Is money printing set to explode? The short answer is yes. I don't even think most people understand the magnitude of how much it's going to explode.

But, what I find is most people really don't understand what money printing actually is. They don't even understand money, loans nor QE.

So before you can figure out how money printing is going to affect your financial future, you have to understand how the QE that the Fed does with the banks' works.

I'll explain it to you in seven simple steps in the form of a series of articles named: Is money printing set to explode? This is part 3 of 7.

The Fed Does QE With The Commercial Banking System

I'm going to start to get into the process that most people would define as money printing. We all know what QE looks like.

-

But is this process in and of itself inflationary?

-

Is it creating more deposits in the real economy, chasing goods and services?

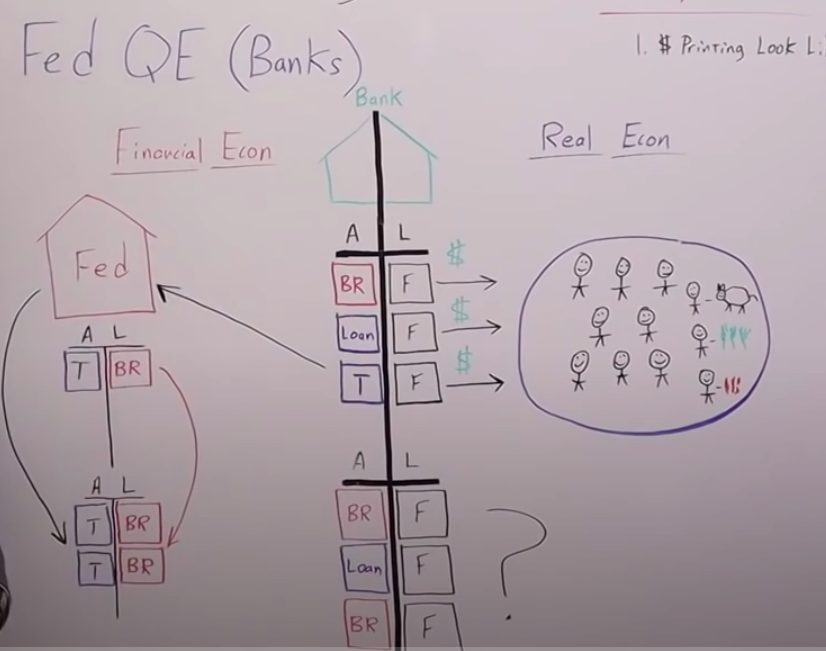

I'll answer that question right away. Take a look at the whiteboard.

I wanted to be very specific and draw a line between the financial economy on the left, and the real economy on the right. Because what we're concerned with when we think about money printing is whether or not it's going to create consumer price inflation.

That's what most people are thinking about when they're trying to get their heads around money printing.

I want there to be a defined line in the sand. This is the way I want you to think about it. And the bank really sits right in the middle. They kind of straddle.

They have one foot in the financial economy and one foot in the real economy. Their balance sheet is split.

The assets are in the financial economy, but the deposits, the liabilities, the Fugazis, the IOUs are in the real economy because those represent the currency units that are available to chase the goods and services in the real economy like cattle, corn, and maybe wheat or whatever those things are. They're goods and services in the real economy, trust me.

When the Fed does QE with a bank, what happens is the bank sells them a treasury or mortgage-backed security.

In this case, we'll assume it's a treasury that is an asset on the bank's balance sheet, but then goes to the Fed.

After that, it goes onto the Fed's balance sheet. Just to back up a little bit, as you can see, on the left, the Fed started having one treasury and one bank reserve on their balance sheet.

The treasury is an asset and the bank reserve is a liability.

