The commercial banking system in the US will no longer be in charge of credit creation because the Fed is trying to manage credit creation by manipulating interest rates.

This may help central planners tame inflation and apply yield curve control, but it will make the US wealth gap bigger, and as a consequence, forge a poorer country.

To better understand this, we need to realize what our preconceived notions are and how wrong they are.

Some Preconceived Notions On Interest Rates And Inflation And How The 1970s Data Can Prove Us Wrong

“If interest rates go up, the dollar gets stronger.”

George says most of us have some common preconceived notions around interest rates and inflation in the US. And the dollar gets stronger with rising interest rates. This is incorrect.

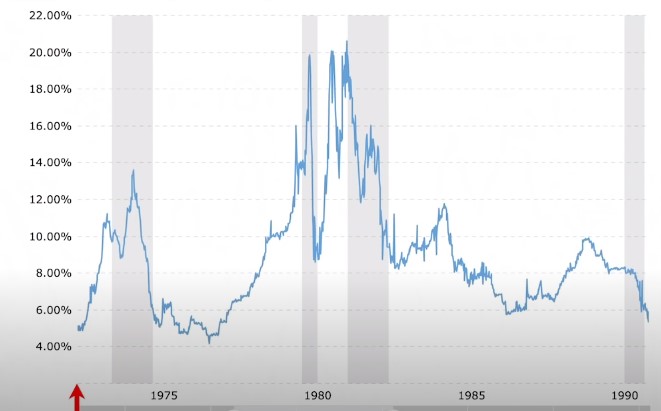

Interest rates went to 14% during the early 1970s, as you can see in the image below.

However, the dollar went up during this time when compared to the DXY, which is the dollar against a basket of other global FIAT currencies, as shown in the image below:

“If the CPI goes double digits, the dollar will collapse.”

Another popular belief George mentions is, if CPI goes to double digits, then the dollar will collapse and lose its reserve currency status.

In the early 1970s, the CPI was at 12% (red line in the image below), and it did go down to about 7%, but only as much as it did in 2020, where it went from 100 to 90.

Then, in the mid to late 1970s when inflation went back up, the dollar went down slightly, but it didn’t collapse or lose its reserve currency status, as some people may think.

There is no tight correlation between the ranges of inflation that the US Government is willing to admit to, and the Dollar on the DXY.

“The only action needed to control inflation is the rise of interest rates.”

George also points out that many people believe the only action needed to control inflation is to raise interest rates. This happened twice in the US between 1975 and 1980 before Paul Volcker, an American economist, was able to curtail inflation.

It’s vital to remember that raising interest rates doesn’t mean inflation will be tamed. Once the inflation genie gets out of the bottle, it’s very hard to get it back in.

George also noticed that mainstream economists or PhDs at the Fed, always seem to conflate inflation as economic growth. But when we look at the 1970s data, we can see this is not true.

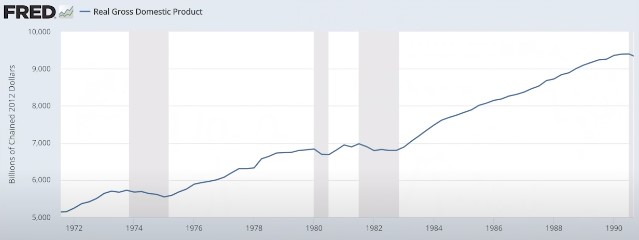

In 1974 inflation was at 12%, yet the real GDP went down (as shown in the image below).

Economic output in the US decreased while inflation went parabolic. And the same occurred during the late 1970s when inflation shot back up.

The economy can get worse regardless of the inflation number. George thinks we can have an economic depression while the prices of goods and services go up. Meaning we can have an inflationary depression.

But, instead of getting hyper-focused on deflation or inflation, we should focus on the economic output of the private sector and the real economy.

According to George, the difference between the 1970s and today is debt. Back in the 70s, it was low.

In 2021, consumer, corporate and government debt are all at, or near, all time highs.

Also, back in the 1970s, the US wasn’t in the financial predicament like it is now.

Today, the US economy needs asset prices going up, or it starts to stagnate. And yes, raising interest rates was the go-to option during the 70s, but is no longer viable today.

Understanding The Yield Curve Control

What can you do with an economy where prices are going up, as well as bond yields and interest rates?

At a certain point, those high-interest rates will crush the US economy because it is burdened with debt and is built on continuously increasing asset bubbles.

