An economic collapse is on everyone’s minds, but should we be worried?

Some say it’s inevitable while others say it’s not only inevitable but imminent.

In this article, I will analyze the future of the economy by making a thought experiment on what would happen to the financial system and the real economy if we normalized, and will also answer the question:

Can the Fed avoid the economic collapse by reinflating bubbles?

Economic collapse: It starts with the financial system breaking down

Let's start by asking ourselves, what would happen if the Fed normalized interest rates and its balance sheet (BS)?

What would that do to the plumbing of the financial system, and therefore to the entire financial system, and the economy?

It starts with the repo market and the primary dealers who provide cash for the financial institutions and hedge funds who swap overnight, or for a specific term, collateral for cash.

This means the repo market is the key to propping up the corporate funding market because if corporations get the funding they need, the stock market is propped.

The repo market is crucial.

Analyzing the 2008 Great Financial Crisis

But, l will go back and analyze what happened in 2008 and the GFC so we can have better answers to what will happen today.

The real economy was fine, people were paying their houses but they started to get upset because the Fed raised interest rates from 1% to 5%, so all of the individuals who had adjustable-rate mortgages, couldn’t afford to pay them.

Those mortgages were most likely bought by the Federal Housing Finance Agency (FHFA) and turned into mortgage-backed securities that went on to the BS of the primary dealers.

There was specifically one primary dealer bank owned by a couple of brothers who only had one piece of collateral, a loan from someone who couldn’t pay his mortgage.

That loan was on the asset side of their BS, but unfortunately, on their liability side, they had payments to make, which is why they took their collateral and went into the repo market looking for cash.

The surprise was they couldn’t sell it because it was already known that the borrower couldn’t pay, which meant they no longer had collateral, nor repo transaction, and no cash for the debt payment, so they went bankrupt.

The catalyst for the GFC was the collateral source for liquidity and funding dried up.

But the more important point is they had an entire system that was incredibly fragile because it was 100% reliant on the collateral.

Here’s a similar example.

Venezuela's Oil-Pegged Economy

We all know the problems Venezuela has been having for being an oil-based economy, so whenever the oil price drops their system collapses, they have to print more money, and hyperinflation keeps growing.

Do you think oil price going down was the main issue of their problems or was it the fact the entire system was built on one component making it very fragile to any unpredicted shock?

In 2008 we had a financial system that was exactly like the example of the Venezuelan economy.

Let's go back to our main question.

What does this have to do with normalizing interest rates and the Fed’s BS today?

If we took interest rates, saying the fed funds, up to 6%, and the Fed did quantitative tightenings by selling their entire asset side of the BS down from $4.5 trillion to $800 billion, where we were prior to the Covid-19, the entire system would freeze.

Why?

Let’s think this through.

If a certain primary dealer bank has a bond they use in the repo market and they purchased it for $1,000, it’s yielding 1%.

Collateral, Interest Rates and The Repo Market

Keep in mind collateral is incredibly important because its the entire repo market, but the other side of it, how much collateral is in the system, is the interest rate.

Going back to the example, if they need $1,000 to make their debt payments, they would take their bond and exchange it for the cash, of course, there is a spread and other things, but I’m just using this as a basic example.

If interest rates normalize, let’s say they go from 1% to 7% on the bond, its value would go down to $300 because the value of the bond has an inverse relationship to the interest rate.

This means the amount of collateral in the system would go down.

If, for example, we have $2.2 trillion of collateral, with the normalization of interest rates, they would go to $500 billion.

To be clear, these are all hypothetical numbers.

The exact same thing that cost the 2008 situation, would happen today if the Fed were to normalize its interest rates.

If the amount of collateral shrinks down, institutions won't be able to get the liquidity they need and the whole financial system would go bankrupt, and that’s just the tip of the iceberg.

I haven’t even talked about the Fed reducing the size of its BS, taking all the collateral and selling them into the market, increasing interest rates even higher.

Interest rates rising are such a great deal that the Fed proved it when they came into the repo market on September 17th with guns and bazookas offering up to $1 trillion a day.

The Fed said it wasn't important, only a temporary glitch, yet, we’re in April now, and even without Covid-19, the Fed would still be in there propping up the repo market.

In other words, they’d be bringing down interest rates in the repo market, from 10% all the way down to where they wanted them, around fed funds.

If interest rates weren’t propping up the entire financial system, just like mortgage-backed securities were in 2008, the Fed never would’ve never done that.

They would’ve kept reducing the size of their BS. Their actions speak much louder than their words.

Also, I haven’t mentioned either, the biggest subprime borrower in human history, which is the government. They roll over and issue at least $10 trillion in debt.

What would happen if their interest rate went from 2% to 6%?

They can’t afford it! They would come crashing down. We would have a GFC 2.0 plus the government.

Back in 2008, we had a system where the “solution” was for the BS of the private sector to go on to the BS of the government and the Fed.

