What to do if you’re thinking about buying or selling a house?

With all of today’s situations, unemployment skyrocketing, Fed’s interventions, government bailouts, the thread of inflation, and the possibility of a recession, how can someone know what to do if they’re currently in the real estate market?

There are special considerations you need to make so you won’t lose a fortune!

In this article, I’ll help you understand in what type of real estate market you live in, and if you should buy, sell, or wait.

This information is especially geared towards homeowners.

Types of Real estate markets

There are three main types of markets in the United States, and around the world: the cyclical market, the linear market, and something in between, the hybrid market.

I’ll explain the three of them so you can have the certainty of in what type of market you live in or in what type of market you’re considering buying or selling.

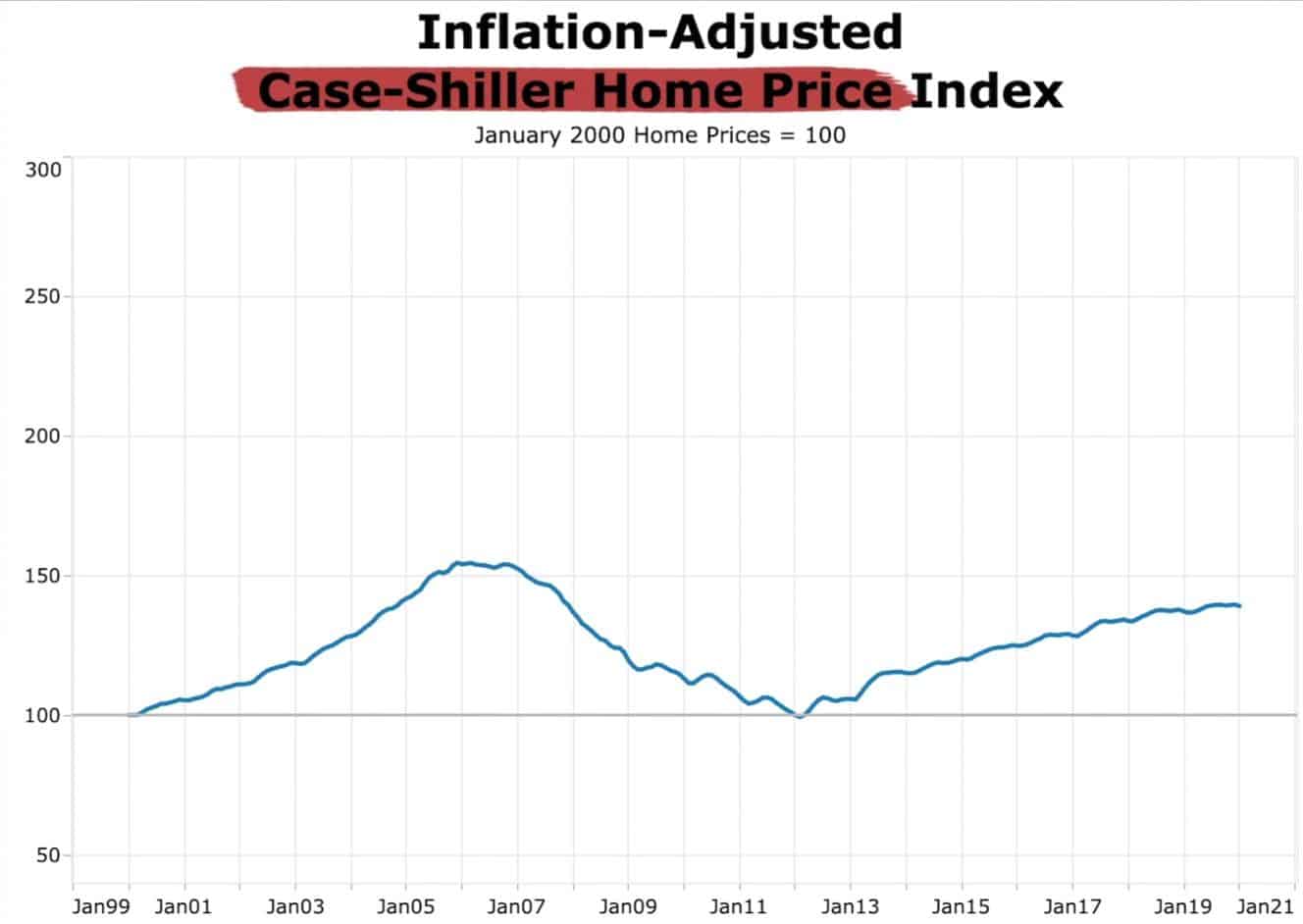

But first, let’s analyze a chart of the U.S. home prices adjusted for inflation.

This chart goes back to 1999, and for this example, we don’t have to draw upon other graphs going back to the 1900s or late 1800s, like I typically do, because of the historic trendline bottoms out right around 1999.

Keep in mind this is an index chart, so the numbers on the left don't necessarily imply the home prices.

The graph starts with the 2006 peak when it went up to 160 or so, and then came crashing down to 2012, and then back up, almost to where we were in 2006.

There’s a small Delta or gap if you look at U.S. home prices as a whole, but if you look at individual markets, some markets are even higher, the same or lower.

I’ll explain each one of them so you can determine which of the three markets you live in.

The cyclical market is one that goes way up in a boom and comes crashing down in a bust, the linear market generally stays the same, kind of boring, and the hybrid market is right in between those two.

As I said, this article is geared towards the homeowners, which means we’re talking about the home where you and you’re family live in, I'm not speaking about a rental property or a flip.

To determine in which market you’re in, I’ll give you various examples.

