The current state of the United States is causing a lot of anxiety among its citizens.

With the ongoing social unrest, rioting, looting, and even the possibility of martial law, it's natural to feel a sense of unease.

However, it's important to stay calm and level-headed during these times.

While it's always good to hope for the best, preparing for the worst is equally important. This is especially true if you're trying to be smart about your financial future and that of your family.

To do this, assessing your potential risks and rewards is important. When investing or speculating, you want to aim for asymmetry – meaning you want to have minimal downside risk but a significant potential for upside gains.

When it comes to your financial future, everything you plan should be looked at through a risk/reward lens. You always want the reward to be much bigger than the risk.

[ctt template=”3″ link=”3mg0P” via=”no” ]When it comes to your financial future, everything you plan should be looked at through a risk/reward lens. You always want the reward to be much bigger than the risk.[/ctt]

In this post, I'll give you three practical steps and some bonuses to help you preserve and protect your financial future.

These steps will help you assess your current financial situation, create a plan to minimize your risks and identify potential opportunities for growth and success.

[ctt template=”3″ link=”Yrq41″ via=”no” ]If you haven't done so already, assess your current financial situation, create a plan to minimize your risks and identify potential opportunities for growth and success.[/ctt]

By following these steps, you'll be better prepared to face any potential challenges that may arise.

But first, let’s first have a thought-provoking discussion about your financial future.

Understanding the Importance of Planning For Your Financial Future

Planning for one's financial future is important for several reasons. First, it allows individuals to set achievable financial goals and prioritize their spending and saving habits accordingly.

Without a plan, it can be challenging to determine where to allocate resources and which financial goals to pursue.

[ctt template=”3″ link=”oE59d” via=”no” ]Without a plan, it can be challenging to determine where to allocate resources and which financial goals to pursue.[/ctt]

Second, financial planning enables individuals to prepare for unexpected events such as job loss, illness, or other emergencies.

With a financial plan, individuals can build an emergency fund, secure adequate insurance coverage, and make other provisions to mitigate potential financial risks.

Third, financial planning can help individuals maximize their wealth and achieve long-term financial security. Individuals can grow their assets and build retirement funds by developing and implementing a sound investment strategy.

Financial planning provides a roadmap for individuals to achieve their financial goals, protect their financial security, and build long-term wealth. It can be a valuable tool for anyone, regardless of their income or financial situation.

You don’t have to be an expert (that’s what your financial advisor is for), but you should have a basic understanding of financial planning and your various options. If you need help, then seek out a certified financial planner.

Planning your financial future can be daunting, but asking yourself the right questions can help you get started. Here are some questions to consider:

-

What are my financial goals? Do I want to save for retirement, pay off debt, buy a house, start a business, or travel the world?

-

What is my current financial situation? How much do I earn, how much do I owe, and how much do I have saved?

-

What are my expenses? How much do I spend on housing, food, transportation, entertainment, and other categories?

-

What is my risk tolerance? Am I comfortable with investing in high-risk/high-reward opportunities, or do I prefer low-risk investments?

-

What is my investment strategy? Do I want to invest in stocks, bonds, real estate, or other assets?

-

How much do I need to save each month to reach my financial goals?

-

Do I have an emergency fund? How much do I need to save to cover unexpected expenses?

-

Do I have any debts? How can I pay them off as quickly and efficiently as possible?

-

What is my timeline for achieving my financial goals?

-

Am I comfortable with my current financial plan, or do I need to make changes to achieve my goals?

Smart Saving Goals for a Secure Financial Future

Smart saving goals are an essential component of securing your financial future.

They can help you stay on track with your expenses, build your savings, and ultimately achieve your long-term financial goals. Here are some smart saving goals to consider:

Emergency Fund: Building an emergency fund is a crucial goal for anyone. It is recommended to save three to six months' worth of living expenses to protect yourself from unexpected expenses, job loss, or medical emergencies.

Retirement Fund: Saving for retirement is important to secure your future. A good rule of thumb is to save 15% of your pre-tax income in a 401(k) or IRA. Starting early and regularly contributing to your retirement fund can help you achieve a comfortable retirement.

Debt Reduction: Paying off high-interest debt, such as credit cards or personal loans, should be a priority. Make a plan to pay off your debt, starting with the highest interest rate first. This will reduce the burden of debt and save you money on interest payments.

Education Fund: Saving for education for yourself or your children is a smart long-term goal. Consider setting up a 529 plan or other tax-advantaged savings account to save for college expenses.

Down Payment on a House: If you plan to buy a house, consider saving for a down payment. A 20% down payment can help you avoid private mortgage insurance (PMI) and save money on interest payments.

