The dollar has been the world's reserve currency for over 70 years, but its dominance is now being challenged by other currencies. The value of the dollar is influenced by several factors, such as inflation, interest rates, and government debt.

Mismanagement of these factors can lead to a decline in the value of the dollar. This could have significant global implications, such as an increase in inflation, a decrease in international trade, and a shift in power dynamics among countries. But will it lead to a dollar collapse anytime soon?

There are various theories about how and when a dollar collapse could happen. Some experts believe that it could be triggered by excessive government spending or a sudden loss of confidence in the US economy.

Others predict that a dollar collapse could be caused by external factors such as a major geopolitical event or the rise of alternative currencies like Bitcoin.

It is important to note that no one can predict with certainty when a dollar collapse will occur or how severe it will be.

However, staying informed about this topic is crucial given its potential impact on global markets and economies.

Understanding the Basics: What is a Currency Collapse?

Causes and Consequences of a Currency Collapse

A currency collapse is a situation where a country's currency loses its value rapidly, leading to significant economic consequences. This can happen due to various reasons, such as hyperinflation, political instability, and economic crisis.

Hyperinflation is one of the most common causes of currency collapse. It happens when there is an excessive increase in the money supply, leading to a decrease in the currency's purchasing power. When people lose faith in their country's currency, they hoard goods and services, further exacerbating inflation.

Political instability can also lead to a currency collapse. When there is uncertainty about the future of a country's leadership or government policies, investors may become hesitant to invest in that country. This can lead to capital flight and decreased demand for that country's currency.

Economic crisis is another factor that can lead to a currency collapse. For instance, if a country has high levels of debt or trade deficits, it may not be able to pay back its creditors or finance its imports. This can cause investors to lose confidence in that country's economy and pull out their investments.

When a currency collapses, it leads to several consequences for the citizens and businesses within that country. One immediate consequence is that imports become more expensive since buying foreign goods takes more units of local currency. This can lead to inflation as prices rise due to increased demand for domestic goods.

In extreme cases, a currency collapse can result in social unrest as people struggle with rising prices and decreased purchasing power. Businesses may also suffer as they struggle with higher costs for raw materials and decreased demand from consumers who have less disposable income.

Bank failures are also possible during a currency collapse as depositors withdraw their funds from banks fearing bankruptcy or loss of value due to the devaluation of local currencies. In such situations, governments may impose restrictions on withdrawals, further eroding trust among depositors.

It's important to note that a currency collapse doesn't necessarily mean the end of a country's economy or financial system. Many countries have experienced currency collapses and have bounced back through economic reforms, fiscal discipline, and international aid.

For example, in the 1990s Argentina faced a severe currency crisis due to high levels of debt and inflation. The government was forced to devalue the peso, leading to bank failures and social unrest. However, through economic reforms and international assistance, Argentina was able to stabilize its economy and regain investor confidence.

Similarly, Zimbabwe experienced hyperinflation in the early 2000s, leading to its currency collapsing. However, through policy reforms and international support, Zimbabwe has stabilized its economy and reintroduced its own currency.

The Truth About Dollar Collapse: Separating Fact from Fiction

While the concept of a dollar collapse may seem like a recent phenomenon, it has actually been predicted for many years due to the country's increasing debt and money printing.

The United States' national debt has been skyrocketing for decades, reaching over $28 trillion in 2021. This level of debt is unsustainable and could lead to a complete economic collapse if not addressed properly.

Many people believe that alternative currencies, such as Bitcoin, will replace the dollar in the event of a collapse.

While it is true that cryptocurrencies offer some benefits over traditional fiat currencies, they also have their own limitations and challenges.

For example, the value of bitcoin can be highly volatile, making it difficult to use as a stable store of value or medium of exchange. Additionally, there are concerns about security and regulation surrounding cryptocurrencies.

Another potential solution to prevent a total economic collapse would be a reformation of the monetary system itself.

Similar to the Protestant Reformation in the 16th century that led to changes in the Catholic Church, a monetary reformation could address some of the underlying issues with our current system.

However, this would require significant changes and control from those in power.

One technology that has been gaining attention as a potential solution for creating a more decentralized and free monetary system is blockchain.

Blockchain technology allows for secure transactions without relying on centralized intermediaries such as banks or governments. This could potentially reduce corruption and increase transparency in financial systems.

However, implementing blockchain technology on a large scale would require significant changes to existing systems and infrastructure. Those who currently hold power within financial institutions may resist these changes due to concerns about losing control or influence.

It is important to note that while some may view a dollar collapse as an entirely negative outcome, there could also be positive aspects resulting from such an event. For example, it could lead to increased innovation and competition within financial systems, ultimately resulting in a net good for society.

Debunking Dollar Collapse Fears: Insights from Brad McMillan

Brad McMillan's Insights on Debunking Dollar Collapse Fears

The idea of a dollar collapse has been circulating for years, and it is not surprising that many people are worried about this possibility. However, Brad McMillan, the Chief Investment Officer at Commonwealth Financial Network, believes that these fears are unfounded and overblown.

McMillan argues that the US dollar remains the world's reserve currency and is backed by the strength of the US economy, which is still the largest in the world. The US economy has shown resilience despite various challenges such as political instability, trade wars, and pandemics. In fact, it has been growing steadily over time.

