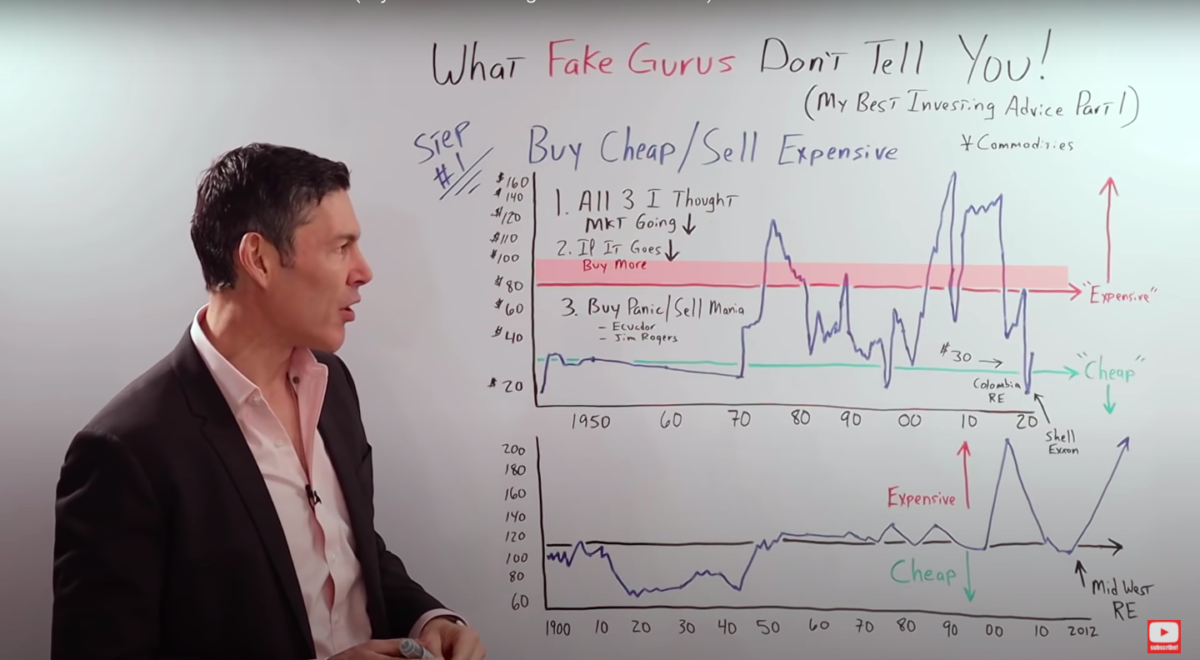

I want to show you where fake financial gurus are wrong and reveal a proven method that will make you successful over the long term, not just for a few months.

The key focus should always be value.

I know buying low and selling high sounds easy but very few people can actually put this into practice.

Why? Because they let their emotions get the best of them. We’re simply hardwired to lose money through investing and speculating. So you need to always be aware of your tendencies towards fear and greed.

Fear and greed always drive bad decision making.

So what makes investing easier?

Focusing on value instead of price action. In this article, I explain my best investing advice.

Buy Cheap, Sell Expensive

This is my very best investing advice, part number one. We have to buy when things are cheap and sell when things are expensive.

The main thing I want to focus on right now are commodities.

Why is that? Because as a sector, they're extremely cheap.

Here is a chart I got from my buddy, Ronnie, who's the editor of In Gold We Trust report.

You'll see that right now, in 2020, commodities are at an all-time low compared to the S&P 500.