Setting and achieving smart saving goals can help you stay financially secure and achieve your long-term financial goals.

Start by identifying your financial priorities and creating a plan to achieve them.

Remember to track your progress and make adjustments as needed regularly.

Establish a Budget for Better Financial Planning

Establishing a budget is one of the most important things you can do to improve your financial planning.

A budget can help you track your income and expenses so you know exactly where your money is going each month.

This can help you identify areas where you can cut back on spending, so you can put more money towards goals like savings, investments, or paying down debt.

Remember: You can save for multiple goals at the same time!

To establish a budget, start by tracking all of your expenses for a month or two. This can include everything from rent and utilities to groceries, entertainment, and transportation.

Once you have a clear picture of your monthly expenses, you can compare them to your income to see if you are spending more than you earn.

If you spend more than you earn, it may be time to make changes. Look for areas where you can cut back on spending, such as eating out less often, canceling unnecessary subscriptions, or reducing your energy consumption.

You can also look for ways to increase your income, such as asking for a raise, taking on a side hustle, or selling items you no longer need.

Once you have established a budget, it is important to stick to it. This means tracking your expenses regularly, avoiding unnecessary purchases, and being mindful of your spending habits.

Over time, you will likely find that you have more money available for savings and investments, which can help you build a stronger financial future.

Avoid or reduce your debt, including student loans – It helps to organize your debt so that you can plan how you will pay down each debt and track your progress.

Financial Future Hack #1 – Protect Your Home Equity

Protecting home equity is crucial for building long-term wealth and securing one's financial future. Home equity is the difference between the value of a home and the outstanding mortgage balance.

Home equity increases as home values increase, making it an essential part of one's net worth. By protecting home equity, homeowners can ensure that they have a valuable asset that can be used for future financial endeavors, such as funding a child's education or retirement.

One way to protect home equity is to make mortgage payments on time and avoid defaulting on the loan. Late or missed payments can result in penalties and even foreclosure, which can quickly erode home equity.

Another way to protect home equity is to make additional payments toward the mortgage's principal balance. This can reduce the amount of interest paid over the life of the loan and accelerate the payoff date, increasing home equity faster.

Maintaining and improving the condition of the home is another way to protect home equity.

Regular home maintenance, such as roof repairs and HVAC maintenance, can prevent costly repairs down the road and help maintain the value of the property.

Improving the home through renovations or additions can also increase home equity, but it's important to ensure that the cost of improvements doesn't exceed the potential increase in home value.

Finally, ensuring that the home is properly insured can protect home equity in the event of a natural disaster or other unforeseen circumstances.

Homeowners should review their insurance policies regularly to ensure that they have adequate coverage for the value of the home and its contents.

By protecting home equity, homeowners can secure their financial future and have a valuable asset to rely on when needed.

Should You Sell Your Home or Stay Put?

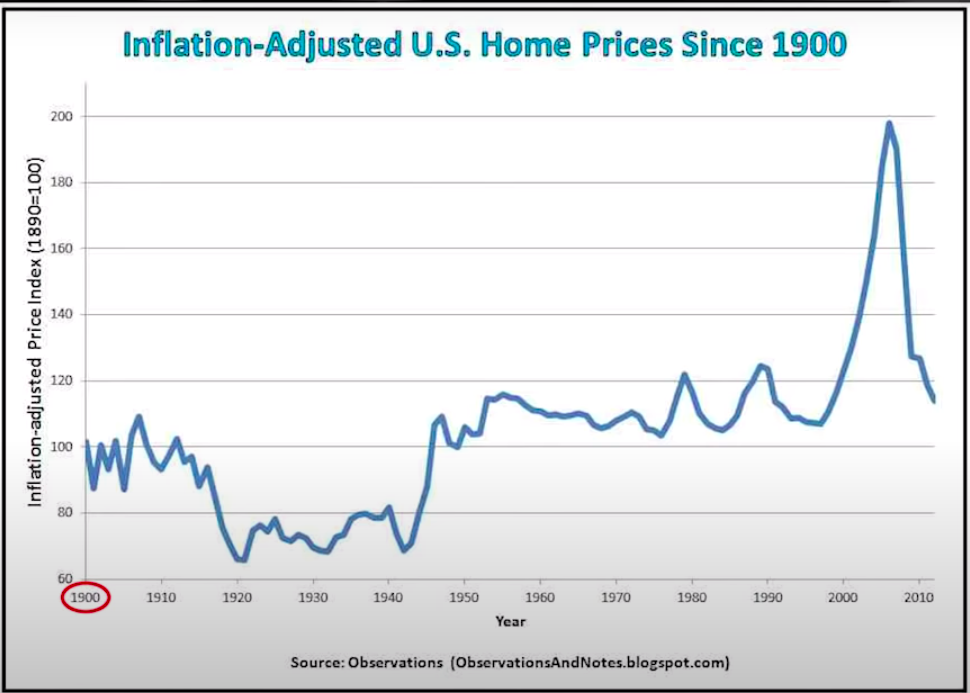

I wanted to start with this chart going all the way back to 1900 of home prices in the United States adjusted for size and inflation. Understanding home prices helps you understand where you stand with respect to home equity.

