to walk out of the meeting, we'll increase production, and flood the market with oil that'll drop the price. We'll still be okay because we can produce oil at a lot lower cost.”

They gave Russia the middle finger, and that is what pushed the price of oil off a cliff and created chaos in the markets.

When I checked, during March, DOW was down 7%, and I read some reports saying almost 2,000 points were in the red. It was insanity. Trading was halted.

All of this triggered a circuit breaker on the New York Stock Exchange that was not good.

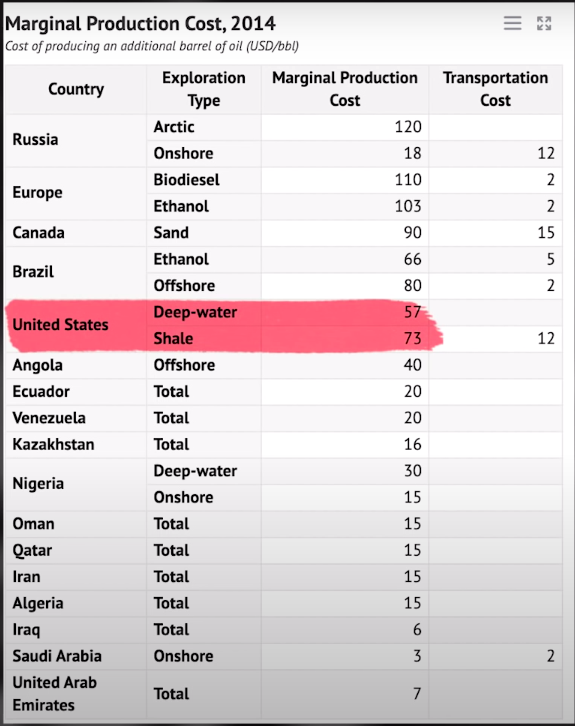

The price of oil, during that period of time in March, was hovering around $30 a barrel, but the cost of producing oil in the United States, especially with the shale producers, was extremely high: $73 a barrel.

This made insolvent Sam, the little guy I drew on the whiteboard with the hat, who could be your uncle, very unhappy when it came to the credit markets.