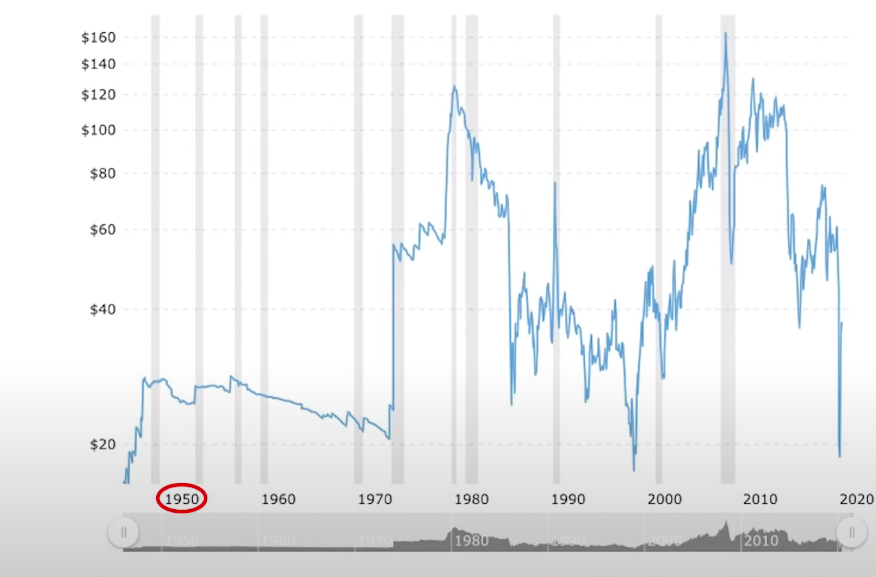

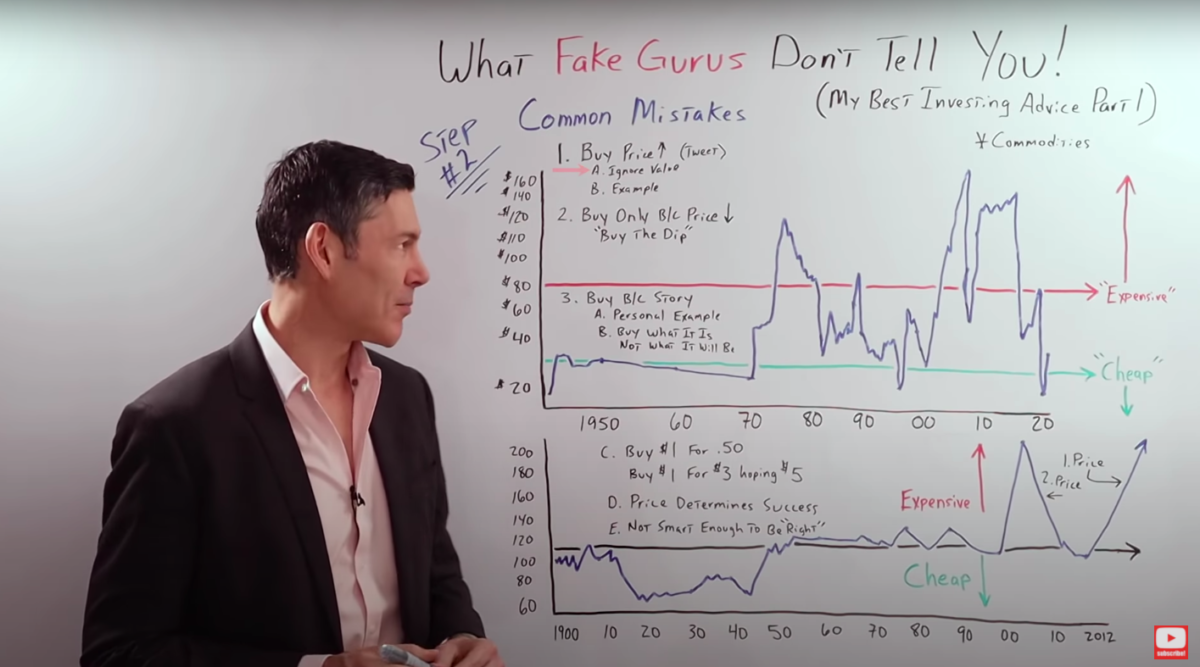

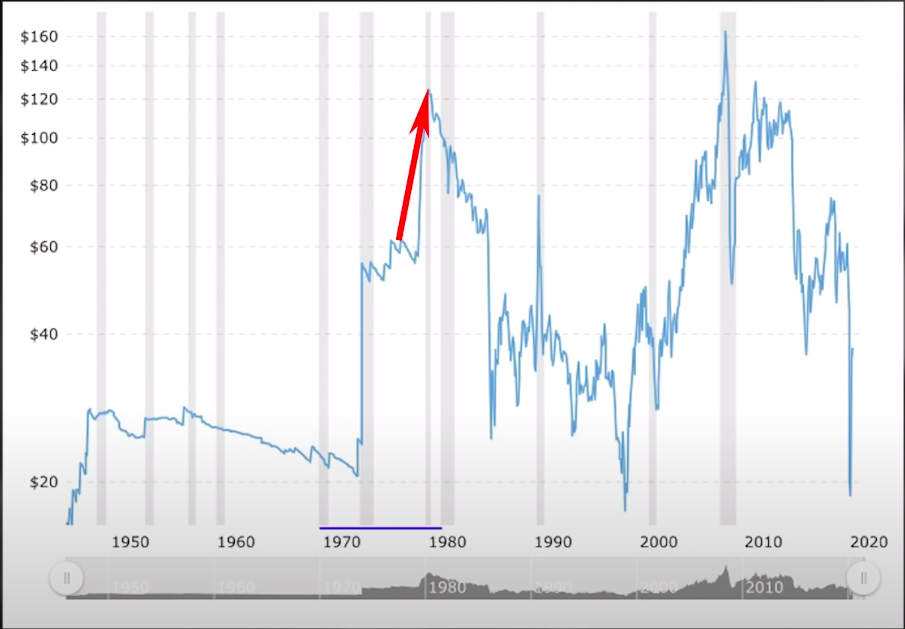

Let's start off with a chart of oil going all the way back to 1950 to 2020.