You might live in a State, city, or neighborhood that’s poised for a big crash. Or you could live in a linear market that’s safe.

Understanding where you fit into the housing market could help you determine whether or not it is wise to free up that equity by selling and moving to a better location or staying put.

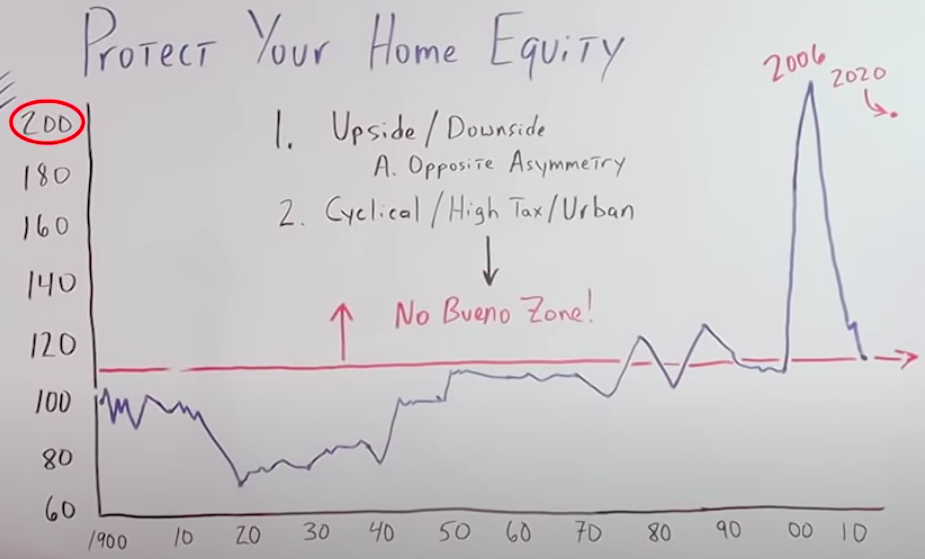

This chart is one of my favorites. It goes from 1900 to 2010, and on the left, from 60 to 200.

In 1900, it started off right around the 100 mark, stayed consistent, and went down to 1920, notice that it was after the Spanish flu and World War I. Then, it stayed very low until World War II.

It popped back up to about its historical average and remained consistent until 2000. Please note that home prices didn't go up or down for a hundred years in the United States. It stays the same when you adjust for inflation and size.

Most people, I think, would be shocked by that information alone. But…

What happened to House prices in 2000?

Well, of course, we got into a housing bubble. Prices went parabolic all the way to 2006 and then they came crashing down till they bottomed out around 2012.

Where did housing prices bottom out?

Of course, on their historical trend line.

What is the no bueno zone?

I use this term a lot in most of my videos and articles. The no bueno zone is when things start to get expensive; you can see that from the red line on the whiteboard. That's when we're getting into the no-bueno zone.

When we are below the line, prices are pretty darn cheap, but if we are above the line, we're in the no-bueno zone.

Can you remind me where we were on Earth in 2006?

We were in the no bueno zone stratosphere. After noticing this, the question becomes:

Where are housing prices in 2020? Almost as high as we were in 2006.

In fact, in some markets, prices are even higher. I don't think anyone would dispute if we were in a bubble in 2006.

How are we not in a housing bubble today?

Prices are almost the exact same.

If you're trying to be intelligent with your financial future and the financial future of your family, you have to look at your upside and your downside.

When we're investing or speculating, we want asymmetry, which means very little downside and a lot of upsides.

Currently, the state of home prices is quite different. The asymmetry has completely flipped, resulting in minimal upside and the potential for significant downside, with potential losses of 50%, 60%, or even 70% when adjusted for inflation.

If you live in one of these cyclical high tax, urban areas, you really want to think about selling.

Right now in the United States with social unrest, looting, rioting…

Do you really want to have your home equity, potentially the majority of your net worth, in one of these urban areas?

And let's not forget about taxes. The states are broke.