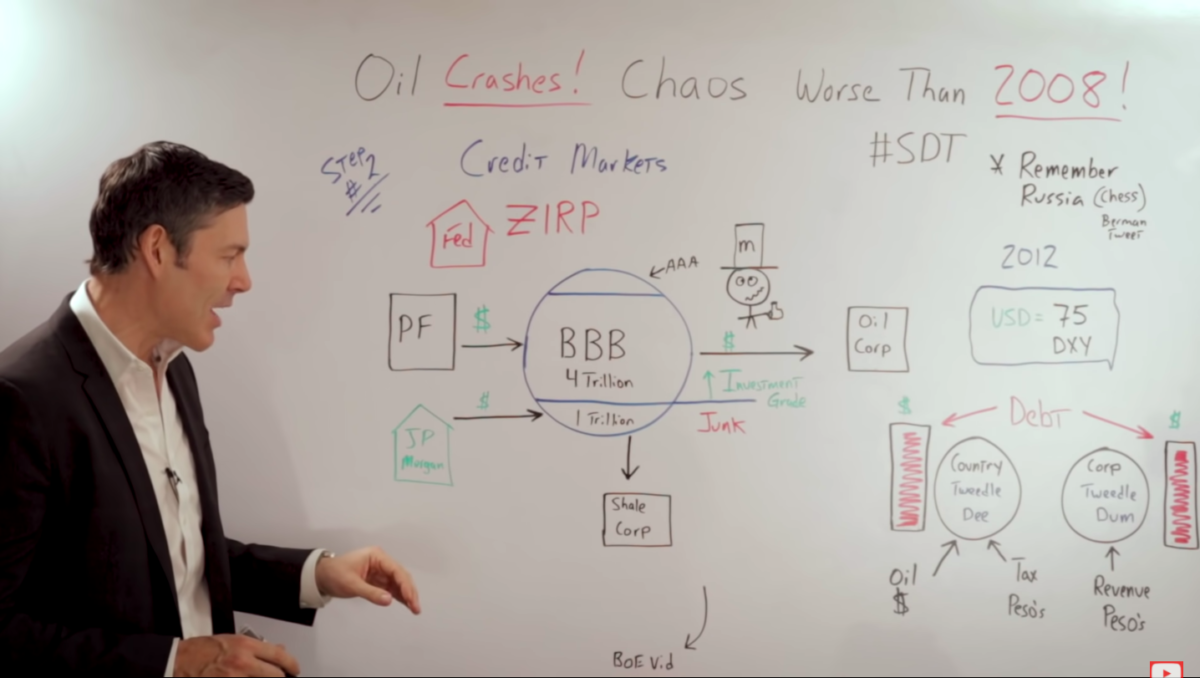

The Credit Markets

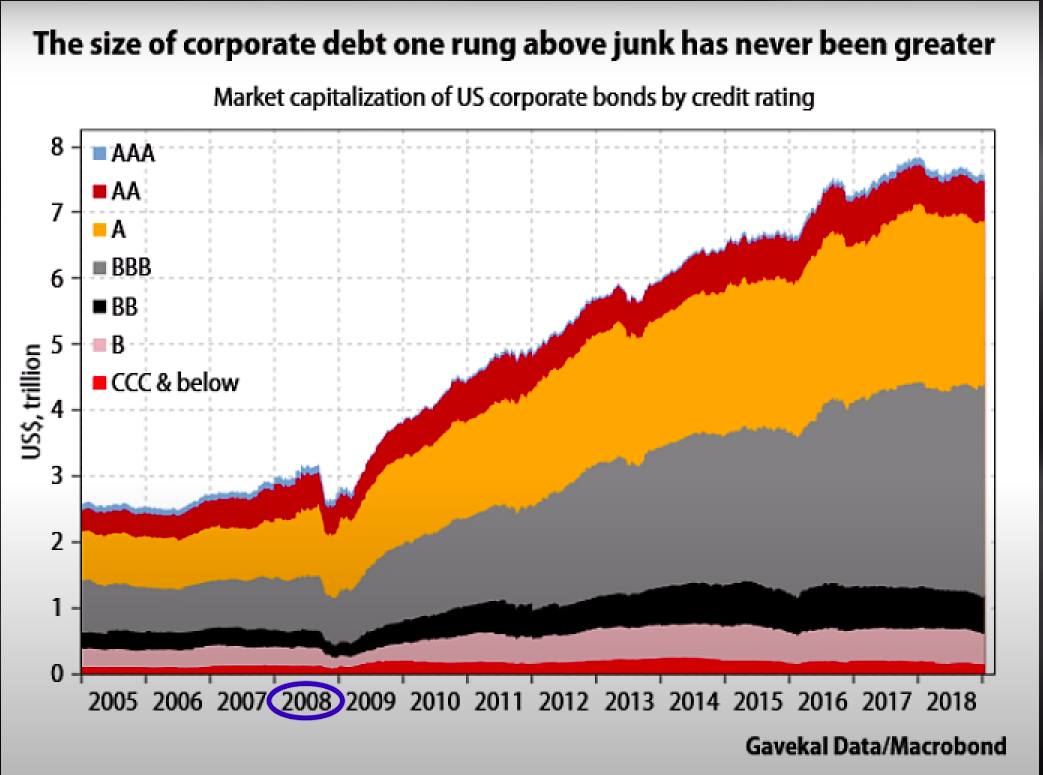

Take a look at the following chart.

-

The US corporate bond market

The US corporate bond market is broken down into two separate categories. Above the blue line inside the circle, there is investment grade. Below that line, junk debt or high yield.

It's crucial you understand the difference between the two. The pension funds can really only put their money into investment-grade debt.

The big banks and other financial institutions, like JP Morgan, could go into the junk bond market and try to eke out that slightly higher yield.

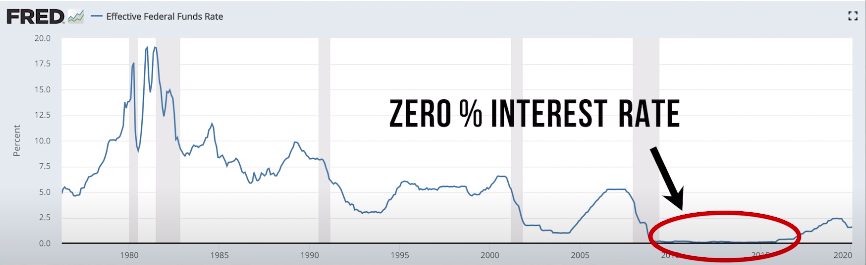

Both of these institutions have been pushed way out of the risk curve because the fed came in, dropped interest rates to zero for over 10 years with ZIRP 0% interest rate policy.