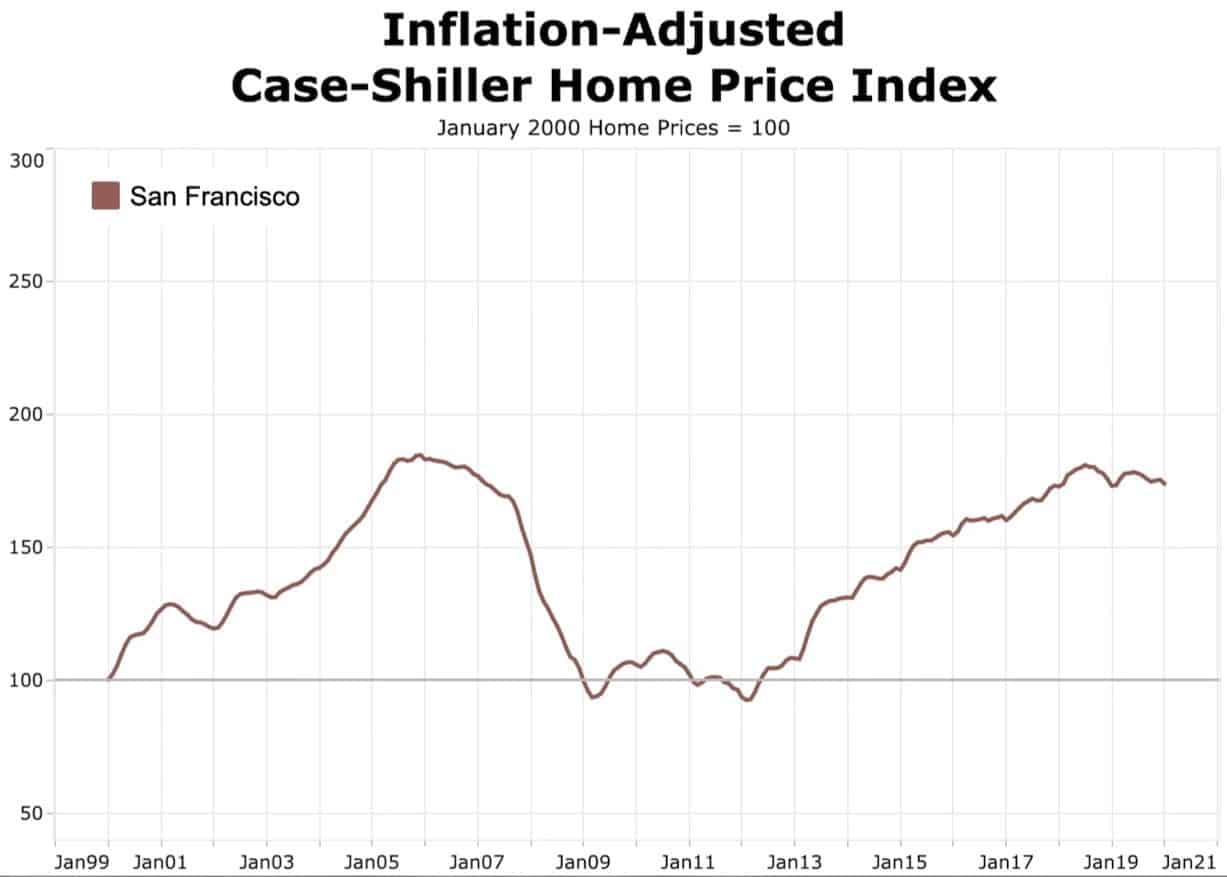

Here’s the same chart we used before, adjusted for inflation index, but for San Francisco, which is a cyclical market.

As you can see the market went 83% up in 2006, higher than where it started, and of course, it came crashing down. After this, it started to go up again until today, when prices are almost as high as they were in 2006.

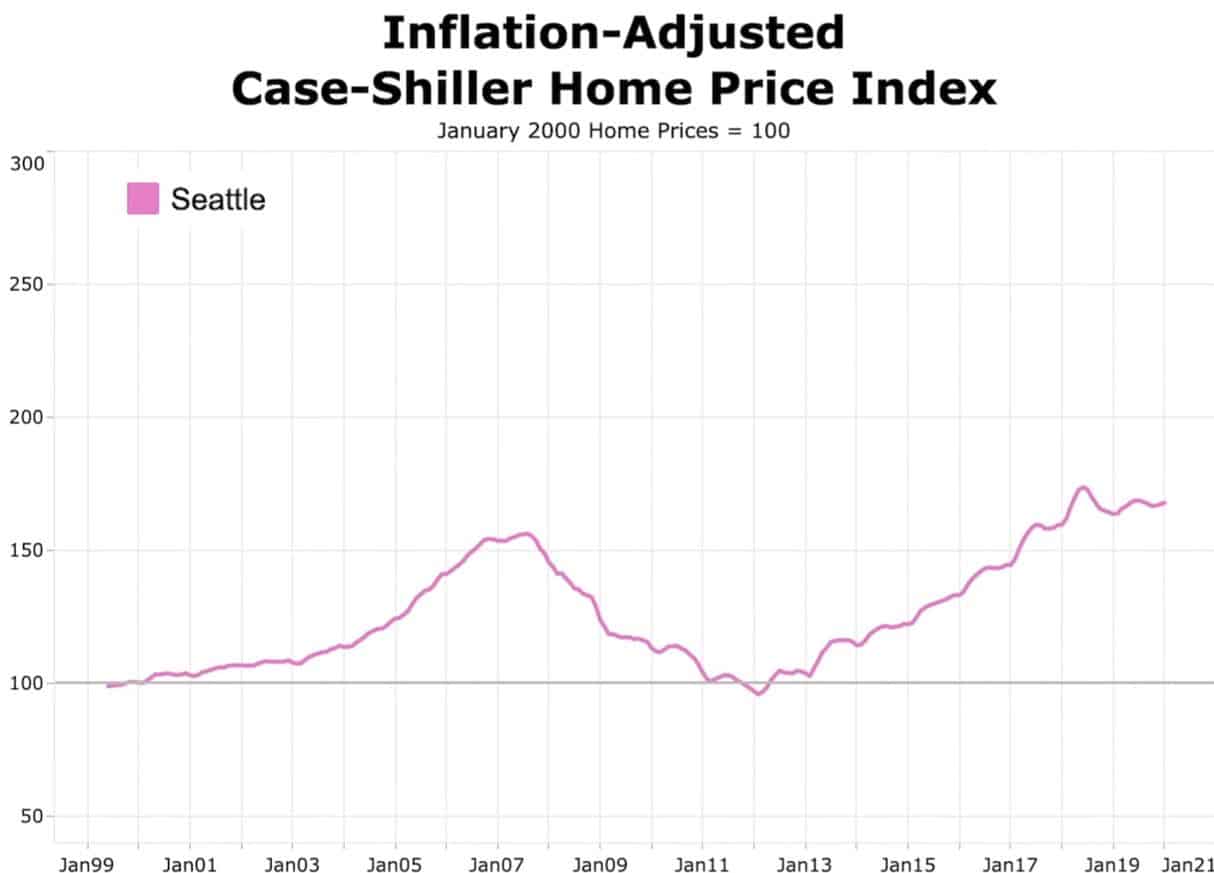

Seattle is another example of a cyclical market that’s even higher than it was in 2006.

