If you thought Bitcoin could solve all of our problems, think again. In this article, I will explain how full reserve, free, and central banking work and why going back to the gold standard wouldn’t make a significant difference.

Full Reserve Banking: Ciao Government

I will explain why gold and Bitcoin don't matter. To do so, you first need to understand full reserve banking because this is where it all started.

With full reserve banking, there is no government involvement, there are no central banks, no fractional reserve banking, or new money created by the banking system.

This is how it began: There was an average Joe who had three pieces of gold. So he went and gave his gold to the goldsmith, which I will call the bank. But it doesn't mean it can only be a bank, it can be any fiduciary, bank, investor, or fund.

As I break down how it works you will see, whether it's gold coins or Bitcoins, the process is still the same.

Once Joe gave the gold coins, they became an asset of the fiduciary, but they went into two separate categories.

One coin is a demand deposit, which means Joe can come in and grab his coin at any time. The other two are a time deposit.

Joe has an agreement with XYZ entity that in two years, five years, or 10 years, he'll be able to collect the money he gave in the first place. In addition to that, a set amount of interest or return.

On the other hand, we have everybody’s favorite character, Moody the millennial. He needs two gold coins to go to the next Antifa rally.

So he goes to the fiduciary and says, “Fiduciary, I need a loan”, and they say, “Okay, you're a good credit risk, Moody. You have a job driving Uber, and in Starbucks. We think you can pay us back.”

Two of Joe’s gold coins go to Moody so he can go to the next Antifa rally and riot himself as any good millennial would right now, and Moody takes the two gold coins and buys a ticket to Portland or Oregon and hops on the next flight.

In this case, I want to point out is that the interest rate is completely set by supply-demand. It's market-driven.

As demand for loans goes up, so does the interest rate because there is less supply of money to be lent.

Therefore, it encourages people to save more money and put it into the bank, lowering the interest rate and bringing it down to equilibrium.

On the flip side…

If the demand for loans goes down, so does the interest rate. This discourages savings and increases spending.

One could argue more people are going to be starting businesses, therefore, there will be more demand for loans, and that goes up. Then, it all becomes just a balancing act, and everything works extremely well.

To give a little more insight on full reserve banking, here's an extract of one of my favorite economists, Bob Murphy.

“There are two distinct functions:

-

Function #1

The first one is that banks could have demand deposits that they're offering to customers. And so that term demand means your money can be returned to you upon demand.

That's what it means. And the point of that would be for convenience or safety, right?

Let's say you have $10,000 in currency. That's risky just to keep on your person or even in your house in a safe. There could be a fire, somebody could break-in.

So that's one function that the bank serves for the community, they have much more secure vaults, they have insurance, they have armed guards and blah, blah, blah.

And so you can go ahead and put your money there. It's just a safer place to keep it. And then there's also the convenience that they have an ATM network around the world.

They have agreements with restaurants and whatever merchants. And so just with your bank card, you can either go to an ATM and get cash all over the place, or you can just be somewhere and swipe your card, right?

So it's just an easy way to keep track of where your money is being held in your name so you can spend it in a very convenient fashion. Okay.

-

Function #2:

The other distinct conceptual function is time deposits for credit intermediation, right? So banks do also act as credit intermediaries and think of this as a savings account or a certificate of deposit, a CD. That's what that stands for. If you've heard of banks selling CDs with associated interest rates or yields.

So here you might go to the bank, you have $1,000 that you want to lend out and earn interest on. So you go to the bank and buy a $1,000 CD. What that says is the bank's promising you.

I'm just making these numbers up, but they'll say: In 12 months, the bearer of this note, this CD redeems it and gets $1,050, okay? So there's the implied 5% interest rate on that for the one year loan, and then they take the $1,000 and they go lend it to somebody else, presumably for more than 5% a year.

So there's where the bank's earning the spread and that's where the bank is connecting the savers and the borrowers.”

(End of Transcript)

One of the key takeaways and a misconception of full reserve banking is they don't store all the money in the vault, and you can't just come to access it for a fee at any time.

They do lend out the money, but they create time deposits. Therefore, they are not creating any additional money supply.

In the average Joe example, it started with three coins that went to the bank. Two of those coins went out, and Moody now has them on their balance sheet.

