Will the Car Markets Subprime Auto Loans Trigger Another Financial Meltdown?

The new and used car market has been one of the most important components of the economy for years, but lately, investors have had reason to be wary.

As subprime auto loans had become more and more common during the pandemic, there's increasing concern that we may now be looking at another financial meltdown in 2023 that could be on par with 2008. However, this time caused by subprime used car and truck buyers rather than subprime homebuyers!

With financial news outlets abuzz with stories about the impending doom of the used car market, it's no surprise investors are asking, ‘will subprime auto loans trigger another financial meltdown?

We'll take a look at what history can tell us as well as some key facts and figures to try and answer this question.

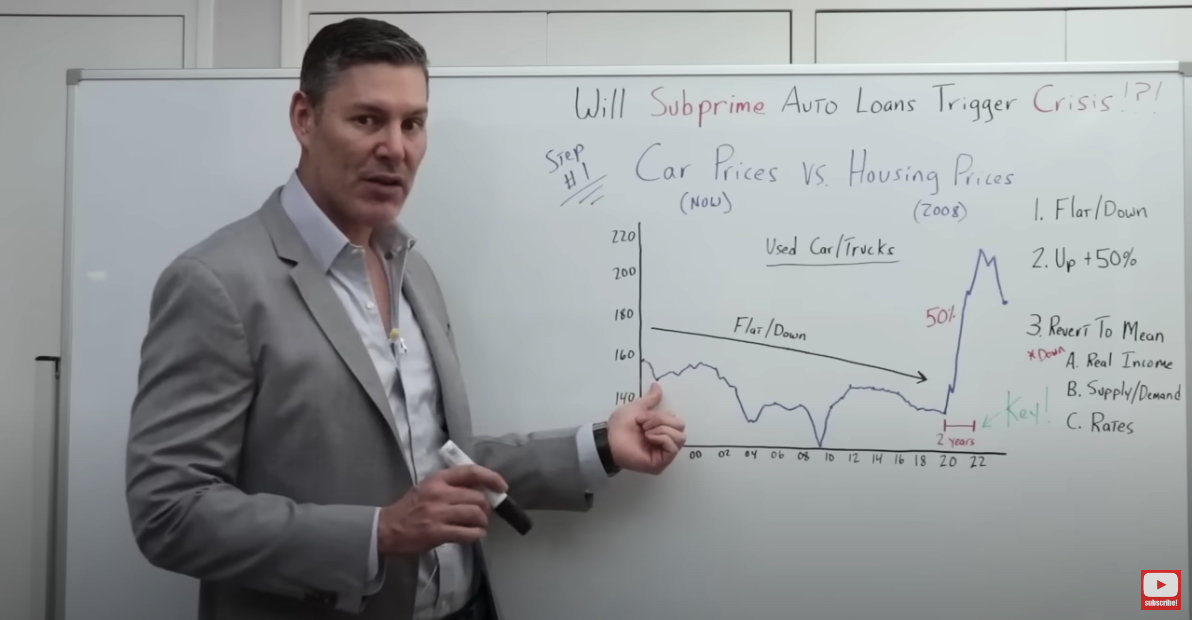

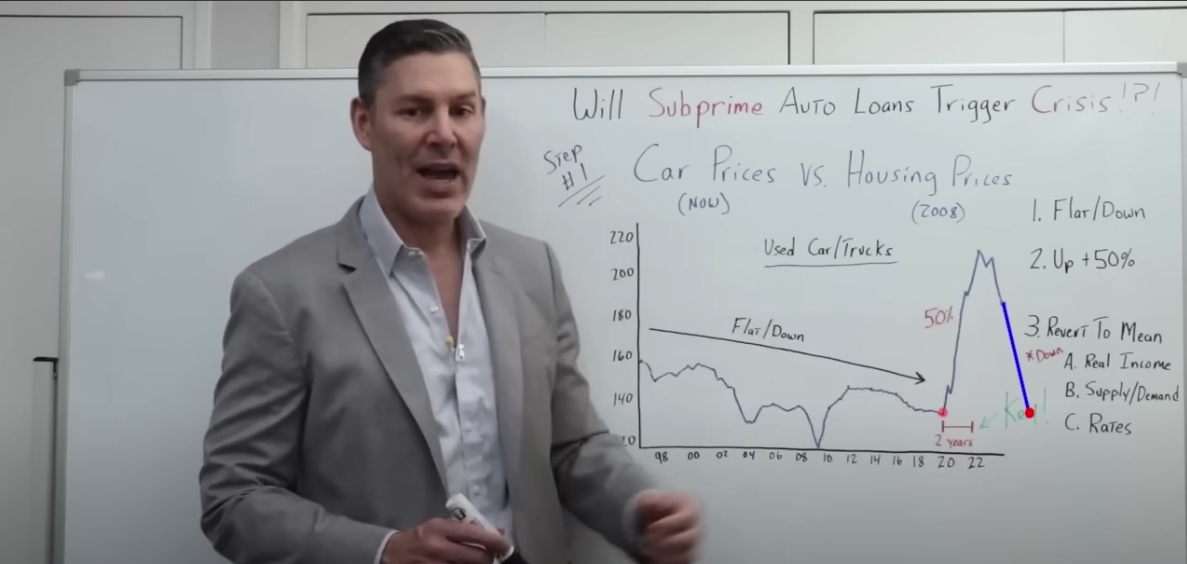

Looking At Car Prices

Look at car prices and how they've fared compared to homes leading up to 2008.