Today, we have a situation where all that debt is on the government’s BS, and if they have to roll it over, they can’t.

Our system is far more fragile today than it was back in 2008.

If interest rates normalized, and the Fed’s BS normalized, we would have a complete disaster.

At a very minimum, it would be GFC 2.0.

The economic collapse follows the financial bust

We already had kind of a top-down view by comprehending that normalizing interest rates and the Fed’s BS would have the same type of effect in the financial system than it did in 2008, if not worse.

Now, let’s look at it bottoms up. What would happen to the actual economy if the financial system was struggling and having problems?

First, let’s analyze the distribution of wealth in the United States population.

The boomers of our society have 57% of the overall wealth, of course, most of it is in their home equity and the stock or bond market.

Generation X has about 16% of the wealth, and millennials only have about 3%.

So if interest rates go from 0% to 6%, the price to earnings in the stock market would also have to adjust.

Assuming the CAPE ratio was at 30, before the Covid-19, it would most likely go down around 15, which means stock prices would get cut in half.

Also, if you look at a mortgage calculator, type today’s interest rate of 4.5%, if it goes up by 600 basis points, to 10.5%, the monthly payments would double, at the very minimum.

Therefore, it would be most likely home prices would get cut in half because it's all about the monthly payment.

So if the wealth for the baby boomers and the Generation X gets cut in half, what does that do to consumer spending?

One man’s spending is another man’s income, so if there’s a lot less spending because they don’t have the same purchasing power anymore, the GDP would go down substantially, if this happens, unemployment would go up, and tax revenues would also go down.

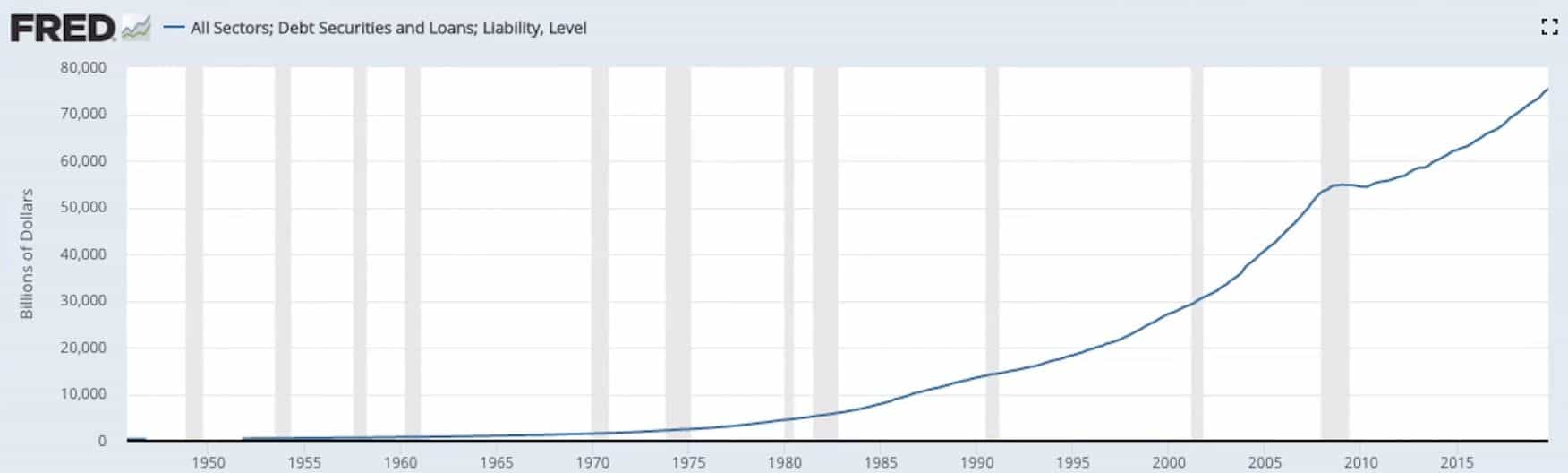

This is easy to understand by looking at two charts combined into one: the overall outstanding debt in all sectors in the United States.

This chart compiles consumer and sovereign debt, which goes all the way up to $75 trillion, but what’s the income or what source of revenue do we have to service the debt?

Well… that’s GDP. Look at where GDP is, $23 trillion.

These charts go back to 1950, notice the GDP along with the debt in the overall economy, at the sovereign level and the private sector were the same, if not GDP a little bit higher.

But, after 1980, the completely diverged.

GDP grows, but at a much slower pace than the debt going completely parabolic.

You may be asking yourself how is this possible? And, what has happened since 1980?

Well… Interest rates have continually gone down, we’ve been in a 40-year down cycle in interest rates which has allowed us to increase the debt exponentially while the income or the ability to service the debt hasn’t grown at the same pace.

In other words, our entire system, the whole economy is based on extremely low-interest rates.

So if interest rates went from 0% to 6% or increased in the overall economy, it would be time to pay the fiddler.