There are still three coins in the system: One on-demand deposit for Joe, and two with Moody, the millennial. No additional currency units have been created, but there was an actual loan.

As I stated earlier, this system works rather great when you take into account global trade. This is something that David Hume referred to as price-specie. It seems a little weird, but I will examine his approach, The Price-Specie-Flow Doctrine, back in the time of Adam Smith.

It was a counter-argument to mercantilism. In essence, it is a trade surplus possible only in the short run. The inflow of gold or other forms of wealth, like Bitcoin, would lead to an increase in the price of domestic goods.

Higher prices for domestic goods would eventually lead to an increase in imports and a decrease in exports. This would reverse the process and bring prices down again.

There would be bouts of inflation and deflation, and I'm defining that by the money supply increasing or decreasing, and the price of goods and services increasing or decreasing as well. But over the long run, the prices would be relatively stable.

The way that price-specie works is pretty simple. It is comparable to the U.S and Europe. They are trading back and forth with one another throughout the year. At the end of it, they settle up with their gold pieces or their Bitcoin.

In this case, let's consider Europe sells more goods to the United States. So, Europe has a trade surplus, more gold coins or more Bitcoin will go to them. In this scenario more equals 100. The 100 coins go to Europe, which increases their money supply.

If the money supply increases and there are no central banks involved, there will be no quantitative easing, there will be more currency units, more gold pieces, or more Bitcoin chasing after the same amount of goods and services. Therefore, prices in addition to the money supply will increase.

I would like to highlight that even if we are using gold or Bitcoin as money, we still would see potential price inflation and an increase in the money supply in a domestic economy if we're trading back and forth from country to country.

The same thing occurred when we had the gold standard.

Now, what happens next?

If the prices go up in Europe, it makes their exports less attractive, and it makes the imports coming in from the United States more attractive because they are cheaper relative to the money being used, in this case, gold or Bitcoin.

As a result, the goods in the United States get more attractive. They become cheaper, so more goods are being sold in Europe, the next year for this example.

If more goods are being sold in Europe when they settle up, then those 100 gold pieces on net or 100 Bitcoin are going to go back to the United States. This increases the money supply, increasing prices, and we go back and forth. We would have inflation and the very next years, deflation.

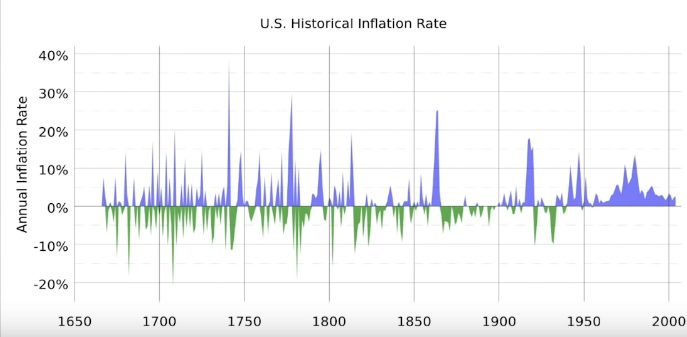

Here we have an image of a chart displaying the U.S. historical inflation rate back in time. You can notice it looked like a heartbeat, as far as inflation-deflation, it went up and down. Over the span, it didn’t change much.

Prices gradually went down as they should with an economy functioning properly, creating more goods and services cheaper and more efficiently. This system was a great example of the free market solving very complex problems extremely well.

No government and no central banks involved in the United States. Some other countries did have central banks, but I won't get too deep into the weeds.

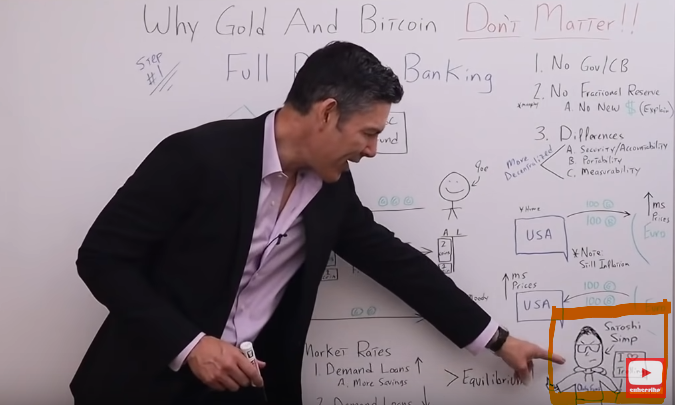

Now you may be asking yourself, “George…Who is this guy down here? Is that the MMT troll guy?”