If interest rates go up, the debt can no longer be serviced and asset prices will come crashing down. This is why central planners have to act and institute yield curve control.

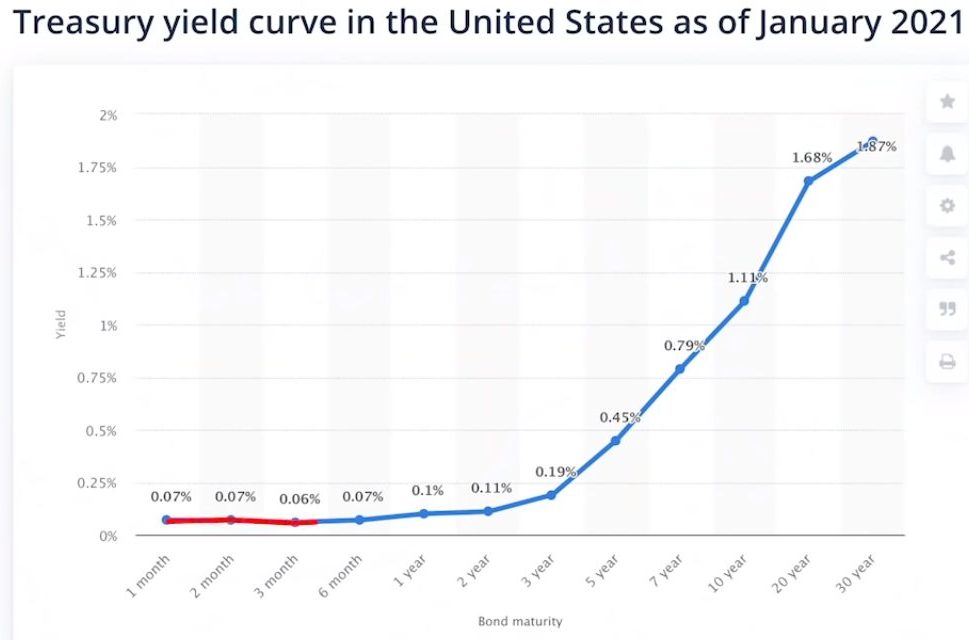

The chart below displays the US yield curve as of January 2021. On the bottom, it goes from one month Treasury bill to 30-year long treasuries. On the left, interest rates go from 0% to 2%.

When interest rates cross the 2% line, the curve enters the ‘no-bueno’ zone, according to George because that is when the economy and the stock market crash.

When this happens, the Fed comes in and applies yield curve control (YCC).

The difference between YCC and Quantitative Easing is that when QE is done, the number of treasuries the Government buys from the primary dealers is limited. With YCC the number is unlimited. This way they can keep interest rates under control.

Then, the Fed comes in and monetizes the debt by creating more funny money and bank reserves.

This is the beginning of Modern Monetary Theory, along with the US government creating Stimulus checks to be spent in the real economy, which increases the M2 money supply.

So the question is:

With the Fed’s yield curve control and the Government’s spending, what can be done to avoid hyperinflation?

Russel Nappier’s Dire Warning About The US Economic Future

Russel Nappier, the pro all pros go-to for advice, and to understand the economy, gives a dire warning: The US is heading towards a command economy.

What is a command economy?

The United States is moving from a market economy to a command economy where central planners control the amount of money supply.

The main problem these central planners have is they need to continue printing money to artificially prop up the US economy. But they can’t afford to allow interest rates to go above a certain level (<2%).

How can central planners prevent hyperinflation?

Currently, and in the past, the commercial banking system was responsible for creating the majority of the money supply. Now, the Fed is trying to manage credit creation by lowering or raising interest rates.

Usually, banks issue loans that go into the real economy, which creates an additional M2 money supply. Producers would receive those loans and increase the supply of goods and services, escalating the standard of living.

When we transition into an economy where the commercial banking system is no longer in charge of credit creation, there are no longer incentives to lend money to producers of goods and services that make society as a whole, richer.

This is called the Cantillon effect, where the newly created money goes to the ‘insiders’, people with political and financial influence, reducing the supply of goods and services.

Then, the Government tries to compensate for this lack of production with stimulus checks that only make the wealth gap bigger.

Inflation may be under control and central planners could apply YCC, but as long as the wealth gap becomes bigger, the poorer the US will become.

Make sure to click on the video above for a deeper understating of the American economy transition from a market economy into a command one.

Comments are closed.