Is the real estate market on the brink of collapse?

These are things nobody is talking about, which is why I'm going to explain them to you. The US economy is headed for a recession if not a depression as a result that real estate prices may drop.

But there are no certainties, only probabilities, these are some catalysts that could trigger incredible amounts of selling, which would flood the market with additional supply.

In this 2020 housing bubble prediction article I explain the following:

- Additional supply hitting the market because baby boomers need cash!

- Supply hitting the market because Airbnb investors are forced to sell.

- Private equity funds rotating out of housing creating huge downward pressure on the housing market.

1. A Large Segment Of The Population Will Have No Choice But To Sell Their Homes

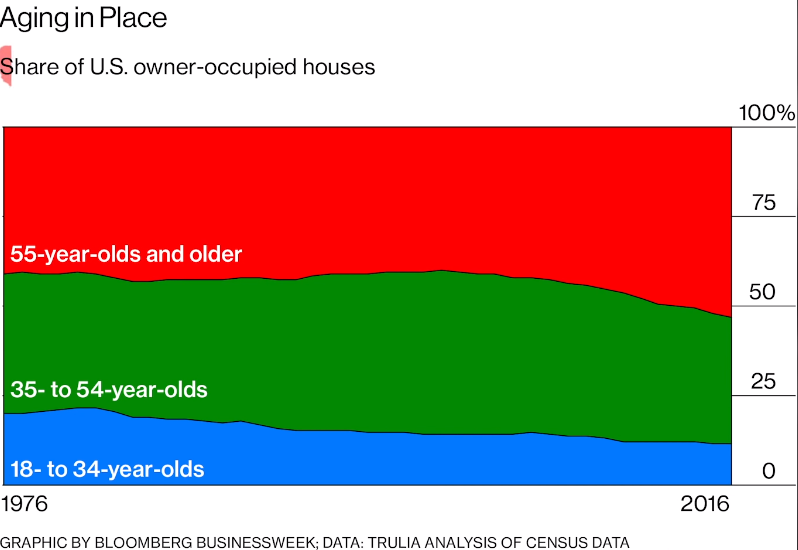

We have a large group of the population that have to sell and an even bigger group that cannot buy. Look at this chart going all the way back to 1976 to 2016.

On the right-hand side, it goes from 0% up to 100%. This is the share of homeownership, owner-occupied houses in the United States broken down by age group.

So 53% of homes in the United States are owned by people of 55 years and older. 30% of the homeowners are between 35 to 54 years old, and 17% ages from 18 to 34.

One thing I'd like to point out, right around the GFC, the percentage of homeownership by 55 and older increased substantially.

Most likely because so many of them were underwater and they couldn't afford to sell their homes without taking a huge hit, and the younger generations were willing to go through the process of just giving their keys back to the bank.

After going through all of this data, I've actually changed my thinking on this slightly. Before, I was looking at additional supply coming onto the real estate market, just through people who couldn't afford to pay their mortgage.

I was looking at the forbearance through the government programs and the fact that it takes a long time for banks to foreclose on people.

So if people are able to postpone making their mortgage payments, for at least a year, then it takes another year, another six months at least, for the bank to foreclose.

We wouldn't have a large glut of supply coming onto the housing market for at least a year and a half to two years.

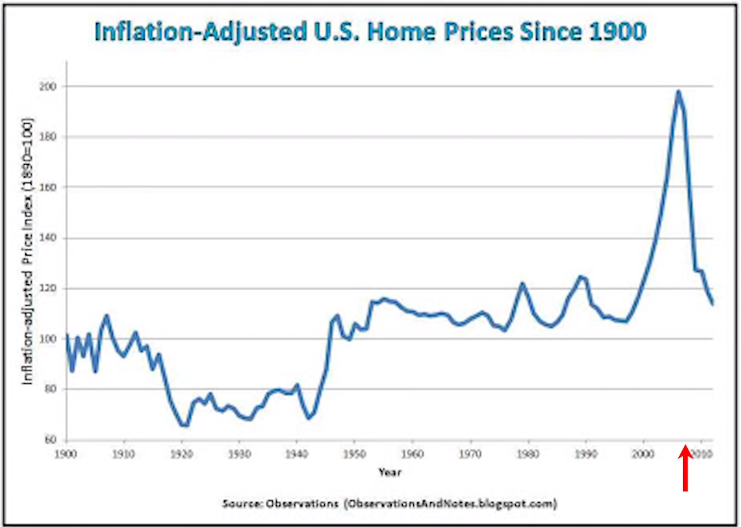

And if we look back to 2008's housing crash in this image, we can see the peak was in 2006 and we didn't hit a bottom in real terms until 2012.