Back in 2006, the price index went to 155 but now is close to 170.

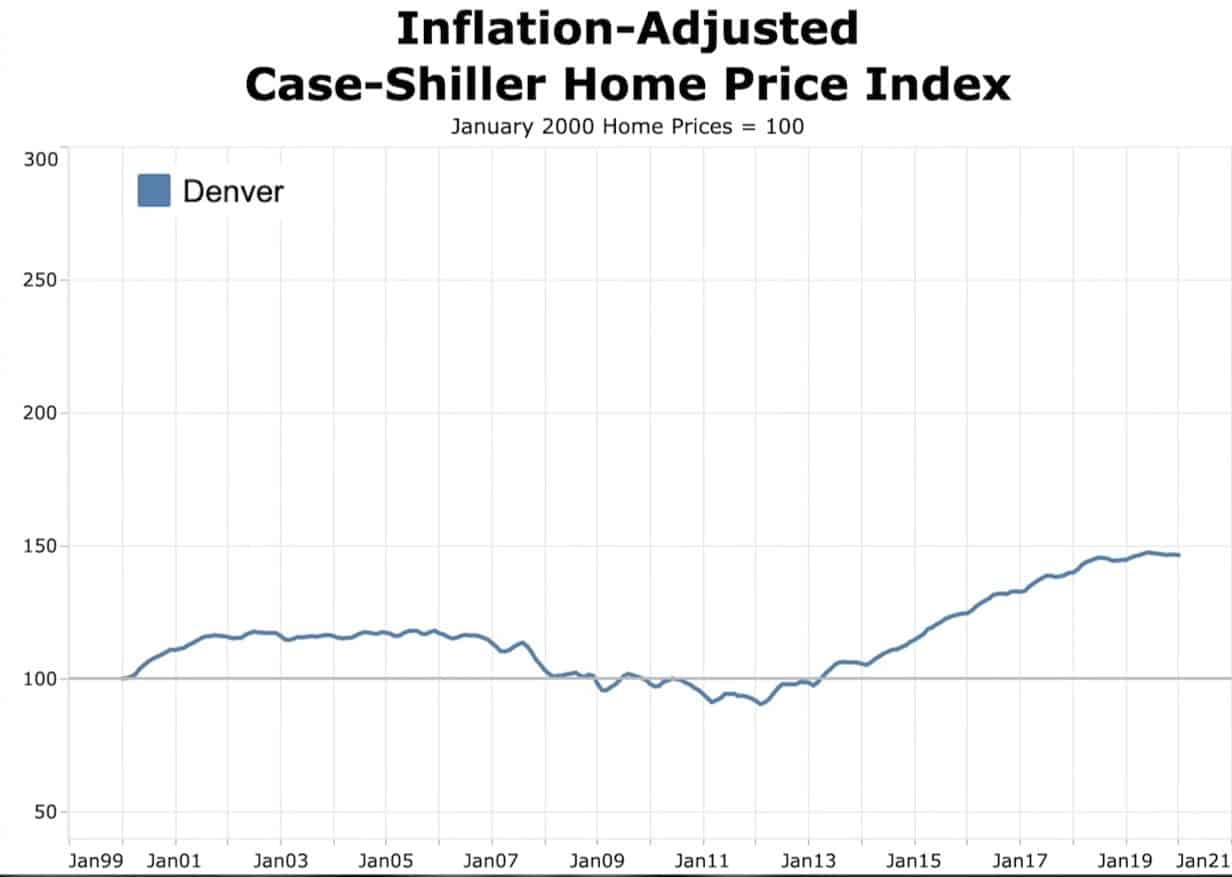

Denver is one more case of a place that used to be a hybrid market where prices would go up a little and then started to go down, but since so many people have been moving there, prices have been going up dramatically since their low in 2012.

So now, Denver might even be considered a cyclical market.

The big problem with these markets is as they go up everything is fantastic, but when the market starts to turn, there’s a big Delta between the current price and where the price will most likely bottom out.

