To predict the future of pretty much everything, you need to answer this question in your own mind: Will we have inflation or deflation? When I'm talking about the future, I'm talking about the dollar, stocks, bonds, gold, real estate.

There's a huge debate around the effect quantitative easing has in the system: Does it produce inflation or deflation? To answer that question I'll explain what the two main voices on FinTwit say about it.

In this article, I explain how you can see what's ahead, but because this is part of a mini-series, I encourage you to read the first part by clicking here. This is part two. I'll start right off with step number three, or the third approach where I express my personal opinion.

Understanding The Fed's IOUs

In the first article I did for this series, I asked if bank reserves were actual spendable cash.

-

Are they fungible?

-

When the primary dealer banks go to the government to buy their treasuries at auction, are they using bank reserves to do so?

There was a mix of opinions. We had Brett Johnson and Steve, the bond King on one side, and Luke Gromen and Lynn Alden on the other.

Now, I want to take it a step further and give you my opinion. Quite frankly, I think that we are all asking the wrong question.

Our focus shouldn't really be on the bank reserves, the cash, and if they're able to buy bonds or assets with these bank reserves. But more so, on understanding the difference between the liabilities in the banking system, the IOUs, and the IOUs on the Fed's balance sheet.

Let me explain. It goes back to the main keys that we need to focus on to understand the main question: Will we have inflation or deflation?

Remember the 3 keys are:

- The amount of currency units.

- How quickly those currency units are circulating.

- How many goods and services they're chasing.

That's what's going to determine if consumer prices are going up or down.