I can almost guarantee you that in the future, they're going to be jacking your property taxes and putting in additional sales tax. They're going to get desperate and you're going to have a target on your back.

My best advice is to consider selling now to protect yourself or move your equity. If you can't sell, maybe you can take equity out in the form of a refinance.

I know it's not right for everybody, but I think it's something you need to start considering, especially if you live in one of these markets.

What can you do with your home equity?

First and foremost, keep some dry powder for heaven's sake. You might be able to move that equity to a more linear market where you can get a better RV ratio.

Maybe you can buy some rental properties or cheap dividend-paying stocks, which pays you to own. I'm not saying rush right out and buy these things immediately.

I'm saying start paying attention, protect your equity now. Get it in some dry powder and just let the market come to you. Be very patient.

I think over the next year or two, prices are going to come to you. You don't have to chase them.

What everybody can do, regardless of whether or not they can sell, is they can at least make sure their mortgage is a 30-year fixed rate.

Make sure that you have a short against the U.S. dollar. Hopefully, if we get some inflation, which we most likely will over the long-term, 10, 15 years, you'll be able to pay back your mortgage with cheaper dollars. That's a transfer of wealth from the bank to you.

Also, think about consumer debt. You really want to eliminate as much as possible. I don't think now is the time to go out and run up the credit card on consumption, especially because it's not a fixed rate.

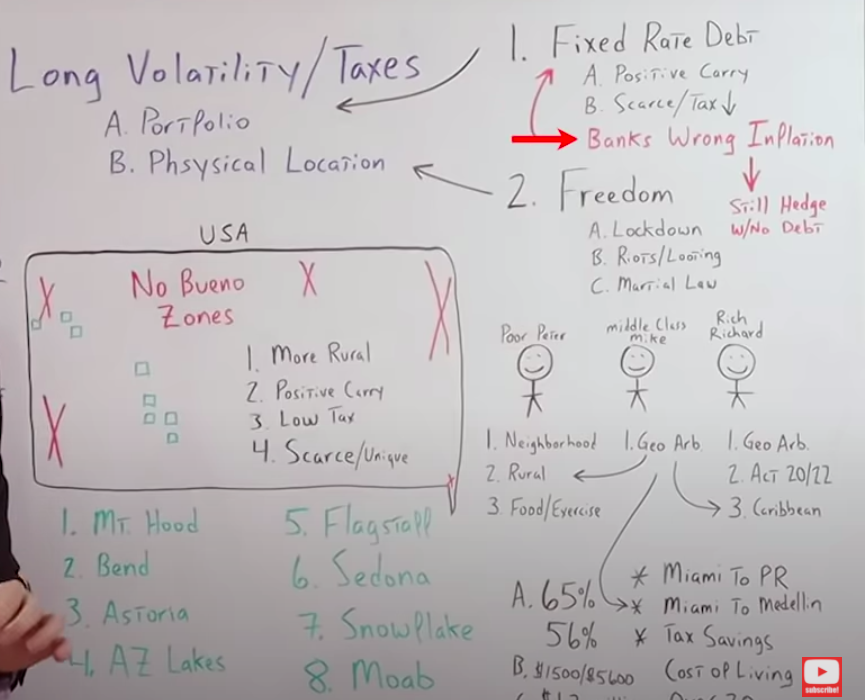

Financial Future Hack #2: Go Long On Volatility And Taxes

I'm not just talking about going long on volatility with your portfolio but also with your physical location. More than just your financial future is on the line here.

Here is a transcript from a recent Real Vision interview with Raoul Paul and Hugh Hendry to see how the pros are executing this in their portfolio and their personal lives.

Going Long Volatility To Secure Your Financial Future Like A Pro

Ripping a Page Out of Hugh Hendry’s PlayBook:

Hugh Hendry: Last year, I borrowed five million euros, 20 years fixed, and I paid a 2% interest rate, and 2% was the wrong figure. Interest costs should have been like 1.3%, but I was like, “Whatever. Hit me, hit me, hit me.”

Let me just say that again, I borrowed five million euros to buy a property in St. Bart's, and a French bank was willing to lend me fixed. That is assuming the euro.

That's a world where gold will go to $3,000 because it will be difficult. But there's enough financial lubrication that it won't be the 1930s, but it's going to be a world of zero interest rates for a long time.

I just don't think banks are that smart. I think they've got that wrong, and I think they've got that wrong, like their German cousins after the First World War.

(End Of Transcript)

I know what you're saying, “George, I can't buy property in the Caribbean. This is pointless.”

But I can promise you, this is very applicable to the average Joe and Jane in the United States.