The exponential growth in the debt would have to come crashing down to some level where it was serviceable by the amount of income in the economy.

The problem is we’d have a doom vortex. If the debt comes down, so would the income because the economy is built on asset bubbles, debt, and confidence.

If the debt comes down, so will asset bubbles and confidence.

In Luke Gromen and Erik Townsend words:

“If the Fed just let markets work like Powell said he wanted to do, repo would go to 10% or more, and the U.S. government would need to roll $6 trillion or so in the next six months at 10% plus, and the U.S. government can’t, can’t, can’t afford to roll that much money at 10% plus.

Especially since at 10% plus, the highly financialized U.S. economy would collapse, so the financing needs would nonlinearly go from $6 trillion to $10 trillion over the next six months as tax receipts collapse.

Mortgages would be at 12% plus, so we’d have housing collapse, the banking system would likely quickly follow, and corporate debt issuance would grind to a halt with repo at 10%.

They can’t afford to roll any of it at 10% plus, so U.S corporate debt issuance would begin defaulting, which with corporate leverage as high as it is, could quickly wipe out significant portions if not the majority of the equity market cap of the United States and the world!

Remember, as we noted in multiple times, in the U.S. equity market cap is 160% of GDP and net capital gains plus taxable IRS distributions alone, are around 200% of annual growth, and personal consumption expenditures, which itself is two-thirds of GDP.

In plain English, there’s no economy in the U.S or the world if U.S. stocks crash, and that’s not hyperbole, its just sixth-grade math. ”

Yet, there’s room for other questions: If the Fed wouldn’t have raised interest rates back in 2005 from 1% to 5%, would we have had the GFC?

Would those subprime borrowers been able to make their payments?

Would home prices continually have gone up?

Maybe we could’ve avoided the entire GFC by keeping interest rates low and gradually taking them down further until they got to zero, and just stayed the course.

Maybe we could’ve avoided the entire thing if we just would’ve started quantitative easing, ZIRP, or maybe even negative interest rates.

We never would have had a housing bust, but just because we might not have had a bust, it doesn’t mean the system in 2008 was stable.

We know it by looking back in retrospect, once they took interest rates up to 5%, and tried to normalize, the entire system came crashing down.

Why is today any different, when the debt in the system, the government, state, corporate, and consumer debt is far greater than it was in 2008?

The system was broken back then, and it’s even more broken, unstable, and fragile today.

Just like mortgage-backed securities were the pin catalyst in 2008 along with interest rates, the pin and the catalyst today is just the Covid-19, not the cause.

We know this by doing the thought experiment we just did of what would happen in the financial markets, systems, and the real economy if we just took rates and the Fed’s BS back to where they were in 2008.

The real problem isn’t the pin or the catalyst, its the structural problems, the underlying problems we have with the economy itself.

Whether it was mortgage-backed securities or Covid-19, it doesn’t matter, sooner or later, a system that is broken will finally break.

Can the Fed save us from economic collapse by reinflating the everything bubble?

To understand the probabilities and possibilities of the Fed pulling this off, we need to understand their game plan.

In my opinion, their plan is to buy everything in sight, equities, debt, and real estate in the form of mortgage-backed securities.

They’re going to try and get it all on to their BS.

As an example, they just set up the Foreign International Monetary Authority Program (FIMA), which is basically, the repo market outside of the United States.

It’s the Fed asking the central banks to stop selling the treasuries, and in turn, buying them in exchange for the dollars they need to satisfy their dollar-denominated debt.

I think the Fed will do this to the entire system outside and inside the U.S.

They’re taking any asset that might get a haircut from the primary dealers and even the individuals and the private sector in exchange for cash.

Their goal is to never have a seller because if there’s never one, prices won’t go down.

So we would have real estate, bonds, and stock markets in the clouds.

This way, the Fed achieves its objective of reinflating and maintaining the everything bubble.

That’s their game plan.

I think is the economy will struggle on a moving forward basis, we’ve inflated what we call the everything bubble which is a direct result of the Fed’s interventions going back to the late 80s when they tried to fix the dot com bust or paper over it by inflating the housing bubble.

Then in 2008, they had to create another asset bubble, and that’s where we are today.

What they’re trying to do is get as much of the private sector balance sheet on to theirs because if those assets take a 50% haircut, theoretically it’s not going to affect the economy, which is very dependant on the asset prices staying high.

The question is now, what are the knock-on effects of the Fed taking its BS to $10 trillion, $20 trillion, you name it?

Also, I think the release valve in the long term is definitely going to be the dollar.

So to answer the question, I would have to say yes.

I think it’s possible the Fed reinflates the everything bubble, yet I don’t think it’s probable.

But, what we have to remember is even if they do reinflate the everything bubble and asset prices go back to where they were, it doesn’t mean they fixed the economy.

The economy is still broken, just like it was in 2008.

For more content like this, take a look at my blog and I will help you build wealth and thrive in a world of out of control central banks and big governments.