A cashless world and its consequences

Most people believe they understand why governments and banks seek a cashless society.

However, most of the reasons are wrong.

Starting with the belief that government and central banks want to generate a booming economy by getting digital cash into the hands of the people who need it faster.

These commonly discussed reasons are quickly eliminated by the explanation of Richard Werner, Economist, and international banking expert who believes the reason they want to go cashless is so they can implement negative interest rates.

https://twitter.com/scientificecon/status/930806729415172097

The shocking part is that the real reason behind the intention to ban cash looks more like George Orwell’s' 1984 novel than our desired progress paradise.

Unfortunately, it's far more diabolical. According to Richard Werner, a cashless society with negative interest rates is a plan to put the small banks out of business and consolidate power with the biggest banks in the world.

And this isn't where the plan ends.

In this video on banning cash, I explain:

- The usual reasons why you think they want to ban cash

- The real reason why they want negative interest rates

- The cashless endgame

Make sure to watch the video above to learn more.

Also, watch the full documentary “The Princes Of The Yen” on youtube. This documentary is based on Richard Werner's book.

The real reason they want to ban your cash

Trust me, you have never heard this before. It is time to sit down and grab a stiff drink.

I'm going to explain this to you in three simple, fast steps. And at the end of the video, I'm going to have you tell me what you think of a cashless society using my official GO scale. More on that later.

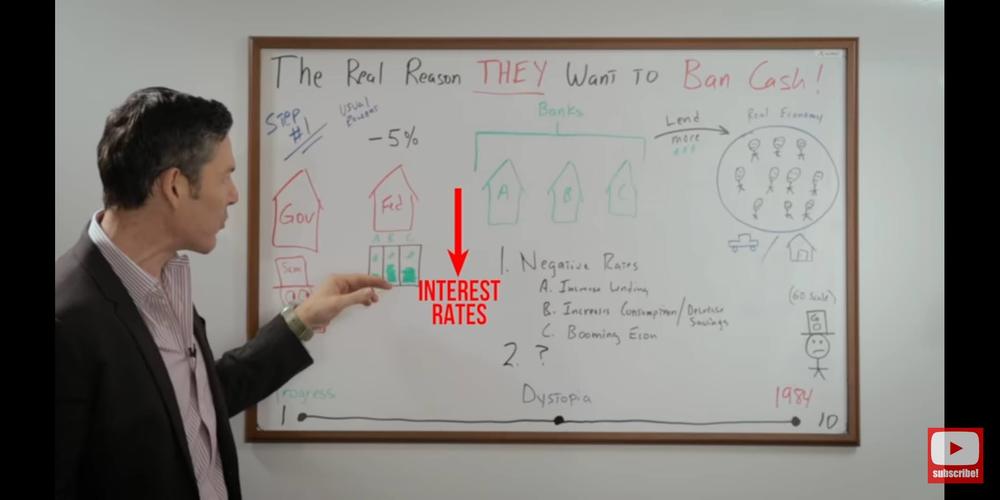

We're going to go over the usual reasons you think they want to ban your cash.

First and foremost, negative interest rates. And how this works is the Fed drops rates, let's say 5%, so all the banks who have money reserves with the Fed, they have to pay 5% on that money.

Of course, the banks don't want to do this so they lend all of that money into the real economy. This boosts consumption, and it decreases savings.

None of these people want to lose money because the banks are charging them negative interest rates as well, so they spend and buy new cars, new houses. They don't save a penny.

And according to the Keynesians, of course, this will produce a booming economy, because what is better for society than for you to spend every single dime you earn and not save a penny.

The problem with that as Richard Werner, economist, and international banking expert, has pointed out, the banks actually don't lend the reserves that they have on hold with the Fed.

If they don't lend out these reserves, that means that we can cross off increased lending, increased consumption, and them actually being concerned about the economy. That is off the list.

the government's ability to do bail-ins

A little lesser known component of a cashless society would be the government's ability to do bail-ins.