On the left, it goes from $20 a barrel up to $160. Back in the 1950s, it was pretty steady, then in 1970, it got off the gold standard. After that, it went parabolic.

Then in the 80s it came back down and went all over the place. It hit another low in the late 1990s and then after 9/11, it started to go up again until it reached an all time peak just before the GFC of $160 a barrel.

Keep in mind, this is inflation-adjusted. GFC came crashing down as you would expect, went back up, and hit another low around 2015.

I was noticing that this chart, I think, is a monthly chart, if it was a daily chart, I think it would've shown a drop right before 2016. If my memory serves me right, it got down under 30 in 2015-2016.

Later it came back up and recovered, but then Covid-19 arrived and brought it all the way down to negative $40 a barrel.

By looking at this chart, it's pretty clear what's cheap and what's expensive. If we just draw a line right about in $30 a barrel, when you're buying oil under 30, it's pretty darn cheap.

When it goes above $80, that's kind of getting into a “no bueno zone” where it gets expensive. Then, if it gets over a hundred dollars a barrel, that's when you really want to hit the bid.

From a standpoint of just looking at things to buy when they're cheap, if oil gets under $30 a barrel, that's when I personally would start to consider buying. When it gets over $80 a barrel, that's when I would consider selling.

Pretty straight forward. Buy when it's cheap, sell when it's expensive.

What's unbelievable is how hard this is for people to actually do in practice.