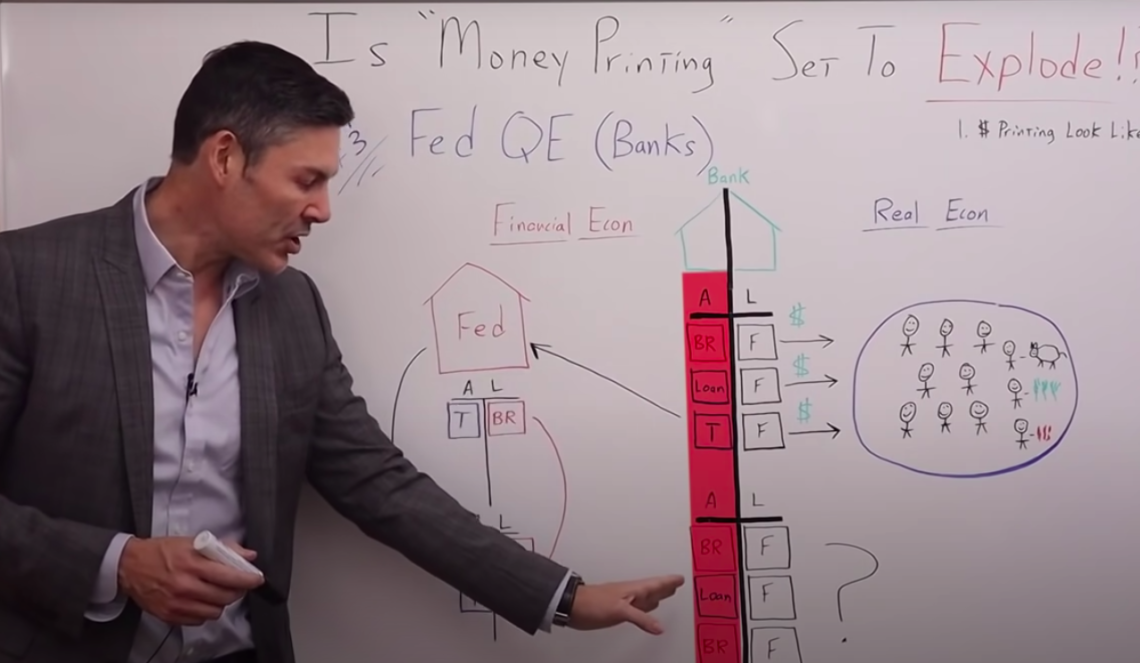

Again, they buy the treasury from the bank that gives them an additional treasury, and then they “print” money out of nowhere. It's just really electronic digits in a computer.

They create more bank reserves to pay for the treasury they just bought from the bank. Where it gets really weird is when you can see there is just as much of a Fugazi on both sides.

I don't even want to go down that rabbit hole, so let's just focus on Fed quantitative easing in the banks right now.