It's important to point out that right on the blue line border of the bond market, on my drawing, there's $4 trillion of triple B rated investment-grade debt.

But if that were to get downgraded into junk, it goes into a market where there's only $1 trillion currently. That's a really big deal.

The gentleman on the board with the hat, who looks like your friend and family member Fred, is the rating guy.

The big difference between him and your friend and family member Fred, is that he is always drunk with his bottle of whiskey, and the big M on his hat that stands for Moody's.

Moody is the one who rates all of the debt, whether it's triple-A triple B, or junk debt.

He has a lot of power because if he downgrades a lot of the triple B debt, that can mean a big problem.

Also, this is the central bank's intent. It seems like it's madness that we're creating all of these unintended consequences, but, when you listen to the central banks themselves, you can see it was what they wanted to pull off.

If you don't believe me, check out this transcript from a video of the bank of England:

Bank of England's monetary policy committee has been purchasing assets financed by new money that the bank creates electronically. This policy is designed to inject money directly into the economy.

The aim is to boost spending to keep inflation on track to meet the 2% target.

The bank purchases assets from private sector businesses including insurance companies, pension funds, high street banks, and nonfinancial firms.

When the bank buys assets, this increases their price and so reduces their yield.

That means the return on those assets falls. This encourages the sellers of assets to use the money they receive from the bank to switch into other financial assets like company shares and bonds.

As purchases of these other assets start to increase, their prices rise, which pushes down on yields generally.

(End of transcript)

Now, taking it back to oil, because those central banks forced all the money to go into riskier assets, most of that money went into oil corporations and to shale corporations.

Over 11% of triple B rated debt is in oil. That's over $400 billion.

Just over 11% of the investment-grade corporate bond market sits within the energy sector, with a host of companies rated BBB, the lowest rung. More pressure on cash flows caused by lower oil prices could result in downgrades, further weighing in junk debt.