It isn't, but it is the MMT troll Bitcoin worshiping cousin. I want to introduce you to Satoshi the simp.

He has a sign that says I love trolling (boy, does he ever!). I'm not quite sure what a simp is, but I almost guarantee the Bitcoin troll guys do. Of course, he has his hoodie on and he's pissed off.

He has given Moody the bird, and they are giving him the bird. Also, he is very proud of his Onlyfans hoodie. He steps in and says, “George, wow. You don't understand what's going on. You're comparing Bitcoin to gold. That is crazy talk.” And it is true.

There are some significant differences, but my point is whether you use gold, Bitcoin seashells, or oil, it doesn't matter. If you have an asset and give it to a fiduciary in a full reserve banking system, this is how the process works, as shown below:

Also, the price to specie model would work the same, regardless of what you're using as the underlying asset.

What are the differences?

- Safer: With Bitcoin, it is more secure. Therefore, with the fiduciaries, they would be held more accountable. You'd be able to tell exactly what they were doing, when, and how much they kept on reserve.

- Decentralized: You could hold Jamie Dimon's feet to the fire as might be. Bitcoin is more portable and this would lead to a more decentralized system because fewer people would need to deposit their asset, in this case, Bitcoin, into the overall system.

I think the takeaway is it would lead more people to keep their Bitcoin in their possession, and the system would be more decentralized.

There would be decentralized lending, maybe peer to peer. But I do think at the end of the day, a lot of those people holding the Bitcoin would give their Bitcoin to an investor or fund to get a return because they just don't have time to do the due diligence on lending to people like Moody, corporations or small to midsize businesses.

To be clear, I think the functionality Bitcoin has that would create a more decentralized system, has significant benefits.

Free Banking: Probably Not What You Have In Mind

Most people think free banking is when they can go down to the local Wells Fargo or B of A and not get charged for a checking account. Indeed, it is what full reserve banking evolved into overtime.

We had a system like this in the United States from 1792, the Coinage Act, through the Civil War. It is where the banks themselves created their currency without the government and the Federal Reserve.

You would take your gold coins down to the local bank and they would give you green, purple, orange, who knows what type of piece of paper, and it would be a currency unit backed up by the bank.

It is the bank giving you a receipt saying that you can come back and redeem that receipt for your gold and it's transferable from bank to bank and person to person.

You can call that: Fractional reserve banking, and is just like what full banking was at the beginning: A creation of the free market. In this case, though, it's fractional reserve banking without the government and the Fed. Just in the private sector.

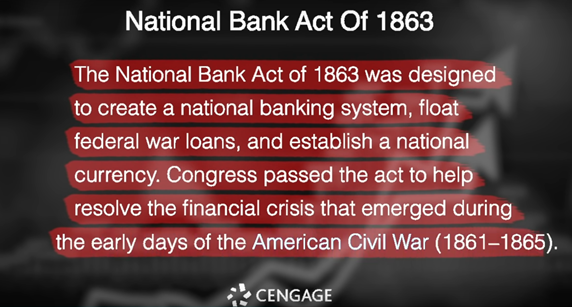

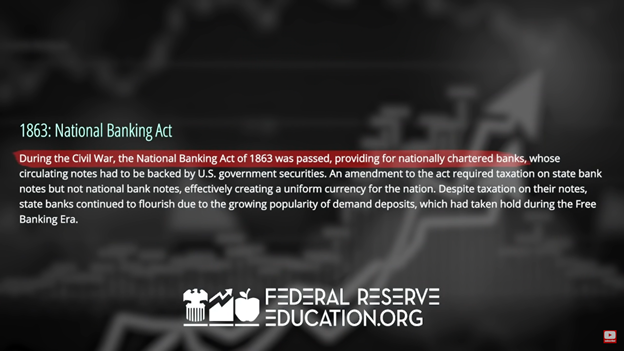

One key I want to emphasize is why this system ended. For that, check out this abstract from the National Bank Act of 1863.