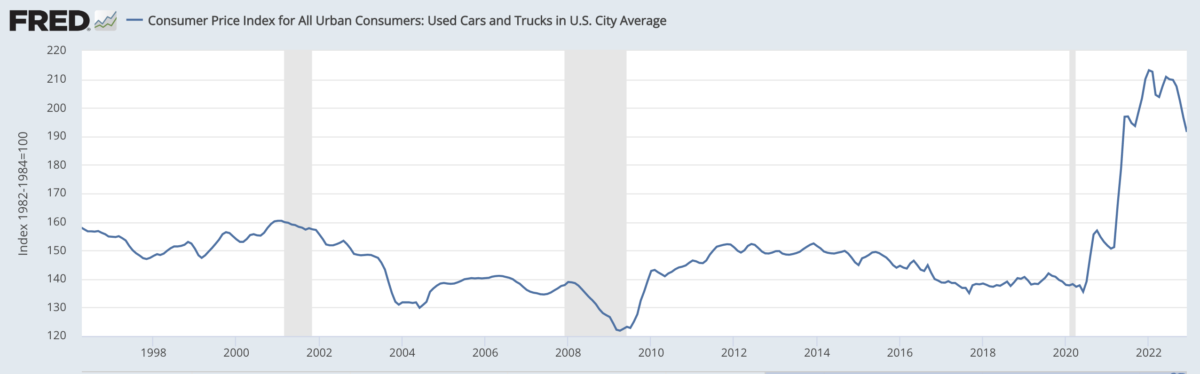

We can track them back until 1997, when their index value was around 160 on our inflation-adjusted scale going from 120 – 220; that spans right up until today!

1997 was the year when used car and truck prices were at their peak. But then, enter the dotcom bust, stampeding these vehicle price indices down like a hot potato! After surviving an economic recession and clambering back up again, it seemed as if things had calmed…

That was until 2020 hit us with yet another curveball, sending those same car & truck values skyrocketing over 50%. Higher than ever!

The dotcom bust, sometimes referred to as the dot-com bubble burst or the internet crash of 2000, refers to a massive economic crash in the early years of the 21st century. It was caused by an investment craze and speculation in stocks of dot-com companies during the late 1990s, leading to a significant drop in stock prices.

And you might say, “George, okay, well, why is that such a big deal?”