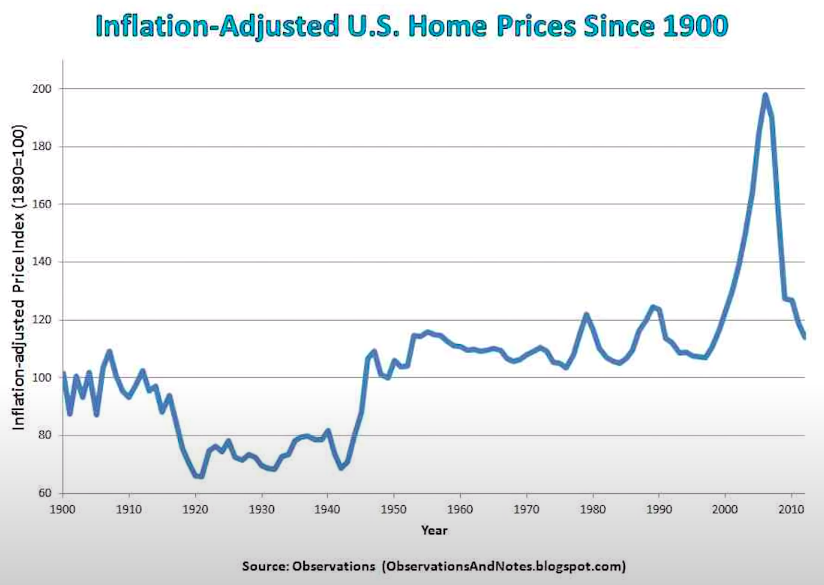

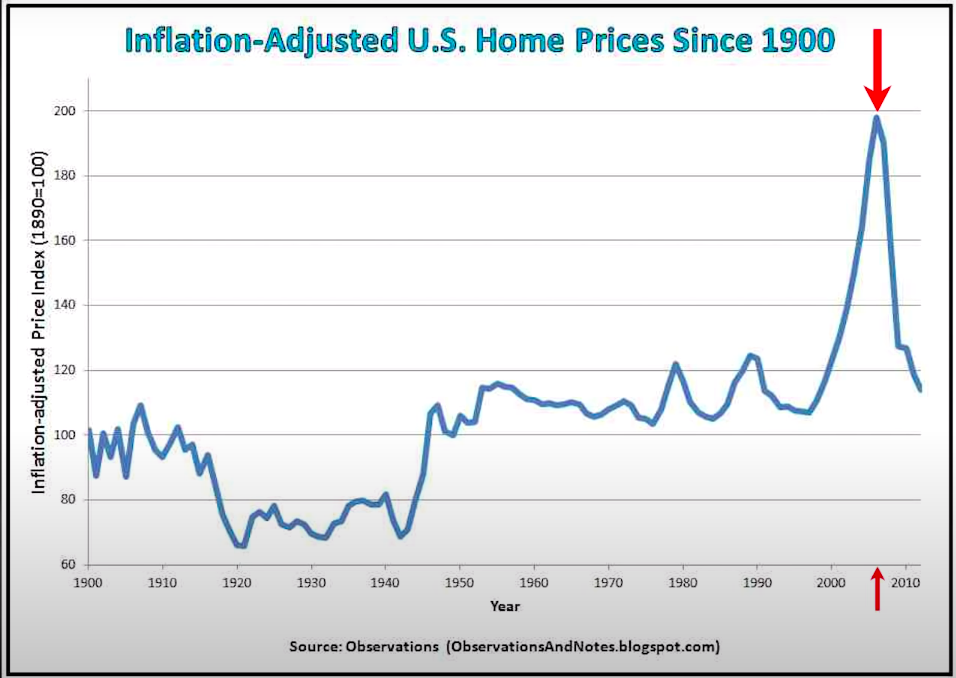

Now, let's move on to a chart of US housing prices adjusted for inflation and size.

It's the chart I always use, goes back to 1900 to 2012. On the left, it goes from 60 to 200. It started at a mean right around $100 until after the Spanish flu, and in World War I, it went down.

After the Great Depression and World War II it went back up, stayed pretty flat all the way to 2000.

One thing I always like to point out is from 1900 all the way to 2000, home prices were flat, they didn't go up at all.

I think this would shock most Americans. To actually look at this chart and understand the reality of prices in the United States compared to what they think prices have done.

But since 2000 we know what happened, the housing bubble, prices skyrocketed to a peak in 2006 and then they plummeted all the way down to a low in 2012.

Since 2012, prices in most markets around the United States have gone all the way back up to levels that are at least as high, if not higher than they were in 2006.

One of the nice things about real estate is it's a very inefficient market. What that means is you can go out, find a motivated seller and although the market, in general, could be in a bubble, you could find someone that's willing to sell to you for a 2012 price. You just have to know what you're doing.

Let's look at this chart from a standpoint of being cheap or expensive.

Our mean is right around 110, anything below that, you can tell is really darn cheap. That's when you want to be an aggressive buyer. Anything above that, it starts to get expensive.

When we get to where we were in 2006, that's when we're at nosebleed levels. You have to sell or at least be extremely cautious.

Let's go over three different times when I actually put this philosophy into practice.

-

2012

During this year that I retired, I saw the chart, loved it, and went almost all in with real estate in the Midwest. Since that time I've done very well.

-

2015

2015 was when oil got really low, and I know this is a monthly chart because I'm almost positive that it got down to $30 a barrel. But at that time, I really didn't know much about investing other than real estate.

So I looked around for something that I knew well to also go long oil. I wanted to bet that oil was going up the price.

I looked around and I saw the Colombian peso's loosely tied to oil and bought real estate denominated in pesos.

Since that time, it has fluctuated back and forth, but I've done extremely well on the real estate itself, it's appreciated dramatically.

-

2020

In March 2020, I went in and bought Shell Oil Company assets because I saw that oil was under $20 a barrel. At this point, it was negative $40 a barrel, and I thought that was really darn cheap.

I couldn't buy oil directly, the asset, nor buy large barrels, I don't have a warehouse, so I looked around at some companies.

I like Shell, Chevron, and Exxon and I bought a little bit of all those, again, just to go long the commodity of oil.

One thing I want to make very clear, and this is the big disconnect for most people, is that although I bought in those three situations, I thought the price of what I was buying would most likely continue to go down.

You would say, “George, if you thought the price was going down, why on earth did you buy it?”

Because it was cheap. It's all about mindset, it's all about how you see particular investments and how you analyze them.

Another question you may be asking is, “What if you buy something and it continues to go down?” That's fantastic, what I do is I buy more. Let's use the example of real estate in the Midwest.

If it would have continued to go down to where it was in the levels of the 1930s or the 1920s, I would have bought all the way down because I was buying the cash flow and I was just loving all of the assets I was buying on sale.

Exact same thing with Shell, if the price of oil goes back down to $10 or $5 a barrel and Shell goes from $30 down to $20 or $15, that's fantastic, I'm going to continue to buy because I'm getting it at a cheaper price than I got it before. It's all about the underlying asset.

Buy Panic And Sell Mania

Another strategy that I like to layer on top of the “Buy cheap, sell expensive” premise is to buy panic and sell a mania.

To dive into this further, here is a transcript of an interview on the original market wizards books with my favorite investor, Jim Rogers.

I want to go over a couple of different parts because it's applicable to other things that I will mention in this article.

Jack Schwager: Do you always wait for a situation to line up in your favor? Don't you ever say, I think this market is probably going to go up, so I'll give it a shot?

Jim Rogers: What you just described is a very fast way to the poor house. I just wait until there's money lying in the corner, and all I have to do is go over there and pick it up.