We first have to understand the concept behind why Hugh did what he did.

First, Hugh took out fixed-rate long-term debt to buy a hard asset that gave him a positive carry.

In other words, positive cash flow. This asset was scarce and it was in a jurisdiction where the tax rates were very low.

Hugh Hendry points out that he thinks banks are going to be on the wrong side of history, just like they were in Germany right after World War I.

What he means by that specifically is 1920s Weimar Germany hyperinflation.

As long as you buy an asset in this category, even if you don't use debt, maybe you're a person that really doesn't like debt and I totally respect that, but if you pay cash for it, I still think it's going to be a great hedge long-term.

Even if we don't get hyperinflation in the United States over the next 10, 15, or 20 years, the probabilities are very high that we'll at least get substantial inflation like the 1970s.

Even for the guys and gals that are dollar bulls right now, over the short term, even up to 5 years, I think that the dollar is headed down in value. In other words, we're going to get a lot of price inflation over the long term.

Improving Both Freedom and Cashflow

This strategy is also about improving your freedom and getting a place where you don't have to worry as much about going into lockdown, riots, looting, or even martial law.

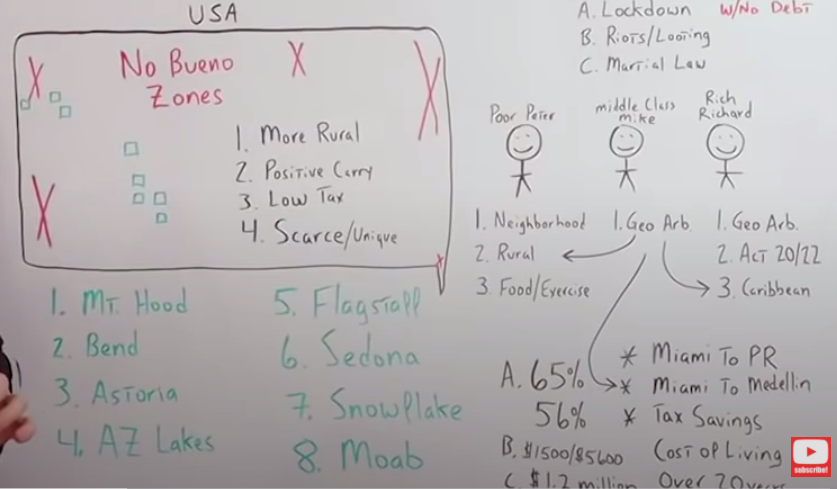

Now, let's go over some specific, actionable ideas you can implement. Look at the three characters on the board.

There is poor Peter, middle-class Mike, and rich Richard. Poor Peter doesn't have as much flexibility, but he does have some options.

He can move to a better neighborhood, maybe not just a better one, but a neighborhood where more people living there own their property.

Why you should Live In Homeowner-Occupied Neighborhoods

People are much less likely to burn down a property they own and live in. You can also go into a more rural area with some space to grow some food and at least get some exercise and fresh air.

Examples of this in the United States are the no bueno zones we talked about in finance future hack number one. Those are the big cyclical markets, urban areas, and high tax zones.

But there are some areas where you could find some opportunity.

Some of the places that came to mind for me, and again, you can apply this to whatever geographical location you're most familiar with, Mount Hood, Bend, Astoria, Oregon, Arizona lakes, Flagstaff, Sedona, huge for tourism, and Snowflake are one of my favorite places on earth. Also Moab and Utah.

All of these locations are going to have properties that are very scarce and unique. But remember, it's also about cash flow, so we have to get creative. It's going to be hard work, that's for sure.

There's no easy way out. It's not the 1980s when you could buy a 10-year treasury and get a 10% yield all day long. So to get more cash flow, you can aim at farming, maybe hunting…

I have friends in the Midwest who own a lot of property and they lease it to deer hunters. A bed and breakfast, or maybe an Airbnb.

My buddy, Eric with Macro Voices, has a fantastic spread on the Northeastern coast, kind of a bug-out place for people wanting to get out of the insanity of New York City. Maybe a rural business.

I also have friends in the Grand Canyon that bought property there, setting up a campground for these specialty RVs called Airstreams and Shasta.

My sister lived on a hundred-acre vineyard and just sold it. The bottom line is you have to use your imagination.

As I was going through the whiteboard and drawing this, something really crazy, way outside the box, came to my mind.

If interest rates go negative, you can get into a rural location and set up a facility for gold, silver, or cash storage.

Next is middle-class Mike. He has all the options we just outlined for poor Peter, but maybe he has some more flexibility.