The point I want to underline is the private sector was doing a great job of creating money and currency. Then the government came in and ended it all as a result of going to war. The war took priority over the system, the free market, and the private sector.

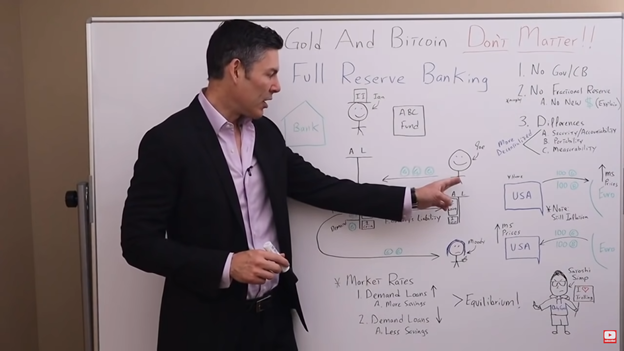

I want to make a parallel between free banking and full reserve banking. Same as in my first example, Joe has his three gold coins, or again, they could be Bitcoin, it doesn't matter.

He gives them to the fiduciary, and I know you say, “George, they probably wouldn't give the gold coins to investor Ian.”

But if you had Bitcoin and you had the flexibility of that security knowing at all times who owns it, you would have no problem giving those Bitcoin to investor Ian, ABC fund, or maybe even lending them out yourself.

For this example let's just use gold coins. They went over to the balance sheet, just like they did with full reserve banking, but now they are demand deposits. Where before, some of them were time deposits.

So Joe can access his three coins at any time and the bank will lend two of those gold points out to Moody the millennial as they did before so he can go to his Antifa rally.

The two gold coins, for the moment, go to Moody's balance sheet, but on Joe's balance sheet, there are also three gold coins.

Moody has two gold coins that he would deposit with his bank, and there would be liabilities for the bank, but deposits for Moody.

What happened is the system has five coins in total, but it only started with three. They added two additional coins. This is the main difference between full reserve banking and free banking.

Free banking is a fractional reserve to where it can expand the money supply. To make it easier to grasp, l want to go over this extract of one of my favorite economists, Bob Murphy.

“The distinction is the Rothbarbadians, who are for 100% reserve banking, versus the so-called free bankers who many of them call themselves Austrians, is they say is, “Hey, we're not central planners. We don't want the government to regulate it. Let banks choose whatever reserve ratio they want. Okay?”

So they got to follow their contracts. If they say to their customers: Hey, whenever you show up and you want to pull money out of your checking account, we'll be able to give it to you.

And if there's a bank run and they get caught with their pants down, then okay, they should get in legal trouble just like any entity, or any firm in the economy that doesn't live up to its contractual obligations, it has consequences.

But we're not going to at the outset have some regulation on the banking sector saying you have to have 100% reserves, right?

So that's their position. So that's why they call themselves: Hey, we're free bankers. We're not going to micromanage the banks and have them set their particular policies, just like…

How much did they charge for a checking account? Or what should the rate of interest they pay on deposits be? We're not going to tell them that. We're a free-market, laissez-faire people. So who are we to tell them what reserve ratio to hold?”

(End of transcript)

To be very clear, this form of fractional reserve banking, although it has no government involvement, no central bank involvement, would increase the money supply regardless of whether Bitcoin or gold was being deposited into the bank.

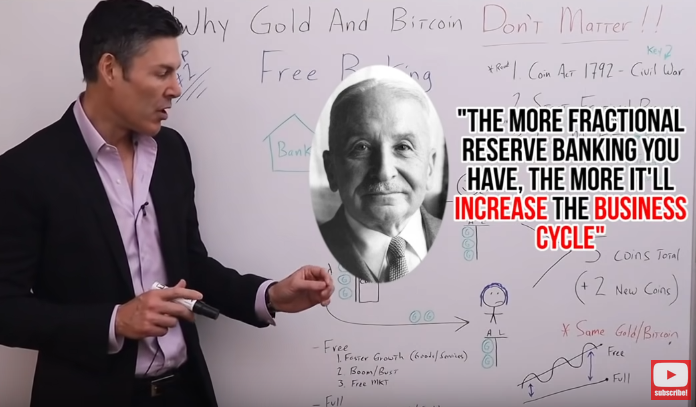

As fractional reserve banking was a creation of the free market, the Austrians go back and forth as to which they prefer. With free banking, since you can match up to demand or productive loans with the supply of money or the supply of those loans, they argue that growth can happen more efficiently and quicker, but there will be a slight boom and bust cycle. This is what Ludwig von Mises -Austrian School Economist- would always argue.