If there's no cash in the system at all, all of your excess productivity is held in this banking system in the form of digital currency.

There would be no way for you to extract that from the system if Uncle Sam who's got his eye, you can see right here, on your money, wants to come in and grab that money and take it for himself because he is 23 trillion in debt and running trillion-dollar deficits.

Although this makes a lot of sense, this isn't the main reason why they want to ban your cash. So we're going to take that one off the list as well.

The real reason they want negative interest rates

If we assume Richard Werner is correct, and obviously he's right here, beard, bald head, and that's banks can't lend reserve. This changes everything. What do I mean by that?

The banks can't take these reserves out into the system. So if the Fed drops interest rates to negative 5%, that becomes a tax that all banks have to pay on these reserves that are stuck at the Fed. That would decrease the amount of reserves in the system.

If there are fewer reserves in the system, that means that there would be fewer loans.

To be clear, the banks aren't lending out the reserves, but the reserves are necessary to back up the deposits that are created by the loans themselves.

In other words, the reserves make the loans possible without the banks actually lending the reserves themselves.

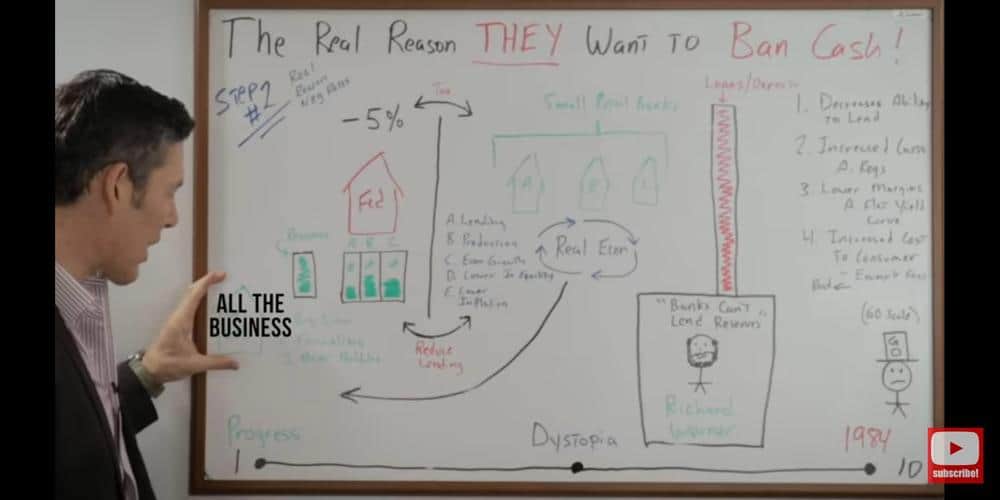

The bottom line is negative interest rates put tremendous pressure on small retail banks, decreases their ability to lend, increases costs through additional regulation.

If it flattens the yield curve, this puts a lot of pressure on their margins and it increases the cost to the consumer.

Because the small retail banks can't make money through traditional lending, they've got a nickel and dime you to death, and this makes them a lot less competitive in the eyes of the consumer.

So why would they want to create this type of environment for the small retail banks?

