What Is FedCoin?

FedCoin will be a reality in the coming years. What will happen to paper dollars is simple. It will be banned.

A digital currency gives both the federal government and the Federal Reserve complete control over spending, money supply, inflation, and your life.

If this doesn't sound terrifying to you, then you haven’t thought this through enough.

In this article, George explains what FedCoin is, how it works, how the government will have limitless control, and what life could look like when we start using it.

FedCoin Explained

We’re not talking about Venmo or Paypal.

Many think a digital currency like FedCoin is not a big deal because it's easily assumed to be the same thing as digital dollars in your bank account, or ATM cards, Venmo, and Paypal. FedCoin is a big deal and it is significantly different.

Modern Monetary Theory or MMT will likely be the transfer mechanism used to get FedCoin into your digital wallet. We'll all have digital wallets on our phones and the Fed will deposit FedCoin directly into your wallet. Your community bank will no longer be required.

How FedCoin Will Work

Let's pretend there are only six FedCoins in the system. A fella by the name of Oliver gets three FedCoins and his buddy Fred gets the other three.

Let's say Oliver wants to buy a Paul Krugman book from Fred. Oliver offers Fred one FedCoin for the book. Fred agrees and they trade the book for one FedCoin.

After the purchase is done, the transaction gets recorded on a ledger at the Federal Reserve.

The government is now fully aware of the exchange between Oliver and Fred. Every transaction can and will be tracked and recorded on the government's own blockchain or master ledger, similar to a cryptocurrency. Every transaction will have a unique and traceable serial number.

The main difference between digital currency and the digital dollars we use today is that every transaction can be traced, which gives the Fed and the government far more power than just being Big Brother.

What FedCoin Will Do To Bank Reserves

Currently, when the Fed does Quantitative Easing (QE), they create bank reserves. When FedCoin becomes a reality, they can replace bank reserves with FedCoin.

The Primary dealer banks will likely have digital wallets as well. They'll receive specifically programmed Fecoin that behaves like bank reserves. You too will receive specifically programmed FedCoin based on your own individualized monetary policy.

For example, let’s say the Fed allocates a specific amount of Fedcoin/bank reserves to green energy, shale oil production, or politically correct mortgages.

So any primary dealer or bank under the Fed’s umbrella would have additional reserves that they could lend against those reserves.

How A Politically Correct Mortgage Loan Could Work

Let's say there’s a lady named Kaitlyn with a high social score, wanting to buy a house from Steve.

Kaitlyn fits a politically correct category. And a certain number of Fedcoins have been allocated for circumstances that fit the needs of people like Kaitlyn.

Kaitlyn goes to her local bank and asks for a home loan of $100,000.

The bank runs Kaitlyn through a government database and discovers she is the perfect candidate for these specially programmed fedcoins that will help her buy Steve's house.

The bank gives her the loan, and the transaction is recorded on the government blockchain.

The commercial banks would still be in charge of creating additional money supply in the real economy, not with electronic dollars, but with Fedcoins.

Today's Dumb Dollars

The electronic dollars we use today are dumb.

Like a scoreboard at a basketball game, today's dollars are agnostic when it comes to purchasing power. You can buy anything with today's dollars, so as long as you have enough of them.

FedCoin is more like a video game. This currency can be programmed to work for specific use cases. Every transaction is traceable.

Think about this. Imagine having 100,000 fedcoins in your digital wallet, and the only thing you could use it for is buying a house. You can't buy a car with it. You can't grocery shop with it.

Now, this makes sense for a house. You wouldn't take out a home loan and go grocery shopping. The bank wouldn't allow it.

But hopefully, you can see how a programmable digital currency could potentially manipulate social habits and spending behavior.

FedCoin And Its Limitless Control

If we get to the point where the government officially has FedCoin, then we’ll have to assume they'll ban cash.

Not only is it inevitable but imminent.

Will They Ban Cash?

To understand why they would ban cash, we need to understand the Fed and the government's objectives.

Their goals are to keep asset prices high and interest rates low.

Both the federal reserve and the US treasury should be considered one entity at this point. They won't admit it, but it's obvious.

Their main objective is to keep inflation high along with sovereign, state, consumer, and corporate debt. Which are all at all-time highs.

The Fed believes the best way to get rid of massive amounts of debt is to inflate it away.

How The Fed Determines Future Inflation

To determine future inflation the Fed uses three metrics:

-

The Fed's balance sheet

-

M2 Money Supply

-

Velocity: How quickly money circulates in the real economy.