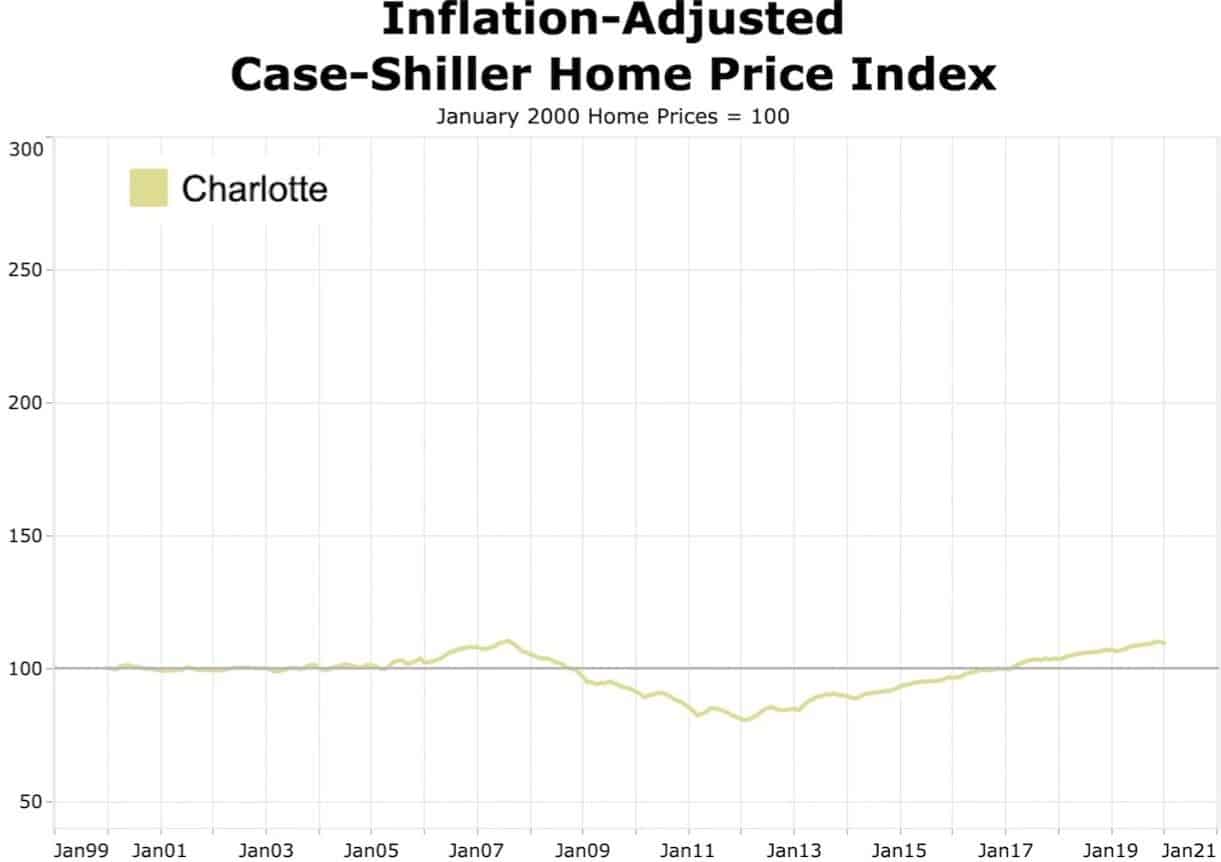

Here’s another example, this time, for a linear market: Charlotte.

Charlotte is the perfect example of consistency, it looks like the prices barely move, compared to the cyclical markets.

It went up to 108, then down to 80, and right back to its historic norm in January 2017, however, since then it’s gone up a little.

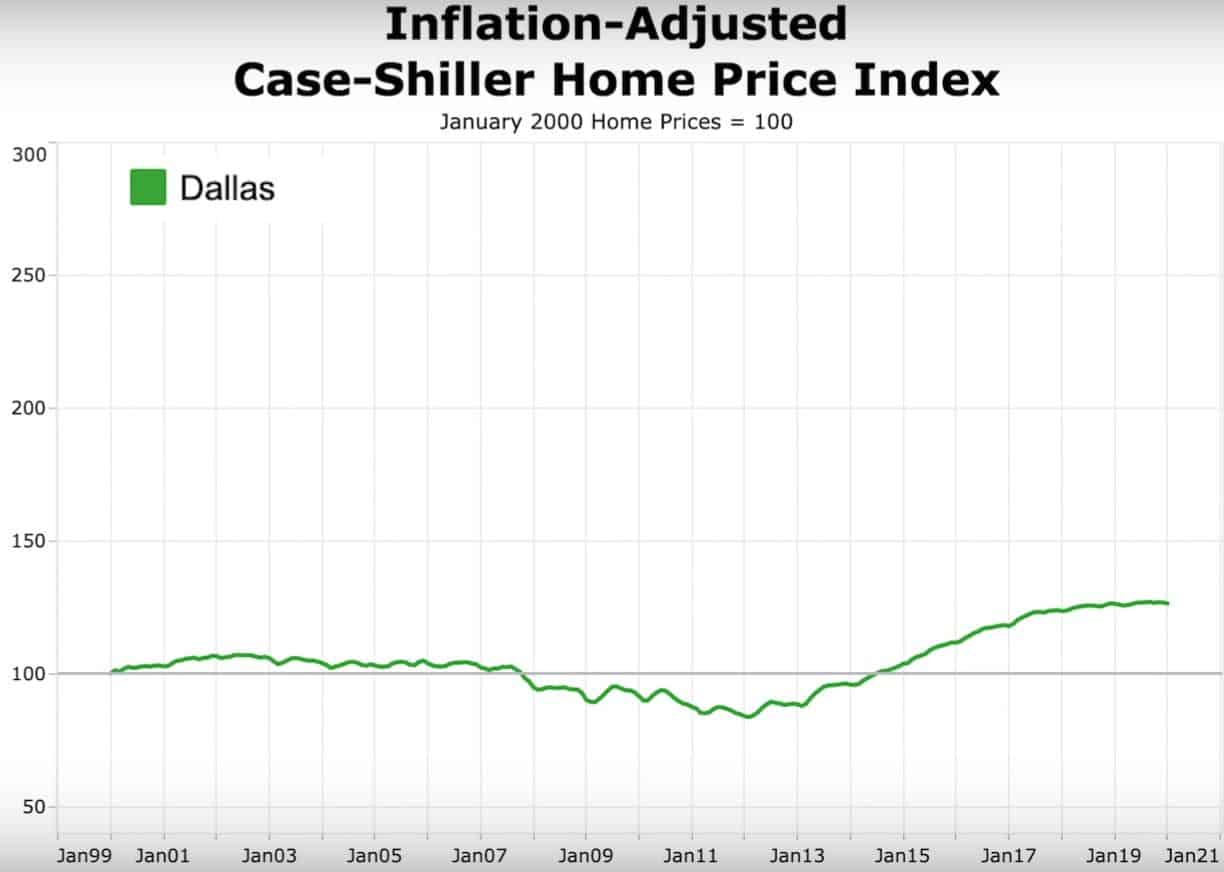

Dallas is also very consistent, which means its another linear market.

This market stays mostly the same, but a lot of people are moving there too so it’s been going up.

The prices have flattened out because although they had an increase in population and growth, due to businesses moving there from higher-tax states, they have very relaxed building codes.