He works online. Maybe he's a retiree getting social security or has a pension fund, so he can look at geo arbitrage. Geographical arbitrage.

Hat tip to my good buddy, Jason Hartman, who came up with that term. It refers to moving to a different country because you improve your freedom, lower your taxes, and increase your purchasing power substantially.

Comparing Cost Of Living – Miami, FL vs Medellin Colombia

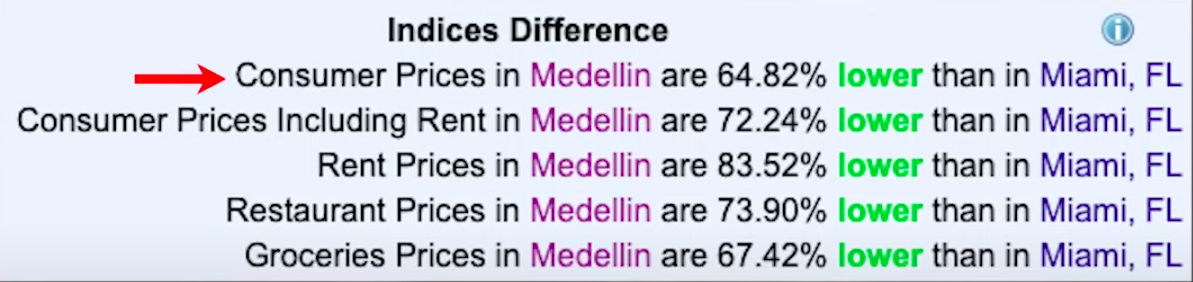

For example, I ran some numbers comparing Miami to where I am now in Medellin, Colombia. The cost of living in Medellin is 65% lower than it is in Miami.

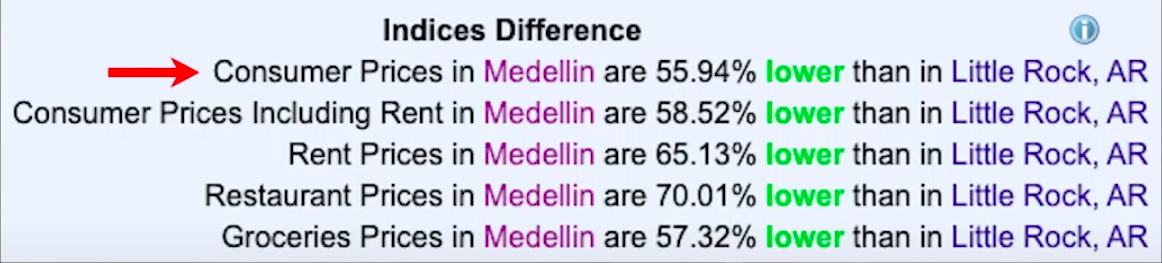

I know what you're saying, “George, well, Miami is a really expensive place.” Okay, fine. Medellin is 56% lower than Little Rock, Arkansas.

To put this into dollars and cents so we can really understand it, in Medellin, if you had $1,500 a month, you'd have the same purchasing power as if you had $5,600 a month in Miami.

And it becomes even better when you go over to rich Richard.

Yes, he has all of the options I have mentioned and the geo arbitrage, but he also acts 20 and 22 in Puerto Rico, which could take his tax rate to whatever he's paying in the United States down to 0% in Puerto Rico, also 0% potentially on some capital gains.

He also has the options Raoul and Hugh discussed for the Caribbean. But to add some numbers to rich Richard, let's say he's making $100,000 in the United States. His effective tax rate is 20%. That means he's saving $20,000 a year by moving to Puerto Rico.

When you add that to his cost savings for the cost of living and a 5% per year return over 20 years, rich Richard would save $1.2 million.

This is why you need to understand the concepts we're talking about, like going long volatility, whether it's for your portfolio or your physical location to improve your freedom and your security.

For poor Peter, it's a great idea. For middle-class Mike, it's a fantastic idea; for rich Richard, it's a no-brainer.

