You've received some good advice on the thread but I think most have glossed over the most important topic…inflation.

Let me start by putting it to you this way.

30 year fixed rate mortgages

The US is one of the only countries on the planet, I'm actually not aware of any others, where 30 year fixed rate mortgages exist.

Why? Because in a free market these loans don't make financial sense for the lender.

In other words, banks don't offer them because they lose money.

So if banks are losing money on these mortgages, borrowers are making money on these mortgages, regardless of how lopsided they may seem to you.

How do these financial unicorns not only exist but thrive in the US?

Because our taxpayers subsidize them.

Just like food stamps, or welfare, it's a transfer payment from the taxpayer to the recipient, or in this case, the borrower.

Unfortunately, most Americans don't like calling a spade a spade so we refer to these transfer payments as Fannie and Freddie.

Fannie and Freddie buy these money-losing loans from banks who originate them.

If, or more likely, when Fannie and Freddie realize these losses, you/me and every other American taxpayer bail them out.

Again, it's a transfer of wealth from the entity holding the paper (F&F) to the borrowers, then F&F is bailed out by the taxpayer.

So transfer payment from taxpayer to borrower and F&F facilitate the transaction.

And inflation is why 30 year fixed rates are money losers.

In the GFC, everyone knows F&F was bailed out because it was holding the bag on so many mortgages that defaulted.

But think about what a default is…essentially it's the bank not being paid back how much it lent.

Like a straight default, inflation is also the bank not being paid back how much it lent.

To understand this you've got to temporarily suspend the way you think about money. Money is only purchasing power.

So it's not just about the number of dollars the bank receives from the borrow, but how much goods and services (purchasing power) of the dollars the bank receives.

As an example. If you borrowed $1000 in the year 1900 and paid it back in the year 2019, the lender would have to receive almost $26,000 to break even.

And keep in mind, we've had very low inflation for almost 40 years. Let's look at the 1970s as an even better example.

If you borrowed $10,000 in 1970, the bank would have to receive $21,000 by 1980 to break even.

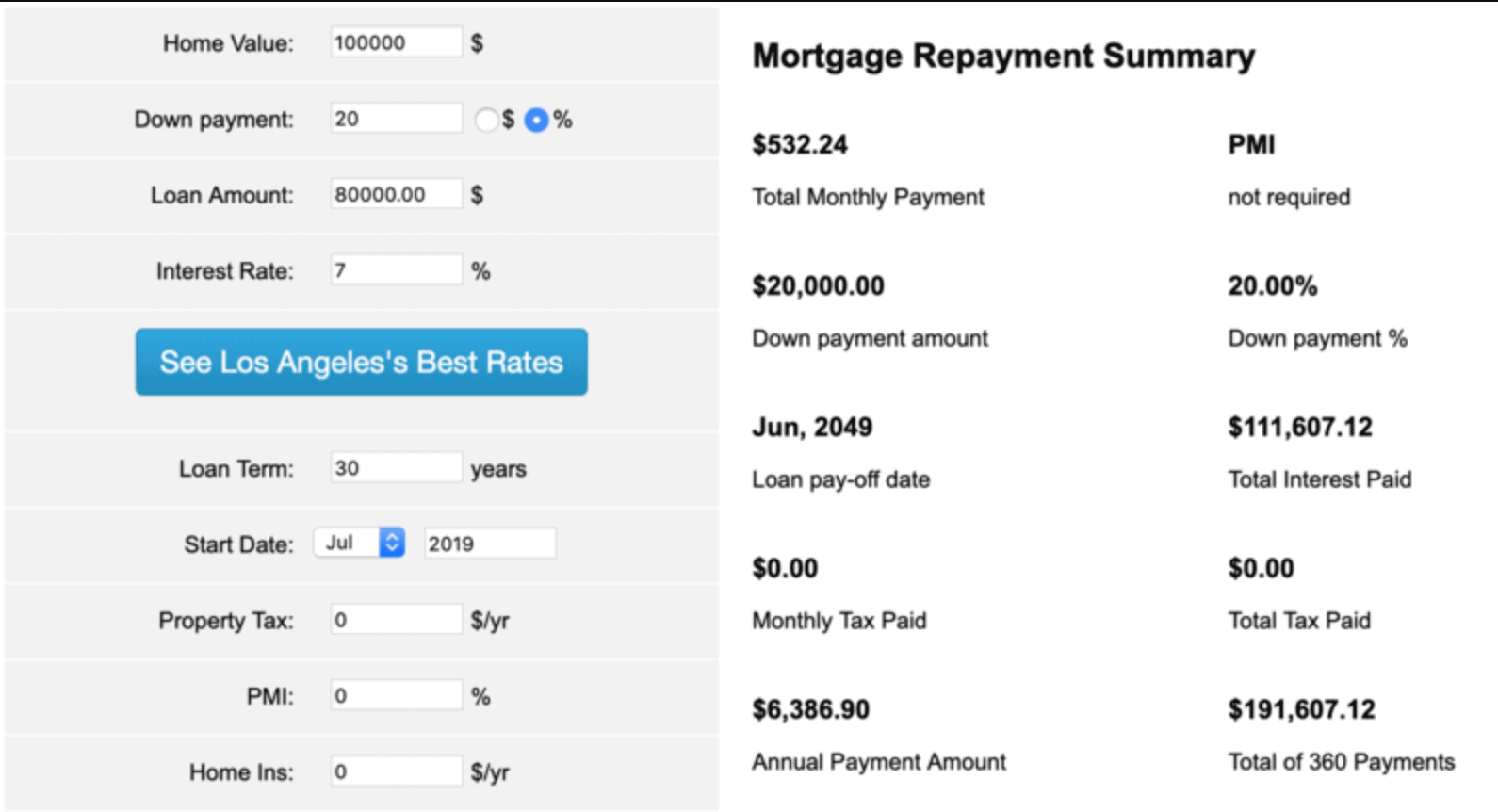

Let's use even more specific numbers. Here's a $100,000, 30 year fixed rate loan, with a 20% down payment (so 80k loan) at the going rate in 1970, about 7%.