According to McMillan, while there may be short-term fluctuations in the value of the dollar due to economic or political events, there is no evidence to suggest that a complete collapse of the dollar is imminent.

He explains that even during times when there were significant economic downturns like during 2008 financial crisis or COVID-19 pandemic in 2020; investors still flocked to safe havens like U.S. Treasuries.

The Strength of The US Economy

One reason why McMillan believes that fears of a dollar collapse are unwarranted is because of the strength of the US economy. Despite some challenges faced by America in recent years, including political turmoil and trade tensions with China, its economy continues to grow at a steady pace.

In fact, according to data from World Bank Group (WBG), the United States Gross Domestic Product (GDP) was $21.44 trillion in 2019, which accounted for almost one-quarter (24%) of global GDP. This figure shows how much influence America has on global economics.

Furthermore, America's unemployment rate was only 3.5% before the COVID-19 pandemic hit, which was considered a full employment rate, meaning most people who wanted jobs had them already. Even after the COVID-19 pandemic, the unemployment rate is still lower than in many other countries.

The Role of The US Dollar as World Reserve Currency

Another reason why McMillan believes that fears of a dollar collapse are unfounded is because of the role that the US dollar plays in global economics. The US dollar is the world's reserve currency, which means that it is used for international trade and transactions.

This status gives America significant influence over global financial markets and allows it to borrow money at lower interest rates compared to other countries. In fact, according to data from International Monetary Fund (IMF), more than 60% of all foreign exchange reserves held by central banks around the world are denominated in US dollars.

Moreover, most commodities, such as oil, gold, or silver, are priced in U.S. dollars, strengthening its position as world reserve currency.

Short-term Fluctuations vs Long-term Trends

McMillan also points out that while there may be short-term fluctuations in the value of the dollar due to economic or political events, these fluctuations do not necessarily reflect long-term trends. He explains that even during times when there were significant economic downturns, like during the 2008 financial crisis or the COVID-19 pandemic in 2020, investors still flocked to safe havens like U.S. Treasuries.

In addition, McMillan argues that even if there were a decline in demand for US dollars due to unforeseen circumstances, this would not necessarily lead to a complete currency collapse. Instead, it could result in a gradual shift towards other currencies, such as Euro or Yuan.

The US Dollar's Dominance: Why It's Here to Stay

The US dollar has been the dominant currency in the global economy for decades, and it is unlikely that this will change anytime soon. The reasons for its continued dominance are multifaceted, including historical, economic, and political factors.

Global Economy and Reserve Currency

One of the primary reasons why the US dollar remains dominant is because many countries use it as a reserve currency. This means that central banks hold large amounts of dollars as a way to stabilize their own currencies and facilitate international trade.

In fact, according to the International Monetary Fund (IMF), over 60% of global foreign exchange reserves are held in dollars.

In addition to being a reserve currency, many countries also conduct international trade in dollars. This is because the dollar is widely accepted around the world, making it easier for businesses to transact with each other across borders.

The use of dollars as a medium of exchange helps reduce transaction costs and provides greater liquidity in global markets.

Global Power Structures

Another reason why the US dollar remains dominant is because of America's position as a global superpower. The country's political and military influence has historically been tied to the strength of its currency.

As such, many countries view holding dollars as a way to align themselves with American power structures.

Furthermore, many commodities, such as oil, are priced in dollars on global markets.

This means countries must hold dollars to purchase these essential resources. As long as this system remains intact, it will be difficult for any other currency to challenge the dominance of the US dollar.

Economic Stability and Reliability

The US economy's stability and financial system's stability and reliability have also contributed significantly to the dollar's dominance.

Despite occasional economic downturns or crises like those seen during the 2008-2009 financial crisis or the COVID-19 pandemic recession period recently experienced by all economies around globe, investors still perceive American assets as a safe haven.

This is because the US has a long economic stability and growth history, and its financial system is highly regulated and transparent.

In addition, the Federal Reserve Bank (Fed) plays a critical role in maintaining the stability of the US economy.

The Fed's monetary policies impact the US and global markets, making it an important player in international finance.

The Fed has shown its ability to act decisively during times of economic uncertainty, such as by lowering interest rates or implementing quantitative easing measures.

Challenges to Dollar Dominance

Despite these factors supporting dollar dominance, there have been challenges to its position as the world's primary currency.

For example, China has been steadily increasing its economic influence on the global stage and challenging American hegemony.

China has been promoting its own currency, the yuan (also known as the renminbi), as an alternative to the dollar. It has established swap lines with other countries that allow them to trade directly in yuan without having to convert into dollars first.

Additionally, China has been investing heavily in infrastructure projects around the world through initiatives like Belt and Road Initiative (BRI). These investments are often made in yuan rather than dollars.

Cryptocurrencies have also emerged as a potential challenge to dollar dominance. Some experts predict that cryptocurrencies could eventually replace traditional currencies altogether due to their decentralized nature and ability to facilitate peer-to-peer transactions without intermediaries like banks.

However, despite these challenges, none of them have yet significantly impacted the status of dollar dominance.

While China's influence is growing rapidly, it still lags behind America in many key areas, such as military power and innovation capacity; thus, it cannot replace America's leading role anytime soon.

Similarly, while cryptocurrencies have gained popularity among some investors, they are still not widely accepted by businesses or governments around the globe for day-to-day transactions.