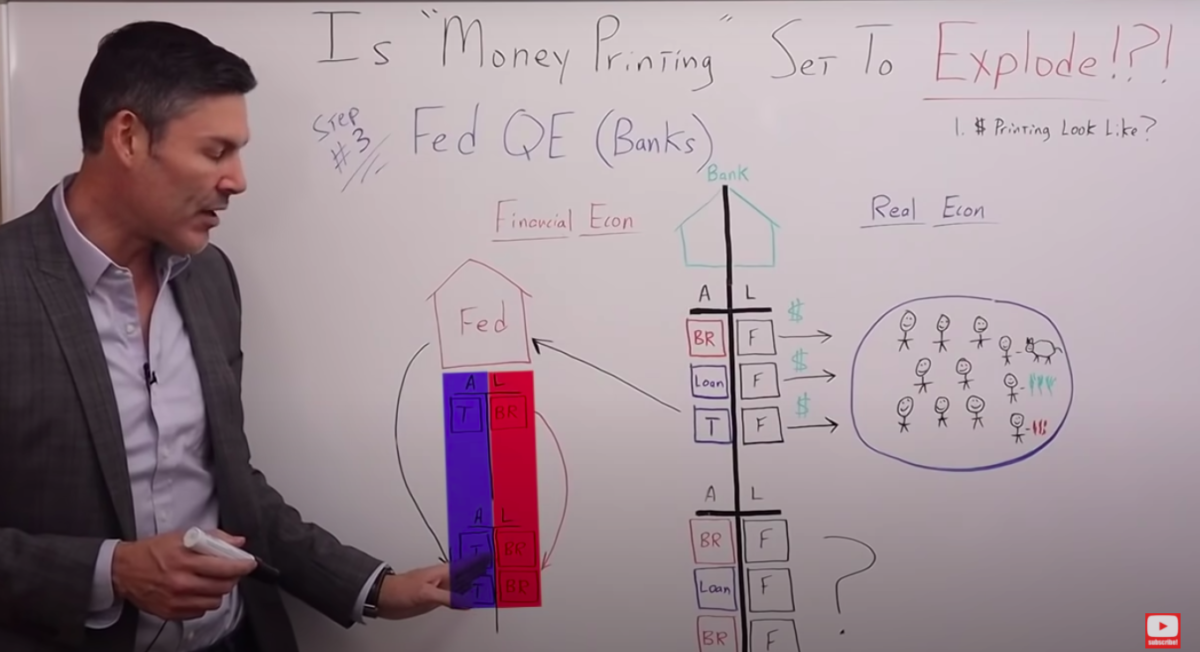

The balance sheet of the bank started with bank reserves alone and treasuries. Now, they have the bank reserves they started with, the same loan, but they have additional bank reserves that the Fed paid them for this treasury.

So the treasury goes to the Fed, onto their balance sheet, they print up the funny money, and give the bank more bank reserves. So the bank reserves now basically trade.

That's why they call it an asset swap. They traded the treasury for additional bank reserves.

Think this through.

What did that do to the liabilities, to the deposits in the commercial banking system?

That's what we need to be concerned with.

Did it increase the amount of currency units available to chase the goods and services?

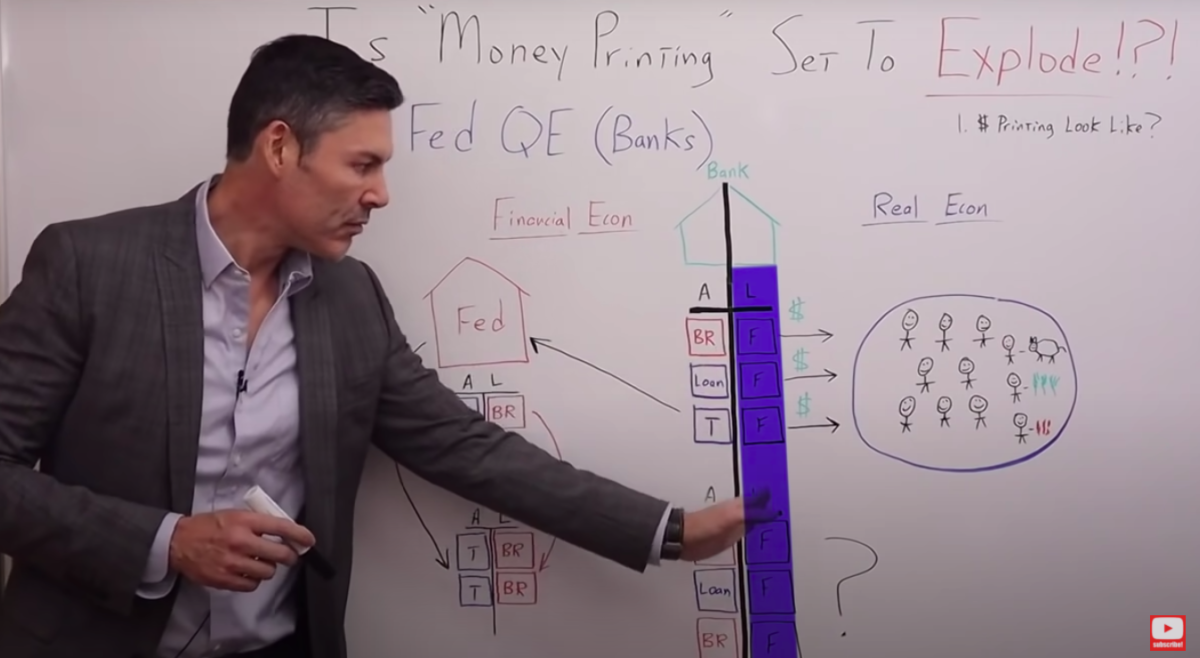

The answer is no, it didn't. The Fed could buy a quadrillion dollars worth of mortgage-backed securities or treasuries or assets, even loans for that matter, from the banking system.

