The big banks are getting bigger and bigger and the small banks, which are the growth engine of our economy, are being eliminated.

There's this barrier that's been built around the big banks that eliminates competition. It prevents smaller banks from coming in and competing with them. Things like Compliance Standards.

As an example, if there's a new regulation that comes down the pipeline, it costs $100 million to comply with it. Only banks that can afford the $100 million like the big banks will survive.

Whenever we have a banking crisis, we always want the government to come in with all these regulations to make the banking system “stronger.”

What we don't realize is they are the problem. The government is the problem in the first place.

For more content that'll help you build wealth and thrive in a world of out of control central banks and big governments, JOIN our Daily Newsletter for FREE!

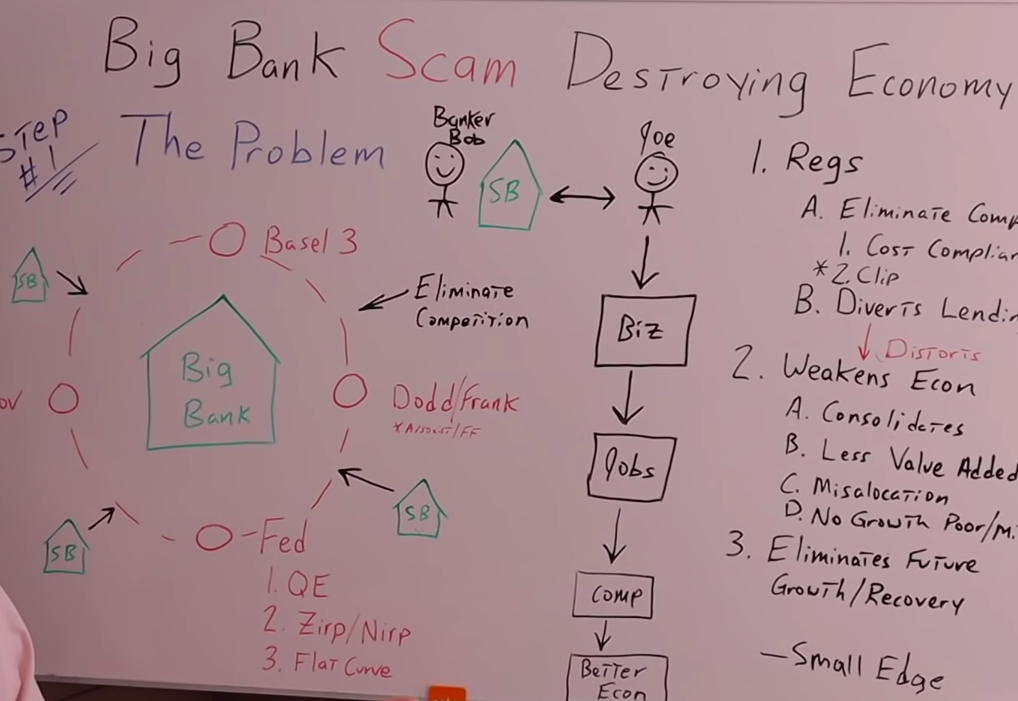

The Main Problem: Big Banks Are Getting Bigger And Bigger

Take a look at this illustration of what's going on. Small banks, which are the growth engine of our economy are being eliminated. There's a barrier that's been built around the big banks that eliminates competition.

This prevents smaller banks from coming in and competing with them, things like compliance standards.

For example, if there's a new regulation that comes down the pipeline that costs a hundred million dollars to comply with, and only banks that can afford the hundred million dollars, as the big banks, will survive.

We see this with things like Dodd-Frank and Basel 3. It's that old story with the arsonist and the firefighter being one and the same.

Whenever we have a banking crisis, we always want the government to come in with new regulations to make the banking system “stronger”. What we don't realize is they are the problem, the government is the problem in the first place.

We haven't even talked about the Fed that really prevents the small banks from competing with things like quantitative easing, 0% interest rates, negative interest rates, especially and flattening the yield curve.

You may be asking…

“Why are the small banks important in the first place?”

To dive into greater detail, here is a little transcript of a video I saw with one of my favorites, Professor Richard Werner.

Professor Richard Werner:

What you will get is large banks, only wanting to deal with large customers in order to do large deals. That's also where you get the large bonuses.

We've done the study on the U.S. which has the biggest banking sector in the world with over 15,000 banks of all sizes and shapes.

