Are Real Estate Investors Asking The Wrong Questions?

Real estate investors are a rare breed. I've never seen a group of “investors” with a more myopic view of macroeconomics and the basic principles of investing.

To invest in anything well, including real estate, stocks, bonds, currencies, commodities, precious metals, (consistently over long periods of time) the prudent investor buys low and sells high…or what I like to say is ” buy cheap” and “sell expensive” which often gets confused with “buy at the bottom and sell at the top”. Two different things entirely.

As a whole, Real estate investors get fixated on the wrong questions. Is the market going higher? Is the market going lower? Is the market in a bubble?

These questions are a fool's game. The correct questions to ask are:

Is the market historically cheap?

Is the market historically expensive?

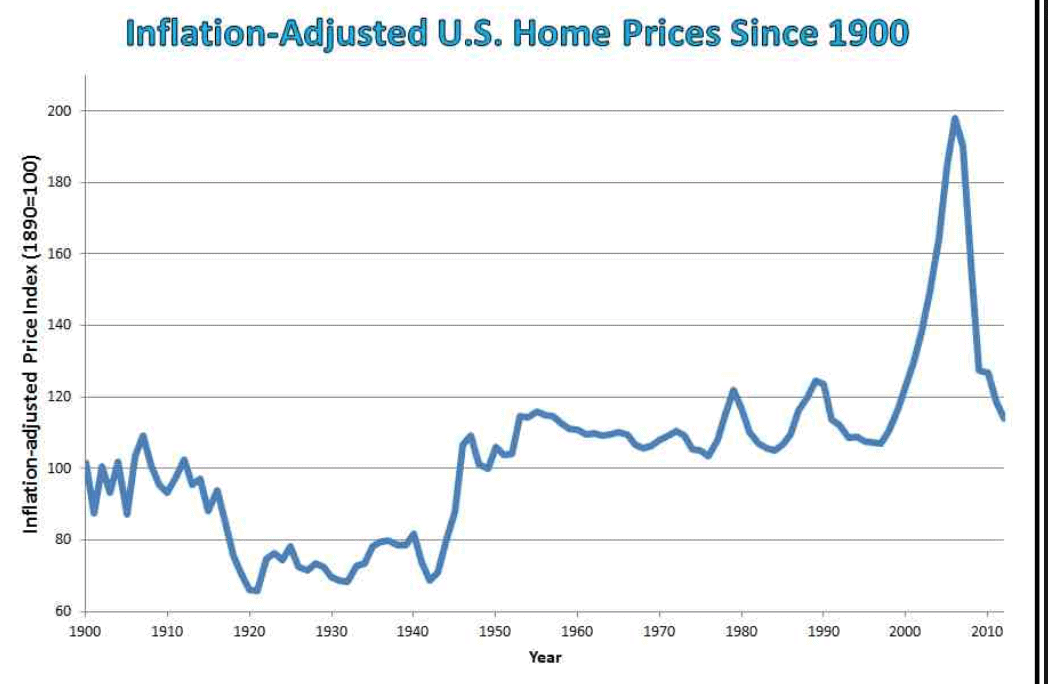

Let's look at an inflation-adjusted chart of US housing prices going back to 1890…

As you can see housing prices in the US really just kept pace with inflation for over 100 years, with a few exceptions, which mean reverted.

Then came the 2000's. We all know what happened then.

But looking back on 2006, can anyone say with a straight face, after looking at the chart above, prices weren't expensive?

Yet today, for some reason we use 2006 as a benchmark for where housing prices start to become expensive.

On this thread, you'll see people reference housing prices, in many areas, haven't even got back to 2006 levels, as if prices in 2006 were healthy?

Prices in 2006 were the equivalent of a natural 150-pound man taking steroids to become 250 pounds.

So when the same man, stops the steroids and drops back down to 150 pounds, then starts them again to get back up to 245 pounds, should we say he's healthy because he's not even back to 250 pounds yet?

Of course not, so why would we use the high watermark of 2006 as anything other than a warning sign of prices being expensive again?

And the only argument against this logic would be to say prices weren't artificially high in 2006. Or that real wages have increased as much as housing prices.