So it’s easy for builders to create more supply to meet the additional demand.

This doesn’t allow flattened prices to go skyrocketing to the moon as we see in California or some places on the east or west coast.

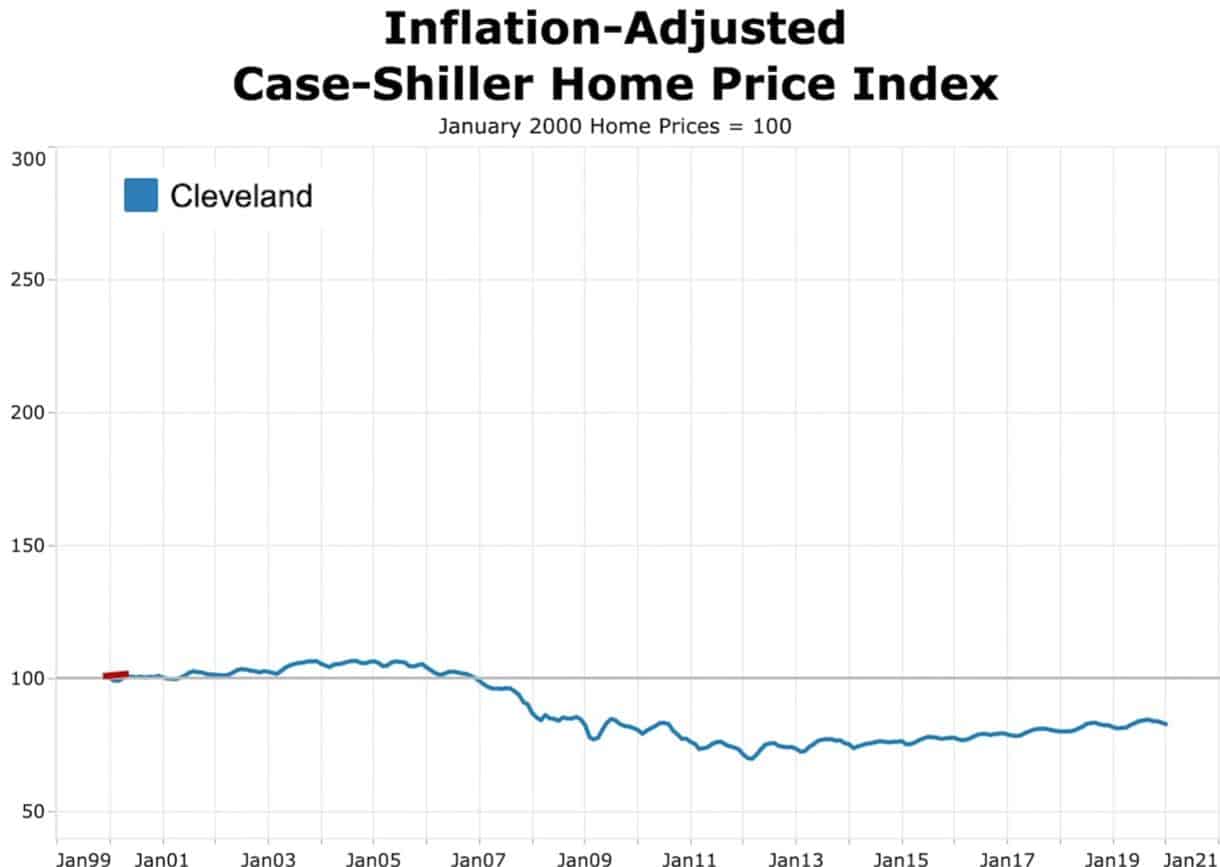

Cleveland is another linear market for sure.

It came down and stayed flat, however, it’s on a slightly upward trend so it’ll probably get back to its historic norm for five or ten years.

There aren’t a lot of price movements there, which means we’re definitely not going to see huge appreciation in a market like Cleveland.

I hope all of these examples help you identify which market you live in because that's our starting point to make a decision of buying, selling or waiting.

Next, I will explain what is it that you need to know in order to determine if you should sell or wait.

During a housing bubble should we sell or wait?

If you thought about selling your house prior to the Covid-19 and now you're not sure what to do, this is for you.

And to answer our question we need to analyze the U.S housing prices.