The very large banks deal with the very large customers and give very large loans. The medium-sized banks give medium-sized loans.

Who is lending to small firms?

It is only the small banks. Now, the UK doesn't have those.

The structure has become too concentrated and what is badly needed in the UK is decentralization. One has to break up the financial sector and have much smaller units because small banks, community banks are locally accountable.

You can't suddenly do a crazy project or big corruption.

(End of transcript)

The big banks only do huge loans to big corporations, and the small and midsize banks are the ones that we really need to support small and midsize businesses that are so vital to the health of our economy.

But that's not where the story ends. It gets more interesting when we think about how these small and midsize enterprises create jobs, goods, and services. Productivity.

To explain that further, read the second part of Richard Warner's interview.

Professor Richard Werner: The banks create the money supply by inventing these claims on themselves.

The fictitious deposits can be positive for the economy as long as the money creation is in line with the creation of new goods and services, implementation of new technologies, and therefore adding value.

Adding value to the economy is funded by this money creation. If that happens, and we're talking about business, investment, productive loans, productive bank credit, you will have no inflation.

The loans can also be serviced and repaid and you can have a stable economy without problems, with low inequality.

Countries that achieve this have banks that lend mainly for productive purposes, whether it's Germany and much of its 200-year history, East Asian economies where bank credit was largely for productive purposes, then you're fine, but there are two more cases.

Interviewer: Just to clarify, inequality is significantly lower, inflation is low, and the real economy is rising.

Professor Richard Werner: Is booming yes. That's when bank credit creation is focused on productive lending for productive purposes.

Interviewer: As opposed to speculation and asset prices.

Professor Richard Werner: There's two other types, if banks create credit for consumption it's obvious what's going to happen.

You suddenly have more money created and more demand for goods, but it's the same amount of goods and services. So, you're creating consumer price inflation that's well understood.

Central banks are watching that a little bit. What's less well understood is it's probably more than 70% of all lending actually, way more than that is bank credit creation.

Money creation for financial transactions, asset transactions, purchasing ownership rights. Now then you have a problem, why? Because you're creating new money, but you're not creating new goods and services.

You give somebody new purchasing power over existing assets and therefore you must push up asset prices.

(End Of Transcript)

The main takeaway is the reason these small banks are so important: They support the small and midsize businesses.

Small Banks Generate Productivity

Let's think this through by looking at the following example in my drawing. We have a small bank(SB) number one on the top and it's run by banker Bob. He is very close to the community and he knows everybody in the neighborhood, like average Joe (on the right).

He has known average Joe since they were little kids. They were together in third grade and all the way to high school. Maybe they even played on the same football team.

They know each other extremely well. This is crucial.

Average Joe goes to Baker Bob and says,”Listen, Bob, I've got this fantastic idea for a business. I want to start a fishing store that sells fishing poles and lures. It's going to be amazing. We're going to compete with Bass Pro Shops.”

Banker Bob knows that Joe is someone that's hardworking and trustworthy, so he ends up giving him the loan. Therefore, Joe creates a business that creates a lot of local jobs.

He continues to grow the business, and over time, maybe he does build something that competes with one of the big players like Bass Pro Shops.

His business creates a better and more diversified economy.

Instead of having all of our eggs in one basket with these huge banks and big corporations.

This is why you'll notice that a lot of the big corporations are in favor of things like compliance standards and the minimum wage. They know it eliminates people like the average Joe from competing with them.

Joe never would've been able to get that loan from one of the big banks, because he's not worth their time. It's such a small loan.

It doesn't make sense, and they don't know Joe. They didn't go to third grade with him, and they didn't play on the same football team.

Whether we like it or not, that's really important to human beings. We prefer to do business with people we know well.

So the regulations that come in…

- Eliminate competition

- Increase the cost of compliance

- Divert lending and resources away from small and midsize businesses to huge corporations.

But, more importantly…

How does this weaken the economy?

- It consolidates everything. We've got all of our eggs in one basket.

- There's less value added to every individual. It only goes to a certain select group.

- It misallocates resources.

- There's no growth in the poor and middle class.

Notice I didn't say wealth inequality. I'm trying to get away from that term because I think we're too focused as a society about the gap between the poor and the wealthy, instead of just trying to improve the lot of the poor.

-

Don't we just want their standard of living going up, regardless of what happens to the wealthy?

-

Would we prefer that everyone was equally poor?

I don't think so.

By not supporting the small and midsize businesses, we're really eliminating future growth, especially healthy growth. That's sustainable.