Is anyone going to claim that?

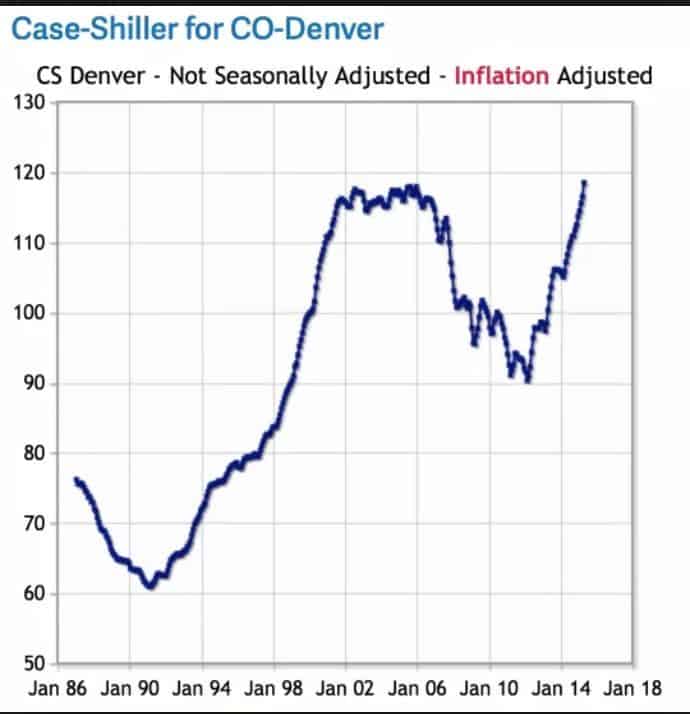

Unfortunately, this chart only goes to 2010 but we all know what prices have done since. And if you're not clear, here's a chart of current housing prices in Denver relative to 2006.

So again, when we ask the correct question, the answer becomes very clear.

Not are prices going up or are prices going down?… But are the prices cheap or are they expensive?

If you buy assets when they're cheap, and sell when they're expensive, you might not catch the bottom or the top, and you might miss a big move, but over the long haul you'll be in the game and you'll make money.

So when anyone says “don't wait to buy real estate, buy real estate and wait…” point them to the chart above showing real prices going back to 1900.

And please note the fact, if you would've bought in 1900 and “waited” until 2012 you would've made exactly zero dollars adjusted for inflation.

Nay Sayers will point out XYZ market has tripled in the last 30 years etc.

And of course one of the main things they ignore is the US (and most of the developed world) has been in a bond bull market since 1980.

In other words, interest rates have gone down for almost 40 years.

Do lower interest rates make mortgage payments lower or higher? 😉 And lower monthly payments mean increased purchasing power, which translates into increased affordability and demand.

But this process works in reverse when interest rates go up.