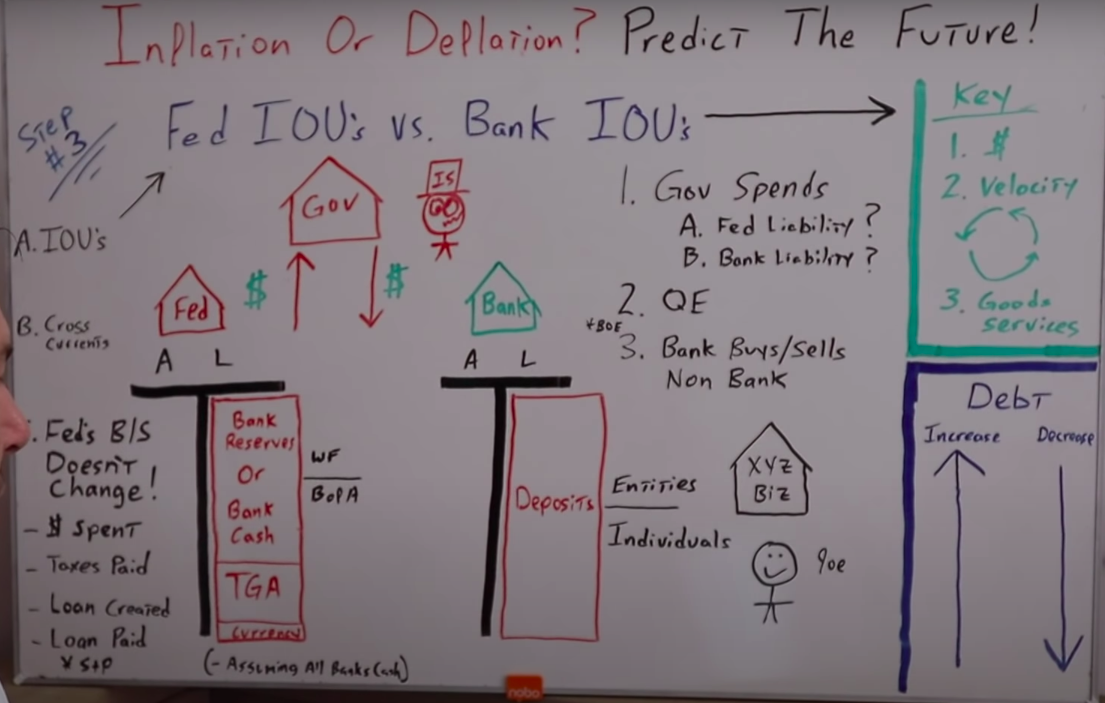

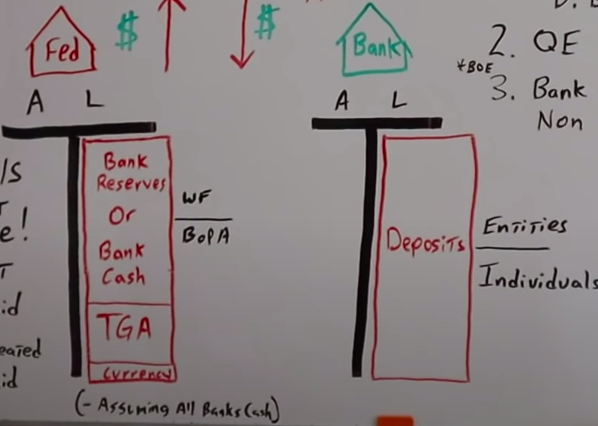

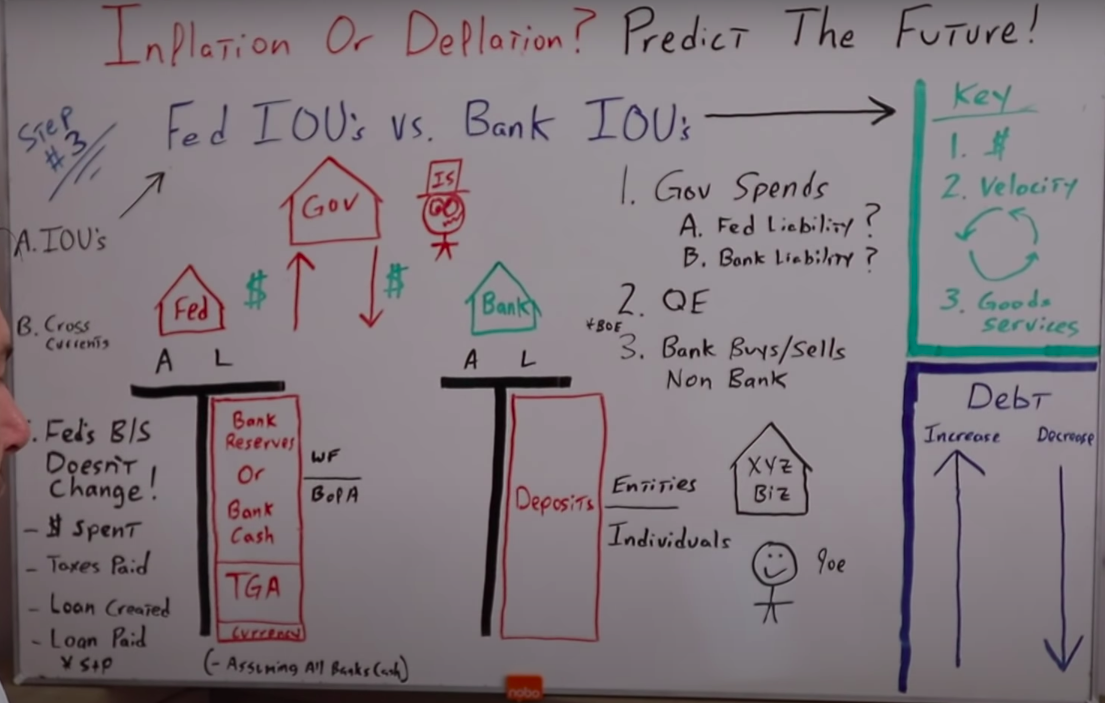

Let's look at two balance sheets.

On the left side, we have the Fed represented in the red little house, and in the middle, we have the commercial banking system in the green house.

We'll just assume that the Bank’s balance sheet is an aggregate total of all the balance sheets of all the banks in the real economy and, just to be clear, the liability(L) side of the bank are deposits, but those are actually IOUs to the entities and individuals that hold those accounts, just like businesses, and you and I, the average Joe.

It really doesn't matter what bank you have your checking account with, whether it's with Wells Fargo or BofA, if your account was a box and you looked into it, it would be completely empty. There's nothing in there, there's zero.

Every single time you get your bank statement or you go to an ATM and it shows your account balance, that isn't how much is actually in your account, that's how much the bank owes you.

Think about that next time you set up a bank account. That bank isn't holding your money, they're taking your money and they're giving you IOUs.

How much do you trust the entity you're giving your purchasing power to, and giving you an IOU back?

I don't want to go off on that tangent, but it's something to think about. Just like the banking system's liabilities are deposits to everyday people and businesses, the Fed's liabilities are deposits or IOUs to the banking system.