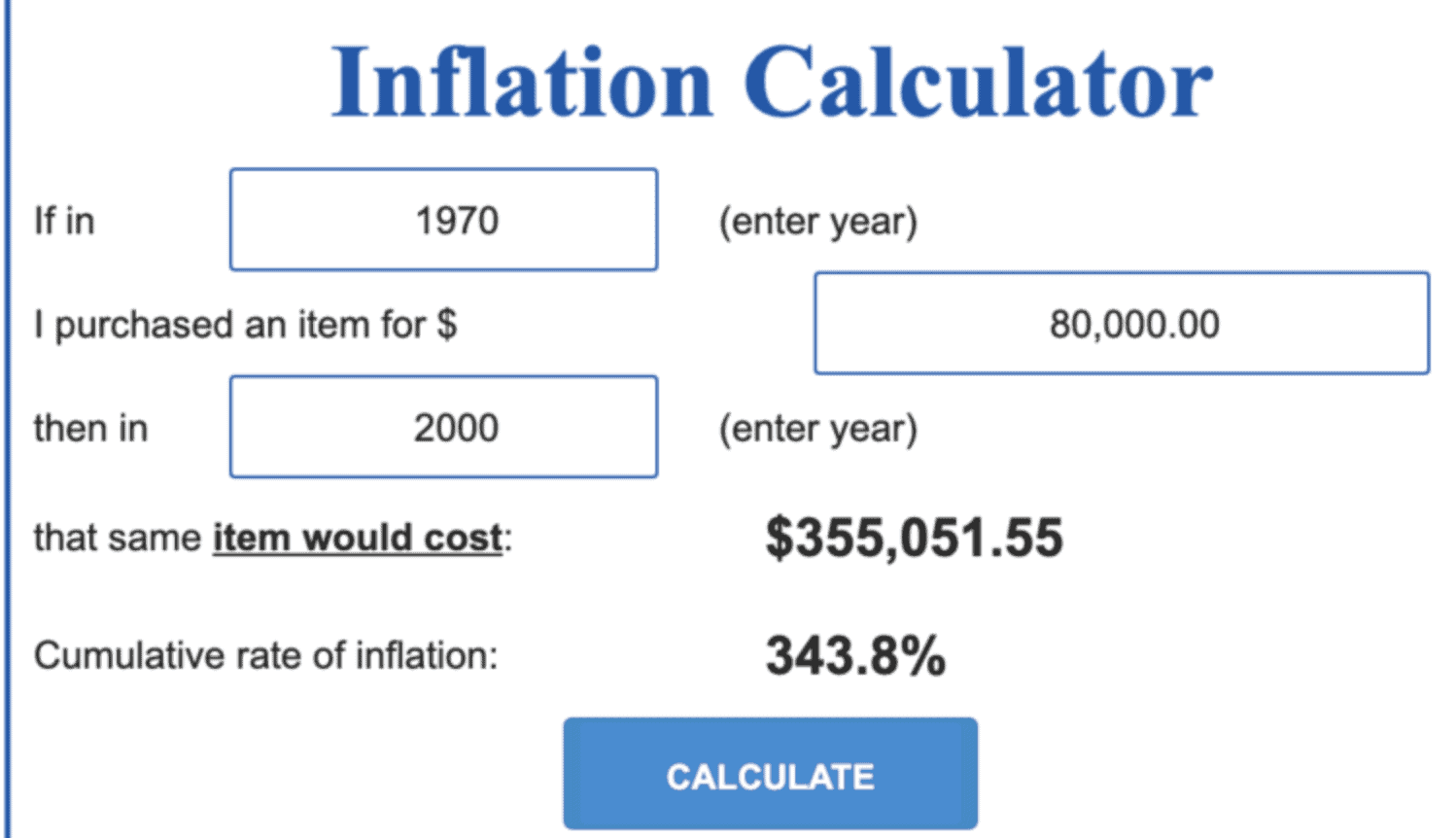

As you can see, the bank would receive a total of $191,607, over the 30 years, for lending you 80k. Now, check out 80k put into an inflation calculator, for 30 years, starting in 1970.

Ouch…355k. That's a massive loss for the bank. But this would be a massive gain for the borrower.

Now, remember the US is the largest debtor nation in the history of the world.

23 trillion in debt and that doesn't include unfunded liabilities, which some estimate to be north of 200 trillion.

And the only way to solve a debt problem is

- Default or

- Inflation.

Point being, there's a tremendous tailwind for inflation over the next 30 years, not to mention interest rates worldwide are at near 5000-year lows.

So the big takeaway is: use as much 30-year fixed-rate debt as you can get your hands on! 😉

George

Comments are closed.