But I think this time it could be slightly different. Because we have such a huge percentage of the housing stock owned by people 55 and older that might be able to make their mortgage payment, or they might own their home outright.

But, they need to sell because they have to have the equity they've built in the home in order to live.

Their unemployment rate is going through the roof. They can't afford to pay their living expenses, and the only source of funds they can tap is their home equity. Therefore, they're forced to sell.

We also have to remember the two largest portions of the population are:

- The baby boomers that will most likely have to sell

- The millennials that just can't buy, even in a healthy economy.

If the boomers were selling, if they were downsizing, the young people that were forming families would be there to buy up the housing stock.

But with the COVID, the instability, and the problem with the underlying fundamentals of the economy, the millennials aren't there to buy.

So we have all this supply coming onto the market and potentially a lot less demand.

So currently we have very little supply of housing in the market, but this could change very quickly as soon as the COVID is in the rearview mirror, and these baby boomers start feeling comfortable showing their house as they get squeezed tighter and tighter on their monthly budgets.

So they'll put their homes up for sale, and we'll see a dramatic increase in the supply and in the forced selling.

To dive further into the details and get some insights from a true insider in the real estate market, and in the macro community, I quote Danielle DiMartino Booth from one of the Rebel Capitalist Show interviews you can fully read here.

Danielle DiMartino B: What the boomers said 10 years ago was I can stay in the workforce for another decade. I'm just in my 60s. I can keep working. I like my big house.

I'm not so sick that I need to be close to a hospital. I can stay out here in the boonies, in my McMansion. I can afford to maintain it.

All of this calculus is going to be stuck on its head because the same generation is now 10 years older.

Are they going to say: “Well, I'm 75, so I can easily work until I'm 85?” We had 1.2 million people, 65 and older in March payrolls lose their jobs.

That I would argue is going to be a permanent job loss, because they're going to be other people who are going to rush to take those open positions who employers are going to hire because they're cheaper than the senior citizens were.

So again, we're going to have older Americans with the need to sell their homes, which we've never had despite this biggest generation. Now, the millennials are bigger.

Despite this biggest generation potentially having to have gone that route 10 years ago, they didn't. The stock market rebounded, quantitative easing was a brand new thing. The rally came roaring back.

The rebound was swift. They had a tripling of off the lows in their stock, and they were able to hold on. That's not going to be the case going forward for residential real estate in America.

We've had millennials, as a generation, lose proportionately more jobs than any other generation post-COVID-19.

Danielle DiMartino B: They have kids. They need homes. They need to buy the millennials homes, but they're in a worse situation financially than they were in pre-COVID.

George Gammon: And prices are skyrocketing…

Danielle DiMartino B: They can afford to buy fewer homes than they could before…

And the seniors are going to put their big McMansions on the market for high prices? No.

The divide has to be closed by prices coming down, such that you put the willing buyers in touch with the willing sellers.