Weaknesses of the US Dollar: Examining the Issues

The US dollar has long been considered the world's dominant reserve currency in international trade and finance.

However, in recent years, other currencies like the euro and yuan have challenged its strength as a global reserve currency.

This shift is driven by several factors that have weakened the dollar's position as a reliable store of value.

One of the primary weaknesses of the US dollar is its vulnerability to inflation. Inflation erodes the purchasing power of money over time, reducing its value.

The Federal Reserve's monetary policies play a significant role in controlling inflation, but they can also lead to fluctuations in the value of the dollar.

When interest rates are low, investors may seek higher returns elsewhere, leading to a decline in demand for dollars.

Another factor affecting the value of the US dollar is government debt. As governments borrow more money to fund their spending programs, they increase their debt levels and reduce confidence in their ability to repay those debts.

This can lead to higher interest rates on government bonds and further weaken the value of the dollar.

The dominance of the US dollar in global trade has also led to trade imbalances and a reliance on foreign investment to finance deficits.

Countries that export more than they import accumulate large surpluses of dollars that they use to buy US assets such as Treasury bonds or real estate.

This inflow of foreign capital can help finance budget deficits but also makes it difficult for policymakers to control exchange rates.

The status of the US dollar as a safe haven currency is being threatened by geopolitical tensions and economic uncertainty around the world. During times of crisis or instability, investors often flock to safe-haven assets like gold or Swiss francs.

However, with increasing political polarization and economic volatility globally, investors are becoming less confident about relying solely on one currency for safety.

Furthermore, there are concerns about the declining use of USD in international transactions as more countries seek alternative payment systems bypassing it altogether.

With the increasing adoption of digital currencies, the US dollar's role in global finance may be further challenged. This trend is driven by a desire to reduce dependence on the US financial system and avoid potential sanctions or restrictions.

The US dollar's role in the global financial system is also being questioned, with calls for a new international monetary system that is less reliant on any one currency. Some experts argue that a multi-currency reserve system would be more stable and less prone to fluctuations than one dominated by a single currency like the USD.

Assessing the Impact of Currency Collapse on Investors

Investors with assets denominated in a collapsing currency may face significant losses as the value of their investments decreases rapidly.

This is because a currency collapse often leads to hyperinflation and a sharp decline in purchasing power.

For example, during the Zimbabwean dollar collapse in 2008, the inflation rate reached an astonishing 231 million percent, rendering the currency virtually worthless.

The collapse of a reserve currency can have a cascading effect on the global financial system, leading to increased risk for investors across all asset classes.

A reserve currency is widely accepted and held by central banks around the world as part of their foreign exchange reserves. The US dollar is currently the world's primary reserve currency, accounting for approximately 60% of global foreign exchange reserves.

If the US dollar were to collapse, it would have far-reaching implications for investors worldwide. As countries begin to diversify away from the dollar, there could be significant capital outflows from US markets, leading to lower stock prices and higher interest rates. This could also lead to increased volatility in other currencies and asset classes.

Alternative currencies such as gold or cryptocurrencies may provide a hedge against currency collapse but investors should carefully assess the risks and benefits before investing.

Gold has been used as a store of value for centuries and is considered by many to be a safe-haven asset during times of economic uncertainty.

Cryptocurrencies such as Bitcoin are decentralized digital currencies that are not tied to any government or central bank.

However, both gold and cryptocurrencies come with their own set of risks. Gold prices can be volatile and subject to manipulation by large players in the market.

Cryptocurrencies are still relatively new and untested, with many experts warning of potential bubbles or scams.

A currency collapse can also impact access to global commerce, making it difficult for investors to buy and sell assets in other countries.

For example, during Venezuela's ongoing economic crisis, strict government controls on foreign currency exchange have made it nearly impossible for citizens to access foreign markets or purchase goods from abroad.

The use of AI and other advanced technologies can help investors better assess and manage risk during times of currency instability.

AI-powered tools can analyze vast amounts of data in real time, providing investors with insights into market trends and potential risks. These tools can also be used to create customized portfolios that are tailored to an investor's specific risk tolerance and investment goals.

Why the Chinese Yuan Can't Take Over: Oceans of Dollars vs. Lake Michigan of Yuan

The Chinese yuan has been gaining strength in recent years, but it is still far from being able to take over the US dollar as the world's reserve currency. There are several reasons why this is the case.

Not Fully Convertible

One of the main limitations of the Chinese yuan is that it is not yet fully convertible. This means that there are restrictions on how much money can be moved in and out of China and on who can hold yuan-denominated assets.

These restrictions make it difficult for other countries to use the yuan as a reserve currency since they cannot easily buy and sell yuan-denominated assets or use them to settle international transactions.

Dependence on Exports

Another factor that limits the use of the yuan as a reserve currency is China's heavy dependence on exports. Because China relies so heavily on exports to drive its economy, it needs to maintain a stable exchange rate in order to remain competitive.

This means that China must sometimes intervene in foreign exchange markets to keep the value of its currency from rising too high, which can make it more difficult for other countries to use the yuan as a reserve currency.

Dominance of US Dollar

Despite these limitations, some analysts have suggested that the Chinese yuan could eventually replace the US dollar as the world's reserve currency.

However, this seems unlikely, given that over 60% of all foreign exchange reserves are currently held in dollars. The size and liquidity of US financial markets also make it difficult for other currencies to compete with the dollar.

