Deflation had devastating effects in the 1930s and it may have worse effects in our near future.

This article is part of a series, this is only part 1. In both of them I address the question:

Is the U.S. headed for another Great Depression?

I do this by explaining what deflation is, Dr. Lacy Hunt's arguments, and the law of diminishing returns.

Make sure not to miss part 2 where I conclude the answer to our main question.

For more content that'll help you build wealth and thrive in a world of out of control central banks and big governments, JOIN our Daily Newsletter for FREE!

Dr. Lacy Hunt's Argument

Is the United States headed for a Great Depression 2.0?

Let's go over Dr. Lacy Hunt's argument for deflation. No one researches this more thoroughly than Dr. Hunt, and nobody articulates his position better than himself, in my opinion.

To have evidence of this, I recommend you to hear the most recent podcast with Grant Williams and Bill Fleckenstein called the End Game that featured an interview with Dr. Lacy Hunt.

A lot of this article is going to be summarizing and explaining what Dr. Lacy Hunt was talking about in that episode.

As soon as you finish reading this, make sure you go to iTunes or whatever your favorite podcast platform is, and check out that episode of the End Game.

All of this will make a lot more sense, and you'll be able to listen to Dr. Lacy Hunt's own words.

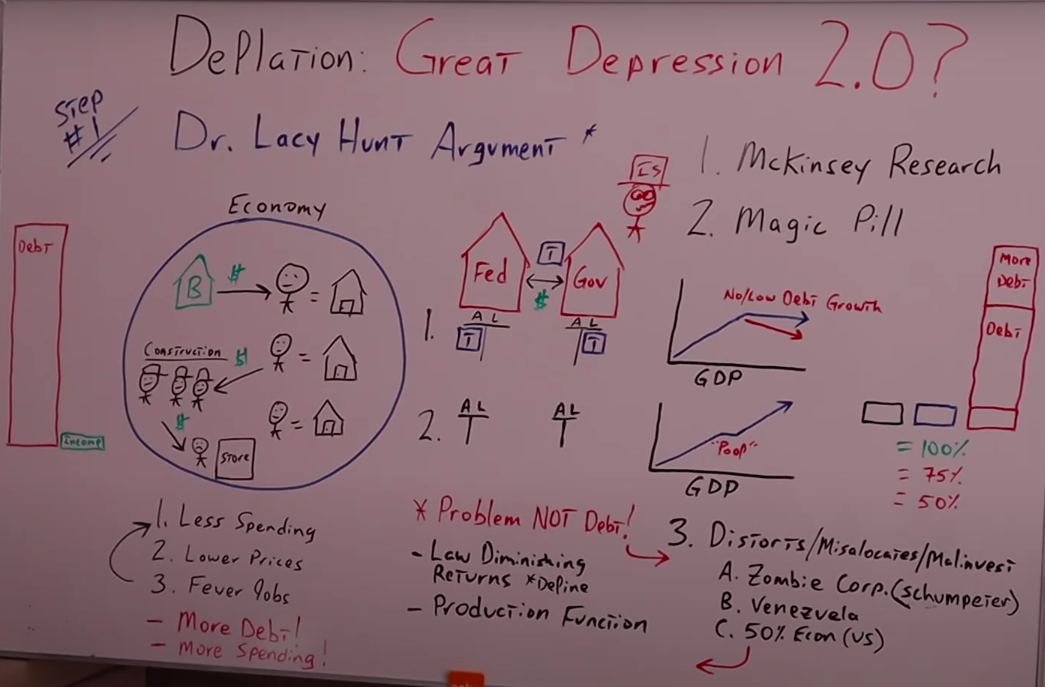

Let's start off by understanding just the basics of deflation. We all know the story so I'll go over it quickly with this whiteboard.

Inside the blue circle, you can see a basic economy with three individuals who own homes. They really couldn't afford them, but they were able to get excessive debt from the banking system.

Because they have their homes, they go up in value, and there's demand. We all know the story of 2002 to 2008 but this chart talks by itself.

The increase in the asset prices due to the debt going up creates more spending, and also more jobs for the construction workers inside the circle.

The money goes from the bank, to the individual, to the construction worker, and then the construction worker spends that money at the local store, as do the individuals who purchased homes by getting this loan from the bank.