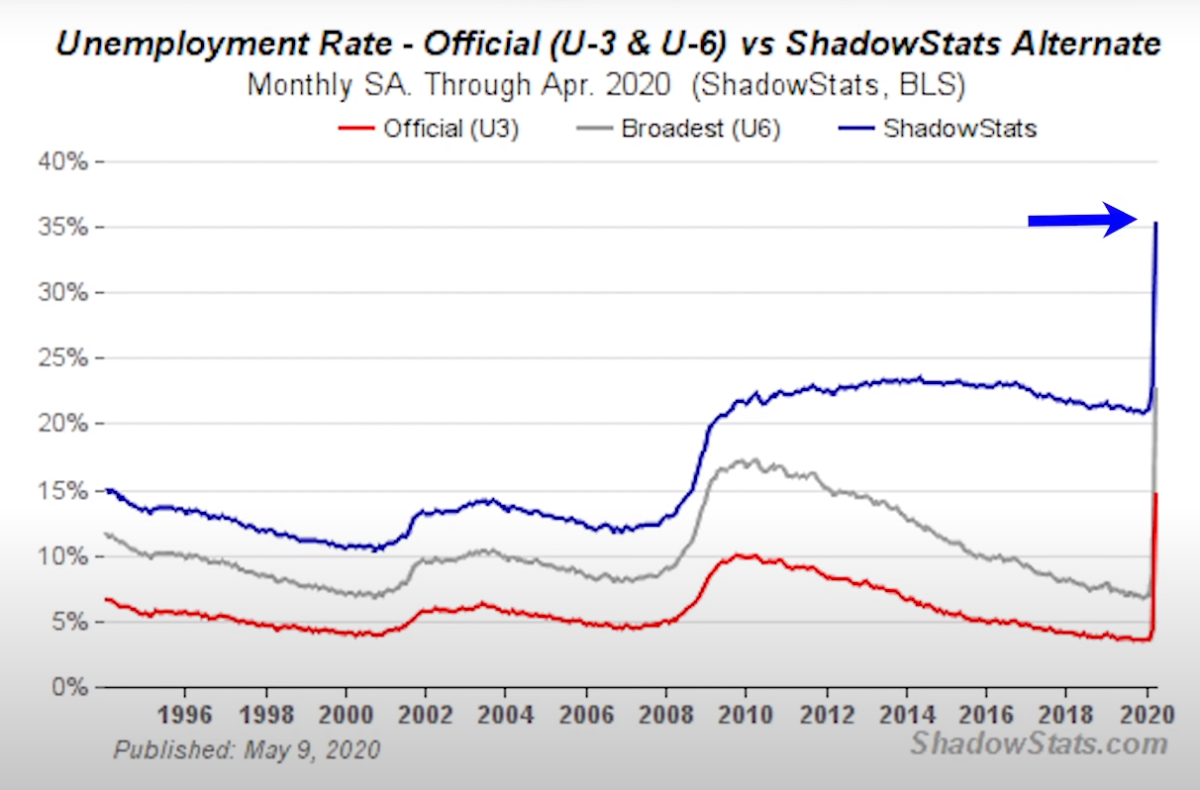

Now, let's look at some statistics and some hard numbers. 15.6% of the baby boomer population is now unemployed, according to the government.

The unemployment rate among people age 65 or older is now 15.6% due to coronavirus-related job losses.

– Sarah O' Biren from CNBC.

Of course, these numbers are most likely very low. If we look at shadow stats, we see that the government's numbers are saying about 15% unemployment overall.

But if you measure things the way they're measured in the 1980s, all the way up to the early 1990s, we see that the actual unemployment rate would be closer to 35%.

So if the baby boomer population is 15.6% unemployment, according to the government, we could safely assume that the number is definitely North of 20%. 50% of Americans, age 56 to 61 have less than $21,000 in savings.

Half of American families in the 56-to-61 age bracket had less than $21,000 in retirement savings in 2016, according to a longitudinal study by the Economic Policy Institute that used the most recent available figures.

– Will Englund – The Washington Post

The only access they have to purchasing power, most likely, is a credit card or their home equity.

Forty percent of Americans over the age of 60 who are no longer working full-time rely solely on Social Security for their income — the median annual benefit is about $17,000.

– Will Englund – The Washington Post

So those are the sellers. Those are the people that are going to be forced to liquidate, to come up with the cash they need to pay for their living expenses.

Now, let's look at the other side of the coin. The potential buyers. The millennials.

According to a recent study Vox published: “55 percent of Americans under the age of 45 had either had hours cut, been laid off, or been furloughed as of April 26.“

And let's keep in mind…

Every industry has been affected by layoffs, but looking at the data from March, it is clear that the leisure and hospitality industry (which includes hotels and restaurants) alone lost 459,000 jobs.

– Sean Collins of Vox –

That section of the economy lost over 450,000 jobs, but also let's look at their balance sheet. The same article also mentions:

Millennials are loaded up with student debt, ages 25 to 34 have almost $500 billion in student loans!

Keep in mind, they cannot get rid of, even if they go through a bankruptcy. Ages 35 to 49 have over $580 additional billion.

So over a trillion dollars in student debt for this group of the population that somehow has to come up with a down payment for a home while 55% of them are either getting their hours cut, being laid off or losing their job altogether.

When you put these pieces of the puzzle together, you have a huge increase in the supply and a complete collapse in the demand.