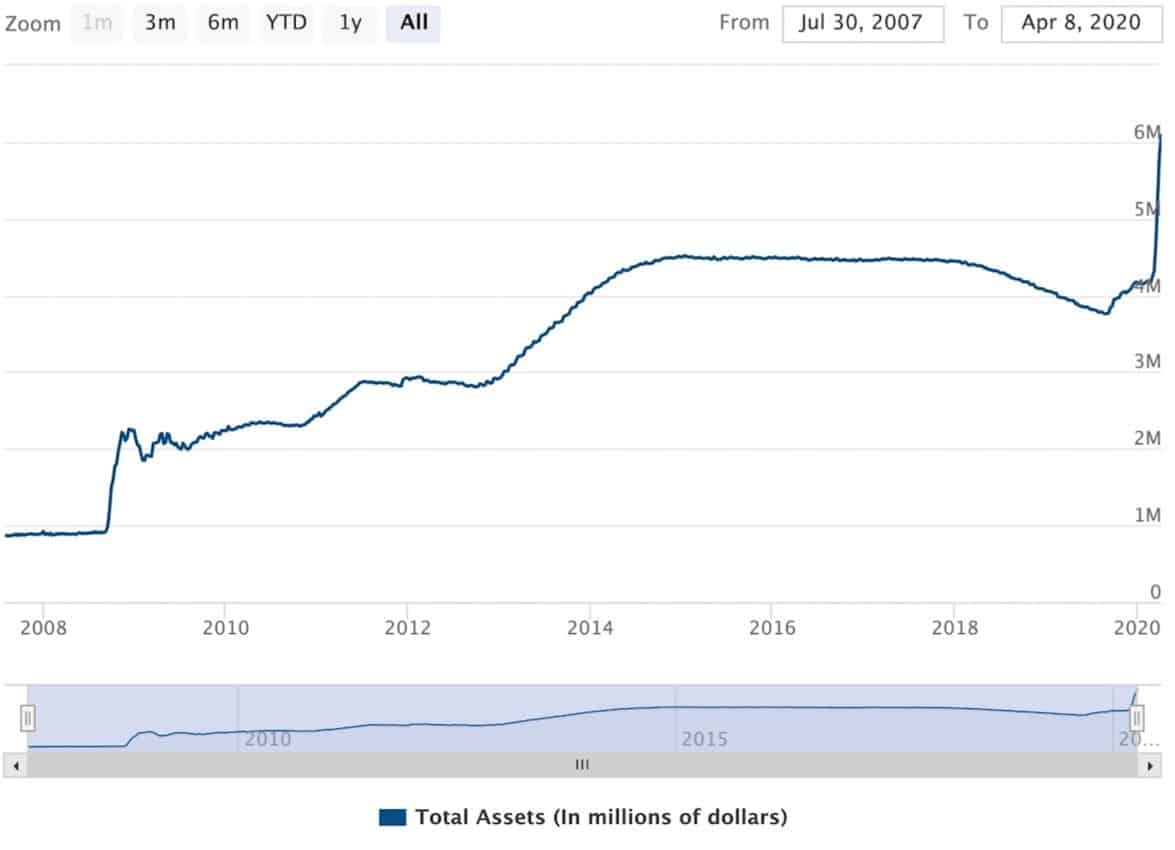

1. The Fed's balance sheet

Currently, they have total control over this metric. So from now on we can look at the Fed’s balance sheet and call it “the hockey stick” because it’s going vertical, as you can see in the image.