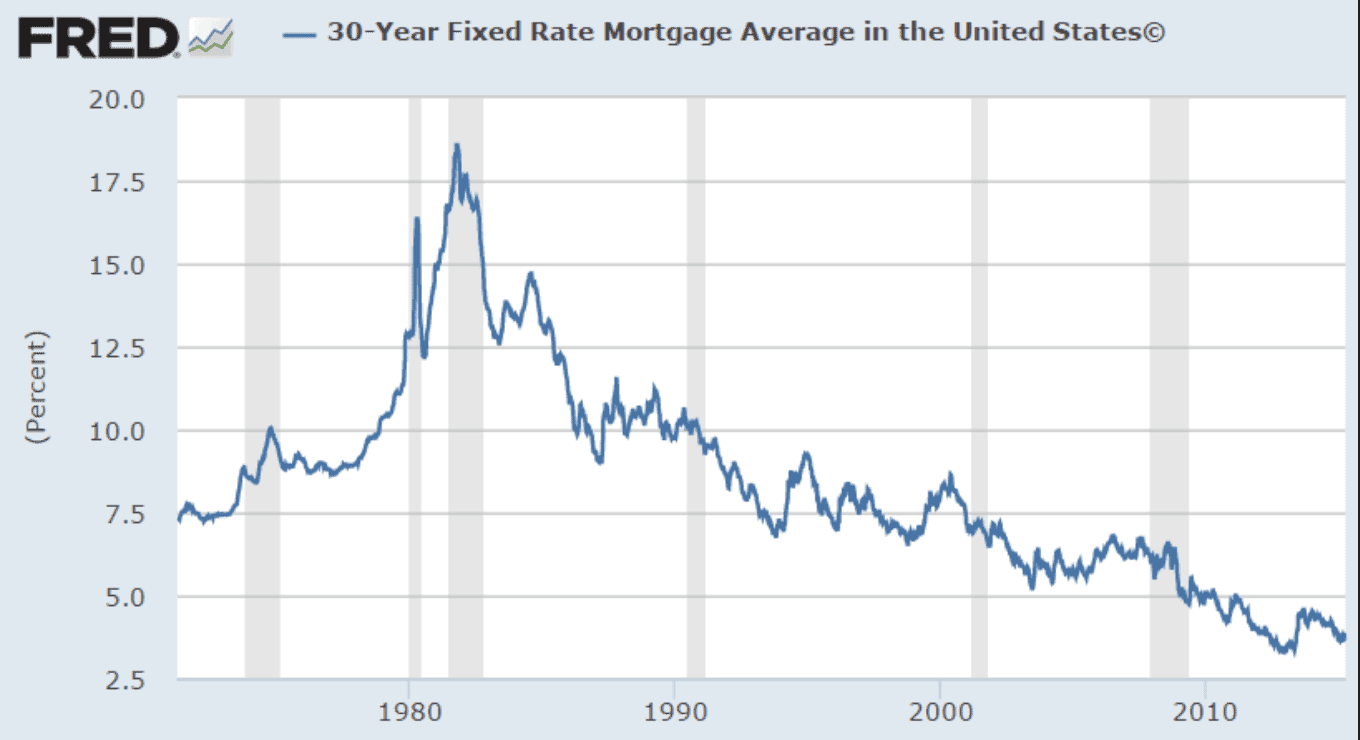

The Fed will most likely start cutting rates again but they've only got 225 basis points until they're at zero and 1600 until they get to 1980-81 highs.

In other words, there's a massive asymmetry in rates. See a chart of rates going back to 1971.

But even if the fed funds rate normalizes and goes back up to 6-7% over the next 10 years.

Where does that put mortgage rates? Maybe 10%ish?

So let's go to a mortgage calculator and look at the payments on your average 300k home.

At 30 year 4% and a 20% downpayment, the monthly payments would be approx $1430. At 7% the payments are $1880. At 10% payments are $2390.

So the question becomes if the monthly payments on the average home in the US increased by about $1000 a month or 70%, what would the effect most likely be on home prices?

To be clear, this thought experiment IS NOT meant to determine if prices are going higher or lower…it's only meant to answer the question are prices currently cheap or expensive on a historical basis.

Let's move on to one of the points made several times above that the housing market is NOTHING like it was in 2006.

The main arguments being we don't have as loose lending standards, no excessive growth in money supply, and low supply.

1. Loose lending.

The US had 0% Fed funds rate for 10 years.

Artificially lowering mortgage rates to 3%! Now at nose bleeds level of 4%.

How could one argue artificially lowering mortgage rates to 3% isn't “loose lending”?

You're putting borrowers in a home they can't afford unless the Fed is holding down the long end of the yield curve.

So what's the difference if the Fed is doing it or mortgage brokers are doing it?

The net result is the same, people in homes they couldn't afford with market rates, except when the Fed makes lending “loose,” it does it for the entire economy, not just housing…which is worse.

And let's not forget the entire 30-year fixed-rate mortgage is “loose lending.”

Nowhere on the planet would banks lend over 30 years at a fixed rate. Not to mention a 3% fixed rate.

That loan is guaranteed to lose money if inflation exceeds 3%.