-Financial Times

-

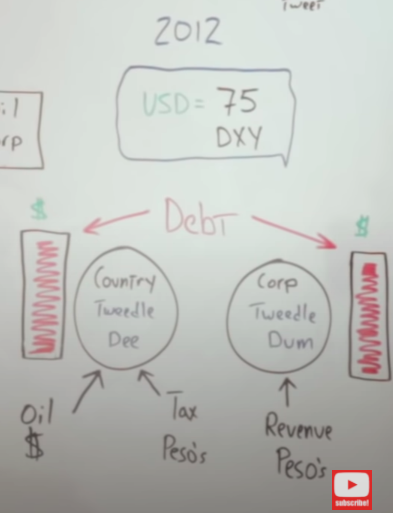

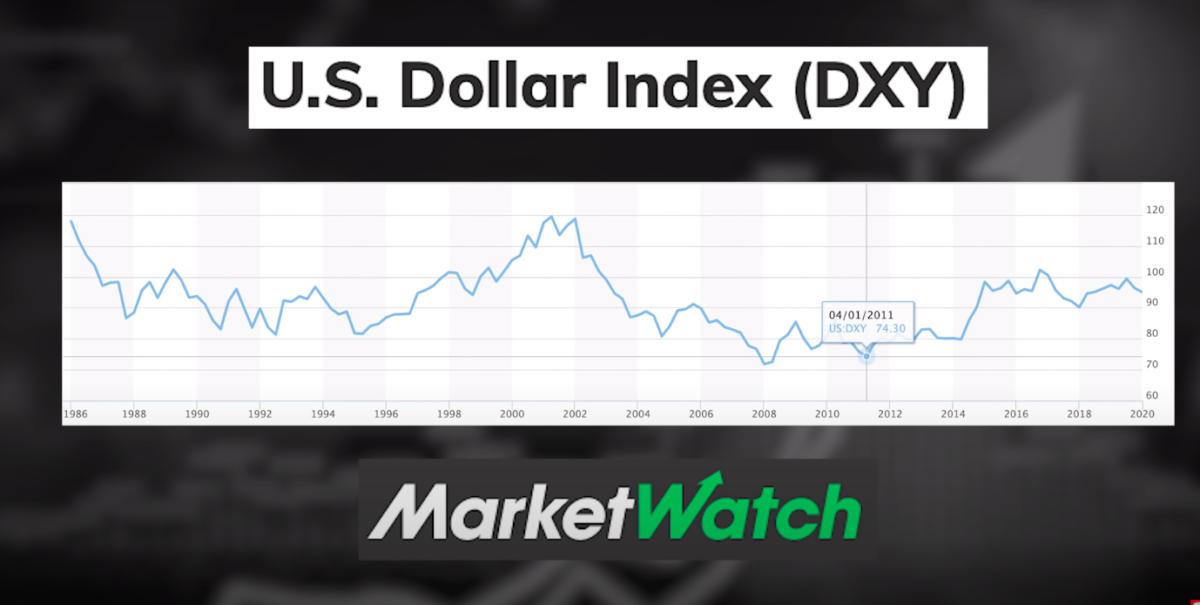

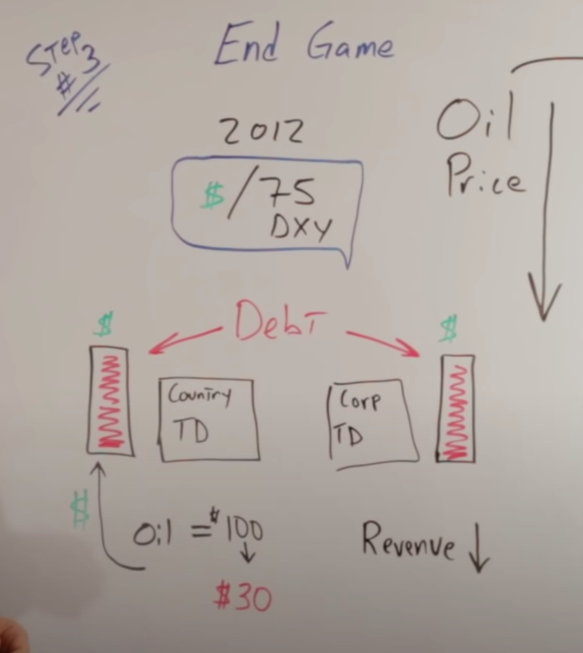

The USD debt market outside of the United States

Look at this illustration of mine for another credit market: The USD debt market outside of the United States.

Countries and corporations in 2012 loaded up on dollar-denominated debt because the DXY dropped all the way right around 75.

To give you some context, it's was at 95 approximately during March of this year, and that has dropped all the way down from about a hundred.

To give you some context, it's was at 95 approximately during March of this year, and that has dropped all the way down from about a hundred.

Plus, the 0% interest rate policy took those rates down so low that this debt was very cheap for them to obtain.

This was a huge benefit for them at the time, but they took a big gamble. A lot of their revenue comes in the form of another currency.

Let's call it the peso. If this trade goes against them, they're going to have a lot harder time servicing that debt.

There were some countries that were big oil producers that said, “well, that's not really a big deal because we have all of these dollars coming in because we sell oil.”

But they forgot that if the price of oil goes from a hundred all the way down to, call it $30, they're going to have a really hard time servicing that debt.

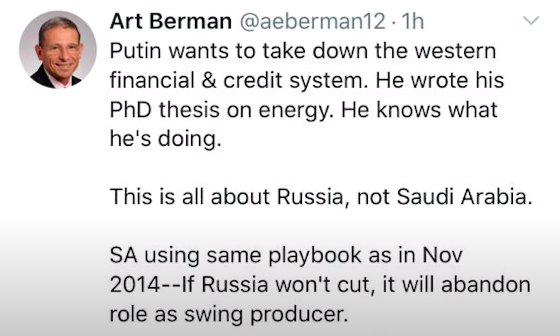

One more thing I want to point out is Art Berman's tweet back in March referencing what I mentioned before, where Russia pulls out of that OPEC deal.

If you're not following Art Berman you need to do that right now. This guy is the leading expert on oil.

Maybe Russia is playing chess while the United States is playing UNO, but I'm going to put the pieces of the puzzle together for you right now.