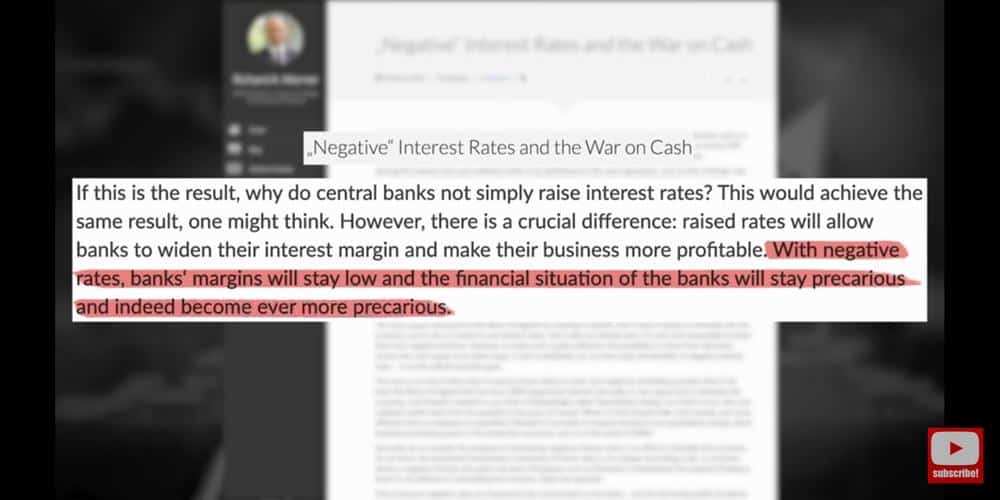

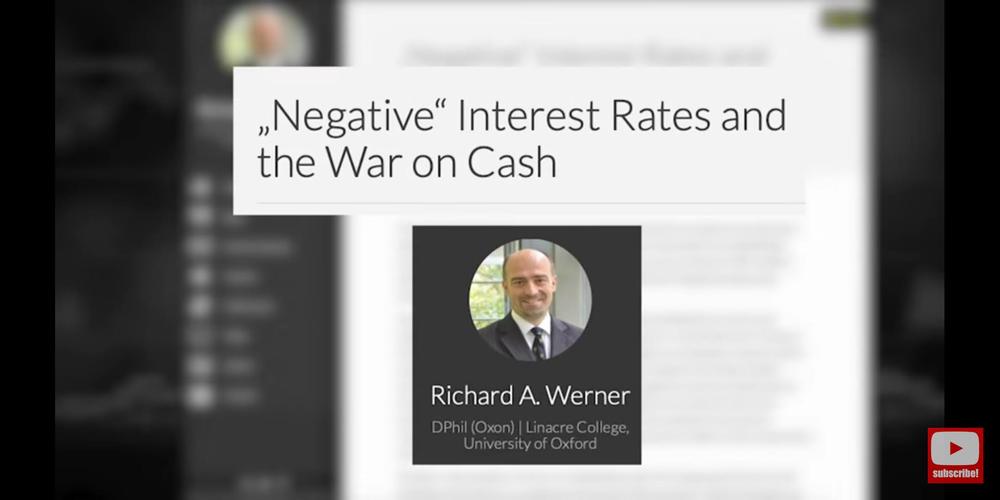

To answer that further, let's go to an article from Richard Werner himself.

With negative rates, bank's margins will stay low and the financial situation of the banks will stay precarious, and indeed, become ever more precarious.

Werner talks about the ECB specifically, but you can insert any central bank.

The ECB and the EU have significantly increased regulatory reporting burdens, thus personnel costs, so that many community banks are forced to merge while having to close down many branches.

This has been coupled with the ECB's policy of flattening the yield curve.

As a result, banks that mainly engage in traditional banking, i.e., lending to firms for investment, have come under major pressure, while QE has produced profits for those large financial institutions engaged mainly in financial speculation and its funding.

And I'm sure now, you guys are starting to put the pieces of the puzzle together.

He goes on to say, “The policy of negative interest rates is thus consistent with the agenda to drive small banks out of business and consolidate banking sectors in the industrialized countries, increasing concentration and control in the banking sector.”

I'd also like to point out that Werner believes that the small retail banks are responsible for the productive lending in the real economy.

They're the ones that lend to the small and midsize businesses that increase production, economic growth, lower income inequality, and low inflation.

But if you wipe out the small retail banks, that means all the business goes to the big banks who are really only interested in doing large transactions that financialize the economy and create asset bubbles.