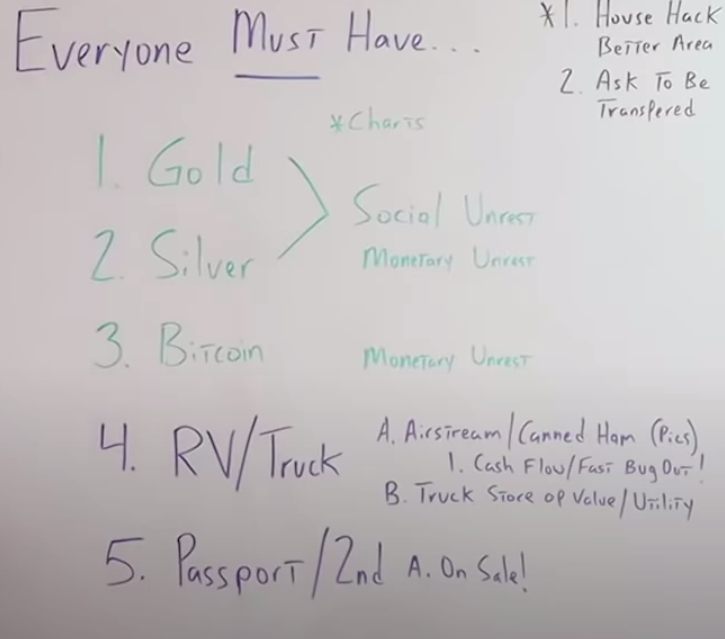

I forgot a couple of things for poor Peter. When I was looking at my notes, I realized it might not be realistic for him to buy property in Moab, Bend, Mount Hood, Sedona, or something like that.

But I think there are a few things that he could do in addition to try to move to an area or a neighborhood where there are more owner-occupants.

-

You can house hack because it's the best financial advice I can give to anybody. You can use the money you would've spent on rent or your mortgage payment to build up some savings and invest for the future.

2. You can ask to be transferred. Maybe you're in one of these places like San Francisco, L.A., New York, Baltimore, Chicago, or in one of these urban areas with high taxes that you just want no part of it.

Why don't you ask your company if you can transfer to a different location?

Maybe you work for a big corporation that could transfer you up to Bend, Oregon, maybe Billings, Montana, Boise, Idaho, someplace where you can have a lot more peace of mind, not only from a personal security standpoint but a financial standpoint as well.

Financial Future Hack #3: The Items Everybody Must Have

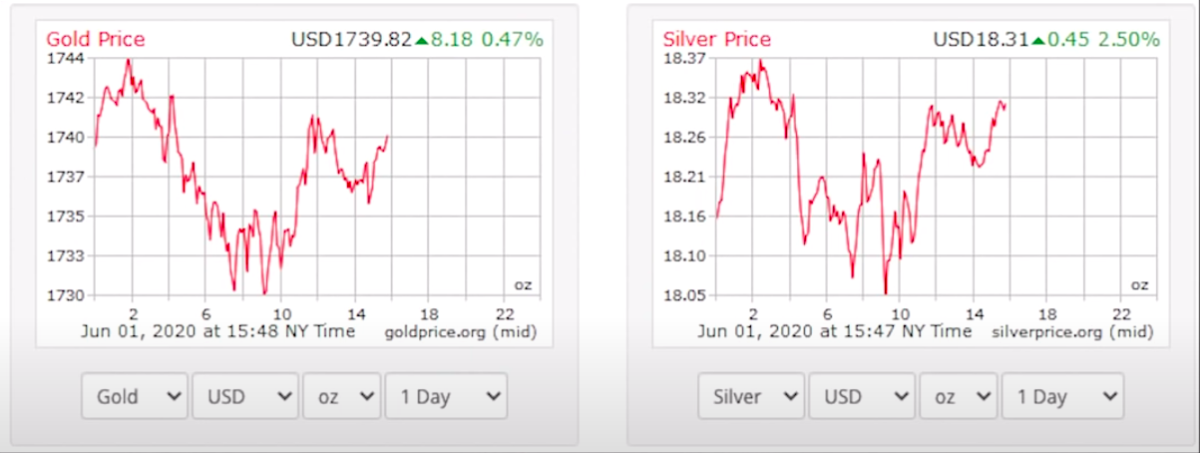

You know what I'm going to talk about… Of course, that's gold, silver, and bitcoins, things I definitely think everyone should own, but for many different reasons. Those of you who read my articles know exactly what I am talking about.

During the month of June of this year, I was looking at some charts over the weekend, and gold and silver opened up the futures market around five o'clock on Sunday like this:

Bitcoin trades 24/7, and I noticed gold and silver were up, but Bitcoin over the weekend was actually down.

It was actually up during that month and I'm not saying this is going to happen indefinitely in the future, but it got me thinking that gold and silver are obviously fantastic hedges against social unrest.

Especially the type of unrest where people just want to bug out and get to the country and just hang out for a while, maybe barter back and forth with something they know has had value for the last 5,000 years.

Bitcoin seems to be maybe for monetary unrest. For example, we have seen hyperinflation in Venezuela or when they put up capital controls like China, where they won't let you take yours out of the country.