Political Stability

In addition to its dominance in global trade and finance, it is unlikely that the yuan will replace the dollar as a reserve currency anytime soon because of political stability.

The United States has long been seen as a stable and reliable country with strong institutions and the rule of law. By contrast, China's political system remains opaque and authoritarian, which makes many investors hesitant to invest in Chinese assets or hold large amounts of yuan.

The Special Status of the US Dollar: Exploring Its Significance

The US dollar is the global reserve currency, and its special status has significant economic and political implications for the United States. Central banks and governments around the world hold large quantities of dollars as reserves, which gives the US government the power to print more dollars to pay off debts and purchase goods from other countries.

Historically, the US government has used this power to influence global trade and politics, often to benefit American interests.

According to some experts, the dollar's status as a global reserve currency is not sustainable in the long term.

Other countries are seeking to diversify their holdings and reduce their dependence on the US economy. Some countries have been increasing their gold reserves in recent years as a way to protect against a potential collapse of the dollar.

Gold has traditionally been seen as a hedge against currency devaluation and inflation.

The Catholic Church, for example, holds significant gold reserves that it uses to support its operations around the world.

Other countries, such as China and Russia, have also been increasing their gold reserves in recent years.

Despite these concerns about the sustainability of the dollar's status as a reserve currency, it remains dominant globally for now. The US government continues to use its power over global trade and politics to benefit American interests.

In order to maintain its position as a global superpower, America must continue to adapt its economic policies in response to changing global conditions. This requires careful consideration of how other countries diversify their holdings and reduce their dependence on American economic power.

One way that America could adapt would be by investing more heavily in education and training programs that prepare workers for jobs in emerging industries such as artificial intelligence (AI) or robotics. These industries are likely to play an increasingly important role in shaping our global economy in the coming years.

What We've Learned About Dollar Collapse

In conclusion, understanding the concept of currency collapse is crucial for investors and individuals alike. While there are fears surrounding the potential collapse of the US dollar, it's important to separate fact from fiction and examine the underlying issues.

We have debunked some common misconceptions about dollar collapse and gained insights from experts like Brad McMillan. The truth is that while there are weaknesses in the US economy, the dollar's dominance is here to stay due to its special status as a global reserve currency.

Investors should assess the potential impact of a currency collapse on their portfolios and consider diversifying their assets. However, it's important not to panic or make rash decisions based on fear-mongering headlines.

Furthermore, while some may argue that other currencies like the Chinese yuan could take over as a dominant global currency, this is unlikely due to factors such as China's closed capital account and lack of transparency.

The Burning Question: Has The Dollar Collapsed?

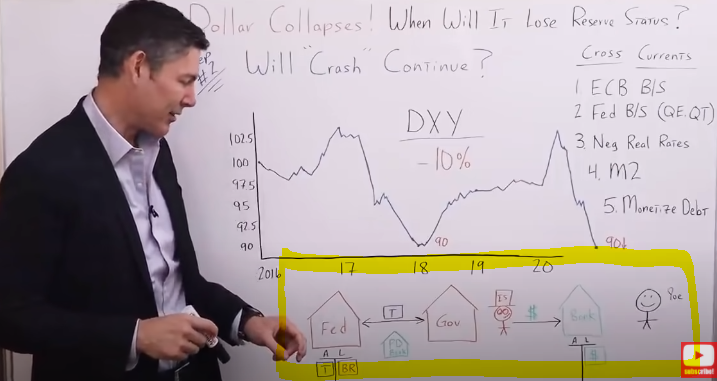

The discussion should not only be whether the dollar collapsed or not, it is critical to ask against what. If you turn on the news or listen to CNBC or Bloomberg, you know the dollar has fallen out of bed.