2.The Airbnb Wildcard

You may be asking yourself, how much impact does Airbnb really have on the overall real estate market?

To answer that question, take a look at this.

…A year-over-year Airbnb contribution to rent and price growth equal to 0.59 percent and 0.82 percent, respectively.

– Joanna Clay of Phys.org.

This means that if prices go up by 6%, Airbnb caused 0.8 of the 6%. It doesn't sound like a lot, but that accounts for 13% of the price move.

Overall, Airbnb probably contributes about… One-seventh of the average annual increase in US housing prices.

– Joanna Clay of Phys.org.

I‘d like to point out that if it adds that much increase to the housing prices, it can add that much decrease, if not more to the housing prices.

Dowell Myers, a professor at the USC Price School of Public Policy thinks it's possible this paper, where we're getting this data could be underestimating Airbnb's impact.

So Airbnb has a significant impact on the real estate market, not only on the rental side, but the price side as well.

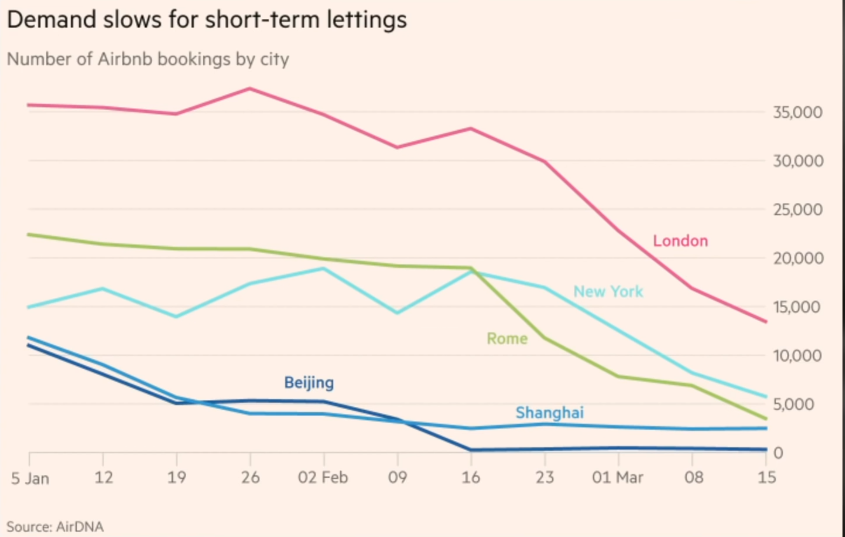

Here is a chart on how Airbnb is doing in a world with the COVID.

Goes from January 5th to March 15th. So obviously, now, in the middle of May, these numbers are going to be a lot worse.

London starts off with about 35,000 bookings. Now, I'd imagine this is per day, but going to March 15th, it tanks all the way down to under 15,000.

Rome is even worse! Starts off at 20,000, ends up under 5,000. New York, where they went into lockdown a lot later, goes up, down, up, down, but then ends up around 5,000 as well.

Beijing and Shanghai started off around 5,000. As of March 15th, they were literally at zero. So the first question I would have is…

What happens to these owners ability to pay their mortgage?

And let's not forget a large majority of the Airbnb owners don't have loans backed by Fanny and Freddie. What does that mean?

It means they don't qualify for forbearance, even though they're renters. These short term people aren't paying them rent.

They can't get a break from having to pay their mortgage. Also the virus liability.

What does this do to their insurance rates?

And what happens when people start to get sued as a result of the COVID. Maybe someone stays there, or, who knows where they got COVID. Maybe they sued the owner of the property as a result of them getting sick.

Especially in the United States, by far the most litigious country in the world, but also a lot of people, even in single-family homes, house hack through Airbnb. That's the only way they can afford to pay their mortgage.

A lot of real estate investors that have specifically focused on Airbnb go into higher-priced properties that would have been cashflow negative with a longterm rental.

But with an Airbnb, because they rent it out short-term, they can still be cash flow positive.

But if this flips to where they can't make any money on the Airbnb side, it goes back to a longterm rental. All of a sudden they're cashflow negative.

They have to sell.

And the biggest question of them all is…

Will Airbnb even be able to stay in business?

We see companies like Uber, Tesla, and Airbnb as rocks, solid businesses that are just immovable. But we forget that these businesses lose a lot of money.