He liked the concept of free banking because it was free of government involvement, but he said:

So there are those favoring the argument that over time we're going to have slightly higher growth, but the cost is going to be the misallocation of resources and the boom and bust cycle that we referred to.

Another argument would be for full reserve banking, where it grows over time due to the productivity of the individuals creating goods and services in the real economy, a little bit slower growth, but it's far more stable.

Those who favor this type of full reserve banking would argue it doesn't miss allocate resources. Therefore, over time you would see greater growth. But the debate goes back and forth. There are good arguments on both sides.

To reiterate:

- Free banking creates potentially faster growth of goods and services, not just the credit supply or the money supply, which means growth in the actual wealth of the economy and the standard of living. However, it lends itself to a boom-bust cycle, generated by the free market. This is not something that the government thrust upon us.

- The full reserve would have slower growth, but maybe more stable. No boom and bust cycle, no misallocation of resources, which some would argue would lead to higher growth long-term.

- Another benefit to full reserve banking is it wouldn't distort the price-specie flow model we discussed from David Hume.

- Within the limits of fractional reserve banking, with those currencies, gold or with the money going back and forth from country to country, if the banking system could increase the money supply, it could distort the equilibrium.

Regardless of whether you're using gold or Bitcoin, the system of free banking and fractional reserve banking would be almost identical.

Central Banking: Everybody's Favorite

I'm being pretty sarcastic here. We started with a full reserve system and then went on to free banking (we got fractional reserve banking as a result of the free market).

Later we nationalized the banking system due to the Civil War. The next step for the United States was central banking in 1913. When I pointed out the IOUs, what I was referring to is the banking system creating a new currency.

The banks were keeping the gold coins and issuing currency, or IOUs, to the average Joe. I want to clarify those were the gold coins (IOUs from the bank) on Joe’s and Moody's balance sheet.

The first step of the process is very much the same. Joe gives his gold coins to the bank, but then what happens is the bank gives the gold coins to the central bank.

So they're now assets on the central banks’ balance sheet. The central bank issues IOUs for those gold coins back to the bank where Joe deposited his coins in the first place.

The bank gives Joe the IOUs for the coins, those are liabilities on the bank's balance sheet, and the IOUs from the Fed are now assets on the bank's balance sheets.

What the bank gives Joe are three IOUs for IOUs. Here is when you comprehend how insane this system is. The bank lends out IOUs to Moody that they later put onto their balance sheet.

We have increased the currency supply. It started with three gold coins, that turned into five IOUs through the process of central banking.

To summarize: Joe gives his coins to the bank. The bank gives those coins to the central bank. They issue IOUs against the gold coins, which become assets on the bank's balance sheet, also liabilities.

The bank is telling Joe, “We owe you three IOUs that we received from the Fed so you can take those out in the real economy and spend those much easier than you could spend the three gold coins you gave us.”

Without any doubt, that's what they lend to Moody. That goes on to their balance sheet, and all the IOUs are going back and forth where we originally had gold pieces.

I also want to point out that this is the way that old-school fractional reserve banking works. It's a little bit different now in the modern age, but for this matter, it is just important you understand this concept.

We went from full reserve to free banking and fractional reserve banking as a result of the free market just doing its job. But we had the Civil War, then the government came in and nationalized the whole process.

We had central banking coming in 1913 because we wanted a system that was “safer”. Then, in 1944, we had Bretton Woods, which was a top-down government type of solution.

As a result of Bretton Woods, the Eurodollar system evolved to solve the problem of scarcity. There weren’t enough dollars outside of the United States to facilitate maximum global growth. This was done while we were on a gold standard.