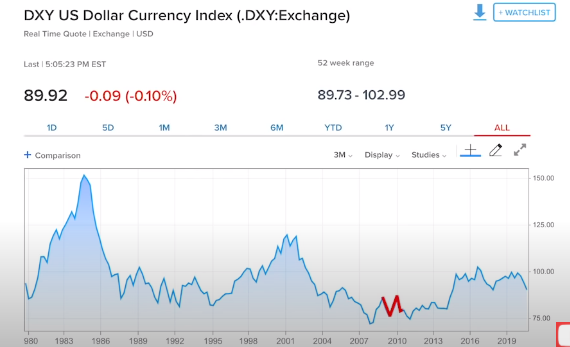

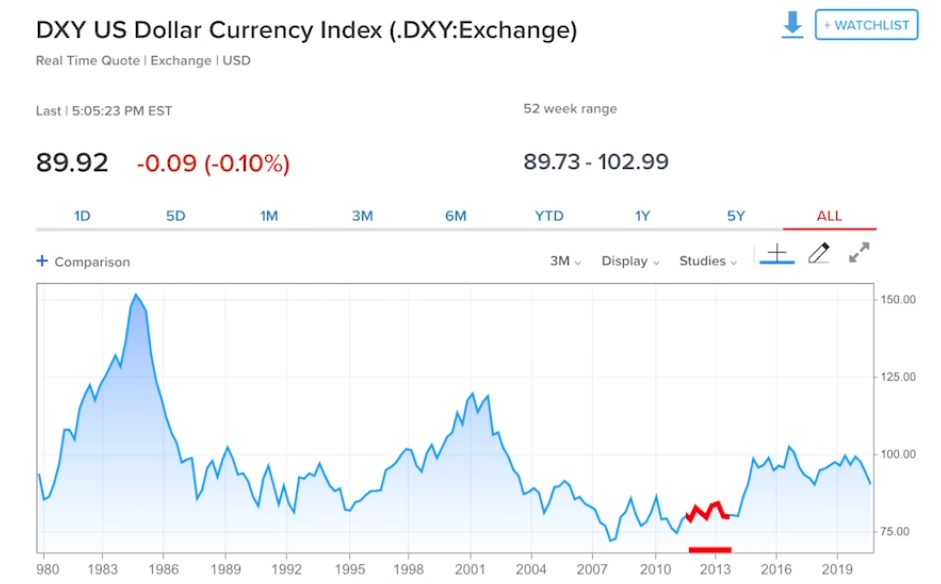

The DXY has gone from 100 to 89, which is huge. Everybody is saying the dollar has collapsed, and it's going to continue to go down from 89. I carefully analyzed what that means and whether the statement -the dollar has collapsed- is accurate.

The Dollar Index Spot (DXY) is a measurement of the dollar against a basket of other Fiat currencies as the Euro. The latter is about 57% of the basket that comprises the DXY.

The chart above displays the DXY from 2016 to 2020. For my initial analysis, I used a five-year timeframe. On the right, it goes from 90 at the bottom, up to 102.5.

In 2016-2015, DXY was right about 100, then went down a little bit, and in 2017 it reached 102.5.

In 2018 it crashed to around 90, slightly increased, and then remained flat until the Covid-19 crisis, where it rose quite high between 110-120, perhaps even 140. We would have needed a Plaza Accord 2.0.

DXY crashed down again after a quick spike due to all the stimulus, quantitative easing, repo market infinity, and everything else the Fed has done. However, I think it's essentially about the Fed monetizing government debt and the new issuance of treasuries.

As of December 2020, DXY dropped below 90, to 89. With everybody saying that the dollar has collapsed, I put it in perspective. It's only gone down about 10% in the last five years.

Would you call that a collapse?

There are other things that the dollar has collapsed against in the past five years, which ironically enough, nobody is talking about:

- Gold: This is first and foremost. The dollar went down around 40% against gold. That means gold went up and the dollar lost purchasing power against it.

- Chapwood Index: My good buddy, Jason Burack, introduced me to it. The Chapwood Index is like Shadow Stats but does a much better job nailing down exactly how much prices have gone up over the past five years in certain cities across the United States. Just as with gold, the dollar fell 40% against the Chapwood Index.

- Housing: We're now at all-time highs, adjusted for inflation, even compared to 2006, the top of the last bubble. Housing has gone up dramatically. In other words, the dollar has lost about 35% or 40% of its purchasing power against real estate.

- Stocks: They've almost doubled in the last five years. The dollar has lost 50% of its purchasing power against stocks.

Bitcoin: Five years ago, it was $200-$300. Today it is worth around $30.000. So, the dollar has lost about 99% of its value against Bitcoin.

The financial media is hyper-focused on the dollar falling out of bed on the DXY. What is crucial to understand is the dollar has collapsed against things that you would want to buy with it: Gold, housing, stocks, Bitcoin, goods, and services.

Will The Crash Of The Us Dollar Continue?

Initially, I took a more holistic approach to answer these questions:

-

Is the dollar collapsing?

-

Against what?

And I think it's crystal clear that in the last five years, the dollar has dropped against everything you would want to buy.

When most people hear about a dollar crash, they're thinking about it through the lens of the DXY, and this is where I want to focus. The dollar is now trading right about 90, or maybe even 89, against the basket of currencies that comprises the DXY.

It is vital to acknowledge that when you look at currencies and their cross rates, there are potentially hundreds or thousands of crosscurrents involved that determine whether or not the individual currency is going up or down concerning other Fiat currencies.

Here are some of the implicated crosscurrents with the DXY:

European Central Bank (ECB): There is “money printing” on their balance sheet because the Euro is almost 57% of the DXY.

Federal Reserve:

- What is the Fed's balance sheet doing?

- How many dollars are being created?

- How much base money, and maybe how much M2 money supply through quantitative easing or quantitative tightening?

Negative real rates: As they have an impact on the dollar and gold, I might add.

M2 money supply:

- How many new currency units in the real economy are being created?

Not just the currency units, but taking it a step further, we have to ask ourselves…

“How many bank deposits or bank liabilities are being created or destroyed in the real economy?”

Monetized Debt:

- Lastly, is the Fed monetizing the debt?

To analyze the crosscurrents above, I examined some graphics, starting with the Fed's balance sheet compared to the ECB.

I went back ten years since the GFC, where the ECB was printing money and the Fed wasn't, or vice versa, which means money, bank reserve, and base money. Then I contrasted that to come to some conclusions regarding what is moving the dollar or the Euro.

In 2008, the Fed's balance sheet took off to try to combat the crisis. It went from $800 billion to about $2.5 trillion. Then it plateaued slightly and went up again during QE2, to flatline in 2012.

Compared to the balance sheet of the ECB, the Fed’s did go up during the GFC, then came back down and remained flat. One could assume the dollar dropped during this timeframe from 2009 to 2012.