I do nothing in the meantime. Even when people lose money in the market, they say, I just lost money, now I have to go and do something to make it back. No, you don't.

You just sit there and wait until you find something.

Jack Schwager: So you trade as little as possible?

Jim Rogers: That's why I don't think of myself as a trader, I think of myself as someone who waits for something to come along. I wait for a situation that is like the proverbial shooting fish in a barrel.

Jack Schwager: Are all your trades fundamentally-oriented?

Jim Rogers: Yes. Occasionally, however, the Commodity Research Bureau charts will provide a catalyst. Sometimes the chart for a market will show an incredible spike, either up or down.

You will see hysteria in the charts. When I see hysteria, I usually like to take a look to see if I shouldn't be going the other way.

Jack Schwager: Can you think of any examples?

Jim Rogers: Yes. Two years ago, I went short soybeans after they had gone straight to $9.60.

The reason I remember it so vividly is because the same evening I went to dinner with a group of traders, one of whom was talking about all the reasons why he had bought soybeans.

I said to myself, “I really can't tell why all the bullish arguments are wrong, all I know is that I'm shorting hysteria.”

(End Of Interview)

There when Jim Rogers is talking about shorting hysteria, what he's saying is he's just going against groupthink, he's going against the psychology of the crowds when the crowds get incredibly emotional.

He's going against mania buying and panic selling.

I've talked to you about three examples of when I've made a substantial amount of money buying cheap and selling expensive. But I also want to point out that I have made mistakes and these mistakes have really taught me a lot.

They've taught me to appreciate how important the philosophy of buying cheap and selling expensive is, even more than the times I've made money.

An example would be Ecuador in 2014, the dollar was all the way down about 70, 75 on the DXY. Money was flooding into Ecuadorian real estate from Europe, Australia, and Canada.

Prices were just going up and up. It was basically a mania and I got caught up in it. I thought, “The prices are going to the moon, I'm going to buy when things are expensive in hopes to sell them when they are more expensive.”

I bought property right there and I got my butt handed to me. I probably lost at least $100,000. Now, fortunately, since I started investing in 2012, I've made a lot more money than I've lost.

But I want to point out, I have made mistakes just like everybody else, but those mistakes have helped me appreciate and solidify my understanding as to why the philosophy of buying cheap and selling expensive is so crucial to your long-term success as an investor.

The Most Common Mistakes People Make

This topic alone could easily take me hours, but I'll go over what I see most often on my Twitter feed and the comments of my videos. First is people's mindset. This blows away everything else.

-

Mistake #1: The price mindset

Most people, I mean like 99% of the general population only focus on price, that's it.

As an example, why would you go in and buy Hertz, when the company has already declared bankruptcy?

It's because you're only focused on price, that's it. Whether you think the Fed is going to come in and save the day, they're going to get a bailout, you're totally ignoring the underlying value of the asset you're actually purchasing.

It's starting from the wrong point. Yes, we want to buy things cheap, sell them when they're expensive because we want the price to go up, but that's not where we start.

We don't start by asking ourselves the question, “Is the price going to go up and down?”

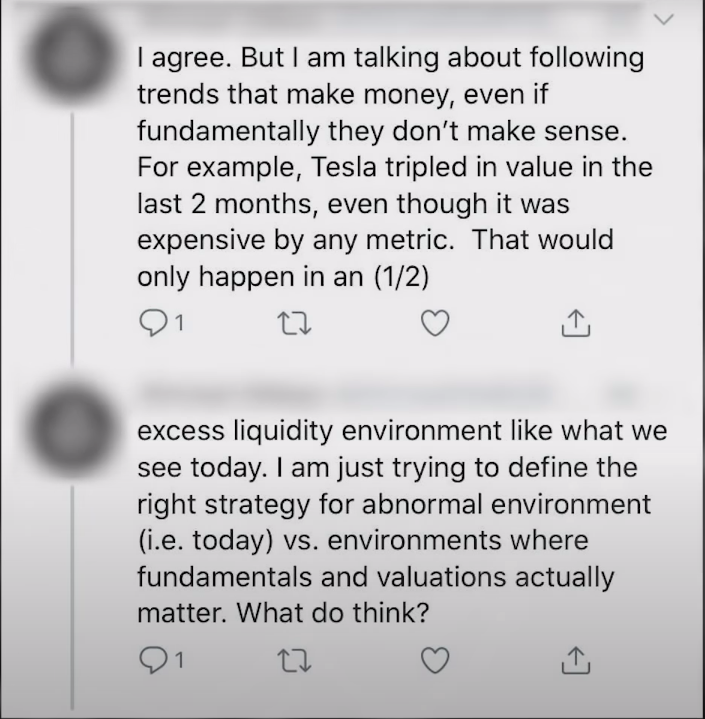

To illustrate this perfectly, look at the following tweet I had on my Twitter feed.