In other words, any of the banks under the Fed's umbrella, like Wells Fargo or BofA, their checking accounts or their deposit accounts, is with the Fed.

Whether they're bank reserves or cash, like we discussed in the last article, they're still liabilities of the Fed. They're still IOUs to the banking system.

There's a big difference between the bank’s IOUs to the entities and individuals in the real economy, and the Feds IOUs to the banking system. Remember it's all about velocity, so let's think this through.

The deposits on the liability side of the bank are being spent daily, the individuals and entities are going to Home Depot, Chipotle, and the grocery store. They're paying rent, and buying cars.

The money is out there circulating in the economy at a much higher velocity than the liabilities held at the Fed.

-

How many of the banks are going to Chipotle for lunch?

-

How many of the banks are going to Home Depot to buy nails or glue?

-

How many of them are buying new cars? Not many.

Again, my point, the takeaway that you have to understand is:

The liabilities in the banking system are moving at a higher rate of speed. There's higher velocity than the liabilities or the IOUs, from the Fed to the banking system.

If we're trying to figure out whether the future is inflationary or deflationary, we have to get hyper-focused on what's happening to the deposits in the banking system.

Are they increasing or are they decreasing?

I'm going to walk you through a bunch of scenarios so you can start thinking about this on your own.

One more thing I want to mention is that the Fed's BS doesn't change. You could be saying to yourself, “George, I know that. The Fed's always full of BS.” But I'm talking about the size of their balance sheet.

It doesn't go up or down. So the IOUs, the deposits held at the Fed, are almost always the same unless the Fed buys or sells assets, like treasuries or mortgaged-back sausages.

It's very crucial you understand this. To get your mind around it further, let's look at some data.

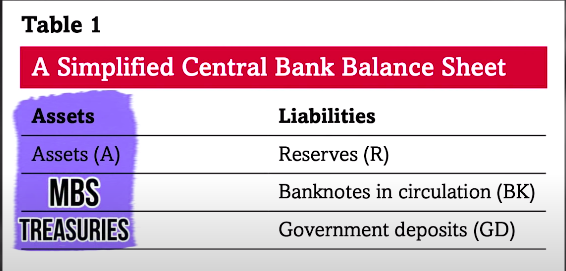

This is from a Standard & Poor's article entitled: “Economic research. Repeat after me: Banks cannot and do not “lend out” reserves.”

I'm not going to review that too extensively, but what is helpful is they give us a very simplified central bank balance sheet.

On the asset side, we have mortgage-backed securities and treasuries, I talk about those all the time.

Then, on the liability side, there are bank reserves and banknotes in circulation, that's hard currency, and also government deposits. That's the treasury general checking account.

There are only three things that can affect this balance sheet:

1. The central bank increases or decreases its assets. That means, buying or selling financial assets like mortgage-backed sausages and treasuries.

- The public could decrease or increase the amount of cash, hard currency, banknotes it wants to hold.

If the public didn't want to hold cash anymore and they gave it all back to the Federal Reserve, since that's an IOU, their balance sheet would decrease.

If for some reason, everyone wants to use cash, which I think would be great, then the Fed would have to create more cash, and therefore, a liability of the Fed. That would be an increase in their balance sheet.

- The government reduces or increases its deposits at the central bank. Which is the TGA that we talked about, because it makes net transfers to, or receives net transfers from the private sector.

Net transfers are just a fancy way of saying the government is getting money by either taxes or selling treasuries. But I want to point out that although the three affect the amount of bank reserves in circulation, it does not affect the size of the Fed's balance sheet.

Even if the government spends all of the deposits in its account, those deposits don't go away. They just get transferred from the TGA, which is a liability of the Fed, to the banking system which also is a liability of the Fed.

The Fed's balance sheet does not change in size. The main takeaway is: The only thing that changes the size of the central bank's balance sheet is the central bank themselves selling or buying assets, or, more or less currency in circulation.

Take a second look at the whiteboard.

What would happen if money was spent in the economy?

On the right side of the board, if Joe goes to business XYZ and buys a hundred dollars worth of stuff, and his bank is BofA, but the business bank is Wells Fargo, the only thing that would happen is the hundred dollars of digital units of measurement held on the Fed's balance sheet, the liabilities of the Fed, would go from BofA to Wells Fargo, but the size of the balance sheet wouldn't change.

Let's take it a step further.

What if taxes are being paid?