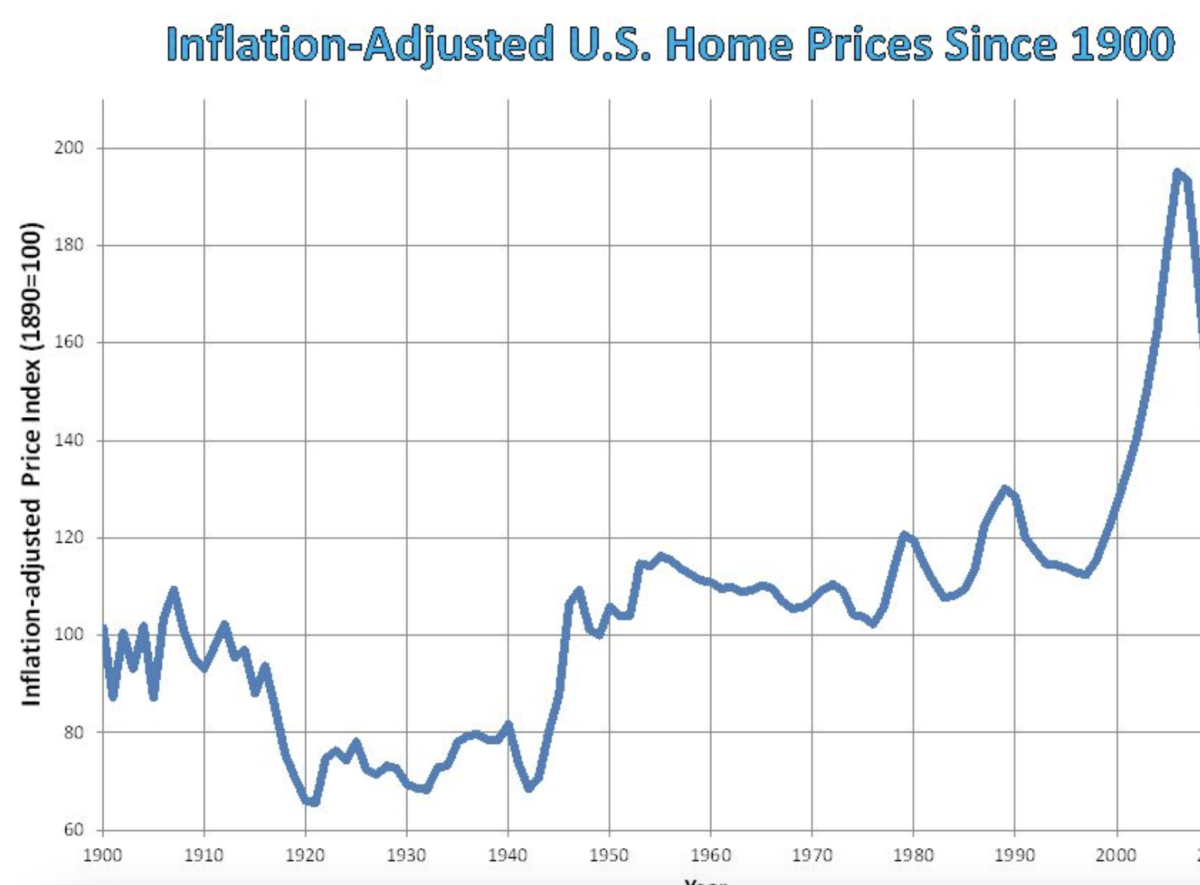

Here's a chart of housing prices adjusted for inflation.

You may be wondering what all the fuss about housing prices is, so let me explain.

It's like a game of musical chairs: in 1998 & 1999, everyone wanted to jump into the party, and by 2006, there were more people on board than available seats… and everybody scrambled for an exit! The price increase was wild, then it took six years to unwind.

Fast forward twenty-plus years later, and we can see history repeating itself – only this time at lightning speed, with similar results achieved in just two short years.

[ctt template=”5″ link=”ST675″ via=”no” ]Fast forward twenty-plus years post-dot-com bust, we can see history repeating itself – only this time at lightning speed, with similar results achieved in just two short years. #carmarket[/ctt]