This tweet was in response to a tweet I made talking about how you need to ignore price, focus on value, buy things, cheap, and sell them expensively.

“I agree, but I'm talking about following trends that make money, even if fundamentally they don't make sense. For example, Tesla tripled in value in the last two months, even though it was expensive by any metric.”

Of course, the question is:

-

Why would you do that at all?

-

Why would you buy something that fundamentally doesn't make sense?

You would only do that if you were focused exclusively on price.

You see what this gentleman's doing, he's focusing exclusively on price. It's just about if the price is going up or down, they don't care about the underlying fundamentals, the value or buying something cheap selling it expensive.

I want to quickly go back to the example I gave to point out something.

In all those three investments I made that did extremely well, I thought the prices of the asset I was buying were most likely going to continue to go down.

But, I ignored what I thought the direction of the price would be and exclusively focused on the things we've been talking about.

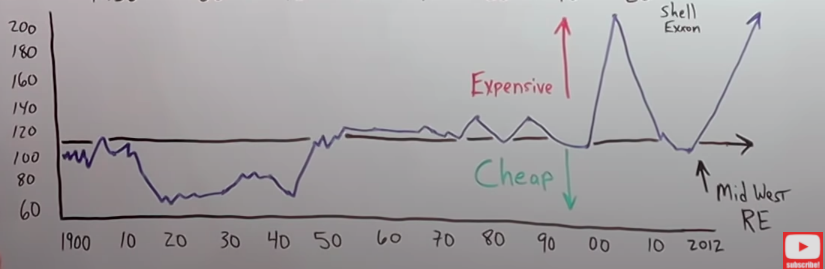

Let's go back to the charts.

Look at the bottom chart on the right side. In 2012, I thought most likely prices would go down by another 10% or 15% because I was looking at prices or charts going back to Japan in 1990 when they had their big real estate bust.

I thought we had more downside, that was a high probability. But I bought anyway because I didn't care if the prices were still going down, I wasn't trying to time the market exactly, I was looking at the underlying value of the asset I was purchasing.

Exact same thing in Colombia back in March of 2020, I thought prices would most likely continue to go down but I bought it anyway.

-

Mistake #2: Buying only because you think the price has gone down

This is the second mistake people make all the time. Again, they're totally ignoring the underlying fundamentals. You hear this all the time when people are saying, “Just buy the dip, buy the dip.”

Here is the chart of housing.

There we see a peak in 2006. You could have said that in 2008, 2009, 2010, and 2011, you could have said, “Just buy the dip, just buy the dip.”

But it's not cheap yet, it didn't really get cheap until we got into 2012. The same thing, if you go over to oil in the 1970s, in the mid-1970s at the peak, $120 a barrel adjusted for inflation.

A bit later you could have said “Oh my gosh, the price has gone down to 100$ a barrel, we have to buy the dip. It was $120, it's $110 now so it has to be cheap, right?”

Do you see what I'm talking about? Totally void of the underlying fundamentals, exclusively focused on price.

-

Mistake #3: People buy just because there's some story

“You have to buy Hertz right now, you have to buy the airlines because the Fed is going to come in and bail everybody out. They're going to buy the equity so you have nothing to worry about. That's buying a story.”

“Oh my gosh, you have to buy this new electric car company called Nikola. They have technology that's going to completely change the world.”

Well, that's fine, I hope they do change the world. But I'm not going to pay a change the world price today when they haven't changed anything.

As a matter of fact, they don't even have a product nor do they even have one penny in revenue. I think I may have an advantage here because I became completely immune to this nonsense when I was an entrepreneur.

I had countless people every single week pitching me on the next idea on their great product.

“Invest in this restaurant, invest in this technology, and by the way, give me a million dollars because my business is worth $50 million although I don't have anything other than a bank account, an LLC, and a business plan.”

When I was in the world of buying and selling businesses, before I retired in 2012, I learned very quickly that you buy what the business is today.

Whatever the P&L or the balance sheet is today, that's what you're buying.

You are not buying what the business will be in the future, you're not buying proforma financials, you're buying exactly what the cash flow and balance sheet looks like today.

As an example, you always make money on the buy-side in real estate, I think it's the exact same in stocks and commodities; gold, silver, anything.

What I try to do is buy $1 for 50 cents. What most people do is they buy a dollar for $3, hoping that it'll go to $5.

Going back to our overall theme of getting hyper-focused on price, another mistake I see people make is they let the price going up or down determine whether or not the speculation or investment was a success.

This takes me right back to my days playing blackjack. If you were focused on whether or not you lost a specific hand, in the end, you would always lose.