Unfortunately, what ends up happening is the debt gets really high and the income stays the same. So at a certain point, there isn't enough income to service the debt and it all comes crashing down.

There's no more debt going from the bank to the homeowners. Therefore, there's no money going to the construction workers, no money going to the store owner.

There's less spending, which equals lower prices, fewer jobs and it creates this doom vortex. With fewer jobs, we have less spending, lower prices, and it creates a feedback loop downward.

The Keynesian or the typical approach from the Fed, the people at the World Economic Forum, Klaus and all his buddies, would be, “Well, we just need more debt because we have to increase spending.

The problem is spending. Therefore all we have to do is increase it and if we can just take on some more debt from the government, or if we could just have the individuals take on more debt, the problem is solved.”

It's really the knuckle dragger approach to solving the deflationary problem. Of course, Dr. Lacy Hunt is a genius, he really gets down into the nuance of deflation and why just adding debt to increase spending won't work.

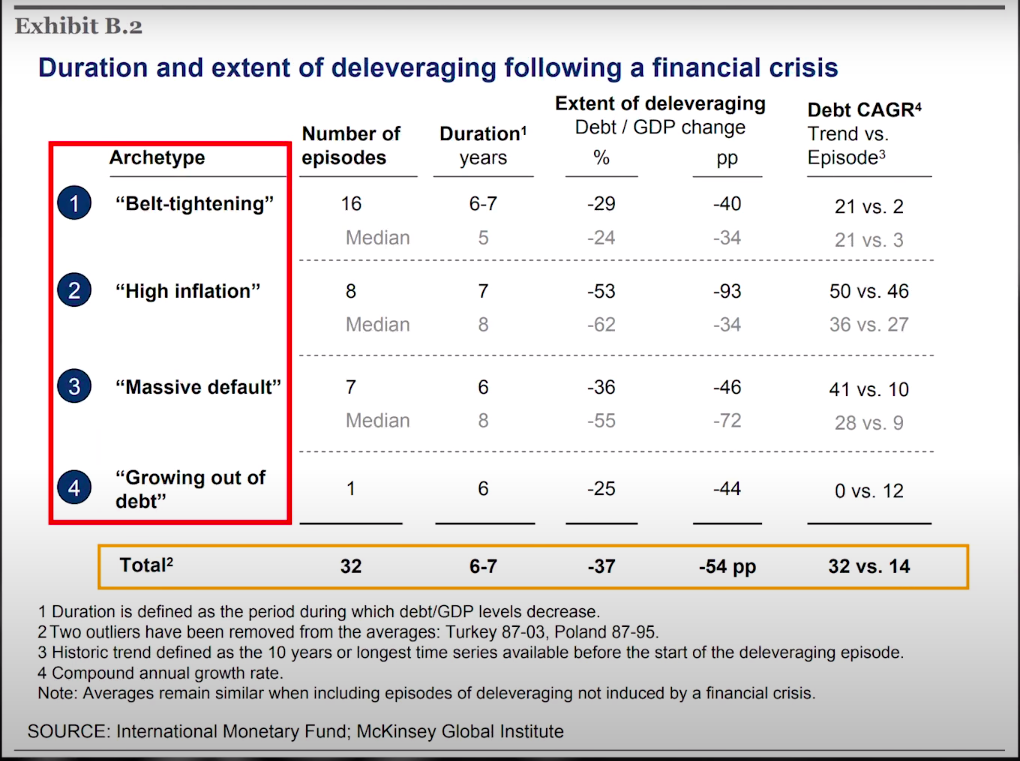

First, let's check out a report from McKinsey Global Institute Dr. Hunt references continually throughout the interview that backs up a lot of his conclusions.

It starts on page 67 of the report where they go over historic episodes of deleveraging.