We need this now, more than ever, when we're trying to go into recovery. I can promise you one thing, we will not get a sustainable recovery focusing only on big banks, huge corporations, and government regulation.

It's going to need to come from everyday individuals like you and I starting businesses, creating jobs, and competing with the big guys.

A lot of you might be saying “George, that's impossible. The little guy can never compete with the big players”.

But what you don't understand is those small businesses are very nimble. They have a lot of advantages that people who have never been entrepreneurs don't recognize.

Take it from me. I have never run a big, huge corporation, but I have run businesses from 0 to 10 employees. I've also run businesses with over a hundred employees.

Although the business with a hundred employees did have its advantages, it had a lot of disadvantages as well.

It's very hard to move quickly, create a product or a new service because you had all these layers of management and human resources that you had to go through.

I can't even imagine how difficult it would be if I had a thousand employees or if I was a huge corporation like Google, Facebook, or Boeing.

It would be almost impossible to do anything new and innovative.

Where if you have a little business with 10 or 15 employees, yes, you might not have the resources, but you can make decisions quickly and get to the market faster than the big guys.

The bottom line is you have to realize there are a lot of advantages to being small, and if we support these people, they can compete.

-

What is the ultimate solution?

-

How do we prevent these monopolies from forming in the first place?

To explain this a little further, take a look at what Milton Friedman says in one of his interviews.

Interviewer:

How do you prevent a monopoly?

You have to have constraints on monopoly. Isn't United Airlines too big?

Look what happened when they went on strike. Should Pan Am absorb national airlines? We're going to have three airlines when it's all over and we're all going to be beholden to them.

You can see it now on the airlines. Nobody looks you in the eye anymore and they're giving paper cups in first class.

Milton Friedman: Personally, I don't see any objection to paper cups, but let's go back. The problem with the kind of statement you're making is to distinguish what's true from what's not true.

The plain fact is that the main on the number of airlines has been the Civil Aeronautics Board.

From the time the Civil Aeronautics Board took over control of the airlines in the 1930s, until now, until the deregulation, they did not authorize a single new trunk line. The number of trunk lines was less.

Interviewer: Because they were owned by the airlines who didn't want any more competition. So the government then became an agency to help the existing airlines, not to have to compete.

Milton Friedman: Exactly. Now, what happened with deregulation?

Interviewer: You filled every seat in the airplane.

Milton Friedman: The number of airlines has gone up, not down. It is true that there are some proposals to merge Pan Am National, but there are also a bunch of new airlines that are coming out.

Here's World Airways, whom you never heard of before that's offering cheap fares. Freddie Laker broke the TransAtlantic monopoly.

There's an old saying. If you want to catch a thief, you set a thief to catch him. If you want to catch a businessman's monopoly, you set another businessman to break it down.

You don't send a government civil servant after them.

The most effective anti-monopoly legislation you could possibly have would be free trade.

(End of interview)