Now let's go over some items that I can promise you nobody talks about.

You're definitely not going to hear this on Real Vision, that's for sure.

Own a Bugout Escape Vehicle With Trailer In-Tow

I think everybody, whether it's poor Peter, rich Richard, or middle-class Mike, should have an RV and a good old-fashioned diesel truck in their driveway.

Think about it.

-

Why not?

-

Wouldn't you want an RV parked in your driveway, ready to go, stocked with food so you can hop in, drive right out to the mountains, the lake, and just watch everything happen from a distance?

Also, you can make a lot of money with these things. I've owned several Airstreams in the past.

My friends have made a lot of money with Airstreams and canned hams, or those Shastas. Everybody loves those things with the wings in the back. You can actually cash flow them.

When they're in your driveway, you can rent them out nightly on Airbnb or there are specific websites that do peer-to-peer RV rental.

This is what's so cool about this is it's not only a way to have some freedom and get outside of the chaos if necessary on a moment's notice, but it's a way to increase your cash flow and make a little bit of money.

Also, with the trucks, I think they're a great store of value if you get the right ones, those 1990s Dodge Cummins and the Ford Power Strokes.

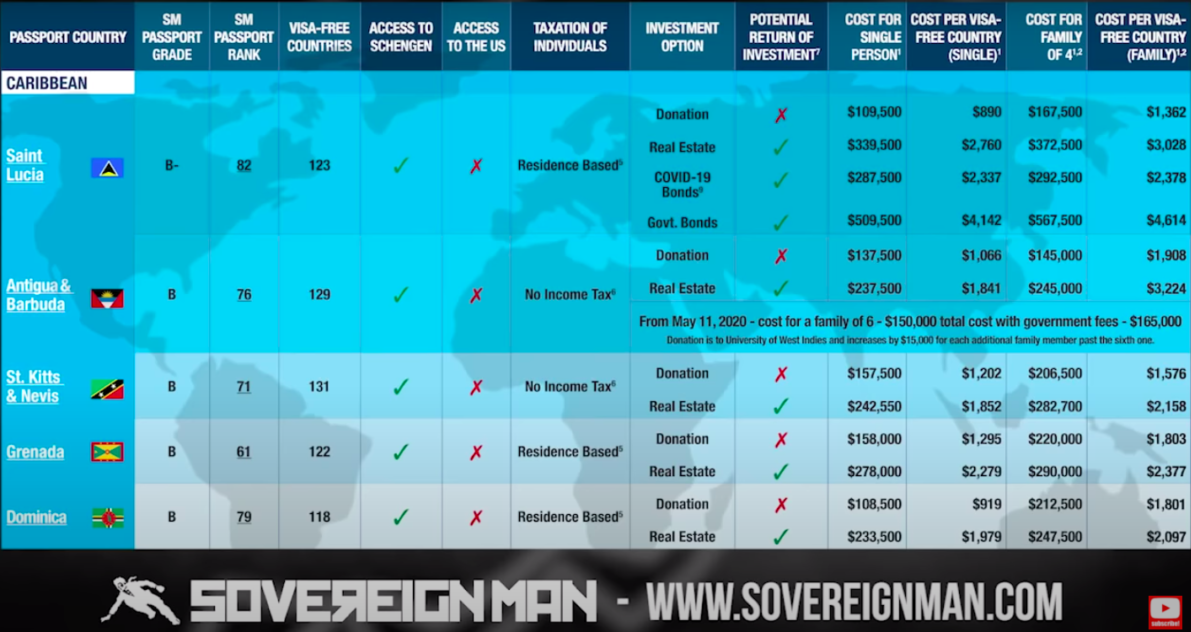

Lastly, every American must have a passport, and I would suggest getting a second one.

Here are some of the countries in the Caribbean where you can get a second passport with an investment in bonds or maybe real estate.

You can just purchase them outright. These passports are on sale right now, big time, because the islands don't have any revenue from tourism because of the Coronavirus, so many of these passports are half-priced.

Places like Antigua, St. Kitts, and Dominica are all on sale, and I know they might look a little pricey, but remember, they're probably half of what they were two or three months ago.

I know this isn't right for everybody, but even if you're a die-hard patriotic American, you're all about the red, white, and blue, I can totally respect that, but I think it's something you should consider.

If you had a second passport sitting in your drawer right now, you have to ask yourself…

What's the downside?

There is absolutely no downside and almost limitless upside.

Remember what we always like to find in our investments or speculations: Asymmetry. And I don't think there's anything that has more asymmetry than having a second passport right now, especially when you consider what's going on in the United States.

Comments are closed.