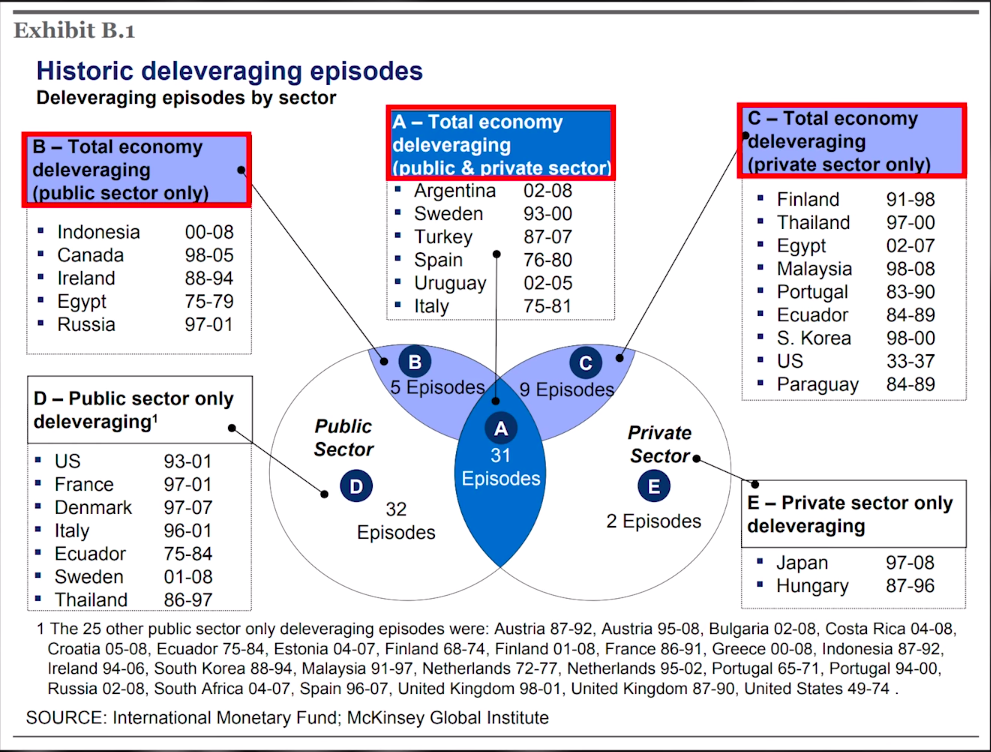

Exhibit B shows us they're not just measuring public sector debt, but also private-sector debt and a combination of both.

There's really only four ways out of this big debt problem and you can see them in the red box of the following chart.

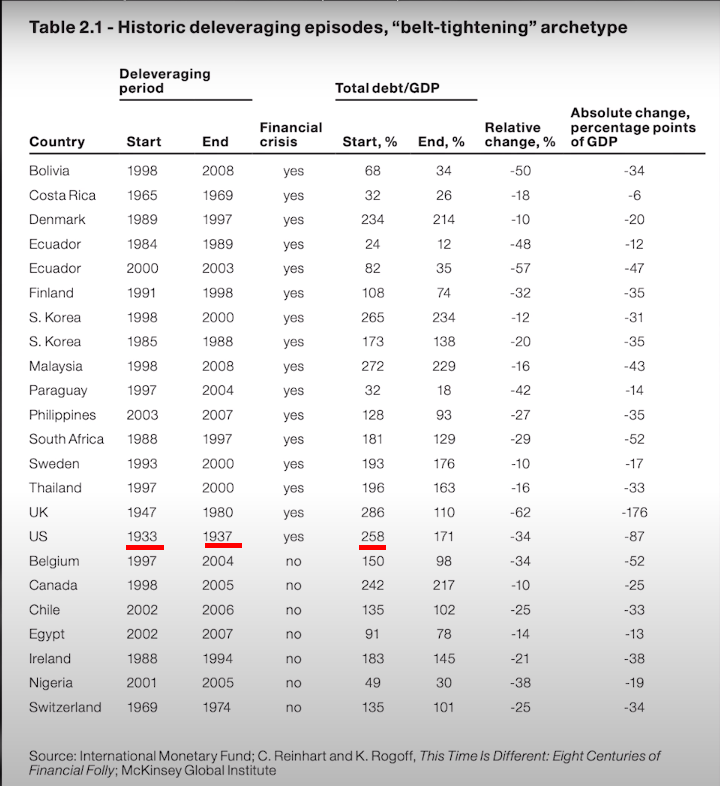

1.Belt-tightening: This is what happened in the majority of the countries that they studied during certain time periods. Basically, this is austerity. This is when you have to live beneath your means.

You overspent, you over-consumed by taking on all this debt. Now it's time to pay the fiddler. You have to under consume until you get back to an equilibrium point.

As you can see in the following chart, they use the example of the United States in the Great Depression from 1933 to 1937.