Joe owes taxes to the government, to your drunk insolvent uncle Sam. He owes him a hundred dollars. The same thing. The digital units of measurement would go from BofA's account, down into the treasury general.

It's just a transfer of a hundred units of measurement from BofA to the TGA. The overall size doesn't change.

Now, what if a loan is created?

We know that creates additional deposits or additional bank liabilities in the real economy, chasing goods and services.

So if Joe takes out a loan from BofA to buy a house for a hundred thousand dollars, and goes and pays the seller, but the seller banks with Wells Fargo, the only thing that would happen on the Fed's balance sheet is a transfer of a 100,000 of the digital units of measurement from BofA to Wells Fargo.

It's just a transfer, and the overall size in aggregate total remains the exact same. I think you get it. I've beaten the dead horse.

Now, here I provide some examples where you can get hyper-focused on what's happening to the IOUs that really determine if the future is going to be inflationary or deflationary.

What happens when the government spends money?

They take taxes or currency units out of the system when they sell bonds, then they go ahead and spend that money in other places.

Well, we have to start by answering the question.

Is that a deposit of the Fed or is it the deposit of the banking system?

Because the deposits in the banking system are going to have a higher velocity.

If the taxes are being paid by Wells Fargo, they're going to your drunk insolvent uncle Sam. That's just on the Fed's balance sheet. It's just going from Wells Fargo to the TGA.

But, when the government spends the money, they're spending it into the real economy, which increases the amount of deposits in the commercial banking system. So, on net balance, the deposits increase.

What happens if originally, the deposits came from the banking system itself?

Well, then it's a net wash.

Because the hundred dollars that are being paid in taxes are going from the bank’s deposits to the government, and then right back to these banks deposits, you see how that's a net wash.

But, if the deposits are coming from the Fed, then the increase in deposits in the commercial banking system is a net increase.

What about quantitative easing?

That's what we talked about in the last article. It really depends, if the Fed is buying the assets from a non-bank, meaning, the average Joe or a business or a bank that has an account with the Federal Reserve.

Let's think this one through. If Wells Fargo has a treasury, the Fed buys the treasury from them, the only thing that happens is, additional reserves go into Wells Fargo account.

Then the size of the Fed's balance sheet would increase, but nothing happens on the deposits on the commercial baking side, because it's a transaction from a banking entity with the Fed.

But, if the Fed buys those treasuries from XYZ business, now, the treasury goes from their balance sheet over to the Fed and the Fed increases the deposits for XYZ business.

Do you see what's happened?

What happens to the deposits in the commercial banking system?

They increase, right?

If they're selling a treasury worth $100 to the Fed, then they have to be compensated somehow, it has to go into their deposit account.

In essence, what they're doing is they're trading treasuries for an increase in their deposit account of $100.Let me say it again, just to be very clear.

If the Fed is doing quantitative easing with the banking system, it does not affect the deposits in the real economy. But if the Fed is doing quantitative easing with entities or individuals, meaning they're buying those assets from entities or individuals, then it is increasing the deposits in the commercial banking system or in the real economy, chasing goods and services.

To take a deeper dive into how this works here is the Bank of England's 2014 report on how money is created.

The link between QE and quantities of money: QE has a direct effect on the quantities of both base and broad money because of the way in which the bank carries out the asset purchases. The policy aims to buy assets such as government bonds, mainly from non-bank financial companies.

So, that would be the average Joe or business XYZ on our whiteboard example.

The definition continues:

…Such as pension funds or insurance companies. Consider for example, the purchase of one billion in government bonds from a pension fund, the pension fund does not hold reserve accounts with the Bank of England, the commercial bank with whom they hold a bank account is used as an intermediary.

The pension fund's bank credits the pension fund's account with one billion of deposits. In exchange for the government bonds, the Bank of England finances its purchases by crediting the reserve to the pension fund's bank.