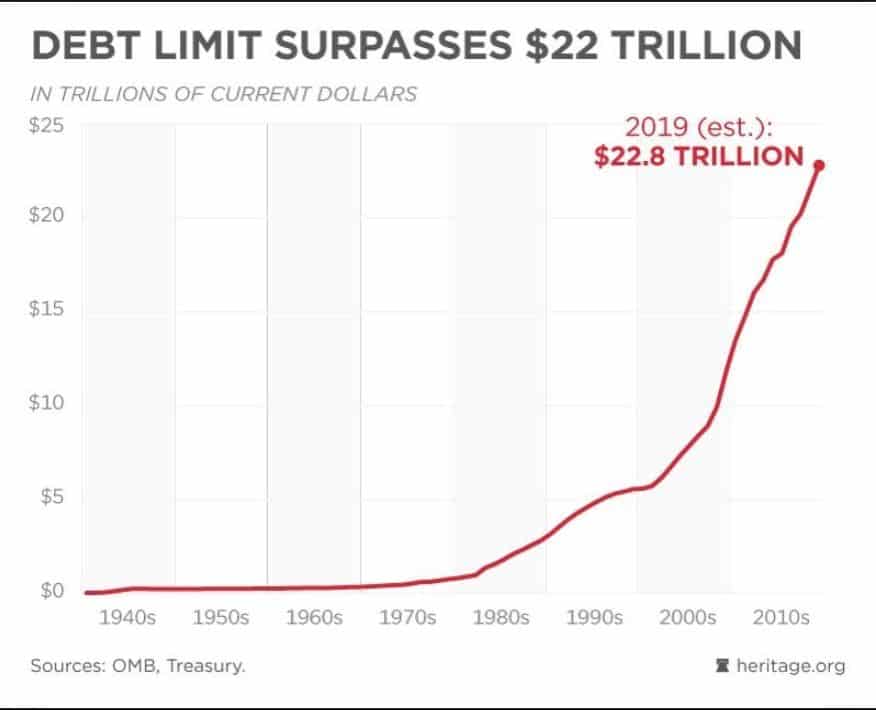

This while the government debt is 22 trillion (on the balance sheet) and the Fed's stated inflation target is a MINIMUM 2%.

Historically, what's the easiest way for governments to lower their debt load…inflate it away.

So banks are going to lend over 30 years at a 3% rate when the government has no choice but to create inflation? And let's not even dive into the growing popularity of MMT.

My point is, 30 year, fixed-rate mortgages would never exist in a free market.

When those go upside down the taxpayer will have to bail out Fannie and Freddie again.

If F&F aren't bailed out again the 30-year fixed-rate loan will be relegated to the history books.

What happens to housing prices then? And if we do bail them out, it increases our debt which puts upward pressure on rates. (it doesn't mean rates go up, just upward pressure.)

Because 10 years of ZIRP (zero percent interest rate policy) and a government fabricated loan, is specifically designed to make lending loose, putting people in homes they can't afford, without government intervention…precisely what caused the first housing bubble.

2. Money supply.

Money supply has doubled since 2008.

It took us 216 years for the money supply to reach 7 trillion, and a whopping 10 years for the money supply to double to 14 trillion. See the chart. I rest my case.

3. Low supply.

Commodity traders have a saying…” high prices cure high prices, and low prices cure low prices.”

In other words, the higher the housing prices go, the greater chance of additional supply hitting the market.

Do you want to bet on prices going higher because of short supply, when prices going higher is a catalyst to more supply coming online?

AGAIN, this is not to say we're in a bubble, or that prices are going down, remember, those are the wrong questions to answer.

It's simply to say, the market is closer to expensive than cheap.

If you've read this far, thank you, I saved the best for last.

Nothing has made me more money in biz or investing than understanding the game of blackjack.

Making the smart move is based not on whether you win or lose a hand, but if you played the hand correctly based on probabilities.

Most investors do the opposite, but the very best investors apply this concept religiously.

Make the move with the highest probability of winning, every hand, and you'll beat the dealer in the long run.

Make a different move, and although you very well may win the hand, in the long run, you'll go bust.

As I stated many times, when considering a real estate purchase ask yourself is it cheap or expensive? Or in terms of blackjack are you doubling down on an 11 or are you hitting on a 19?

Just like buying a property in Denver right now could make you a lot of money, hitting on a 19 could get you a blackjack… 😉

George.