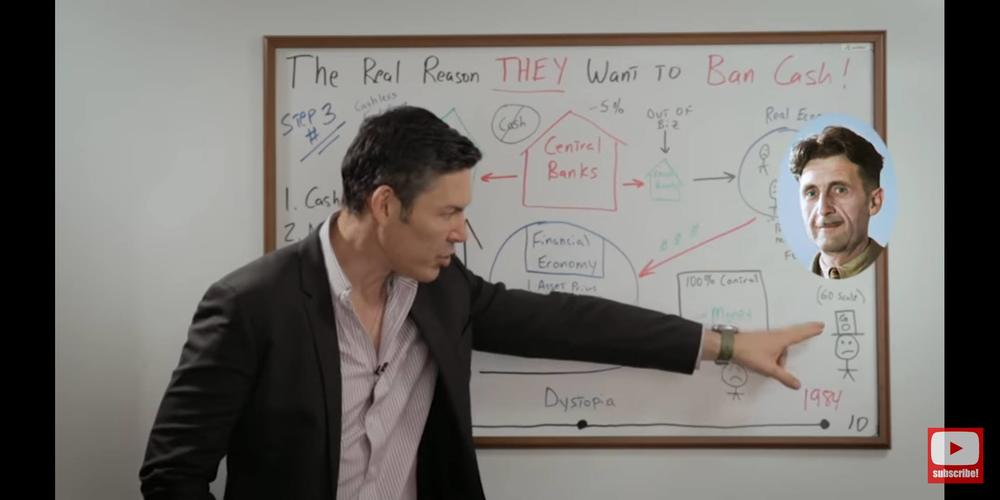

Now, it's time to connect all the dots in step number three. So sit down, grab a stiff drink, because this is going to blow your mind.

the cashless end game

Cash is banned, central bankers drop interest rates into negative territory. This puts the squeeze on all those small retail banks, putting most of them out of business.

As a result, the real economy shrinks because small and midsize businesses, the backbone of economic growth, don't have access to funding.

The average people look to the Fed and the government and say, “Oh, please protect us. We can't get ahead in the real economy anymore.”

They say, “No problem. There's a Fed put.” So all of the average Joe's take their resources and put them into the financial economy because now this is the only way that they can get ahead.

So they bet on asset prices, speculation, and timing bubbles.

So as the real economy is decreasing in size, the financial economy is increasing in size exponentially, making all of these bubbles bigger and bigger and bigger. The central banks know this.

At some point in time, it all comes crashing down.

When it does, the big banks go to the central banks and say, “Hey, we need a bailout.

We've got systemic risk.” That's when the central banks look at the big banks and say, “Ah, no. I don't think so.” They let them fail.

The central banks have then wiped out the small banks and the big banks so they are now the only game in town. They have 100% control of the money and the credit.

If they control the money and the credit, they control you. And to hear Richard Werner explain this in his own words, let's go back to that article.

Here, Werner talks about the bank of England, but you can insert the name of any central bank.

By supporting monetary reformers, meaning people who want to ban cash, the bank of England may further increase its own power and accelerate the drive to concentrate the banking system if credit creation was abolished and there was only one true bank left, the bank of England. It would further the project to increase the control and monitoring of the population. With both cash and bank credit alternatives abolished, all transactions, money creation, and allocation of that money would be implemented by the bank of England.

Werner goes on to imagine how the PR departments of the central banks and the mainstream media would spin this.

How one could increase their security and safety with this digital money. What if one loses one's direct debit card?

No doubt, some bright bank of England spark, or else any of the talking heads in the media, will then suggest we should adopt the techniques long practiced with our pets, namely implanting microchips under the skin as our money of the future. Whether this spells progress, readers need to decide for themselves.

Conclusion

So a cashless society, negative interest rates and central banks being the only banks left on the planet, and microchips implanted under your skin.

Using the GO scale or the George Orwell scale. I want to hear what you think. Is this progress, dystopia, or 1984?

I'll look forward to reading the comments below.

Comments are closed.