You have to get that thought out of your consciousness altogether.

So what do you focus on?

You focus on the probabilities, in making the correct decision every time. But the correct decision isn't based on whether or not the price went up or down, it's only based on how well you analyzed the value and the fundamentals.

In blackjack, whether or not you made the right decision based on the probabilities.

Let me just say this another way to be crystal clear, I would prefer the value of my portfolio go down having made good smart decisions, based on value and fundamentals than have my portfolio go up as a result of me being a complete knucklehead and buying the story or doing something that DDTG is doing on his Twitter feed.

You may be saying to yourself, “George, I get it, but I'd rather have my portfolio start at $100,000, go up to $200,000 because I'm making dumb decisions than have it go down to $50,000 by making smart decisions.”

That may be true over the short run, you can get away with those dumb decisions, you can get lucky. But, over the long run, if you're making dumb decisions, you will lose money, if you're making smart decisions, you will come out ahead.

In Practice

We started by looking at the 30,000-foot level, the macro stuff with oil, commodities, and the real estate market. But let's take the next step, let's look at an actual business.

We're going to start with the financials and the fundamentals instead of asking ourselves if we think the price is going up or down.

It's a novel approach, I know it sounds crazy. But we're going to look at the profit and loss from a McDonald's franchise to help us understand things even better and become smarter, more intelligent investors.

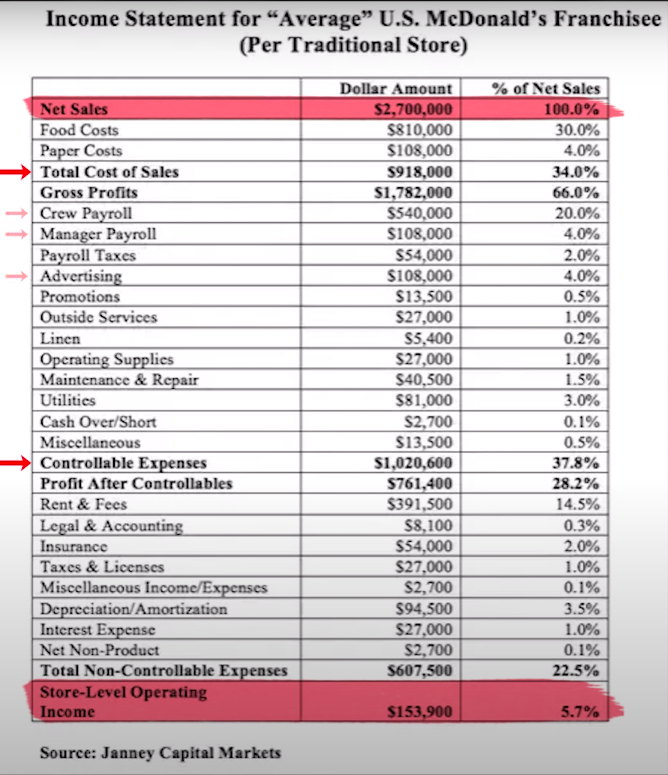

If I was considering buying a McDonald's back in the day when I used to be an entrepreneur and do this type of stuff, I would look right at the top for the line sales, gross sales. In this case, this McDonald's franchise is making $2.7 million.

Then I'd look at the bottom line immediately and say: Okay, they're making $150,000 from that $2.7 million…

-

How is that broken down?

-

What are their costs of goods sold, especially in a restaurant or a bar?

Then I'd look at their controllable costs, mainly payroll, their marketing/advertising budget, and see if there are some efficiencies that you could add there, also look at their non-controllable costs.

After I'm looking at the top line and bottom line, I'm going over just to make sure all of it makes sense.

I'm going to assume these financials have been audited, therefore, the bank statements would back up every single number on this P&L, but that's a topic for a completely separate article.

All of that is exactly what you'd want to do when you're considering purchasing a stock of a publicly-traded company. There is no difference, you're starting with the fundamentals first.

As an entrepreneur, this is how I'd analyze this deal. It's just back of a napkin math.

- First, we have a profit of $150,000 a year. This means you're making money on the buy side, we always have to be cognizant of that.

- Their asking price is a million dollars, but of course, that's negotiable.

I'm looking at this and thinking, “If I pay them a million dollars, I have to take out a loan for $800,000 and put $200,000 down.”

- So I'm 200 grand out of pocket to service the debt on $800,000 grand, probably 50k a year.

Again, these are just broad numbers, I'm using them as an example.

- I'm going to be left with about a $100,000 in profit after I service the debt.

That would start with $150,000, but you're deducting the $50,000 to service the debt, so you're left with $100,000. So, if you have $200,000 out of pocket, it's a 50% return. Not bad.