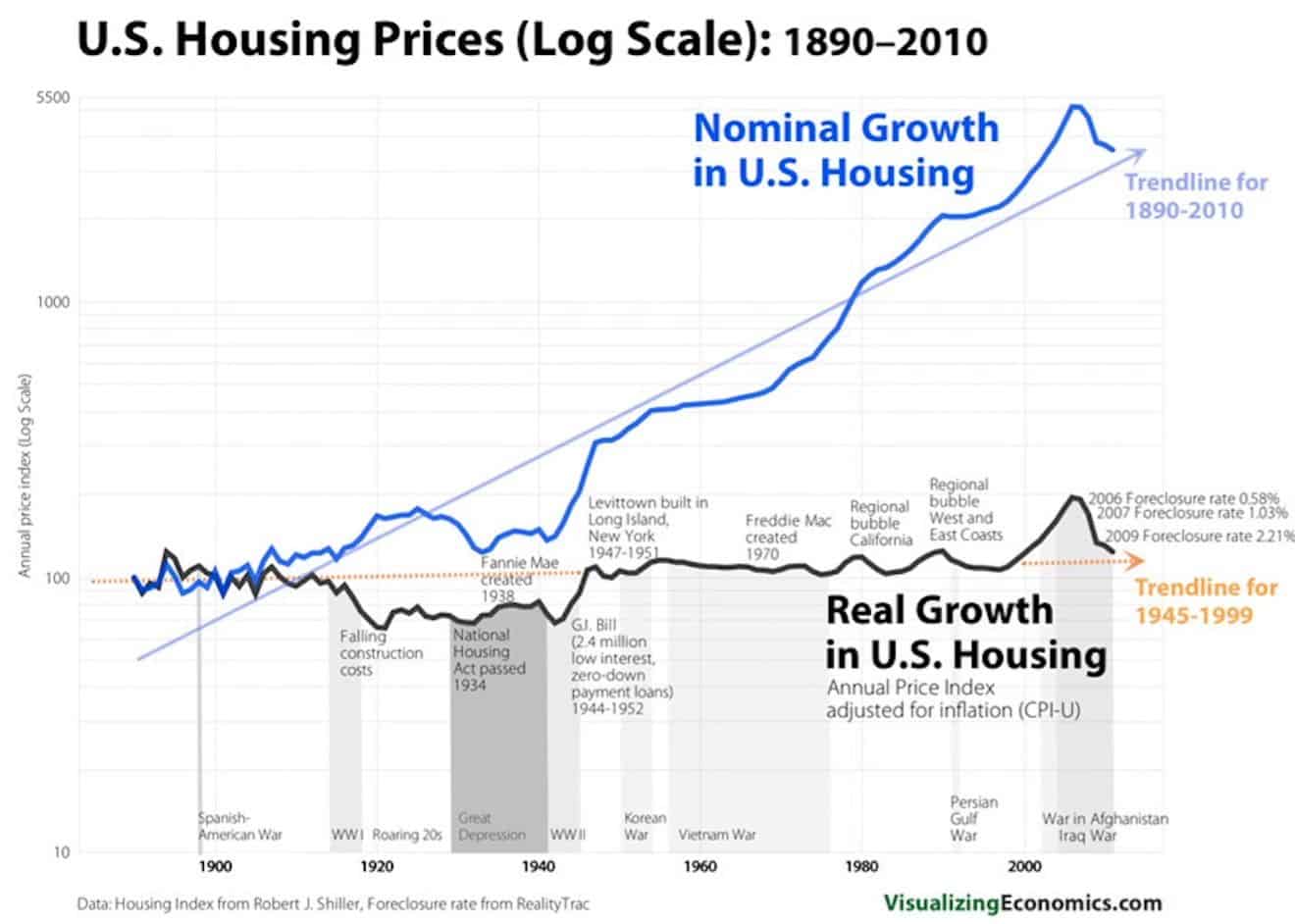

This chart goes from the 1900s to today and displays the U.S. housing prices adjusted for inflation in contrast with the nominal home prices.

There’s a big difference between them, which is why I often tell people, when they’re looking at real estate, to look for inflation-adjusted prices.

Most of the Youtube gurus who talk about real estate investing, usually just use nominal charts to show that“real estate is always going up in price over time.”

But when we look at the inflation-adjusted prices, we see home prices don’t appreciate over time, they really just inflate.

In other words, they go up with the rate of inflation.

Yet, I know many might be thinking about the 1970s rise of home prices and the lending standards, but I'll get into it and explain it.

1. The 1970s home prices

At that time, home prices went up dramatically, yes, in nominal terms, but adjusted for inflation, they really only went up in the late stages of the 1970s, and that’s starting from a base of a historic norm, today, we’re starting at a base of an all-time high.

There’s a big difference between starting at a very low and starting at a high point. I always say its better to buy low and sell high instead of buying high to sell higher.

2. The lending standards

People also say lending standards are much better now, but please! Think this through. In 2004-2005 they were giving loans away to anybody that could fog a mirror.

However, many still believe the lending standards are very strict and don’t see a downside to the housing market.