-Bank of England, 2014

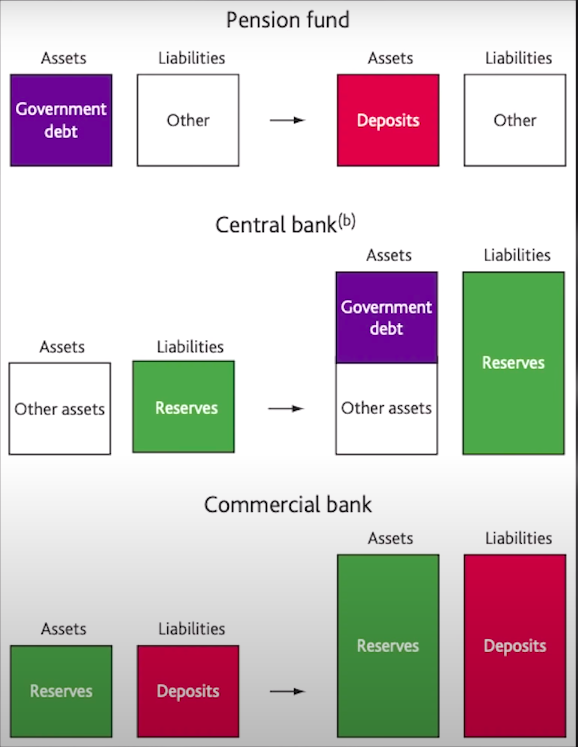

Let's check out this diagram. We have the balance sheet of the pension fund, the central bank, and the commercial banks involved in the transaction.

The government debt starts off as an asset on the pension fund's balance sheet, which they sell to the central bank.

So, it goes onto their balance sheet as an asset. Then what happens with the commercial bank, is the central bank credits their account by an additional billion dollars.

Their reserve account grows by a billion dollars. Then the commercial bank credits the account of the pension fund by the same one billion dollars.

The reserves increase by a billion. The deposits increase by a billion, and the government debt goes from being an asset of the pension fund to an asset of the central bank.

The key here is to notice the deposits in the real economy have increased, but that's because the central bank, in this scenario, purchased the assets from a non-bank entity.

If they would have purchased the assets from the commercial bank themselves, the only thing that would have changed is the amount of reserves. The deposits in the real economy would not have changed at all.

The third thing that really affects the amount of deposits in the real economy, chasing goods and services, is if a bank buys or sells an asset to a non-bank.

So, the bank owns some treasury (T), they want to sell it to Joe, and Joe gets it. If that happens, it goes from the balance sheet of the bank onto Joe's balance sheet, but then the deposits would decrease because Joe has to pay for the treasury he just purchased.

The bank's liabilities, their IOUs to Joe would decrease by the amount of the treasury, let's say, a hundred bucks.

Their IOUs to Joe would decrease by a hundred dollars, they'd owe Joe a hundred dollars less than they did before and their asset would go from their balance sheet to Joe's balance sheet.

The opposite would happen if Joe sells a treasury to a bank. If Joe has the treasury initially, it would go to the bank's balance sheet and then the bank would add another deposit for a hundred dollars, or they would increase their IOUs to Joe by the amount of the treasury.

Just as a quick recap, if a bank is selling to a non-bank entity, the amount of deposits in the system decrease. If a bank is buying from a non-bank entity, then the deposits in the system actually increase.

To back this up, here's the Bank of England's statement:

Banks buying and selling government bonds is one particularly important way which the purchase or sale of existing assets by banks, creates and destroys money.

The deposits we are talking about in the commercial banking system.

When banks purchase government bonds from the non-bank private sector, they credit the sellers with bank deposits.

So, additional deposits have been created, and of course, the opposite happens if the private sector buys government bonds or financial assets from the banks.

If you want to predict the future, to determine what's going to happen with the dollar, the stock market, the bond market, interest rates, gold, real estate, you've got to start by focusing on the commercial bank's deposits.

-Bank of England, 2014

Are they going up or down?

That's the only way that you're going to determine if the future is inflationary or deflationary.

If you think you've got your head around how it works, first and foremost, I'd like to congratulate you, but I'd also like to remind you, there's one more piece of the puzzle.

The majority of the deposits are created or destroyed by debt being increased or decreased in the economy itself.

Once you get your head around this, then you have to layer over what's going on in the real economy with another crosscurrent, which is even more powerful.

- How many loans are being created by the banking system, creating additional deposits, additional money supply, and chasing goods or services?

- How many loans are being paid off by the real economy, decreasing the amount of money that's chasing the same amount of goods and services?

I'm sorry if this is too confusing. I wish there was an easy way to explain it, but this gets really complicated.

I think the easiest takeaway is: Get your head around the real economy and then try to compartmentalize what's going on with government spending, QE, the banks buying and selling things.

Then, another completely separate area of focus would be how much debt is being created by the banking system. Try to come to a conclusion of what's happening on net balance. That's the best advice I can give you.