However, the DXY chart below shows the dollar didn't go down significantly. It was just more choppy during this timeframe. Although this is a significant crosscurrent, it didn't affect the dollar that much back then. I can't find a correlation.

The same occurs from roughly 2013 to 2014 when the balance sheets were going in completely different directions. The Fed was increasing base money significantly, and the ECB was doing their version of quantitative tightening. One could expect the dollar to go down during that timeframe, but it was pretty flat.

The chart below displays the 10 year Treasury yield adjusted for inflation. I wanted to check if there were negative or positive rates during a specific timeframe.

What stood out the most was the period from 2012 to the end of 2013 with negative real rates. The dollar could have gone down during that span. But the graphic of the DXY shows it was pretty flat.

Gold went up during this timeframe, and it's gone up again now in 2020 when we have negative real rates again. So, the conclusion that I would draw is:

Negative real rates, although they may be a crosscurrent, they do not affect the dollar, the DXY index, as much as they affect the price of gold.

You say to yourself, “Okay, George, so the ECB's balance sheet isn't affecting the dollar too much relative to the Fed's balance sheet, nor our negative interest rates. We're kind of going through this process of elimination.

-

What is affecting the DXY?

And, therefore…

-

What can we focus on how to determine what may happen with the dollar moving forward?

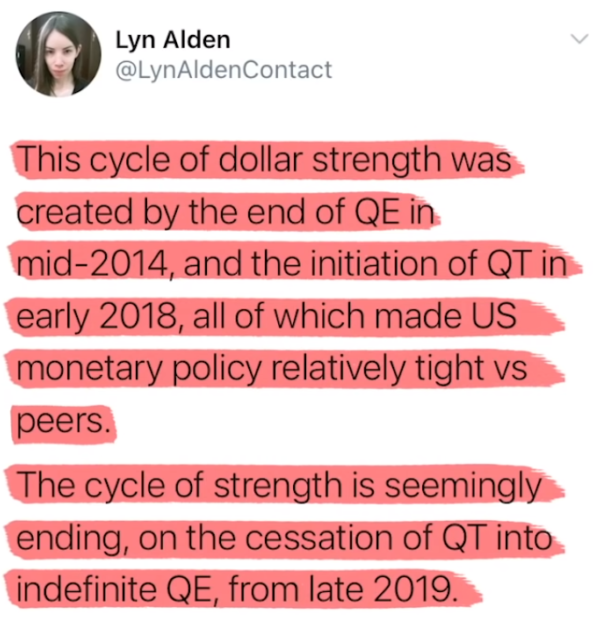

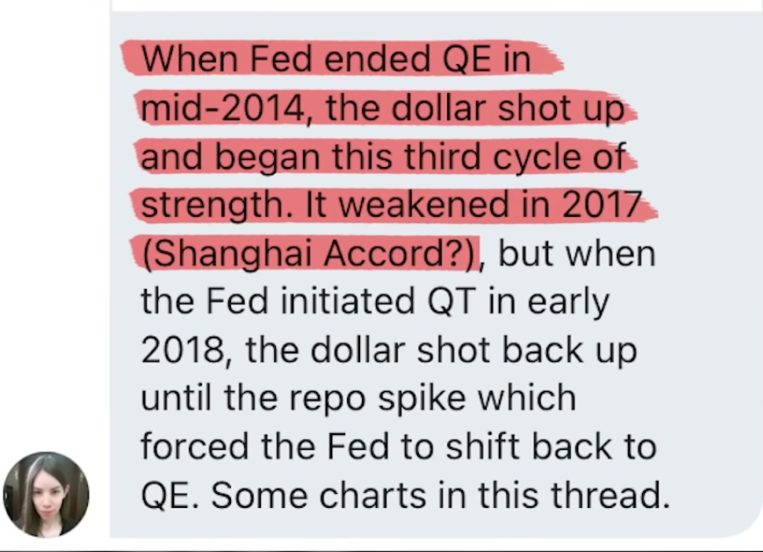

To answer this question, I reached out to my good friend and partner in Rebel Capitalist Pro, Lyn Alden. She is one of the smartest people I know, and she's studied this extensively. Here are her answers straight from Twitter:

That's when we had interest rates spike up to 10% in the repo market, and the Fed had to reverse QT and go back to doing QE. Then she went on to say:

If you don't know what the Shanghai Accord was, it was an agreement in 2016 where they were going to try to devalue the dollar. They, meaning the central banks that were incentivized to have a weaker dollar.

Lyn’s opinion is:

Real rates do matter, but given the global dollar shortage, QE and QT matter even more.