That would start with $150,000, but you're deducting the $50,000 to service the debt, so you're left with $100,000. So, if you have $200,000 out of pocket, it's a 50% return. Not bad.

I know most of you right now are saying, “George, but you don't get all the dividends of the publicly-traded company. It's not like all those profits are going right into your back pocket.”

You are correct, but you have to think of it in different terms. Let's assume I hired someone to manage this McDonald's for me, so he manages the asset, and I'm completely out of the loop.

The manager took the profits every single year, distributed some of it to me so I got a little bit, but he took the majority of the profits and went right back in and bought more McDonald's franchises.

So, every single time we had an extra $200,000 in profit, they would buy another franchise. And because it's under your name, the portfolio is growing and growing.

The value of what you own is always increasing even though you're not getting 100% of the profits in distributions or dividends.

It all goes back to having great management, and that's why you have to look at the fundamentals of a company prior to buying it. Regardless of whether it's a publicly-traded company or a McDonald's franchise.

Going back to making money on the buy side, I'm always going to negotiate, I'm trying to get a $1 for 50 cents. You can do that in a few different ways.

Number one, you negotiate with the seller. I understand in a publicly-traded company you're not able to negotiate with a seller, but what you do there is go right back to buying panics and selling manias, just like Jim Rogers.

Let's say typically a McDonald's franchise is trading at six to seven times profit. Well… Let's say because of the coronavirus, all of a sudden they're trading at four times multiple.

That is an example of buying a dollar for 50 cents. You have to look at stocks and publicly traded companies the exact same way.

Now, let's go back to the mistakes people typically make and apply them to a real life business to see how ridiculous it actually sounds.

-

Mistake #4: Buying because the price is going up

Someone comes to you and says “Oh my gosh, you have to buy this McDonald's franchise. It's a million dollars right now but next year I'll bet you the price will go up to 1,000,002, it might even go up to 1,000,003. We're going to have to buy right now.”

Completely ignoring the profit, the dividends, and everything else that I just went over.

Think about how ridiculous that would be if one of your buddies came to you and says, “Listen, I want to buy this McDonald's, it's only a million bucks right now and in two weeks, I'll bet you we could sell it for 1.2 million or maybe 1.5 million.”

You'd be like, “What are you talking about? You're not buying McDonald's to sell it in two weeks.” That's my point.

We would go straight to looking at the value if we're considering purchasing a McDonald's franchise. Or, let's say that you would buy only because the price had gone down.

If instead of asking for 1 million, understanding the multiple on a McDonald's franchise is typically six or seven, they were asking 3 million but they dropped the price down to 2.5, does that mean the McDonald's franchise is all of a sudden cheap because it's 2.5 million instead of 3 million?

No. You have to do the homework, go back in history, and determine what multiple McDonald's franchises typically sell for.

Next, you're buying the story. Someone goes “Oh my God, you have to buy this McDonald's, they have this new hamburger coming out that's vegetarian, it's a vegan, it's a game changer.

They just did a deal with Beyond Meat or whatever that crazy company is, and all these people are going to flood into the McDonald's franchise.”

Okay, well, that's great, but I'm still not paying more than a million bucks if right now they're only making $150,000 in profit because historically they're only trading at a six or seven multiple.

That's all I'm willing to pay right now. I'm going to go ahead and buy what it is now, not what it will be tomorrow. Just because the McDonald's franchise just signed a deal with Beyond Meat, I'm not willing to pay $5 million for it because then what I'm doing is I'm paying $3 for $1, hoping to get $5.

That, as Jim Rogers says, that is a quick way to the poor house.

The next step, as I mentioned, is determining the success or failure of this McDonald's based on whether or not the price went up.

Let's assume that you have this McDonald's for five years and it's making $150,000 a year, which means you're able to buy another McDonald's franchise every three years.

But the price is still a million dollars, or it went down to 900,000 because interest rates went up or something happened in the marketplace.

Would you look at that and say: Oh my gosh, I've made a terrible investment?

On the flip side of the coin, let's say that interest rates went down but your profits went down as well. Instead of $150,000, now you're only making $100,000 a year. The debt burden is $50,000, so your bottom line is only $50,000 grand a year.

Your margins are really getting squeezed but because the Fed has interest rates artificially low, the price of McDonald's went from $1 million up to $1.2 million.

Would you say: Oh my gosh, my McDonald's is a huge success. I'm almost going out of business but the price has actually gone up?

Of course not, you would never say that. Your opinion would be based on how much profit you were making and losing, not by going back to your business broker every three weeks and asking them for a new appraisal price.

-

Did the price go up?

-

Did the price go down?

-

Did it go up?

-

Did it go down?

That's complete madness. It's all based on the fundamentals of the underlying business. That's what you're buying when you buy a stock.

Comments are closed.