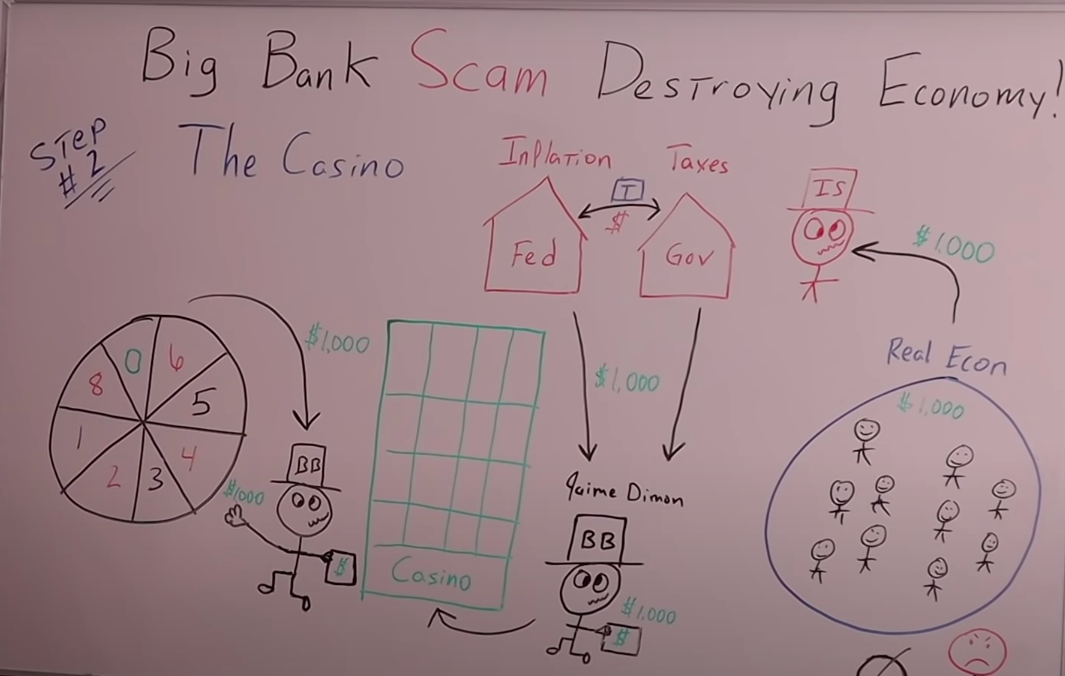

We Are Headed For The Opposite Of A Free Market Solution: We're Heading To The Casino

Unfortunately, we're not headed for a free market solution. We are headed straight for the casino. In fact, we already went to the casino in the early 2000 and 2008, 2009 to the GFC.

I know most of you understand how it works, but I wanted to put it up on the dry erase board. I think it's more impactful if you have a visual.

It starts with the big banker(BB) himself named Jaime Dimon, obviously Hispanic gentlemen.

He goes to the casino with a thousand dollars in his suitcase full of cash because he knows that if he wins at the casino, he gets to keep the profit.

If he doesn't, he gets bailed out by the Fed and the government. He goes straight to the roulette wheel, puts it down on red, number four, and if he wins, he now has $2,000.

But if he loses, as I said, he still has his thousand dollars that he started with because the Fed and the government will bail him out through the form of additional taxes or future inflation.

We always kind of get fixated on the left part of the board, but we forget the real economy.

If the real economy started with a thousand dollars of purchasing power, after Jaime gets his butt handed to him at the roulette wheel, you're drunk insolvent.

Uncle Sam with the red hat says, “Oh, we have to raise your taxes” That thousand dollars of purchasing power go straight to Sam, then straight to Jaime.

If Sam doesn't increase your taxes, then he goes to the feds saying “Fed, I've really got a problem. I need you to help me out. My back is against a wall. I promised Jaime that I'd bail him but I can't do it because these people, the average Joe and Jane will be pissed if I increase their taxes.”

The Fed says” No problem, Sam, we'll help you out. We'll print up all this funny money and buy your treasuries so you can bail out your crony Jaime.”

The Fed monetizes, the debt increases based money and broad money, which will most likely lead to future inflation.

Whether that's for you right now, your kids, or your grandkids. The bottom line is there's no getting around it.

If Jaime loses at the casino, he'll be made whole, but your purchasing power will go from a thousand dollars down to zero.

You may be asking yourself, George, why is Jaime taking a knee all the time? Because Jaime knows it's way easier to virtue signal than to actually do something about the problem.