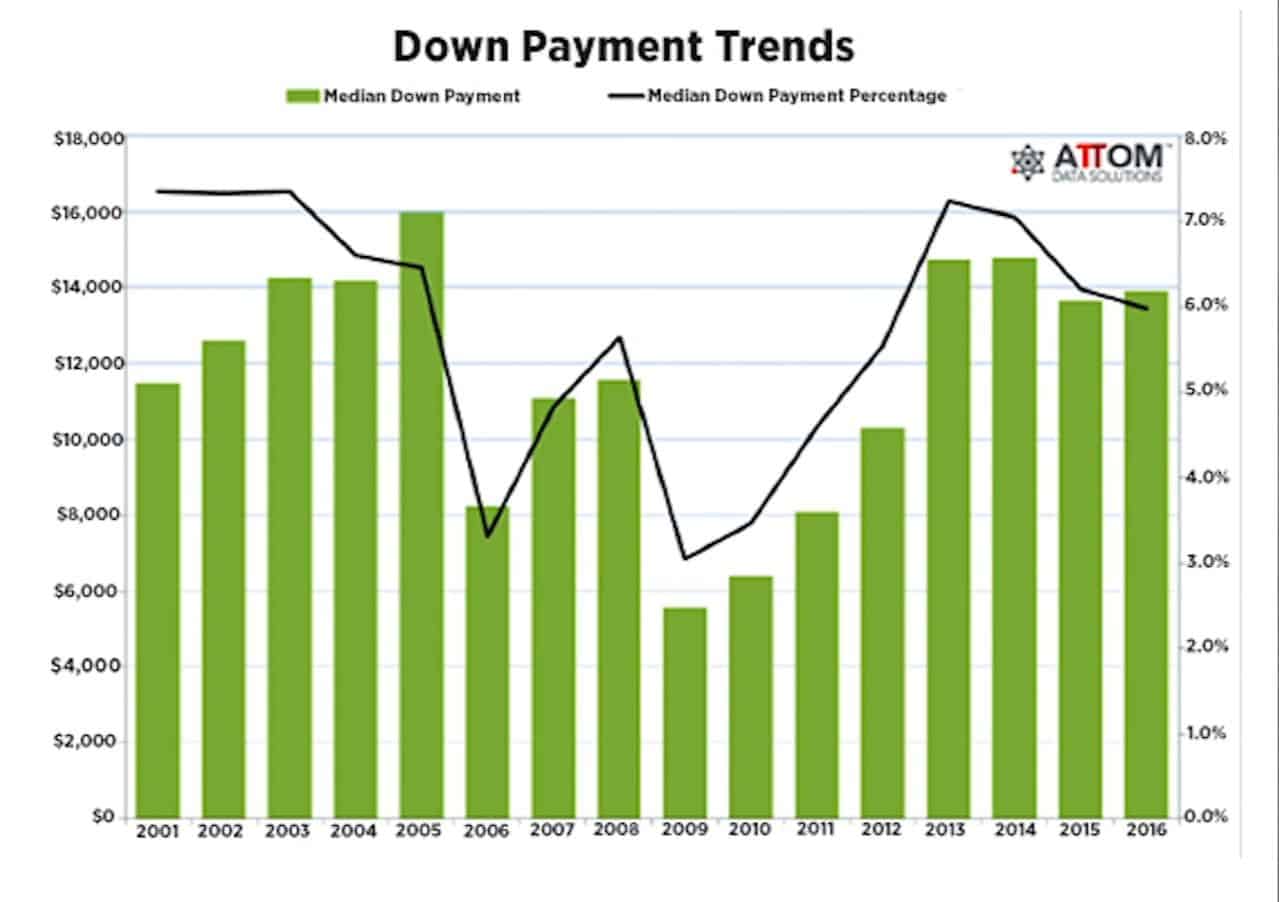

Yet, please look at the down payment trends chart.

We can see by looking at the chart that those claims are just fake news.

From 2003 to 2005, the average down payments were around 6%, they went down dramatically in 2006, but just for one year when the bubble was at its peak, and then, the average dropped way down in 2009 because of all the government programs trying to prop up the housing market.

Now look at where it was back in 2015, my guess is it would be very similar today, right around 6%, the exact same downpayment on average that was required in 2003, 2004 and 2005 as the bubble was growing in size.

The lending standards are identical.

Having said this, I think you honestly need to asses what you’re upside is versus your downside and consider asking yourself before selling your house.

Look at the fundamentals, what could possibly drive prices higher? Are interest rates going to go down a lot?

Probably not, they’re already at zero.

Are we going to see a tremendous wage growth that will give consumers more purchasing power?

Probably not, real wages have been stagnant for the last couple of decades, they’ve increased slightly, but analyzing the last 20 years, they’re almost flat.

You also need to consider the Covid-19 and the last week’s 6.6 million jobless claims.

What are the people’s purchasing power increases over the next year?

You need to turn on your investment mindset and ask yourself, is your home right now cheap or is it expensive?

As we know, when things are cheap we buy them, and when they’re expensive we sell them, especially if you’re in a cyclical or hybrid market.

But looking again at the U.S. home prices, adjusted to inflation, the answer is it's most likely expensive.

It's also important you consider asymmetry. Even if you came to the conclusion that there’s a 50% chance of prices going up in real terms, and a 50% they go down, if they do go up, by how much?

Are they going to go up by 100%, 200% or 10%? And if they’re going to go down, by how much? 20% or 50% like they did in 2009 and 2012? Or maybe down by 60% like it did in Japan from 1990 to 2005?

Remember, over time, home prices tend to mean revert in every single market, regardless of whether they’re cyclical, linear, or hybrid.

This is due to wages typically staying consistent with inflation because wages are what people use to buy a home, therefore it makes sense home prices stay consistent with inflation, if not a national level, definitely on a local level.

So if you live in a cyclical market, and you thought about selling prior to the crisis, you should definitely sell now, I can’t see any upside in waiting.

The same exact thing goes for a hybrid market, but if you live in a linear market and your home is under $250,000, I wouldn’t rush to sell right away, I might think about it a little bit longer.

In conclusion, with a cyclical market and a hybrid, I would hit the bid right now, I think it’s a no brainer, and with the linear, I would wait.

However, that's not all, I want to throw a curveball.

This is just if you have 100% equity in your home, it's not for everyone.

If you are one of those, and if you want some dry powder to invest in other assets that may become very cheap over the next months with a recession, or you're hesitant about losing your job, it might be a good idea to take out some of your equity right now.

This way, you’ll have some cash, so if you do lose your job and have little to live on, or if you’re not worried about your income whatsoever, you should have some dry powder to take advantage of very cheap assets on a moving forward basis.

But, again, I want to be clear, I’m not suggesting everyone should use its house as an ATM machine.

I’m just giving an idea if you got to the conclusion that you don’t want to sell your house but you need cash either for dry powder or because you might lose your job.

Next, I will explain what is it that you need to know in order to determine if you should buy or wait.

During a housing bubble should we buy or wait?

If you thought about buying a house prior to the Covid-19 and now you're not sure what to do because of what’s coming down the pipeline, this is for you.

There are three components you need to consider: The R.V. ratios, the cost of the mortgage and the cost of construction.

First and foremost, ask yourself what are the R.V. ratios of the property?

Meaning the amount of rent you can collect per month compared to the amount of money you have in the property.

If you don’t know what R.V. ratios are, you can learn about them in this article.

If your R.V. ratio is under 1, then it might be a better deal to rent, and this goes back to what I said about the cyclical, hybrid, and linear market, and the home being under $250,000.

The reason that’s kind of a benchmark is that when you get over the $250,000, it’s really tough to find a home with an R.V. ratio of over 1, but if the house is under that price, it’s easy to find a deal.

If you can find and R.V. ratio of 1 is better to buy, if its lower than 1, maybe 0.4 or 0.5, it’s a much better financial decision to rent.

Next, you have to consider the cost of the mortgage.

Of course, interest rates are extraordinarily low, so if you can lock in a fixed rate interest 30-year mortgage, it might be wise to go for it, just if all the other conditions line up.

The third component I think it’s extremely important and most people overlook is the cost of construction.

Jason Hartman puts it this way.

“With real estate, one way to know if it's cheap is if the ingredients and the assembly of those ingredients cost more or about the price you’re paying.

Basically, the cost of all the raw materials and the ingredients of the house, copper wire, petroleum products, and look how cheap oil is right now, energy in general, lumber, concrete, steel, and glass are the ingredients of a house, plus the labor to assemble them.

So, if you’re buying a house at, close or below, ideally, the cost of construction, which depends on where you are, you’re fine, in terms of the cost of the construction approach, and especially with cheap debt.”