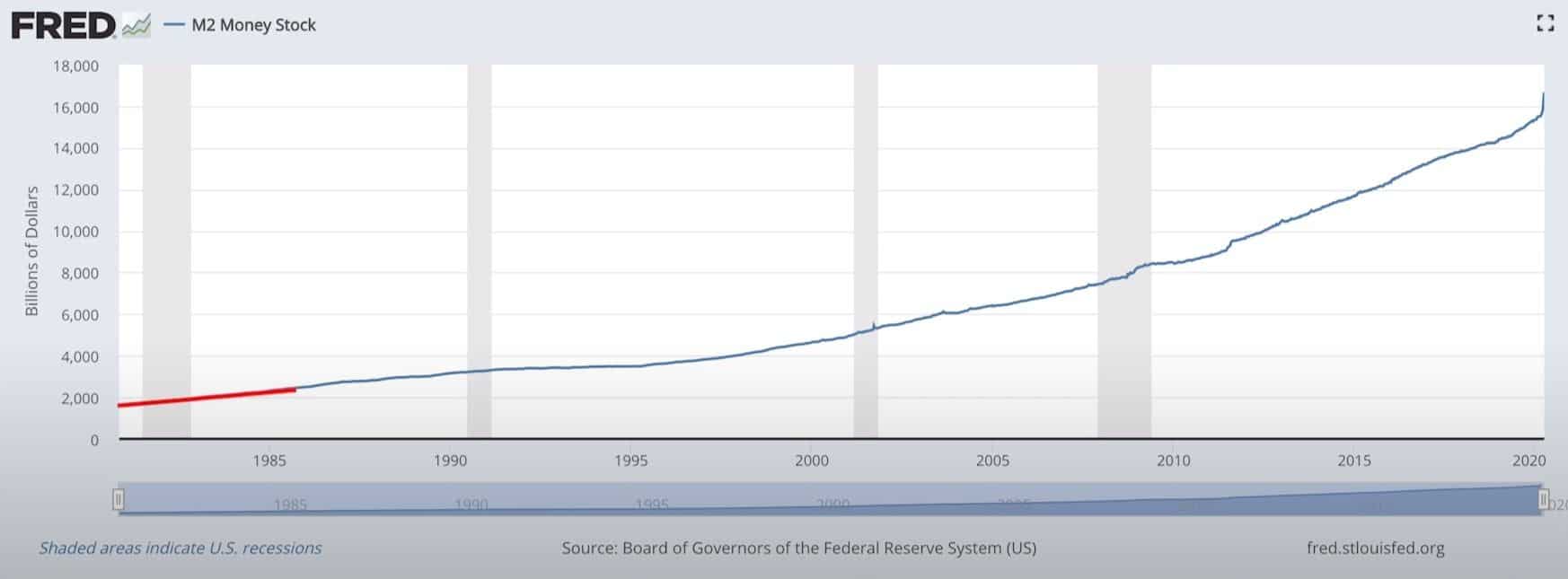

2. M2/Broad Money In The System

The curve starts out rather flat until 1995.

In 1995, the curve begins a new trajectory. Notice in 2008, during the Great Financial Crisis, the curve begins going parabolic.

Yet, this is nothing compared to what’s been happening in the last month.

The Fed's balance sheet has moved up by almost a trillion dollars in four weeks.

To add context, it took six years from 1980 to 1986 to move up a trillion dollars.

3.Velocity: How quickly money circulates in the real economy.

Around the late 70s, velocity was very consistent. Moving up and down between 1.6% and 1.8%.

Then it flatted out. But once we got into the late 70s, when inflation got out of hand, velocity started spiking.

So Volcker came in, jacked interest rates to almost 20%, and velocity decreased.

But then in the 90s, it went through the roof.

Velocity peaked out a little after 1995 and since then it has done nothing but go straight down to where we are today at an all-time low around 1.4.

With FedCoin, the Fed will have control over all three inflation metrics.

They would have the power to guide spending in the real economy and control the amount of credit that goes into the system.

But more importantly, who is the credit going to?

Cantillon Effect Power Grab

If they can control the credit in the real economy, it means they can control the M2 money supply and the Cantillon effect.

The Austrian Economics Center explains what the Cantillon effect is.

“The so-called Cantillon effect describes the uneven expansion of the amount of money. If a central bank pumps more money into the economy, the resulting increase in prices does not happen evenly.

The Austrian economist Friedrich August von Hayek compared this monetary expansion with honey. If you pour honey into a cup, it won’t spread out evenly. It will clump in the middle of the cup first before spreading out.

Same with money: in case of a monetary expansion, the ones who profit from it are the ones who are close to the money. “Close to the money” in this case means everyone who can access the money right at the beginning, i.e. big companies, banks, etc. They get loans and make investments. Prices then start to rise even though the rest of the population has not received any of the new money yet. This part of the population usually is not the one with too much money. Nonetheless, they have to pay the higher prices even though they have not profited from the increase in money at all. And they will never profit from it in the same way as the ones who received the money first. The result is a redistribution from the poor to the rich.”

Does this sound familiar?

Keep in mind the gentleman that came up with this concept was an economist in the 18th century.

It's just as true today as it was back then.

You may think this new FedCoin idea sounds good because technically, money isn’t hitting the big banks and corporations first, which does nothing but drive up asset prices, creating economic bubbles.

You would think the new FedCoin fiat currency would get straight to the people who need it most.

But George sees it differently.

FedCoin Could Make Political Corruption Worse

George thinks politicians and bankers will take this newly forged power and reward people who are politically connected.

Think about all the special interest groups, big corporations, big banks, and whoever else is rubbing elbows with powerful politicians.

So it would get more corrupt than it is now.

It will be easier to get Fedcoins into the digital wallets of those who have political connections first.

And once those entities spend the coins, then it trickles down into the real economy to all of us peasants.

By then, prices will have shot up and the average income will always lag behind.

Velocity Of Money Manipulation in A FedCoin Economy

Also, let's not forget big government would now have a way to control velocity in the economy.

George discussed this on an interview he had on infowars.com. Here's what they said…

Info wars: “Especially when you combine politics and economics, something like a digital currency fits within what the state would want, because it empowers them to an extraordinary degree, and they could have every justification for it.

In fact, their current currency problems that are about to be accelerated over the next year would particularly be the pretext for a solution. They would be like hey! What do you think about those ideas, is there a possibility of that occurring? And how much of that is a risk versus a national digital currency?”

George definitely thinks it's a possibility because, to infowars.com point, FedCoin gives the government so much control. Both taxation and control over interest rates.

Spend it or lose it!

George sees this playing out. Not only with negative interest rates but also with a timer on every single Fed coin.

Think about it, let’s assume every single American gets a thousand Fedcoins per month on the condition they have to spend it all by the end of the month.

So there would be an expiration date on each coin, and if we don’t spend them fast enough, they expire and disappear.

If velocity was too low, then all they would need to do is adjust the expiration date so the coins expired sooner.

They could literally force people to spend their Fedcoins immediately in an effort to increase the velocity of money.

Increases in velocity will also increase the rate of inflation.

Comments are closed.