Starting off at 258% debt to GDP, this would include private and public sector debt.

2. High inflation: Of course we know all the stories of hyperinflation and the devastation that does to the economy, but the upside is that it definitely does wipe out any debt you have denominated in the local currency.

3. Outright default: Which is just as bad.

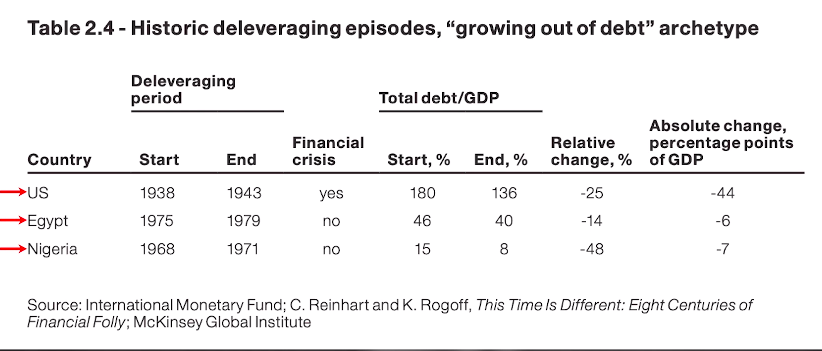

4. Growing out of the debt: This is what all the Keynesians want us to do. This is their perfect world scenario. Unfortunately, it rarely happens.

In the following chart you can see the only time that has happened, in the McKinsey Study.

It has happened three times, once in the United States, once Egypt, and one in Nigeria. I point out that in Egypt, their total debt to GDP started at 46% and only went down to 40%, and that was after four years. Not that much of a de-leveraging.

In Nigeria, it went from 15% down to 8%. The United States is the only example of where it went down substantially. But I'd like to point out that it was a result of World War II.

To summarize, the options right now for the United States are to:

1. Live beneath our means, and produce more than we consume for a continued period of time, probably a decade.

- Opt for high levels of inflation that might even turn into hyperinflation, which would be far, far worse than just a belt-tightening or austerity.

3. Default really isn't an option for the United States. So the only thing left would be World War III.

Obviously belt-tightening is the best way out, although it still would be very painful, but ironically, it's the one that all the central planners, the Fed, and the government, are trying to avoid at all costs.

The main takeaway is there's no magic pill.

There isn't a benevolent super genius to put in charge of the Fed or the government, that can figure out a creative solution that nobody's ever thought of that would allow us to get around having to take the medicine.

It doesn't exist. It just won't work. Here is Dr. Lacy Hunt explaining this in his own words.

Dr. Lacy Hunt:

The fact of the matter is the debt is still effectively there, which means that you cannot bypass the law of diminishing returns.

Because what you're thinking is that we somehow put it aside and then we go about borrowing more money to facilitate the economy.

Well, if you overuse a factor of production, the growth rate will just get weaker and weaker. There is no financial solution. Everybody's looking for a cutesy fix and it's not there.

By the way, I've heard people say to me, “I've been told that you're a bright fellow. Well, if you're so bright, why can't you tell me what the fix is?” There is no fix.

(End of transcription)

To understand Dr. Hunt's arguments even further in greater detail, let's go through a quick thought experiment.

We've all heard of a “solution” that's becoming very popular in the mainstream media. It's pretty much looking at the balance sheet of the Central Bank and the government just like an NBA scoreboard.

Let me explain. The government issues debt. We'll call them treasuries, and the Fed prints up money. That goes to the government and they spend it into the economy.

This creates GDP growth, but at a certain point, people start to worry, whether it's the politicians or the crazy Austrians that think debt is a big deal. Of course, this is their words, not mine.

Then we have a debt ceiling. So the government has to limit its spending. It can't spend as much as it was at the beginning that produced the original high levels of GDP growth. It levels off, if not sometimes goes down.

The people that look at this say “Well, that is craziness. Obviously we can see that the more government spending we have, the higher the GDP goes.”

Imagine the Central Bank takes all of the liabilities of the government, the treasuries, all of their debt and just move it over to their balance sheet

Since the Central Bank can take an infinite haircut and their balance sheet really doesn't matter, at a certain point when the Fed or the Central Bank owns all the government debt, we can just press a button and poof, the debt gone.