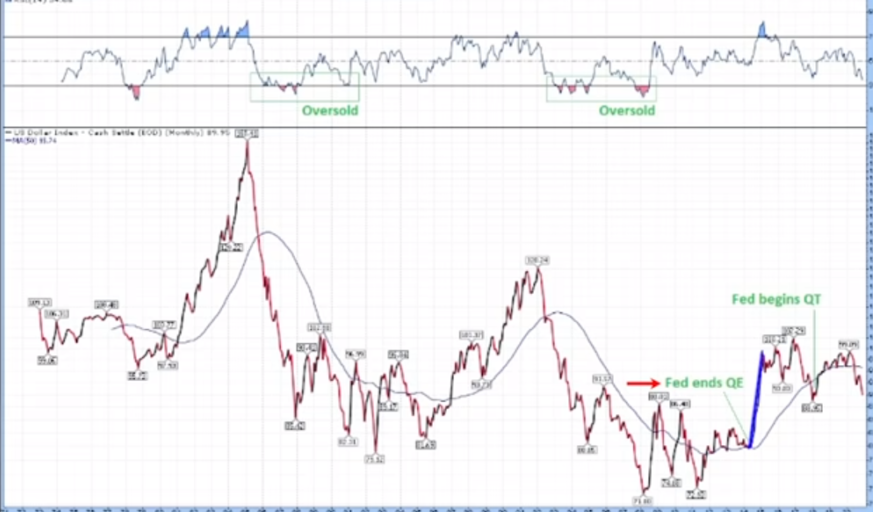

I would add the Fed monetizing the debt while doing quantitative easing matters the most. She also sent me a cart that illustrates her point beautifully:

When the Fed ended quantitative easing, the dollar shot up and plateaued. Then, during this 2016/17 timeframe, when we had the “Shanghai Accord,” the dollar fell out of bed, even below 90.

Then it gradually went back up when the Fed did quantitative tightening. Since then the dollar has come down significantly, back under 90 in December 2020.

I think the key takeaway from looking at those crosscurrents is the main driver for the DXY right now is the M2 money supply.

It has gone up by over 20% in just the last year. Think about that. There are 20% more bank deposits chasing goods and services today than there were just one year ago. This goes back to the Fed monetizing the debt. Let me remind you how that works.

There is the Federal Reserve (balance sheet, assets, and liabilities), the government, and the character named your drunk, insolvent uncle Sam's spending money like the drunken sailor he is.

What does he do to get the money?

He issues treasuries. Normally those treasuries would be purchased by the private sector. They would be taking money out of the private sector, giving it to your drunk, insolvent Uncle Sam, and he would spend it right back into the real economy, so the net effect on M2 money supply would be a wash.

What happens now when the Fed monetizes the debt, those treasuries go directly to the Fed's balance sheet. They're now an asset on the Fed's balance sheet, and the primary dealer banks kind of get in the middle, like a shell game.

The net result is those treasuries go onto the Fed's balance sheet. And to pay for them, they create additional bank reserves in the account of the Treasury, the TGA.

The TGA writes checks against those bank reserves that go back into the real economy, to one of my favorite characters, the average Joe, in the form of a stimulus check.

He deposits that stimulus check with his local commercial bank, which increases the M2 money supply because the government is spending the money into the real economy without taking the money out of the real economy in the first place.

Normally, they would take the money out of the real economy because the average Joe would buy the treasury from your drunk, insolvent Uncle Sam. Then the government would spend that same money back into the economy, redistributing it.

When the Fed monetizes the debt, the treasury goes right to the Fed. They pay for it with newly printed bank reserves, and then those checks go out because the government spends the money.

Instead of it being a net wash, because it first extracted money from the real economy, then added back into the real economy, now all it's doing is adding money into the real economy without extracting it first.

So, the questions you have to be asking yourself to determine what the future has in store for the United States dollar:

-

What are the probabilities the Fed continues to monetize the government debt?

-

What are the probabilities the government continues to run huge deficits?

I would say the probabilities of those two things are extremely high. And if that happens, M2 supply continues to go up. The deposits for liabilities in the commercial banking system continue to go parabolic, and this being the strongest crosscurrent for the dollar, most likely over the long run sends it lower, as measured by the DXY.

What is the end game for the dollar?

When will it lose its Reserve Currency Status?