Airbnb last year, 2019, lost over $276 million for the year, according to Yahoo! Finance.

So if that was 2019, what's going to happen to their balance sheet in 2020?

To give you a perfect example of what I'm referring to, look at this article from The Financial Times. They give an example of someone who has properties near Universal Studios in California.

Evandro Patricio is a full-time Airbnb host in the city. His five apartments are in condominiums, a stone's throw from Universal Studios. Three weeks ago his occupancy rates were 80%. Today there is not one guest in sight, with all bookings canceled until the end of July.

“I have nothing booked for the next few months. We've been really feeling the whole thing.” says Patricio.

He will lose about 24,000 in revenue, monthly, as long as the Covid-19 emergency continues, but he must still find $5,000 – $6,000 in taxes, utilities, and homeowner association fees.

The bottom line is this could create a massive amount of forced selling. In addition to what we talked about the baby boomers.

3. The Private Equity Wild Card

To understand this further, let's go straight to the New York Times.

Wall Street's latest real estate grab has ballooned to roughly $60 billion, representing hundreds of thousands of properties. In some communities, it has fundamentally altered housing ecosystems in ways we're only now beginning to understand, fueling a housing recovery without a homeowner recovery.

Regarding private equity, I wanted to throw in my own personal story. I retired in 2012. When I did, I started investing in real estate.

Specifically, I would go to tax foreclosure auctions in the Midwest. And I remember back then through 2012, '13, '14, every single person at the auction, I'd say 90% of them, that I was competing against were representing private equity funds. Especially going from 2012 to 2014.

In 2014, they were just packed. I mean, hundreds of individuals representing private equity funds and hedge funds bidding on foreclosures.

This is back when I didn't know a lot about macro, but even back then, I saw this as being a huge potential problem in the future.

Now, please look at this awesome diagram I found online. It starts off with the Fed. They dropped interest rates down to 0% for over eight years. So these pension funds can't get a yield. They have to go further and further out the risk curve.

What do they do? They invest in private equity funds. They take the money, invest in single-family homes, and they also provide financing, kind of like a hard money thing.

And they buy non-performing mortgages from banks. They foreclose on the individuals, take those homes, and put them into their portfolio.

They rent the homes out to generate cashflow. This is basically institutionalizing the market, which used to be made up solely of just mom and dad real estate investors.

They introduced cloud computing and proprietary software, basically a lot of technology that they say they can use to manage thousands of rental properties.

In reality, they can't. They cannot manage these things well. There is an article, after article of these private equity funds buying up all these homes and the property management goes straight down the toilet.

Property management is something that's incredibly difficult to scale.

Even with technology, it's still just a person to person business. Then the funds use the cash flow from the rent to create a new asset class, to sell to investors, to generate more liquidity.

In other words, they securitize them and sell them to Wall Street.

Of course, the ratings agencies play right along with this financial engineering. They give all of these assets great ratings, and that allows the investors of the private equity funds to generate more money from the pension funds themselves.

But let's think this through…

What happens if these private equity funds think the market is going to start to go down?

Their margins are extremely thin. They're not going into these linear markets like I suggest with Hartman about getting huge positive cash flow and taking out 30 year fixed rate debt.

This is a completely different ball game.

What's going to happen if prices start to go down?

These private equity funds could say, “Listen, we want to sell at the top. We've made a ton of money. Why should we hang on? Why should we keep buying these properties? And what we do have in a portfolio, we're just going to go ahead and liquidate it and get out before the crash comes.”

They're going to liquidate their portfolios and get out of Dodge as fast as they can, leaving the investors, the renters, and the real estate market as a whole to be left holding the bag.

So when you look at the situation:

- The baby boomers

- The collapse in Airbnb and

- The liquidation from all of these private equity funds…

This is a massive amount of forced selling, creating potentially huge amounts of supply in the current real estate market.

But I want to be very, very clear. I'm a big fan of certain real estate investing. Not all of it. I'm very, very nuanced.

As most of you know, I like going into linear markets, having a lot of positive cash flow, and using 30 year fixed rate debt to your advantage.

But now as we go into a recession, if not a depression, I don't think it's the time to be aggressive. Yes. Look at the market. Look at deals. Do your comps, do your homework, but sit back and be patient.

Let the market and the good deals come to you.

Comments are closed.