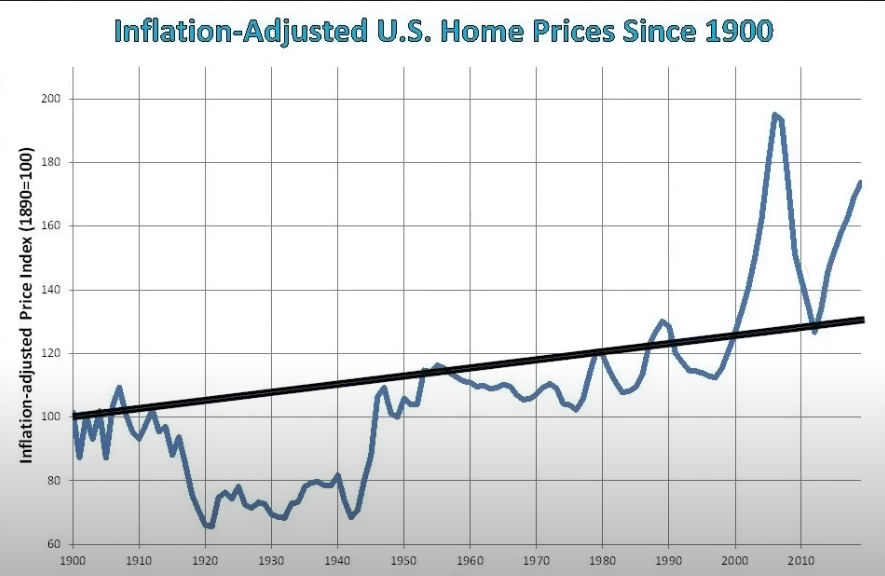

So one thing I want to point out here is that these prices usually revert to a mean.

Reverting back to a mean: When prices are said to revert back to a mean, this refers to regression to the mean, which is a statistical principle that states that values tend to drift toward the average over time. This phenomenon can be observed in many different fields of study such as economics, finance, and biology.

Why Would Prices Revert To A Mean?

Most people typically pay for a house or a car out of their income. Assuming that you kept interest rates constant, home prices would be a function of real income and supply and demand, which are slightly different from cars. It's a lot easier to fill the demand with cars in the car market than it is through housing stock in the housing market.

And despite the popular narrative, you aren't necessarily bringing home more bacon.

Adjusted for inflation, real incomes have actually declined over the last year – leaving many of us with less purchasing power than we had before!

And this would increase the probabilities that we continue to see price declines with used cars and trucks.

The bottom line is just like home prices came all the way down from 2006 to 2012 and bottomed out at their historical trendline, I think used cars and trucks will do the same thing.

[ctt template=”5″ link=”5QVC8″ via=”no” ]Used cars and trucks will likely hit their 2019 historical trend line, just like housing prices did back in 2012.[/ctt]

I would be prepared for car and truck prices to not only come down from where they were just six months ago, but I would also assume that they would continue to go down to where they were at the end of 2019.

If prices continue to collapse, what will this do to the subprime auto loan market? And what will this do to the banking system? Could this be a repeat of what we saw with the subprime mortgages in 2008 and the GFC?