But the only thing that would change is the balance sheet in the financial economy: The asset side of the bank's balance sheet and the liabilities side, and the assets side of the Fed's balance sheet.

It wouldn't directly affect the deposits in the commercial banking system or the amount of currency units available to chase the same amount of goods and services.

In other words, this process in and of itself isn't necessarily inflationary.

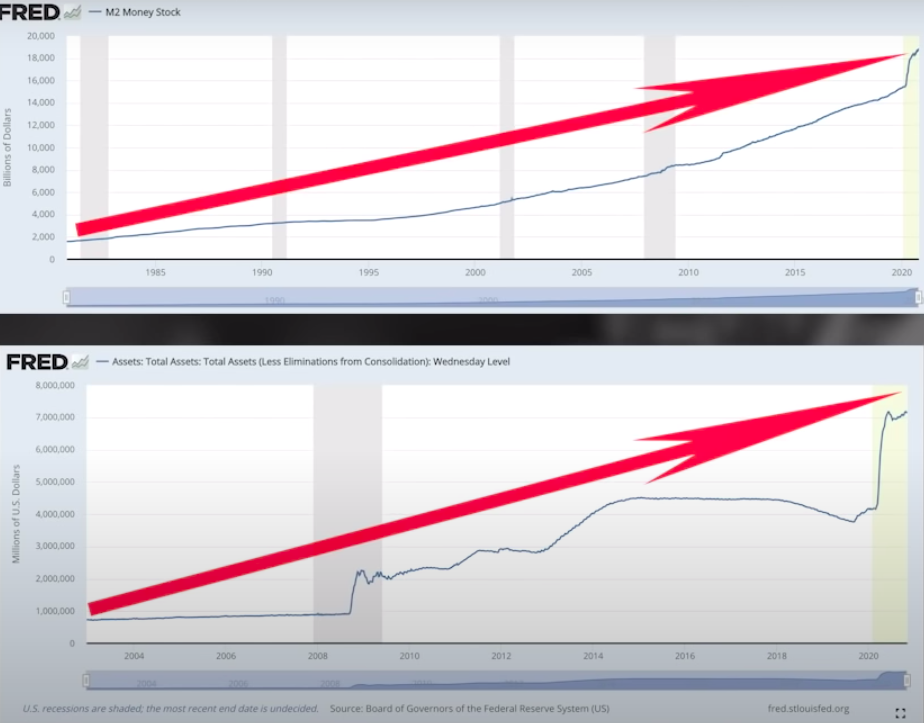

To give you an example of this, let's cut to a chart of the M2 money supply.

We know the Fed started quantitative easing in 2008. They did quantitative easing one, two, three, and four, which was called not QE.

They wouldn't admit to it, but if we can focus on the timeframe between 2008 and say 2018, those 10 years the Fed was doing quantitative easing with the banking system, you can notice, the M2 money supply really didn't spike. It just went up gradually.

This is showing us that although the Fed took their balance sheet up to $4.5 trillion from $800 billion, meaning they created an additional $4 trillion almost worth of bank reserves, it didn't have a direct relationship with the number of currency units that were in the real economy chasing goods and services.

This becomes clear when we compare a chart of the M2 money supply with a chart of the Fed's balance sheet.

Although they both go up, that's where the similarities end. For those of you really paying attention, you'll notice M2 money supply does go parabolic in 2020.

I'll address that in one of the future steps.