The asset side of the Fed goes to zero and the liability side of the government goes to zero. Then we can go right back on this trajectory of having GDP grow and grow. It's absolutely infinite.

The only thing we have to do is get out of our own way and realize the power of our own currency. You hear it all the time.

We're not a currency user, we are a currency issuer, and that makes all the difference in the world. Again, his words, not mine.

When you look at it in the terms of a basketball game, where you could just take the score from 100 for each team right back down to zero and start the game all over again, it kind of makes sense.

But as you can imagine, there's a big problem with this way of thinking.

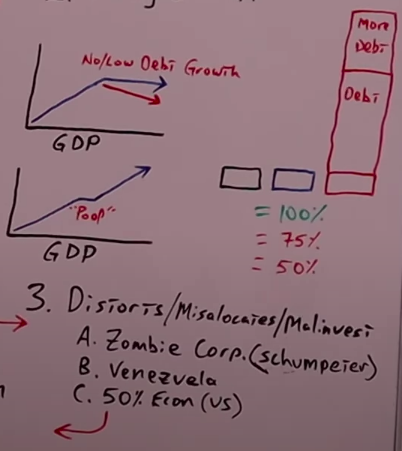

The problem is it's really not about the debt or having to service the debt. It's what's been done to the economy as the debt was being produced, as the government was creating that spending.

What they're not realizing is as GDP was going up as a result of all the additional debt, whether it's private sector debt or public sector debt, it's distorting the economy.

It's misallocating resources and it's creating malinvestment.

Let me give you an example. Japan, they have all these zombie corporations that we've heard of.

So even if you're able to eliminate all of the Japanese debt tomorrow, you still have all these zombie companies.

It wouldn't really make that much of a difference. Also, let's think about Venezuela. They created their entire economy around one revenue stream. It was oil. This made their economy extremely fragile.

Even if you're able to wipe out all their denominated debt, it doesn't mean that their economy is any less fragile moving forward.

The damage has already been done.

Let's look at the United States. Right now the government is over 50% of the economy. In other words, government spending is responsible for over 50% of our GDP.

Even if you are able to wipe out all $26 trillion of our balance sheet debt, it still doesn't rearrange our entire economy. It's just as bad as it was before. Dr. Hunt gives us the reasons why in economic terms.

First is Schumpeter's creative destruction.

But, let's go back to Japan. If Japan or the United States back in 2008, 2009 would have let these big corporations fail, we would have had this creative destruction.

All of the good players, people who were prudent, new young entrepreneurs with great ideas, would have taken over the assets from all of those old monopolies.

As a result, our economy would be a lot stronger today than it would have been. Yes, we would have had to go through a year or two of pain, but we would be far better off today, not just in the United States, but Japan as well.

Law Of Diminishing Returns

Check out the definition:

“The law of diminishing marginal returns is a theory in economics that predicts after some optimal level of capacity is reached, adding an additional factor of production will actually result in smaller increases in output.

For example, a factory employs workers to manufacture its products, and at some point the company operates at an optimal level.

With other production factors consistent, adding additional workers beyond this optimal level will result in less efficient operations.”

– Investopedia

It goes right back to the production function. We've all heard of land, labor and capital. Those are the basics.

So on the right side of my board, I drew a black rectangle that represents land, a blue rectangle representing labor, and a red rectangle capital.

If they're all in harmony, running at capacity, we're producing 100% of our potential economic output. But if we layer on additional excessive capital, let's say in the form of government spending in debt, it will actually lower economic output. We go from 100% down to 75%.

If we think the solution to a debt problem is just more debt, so the government spends, even more, then the economic output goes from 75% down to 50%. You see the problem here.

What it really boils down to is there's only one way to produce economic growth, and we were all taught that way back when we were kids growing up, but no one articulates it as well as Dr. Hunt.

So, to finish up, here is another comment from that recent podcast with Grant Williams and Bill Fleckenstein.

Dr. Lacy Hunt: What we have here and really the thrust of where the modern monetary theory is going, people are talking about the technicals of MMT.

The real flaw is that what creates economic prosperity, wellbeing, and advancement is hard work, ingenuity, saving, reinvesting. The solution's not with the government.

But, what we're looking for is some sort of easy governmental solution, which is not the way we achieved our prosperity. That's the fundamental flaw.