Is going back to a gold standard the solution for all the problems we have today?

It might be a short-term solution, it might be able to solve it for 10 or 20 years, but in the next 100 years…

Don't you think we'd probably be right back in the same spot?

As an example of this, I want to go over a fantastic article from Philosophical Economics titled “How Money and Banking Work On a Gold Standard”. It illustrates very well what I am referring to.

The article does a great job of describing the systems and how they evolved. After reading it you will be able to tell this guy is not Austrian.

The reason not to use monetary systems based on gold is that they're obsolete and unnecessary with no real benefit over fiat systems, but with many inconveniences and disadvantages. In a fiat system, the central bank can create base money in whatever amount would be economically appropriate to create. But on a base gold-based system, the central bank is forced to create whatever amount of base money the mining industry can mine, and destroy whatever amount of base money a panicky public wants to destroy. There's no reason to accept the system that imposes those constraints even if they aren't much of a threat in the majority of economic environments. If the goal is to constrain the central bank, then constrain it directly with laws.

So what the author is saying is if we're worried about the central bank going crazy, we should just set up laws to prevent them from doing stupid things that are going to destroy the economy.

We should prevent them from being the arsonist, and we should just make sure they're the firefighter, but that's what the Federal Reserve Act is supposed to do.

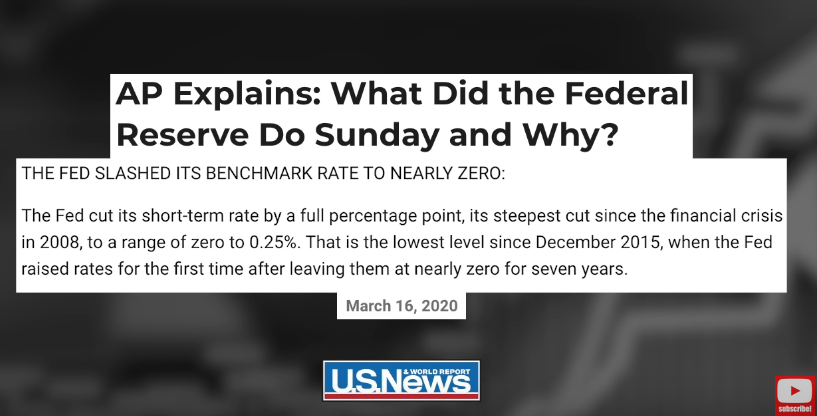

Let's rewind to March 2020 of this year.

How many teeth did the Federal Reserve Act have?

Zero. The Fed completely ignored it.

-

Are they allowed to buy corporate debt?

-

Are they allowed to buy junk bonds?

-

Are they allowed to set up these special purpose vehicles?

No, but they did it anyway regardless of the law. Why? Because they're human beings and we had a catastrophe. We had fear in the markets and we were saying, “Fed do whatever you need to do to make sure we are safe.”

So right about now, all the Bitcoin people are probably screaming, “George Bitcoins solves all of those problems.”

But does Bitcoin truly solves it all?

I understand that Bitcoin is decentralized and we would have a lot less government power if any government or central banks at all. But, let’s try to figure it out. Picture this example.

Covid-19 has just started, and the only form of money we have is Bitcoin, meaning we don't have fractional reserve banking, but we have a virus that no one could have foreseen.

Everyone starts to panic and hoarding their Bitcoins. So there is no lending, even in a full reserve decentralized system and everything starts to collapse. So you can see what would happen.

The people would go to the streets and say, “We need fractional reserve lending. We can't be so strict on these rules that we can't issue currency or pieces of paper against our Bitcoin. This is a national disaster. We have to take emergency action.”

You could see the same thing happen if we went to war or had a national disaster. I want to refer to a quote from one of the OGs of Bitcoin, Hal Finney.

Finney saw Bitcoin as being a substitute for gold, not really money itself, but it would be used as a reserve asset to issue currency against.

Very similar to what we saw with the free banking and fractional reserve system we had before the civil war. Again, once you have a war or a national disaster, everything seems to change.

My whole point with this article is not to claim that gold and Bitcoin don't matter at all, but it is to say that at the end of the day, human nature and the fact that we are imperfect creatures, living in an imperfect world matters even more.