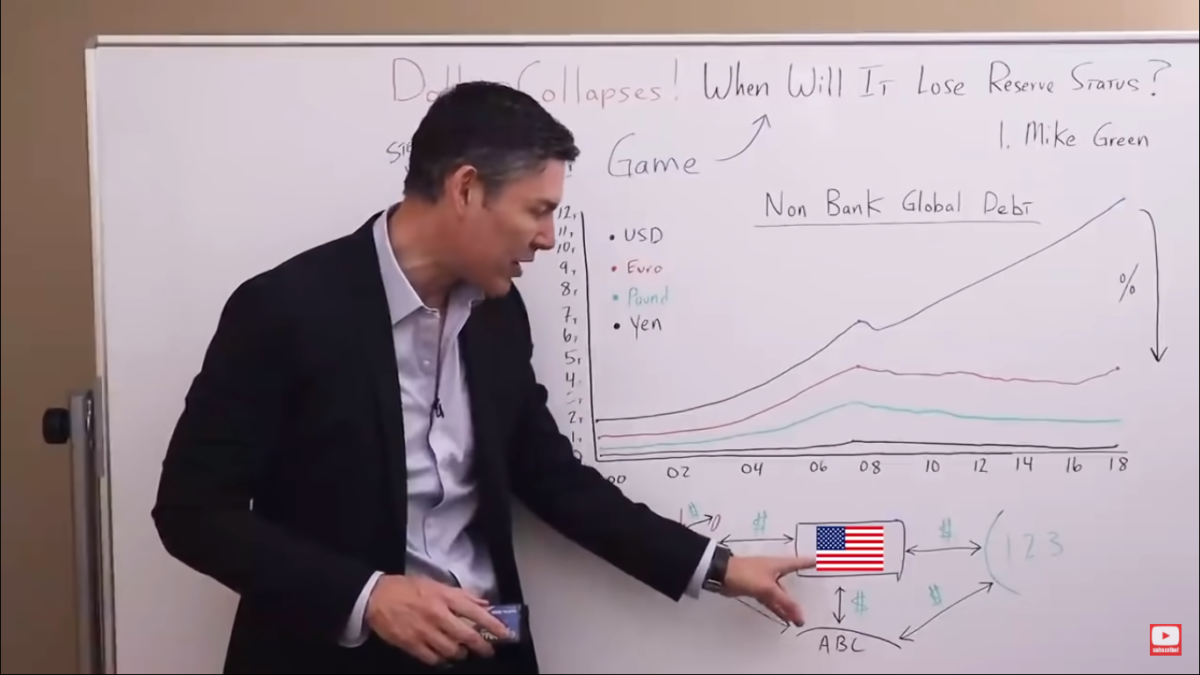

As you can imagine, I can't give you a specific date, but I can give you a chart that I've been looking at.

I think if you focus on this chart and see which direction it's going, it'll give you the information you need to determine if the dollar is in the process of losing its Reserve Currency status.

To get our minds around this, I think we reviewed a clip from Mike Green's most recent Real Vision interview, where he gives us his definition of money:

Money is that which cancels the debt. To the government, that's the form of taxes, on an individual or a private basis, that is debt. If you read a dollar bill, it says very clearly. This is legal tender for the extinguishment of all debts, public or private.

If one of the definitions of money is its use to cancel the debt, and we look at debt denominated in specific currencies, it is visible which of those currencies are being used more or less as money itself.

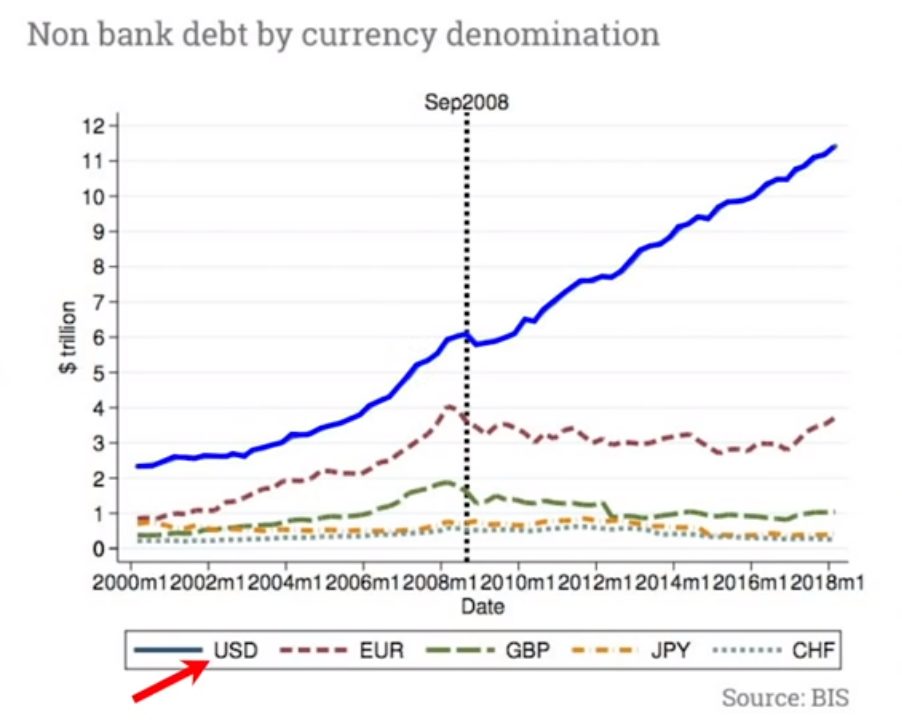

The chart above goes from 2000 to 2018. It is non-bank global debt denominated in four main currencies: United States dollar, Euro, British pound, and Japanese yen.

The blue line is the United States dollar, that's what we should be most concerned with. It went up, peeked out at the GFC, wend down slightly, but then continued on an upward trajectory.

Back in 2000, there was about $2 trillion of global debt. 2018 there was over $12 trillion in global debt, and I imagine it's even higher today. Compare that to only maybe four trillion euros, maybe two trillion British pounds, and under a trillion in Japanese yen.

The chart shows us the dollar is being used to create debt far more than any currency.

Let's think this through. We have the United States, Japan, China, and South America:

Currently, global trade, or the majority of global trade, is done in United States dollars. So, they're paying dollars for goods and services from Japan to China. China to South America, dollars. South America to the United States, Europe down to South America, mostly in dollars.

Nonetheless, the percentage of overall debt in the world, denominated in dollars, tells us the dollar is being used less and less.

If instead of using dollars with transactions, they start to use other currencies, not just one necessarily, the dollar doesn't have to have a replacement. It could happen very slowly by the use of other currencies instead of dollars.

Maybe China starts doing business with South America in Yuan. Or South America starts doing business in Europe in euros, and then between Japan and China, maybe that's done in Japanese yen.

The dollar is being used less. Therefore, the amount of debt seen on the chart above, denominated in dollars, would be going down.

My point is, when the percentage of global debt denominated in dollars starts going down, that's when you know the dollar is losing its World Reserve Currency status.