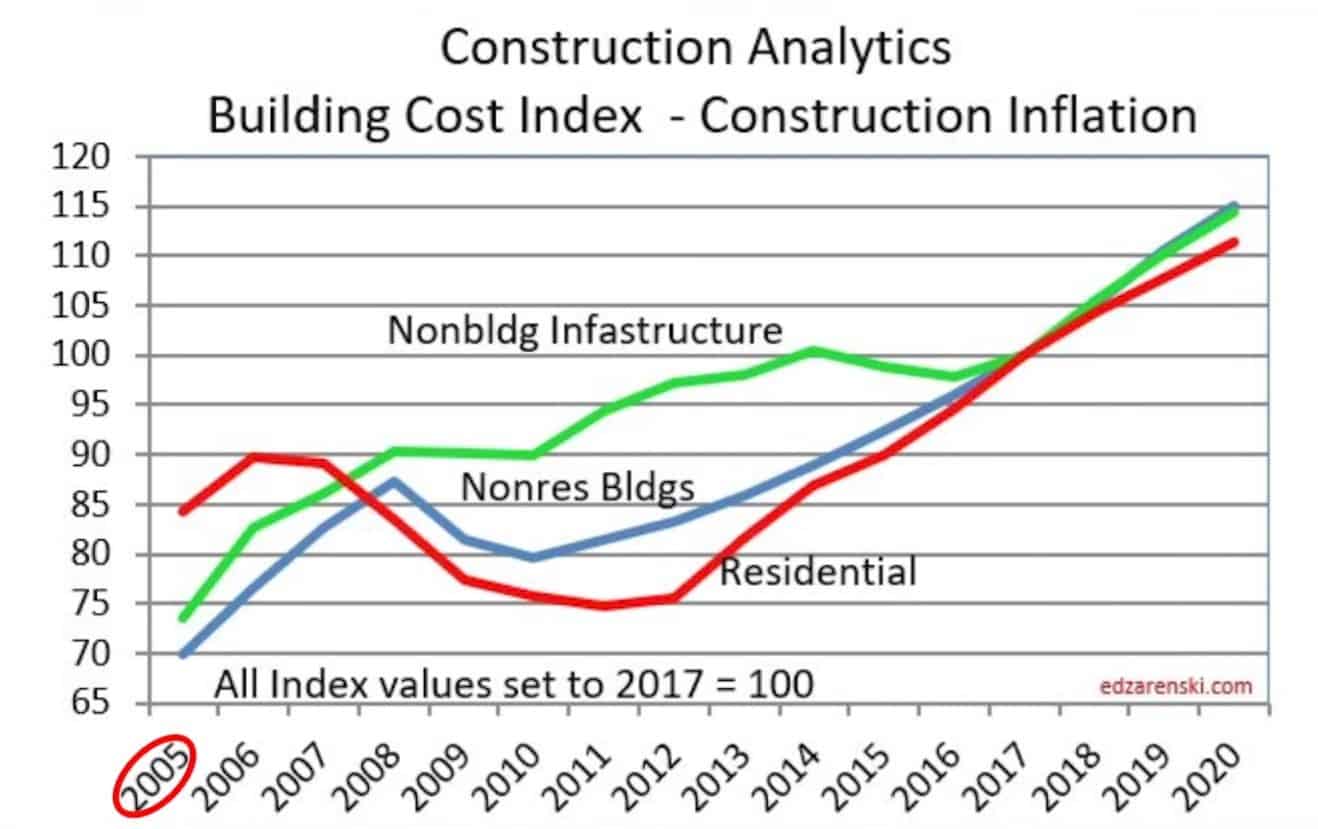

But, where is the general cost of construction right now? To answer that, let’s look at the United States construction analytics as a whole.

This chart goes to 2005 all the way to today’s date. This is an index chart, so it indexes to 2017, which is our starting point, a 100.

In 2005, the index was around 85, it went up to 90, stayed consistent but then crashed when housing prices went down in 2006 all the way to 2012.

Notice the downtrend in the building cost, which makes sense. Labor costs also went down, materials probably didn’t change much, but labor is what changed a lot along with the price of the land.

In 2012, when we hit the bottom and the market started to “recover” or re-inflate, so did the cost of construction taking us where we are today, around 115.

This graph shows us trends of what’s been happening in the United States, but it doesn’t show specific dollar amounts broken down by where you live.

So if you want to understand that further, visit Home Guide, a fantastic website and a great resource I found when I was doing some research for this topic.

On this webpage, you can start by looking at what is the cost of construction by region, the cost per square foot to build a house, and the breakdown of what it costs for each segment to build a home.

Still, all homes are not created equal from a standpoint of cost per square foot because when we look at $100 square foot to build or $150, we’re referring to a very basic, kind of a starter home.

Once we get into the custom finishes, the square foot cost goes through the roof.

Before we get to the end, I want to give you a bonus because I think many of you would love this information.

The Home Guide website I mentioned, also offers information on what does it cost to build a shipping container home. Cool, huh?

You can build one with $60,000 to $90,000, and if you want to build it bigger, it can cost around $150,000 to $175,000.

That's not all! You can also build a tiny house, which are very popular right now, and it can cost around $25,000 to $35,000.

If it’s a little bigger than the tiny house, about 600 square feet, you can build it for about $50,000 to $70,000.

I think this is a very cool idea, especially now when we’re maybe going to budgets because of the Covid-19 and looking to get out of the urban areas.

Check out how cool those tiny houses are.

In conclusion, if you’re in a cyclical market or a hybrid one, definitely wait to buy!

Don’t pull the trigger right now, and this isn’t investment advice, I’m just telling you what I would do or I would suggest to my family members.

There’s no way I would buy a house right now in a cyclical or hybrid market, I’m a 100% renter.

If you’re in a linear market, it's tougher, it’s 50/50, I can understand why someone would like to buy, and I also see a reason why you might want to hold off, but again, look at your R.V. ratio.

If you can get a house with a great R.V. ratio, it means it’s a better deal to buy, and of course, keep in mind the cost of construction. That would be my main consideration.

If I could get a home in a linear market and buy it for under the cost of construction, in a great area, with a great school and where I really want to live in, then I would consider pulling the trigger.

For more content like this, take a look at my blog and I will help you build wealth and thrive in a world of out of control central banks and big governments.

Comments are closed.