Oil Price Crash End Game

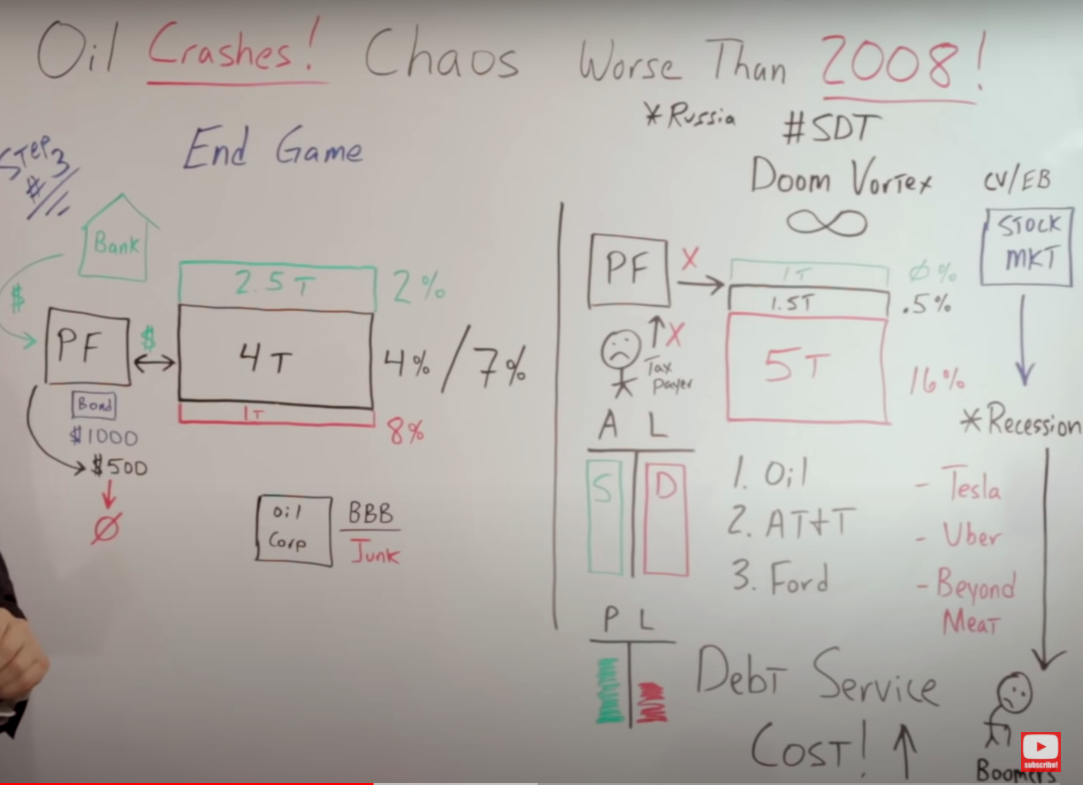

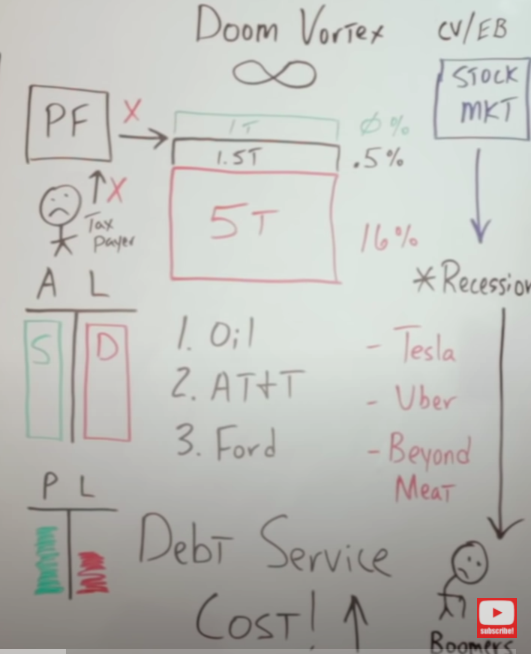

Let's connect the dots going right back to the corporate bond market. Start by looking at the left side of the following whiteboard.

You can see there's 2.5 trillion on AAA, 4 trillion for BBB, and 1 trillion above for the junk bonds.

Notice how much the corporate debt has grown since 2008, absolutely staggering. Remember, the pension funds need that 7% to meet their liabilities.

If they're only getting four by buying the debt of oil corporation, even though it's triple B, they have to go to the bank they levered up in order to buy that debt just to get close to that number they need.

If they have a bond, let's say for a thousand dollars, they might have only paid $500 for that bond. The rest of the money they borrowed from the bank.

If oil corp's bonds go from triple B down to junk, they get downgraded because the price of oil goes down.