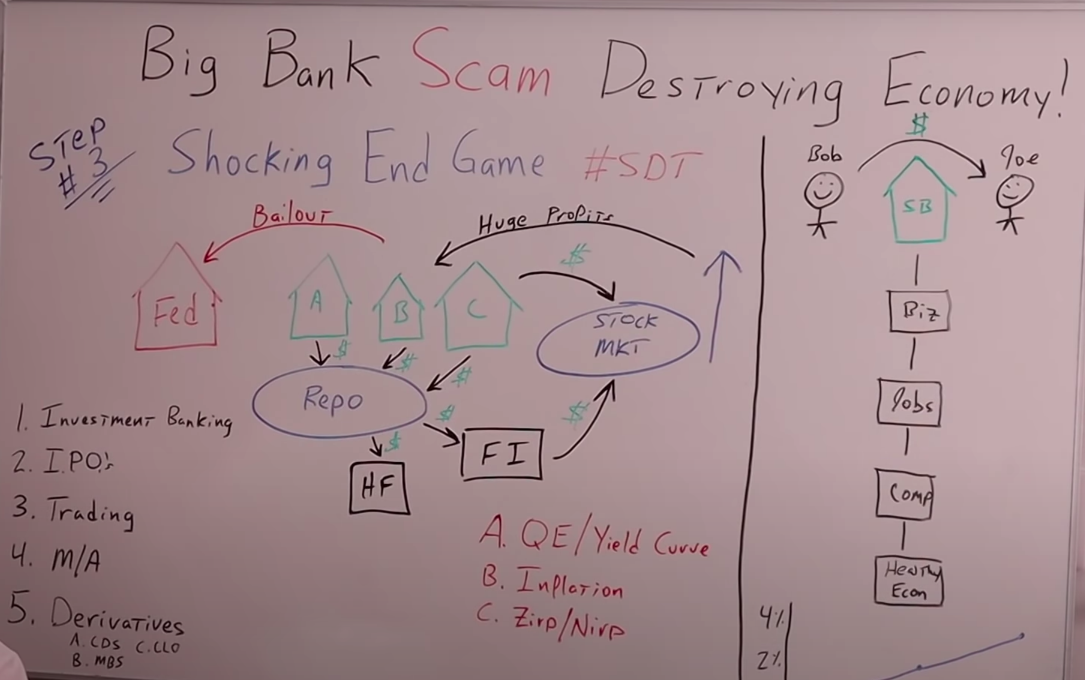

The Potential And Shocking End Game

Here is the third example, but first, let's focus on the left side of the dry erase board.

We have the Fed in red, the other big banks with green, and the primary dealers that are under the feds umbrella.

The Fed comes in with a lot of liquidity through quantitative easing and a trillion dollars a day in repo commitments.

This gives additional capacity to the balance sheets of primary dealer banks, A, B, and C. So they go right into the repo market.

The money goes to the hedge funds and the financial institutions take it to the stock market. Plus the dealer banks are going into the stock market themselves, so all this liquidity going in, drives prices up.

That means huge profits for all of the big banks because they're making their money on the following things :

- Investment banking

- IPOs

- Trading

- Mergers and acquisitions.

- Derivatives: Creating credit, default swaps, collateralized loan obligations, and mortgage back sausages.

Everything that creates a healthy, strong economy that we would want our banking system to do. Obviously you can sense the sarcasm there.

Compared to the small banks that actually make money by doing productive lending.

Instead of these types of transactions that makes our economy weak and builds this house of cards. It's built on a foundation of sand.

Going back to our example number one, what Bob would do to make money, if very different. He wouldn't create derivatives. He wouldn't create mortgage back sausages.

He would lend money to Joe. That's productive! Then, Joe takes that money to create a business, starts jobs, competes with the big corporations, and produces a strong, healthy, diversified economy.

In order for Bob to continue this type of productive lending, he needs a positive sloping yield curve.

In other words, if we have three month T-bills, 10-year treasuries, and 30-year treasuries, he needs the 30-year treasury to yield a lot more than the short end of the yield curve at fed funds rate or three months.

Because his business model is that he borrows short and lends long. A way to think about that is his liabilities have a lower interest rate, then his assets and he's pocketing the spread.

If the Fed comes in with quantitative easing to try to flatten the yield curve, thinking it'll stimulate the economy, what happens to Bob is he can't make any money because now he's paying the same for his liabilities as he's getting for his assets, there's no spread.

It doesn't go from 1% to 4%. If it stays at 1% the whole way, there's no way for Bob to make a profit.

He goes out of business and it makes matters worse if you create inflation, because inflation is what Joe is paying Bob back with cheaper dollars.

Therefore, Bob is taking a haircut and he can't create more loans in the future for Joe's kids or Joe's grandkids. Is really this cycle.

It gets even worse when we look at negative interest rates, how can the small banks survive if they have to pay to give loans? Think about that. That's how they make their money.

If the way they make their money goes from a profit center to an actual expense, they're done, they're all going bust, which will completely destroy the real economy.

Meanwhile, the big banks are making money hand over fist because they don't do any retail lending. They don't deal with Joe. They just deal with financial assets that are being propped up by the fed.

Think this through. The fed, if they're smart and that's a big if, they know what they're doing is destroying the small banks, but they also know what they're doing with the big banks: Creating a huge boom and bust cycles.

It might be good for the Jaime's of the world while we have a boom. But when we have a bust, they need to go to the fed to get a bailout.

-

What happens in the future, if the Fed doesn't bail them out?

They're holding all the cards.

We could go into this future scenario where all the small banks are completely wiped out.

The power has been consolidated to the big banks, but the Fed is creating an environment where eventually they'll have to come into the Fed to survive. They'll need that bailout.

If the Fed doesn't extend the bailout to them, all of a sudden they're bust as well and the only bank left standing is the fed. The ultimate consolidation of power.