The interest rate on that debt, for the sake of this example, let's say it goes from 4% to 8%.

Remember there was an inverse relationship between the interest rate and the value of that bond.

If it goes from 4% to 8%, most likely the value of the bond goes from a thousand down to 500, but they levered up.

They took 50% leverage so their equity goes to zero even though the value of the bond is still $500. This is just the tip of the iceberg.

It gets a lot worse when we come over to the train wreck that I am calling the doom vortex infinity, as shown in my drawing.

And yes, if you're wondering, now is officially stiff drink time. So sit down, pour yourself that glass of whiskey, because you're going to need it.

The oil prices were crashing and while that was happening, the COVID-19 was wreaking havoc that everything bubble was going to turn into everything crash.

The stock market was plummeting and it went down 1800 points the last time I checked, during the month of March.

This had a huge effect on the corporate bond market.

Why? Going back to 2010, all the corporations loaded up on debt to buy their own shares back.

So moody the drunk ratings guy saw the value of their assets going down and downgraded them from triple B into junk status.

Even though the oil corporations were only 11% of the total pie, there was a possibility of having a scenario where the majority of the triple B debt was downgraded into junk.

Also, interest rates increased dramatically because we had an additional 4 trillion of supply hitting the same limited pool of capital.

But, let's be gentle for a moment and assume interest rates only double going from 8% to 16%.

How do these corporations service their debt?

I'm not just talking about oil, but blue chips like AT&T and Ford that have loaded up on debt over the last few years to buy back their own shares.

If interest rates go through the roof there's no way they're going to be able to service that debt.

Also, let's not forget we're most likely going into a recession/depression, and in a recession, the revenue of these corporations goes down.

So they have less cash coming in while at the same time the amount of debt, or their debt payments, are going to infinity and beyond.

I haven't even talked about all those corporations that are already in junk status like Tesla, Uber, and Beyond Meat. I'm not sure if Beyond Meat is, but if they're not there now, they definitely will be in the future.

All of these corporations are burning cash. So there's no way they're going to be able to go back into the market and take that money at 16%. They can't afford it. They will all go bust. That is the bottom line.

But, going back to the pension funds on the left side of the whiteboard, even if they were able to survive this debacle, they go back into the market, and now there's a much larger pool of cash for a limited supply of investment-grade debt.

That has the opposite effect, instead of increasing interest rates that dramatically lowers them.

So if they couldn't get yield at 7% yield nor 4%, there's no way they're going to be able to get it at zero or 0.5%. Then they go to the taxpayer.

The states say, “listen, our pension funds are completely bust.” They increase property taxes or do anything they can to get that last dime out of your back pocket.

But they're increasing these taxes as we go into a recession.

What happens to the tax revenue in a recession/depression?

It falls off a cliff.

There's no way the pension funds will be able to survive, and the baby boomers are all retiring!

Who has been the main driver of the stock market, other than the corporations, over the past 25 years?

Baby boomers putting all that money into their 401k!

If we go through a crash, there's no way that they're going to buy that dip, they can't afford to.

We're left with a situation where there are no buyers in the junk bond market and there's potentially no buyers in the stock market, and all of it feeds on itself.

I think it can all start with oil prices crashing, COVID -19, and this everything bubble that the Fed has created coming crashing down. That's why I call it the doom vortex infinity.

It goes back to the price of oil, where you have to ask yourself…

Did Putin just throw a hissy fit or is he playing a three-dimensional game of chess with the United States economy and the dollar?

Oh, but wait, there is more.

Remember there's another credit market I mentioned before?

Country Tweedledee (TD) and corporation Tweedledum loaded up on USD debt in 2012. They still have the debt, but oil goes from a hundred to $30 and puts them in a bad spot.

Country Tweedledee has two options:

1. Go into the FX market, print their own money, buy the dollars they need

This devalues their currency, creates domestic inflation, crushes corporation Tweedledum because their revenue is in the form of that devalued currency, but they still have the dollar-denominated debt.

2. Pump more barrels of oil out of the ground

If they have a thousand dollars in debt, before, they needed 10 barrels of oil to service the debt. Now they'd have to pump over 30 barrels of oil to get the same amount of dollars.

This creates a greater supply of oil in the open market. It's just supply and demand. There's more supply, the price of oil goes down, which makes the doom vortex of infinity much worse.