Housing Market Bubble vs. Car Market Bubble

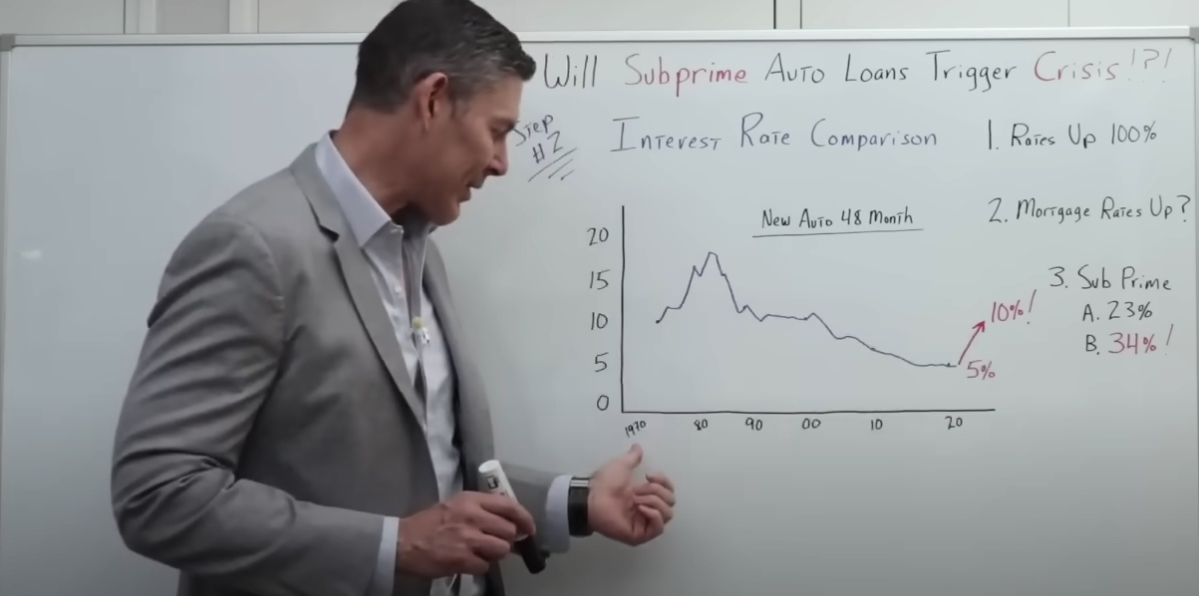

We saw how the housing bubble was very similar to the car bubble we live in today. But now, let's go ahead and compare interest rates to further determine whether or not this is something that we should be concerned with moving into 2023.

We start with a chart going back from 1970 to today's date. This is a chart of interest rates on new 48-month auto loans.

On the left, the interest rates go from 0%, up to 20%.

In 1975 interest rates on new 48-month auto loans were about 10%, then they went up when Volcker raised rates to a peak of around 20% in the early 80s.

Since then, they've come down to about 5%, just before and during the pandemic.

But recently, auto loan rates have gone straight up because Jerome Powell has been increasing interest rates, among other things. So I want to point out that we went from 5% interest rates on auto loans to roughly 10%.

Interest rates have almost doubled, over the last year in this market.

We can see that mortgage rate increases prior to the GFC were substantially less than what we see in the car market today. An ominous warning sign. But wait, there is more.

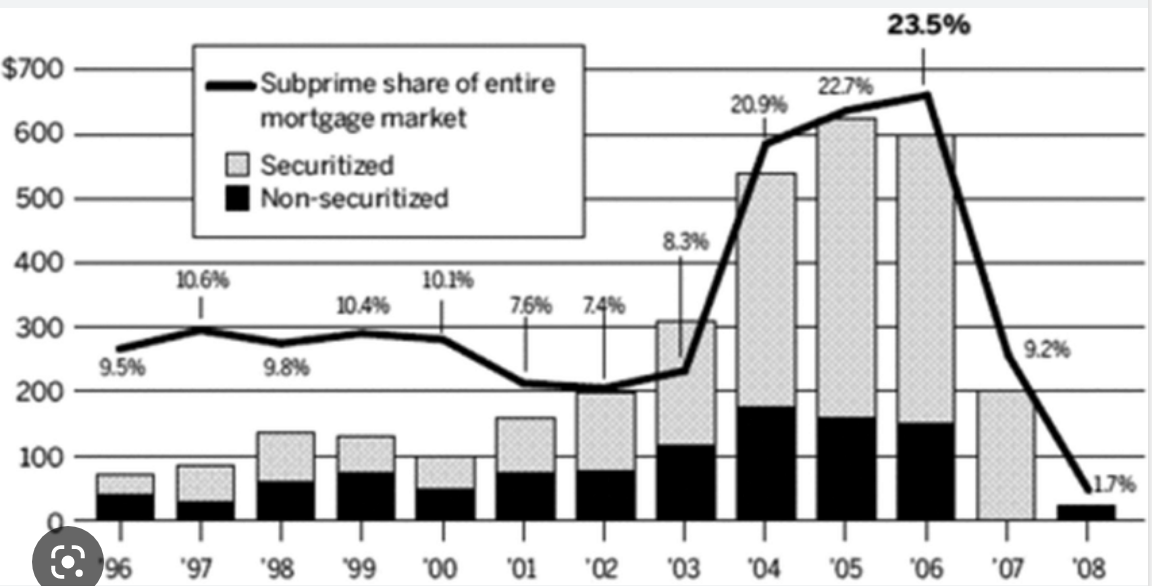

Let's look at the subprime category of home loans prior to the GFC, compared to car loans today.

Before the GFC, the subprime percentage of overall home loans was about 23%.

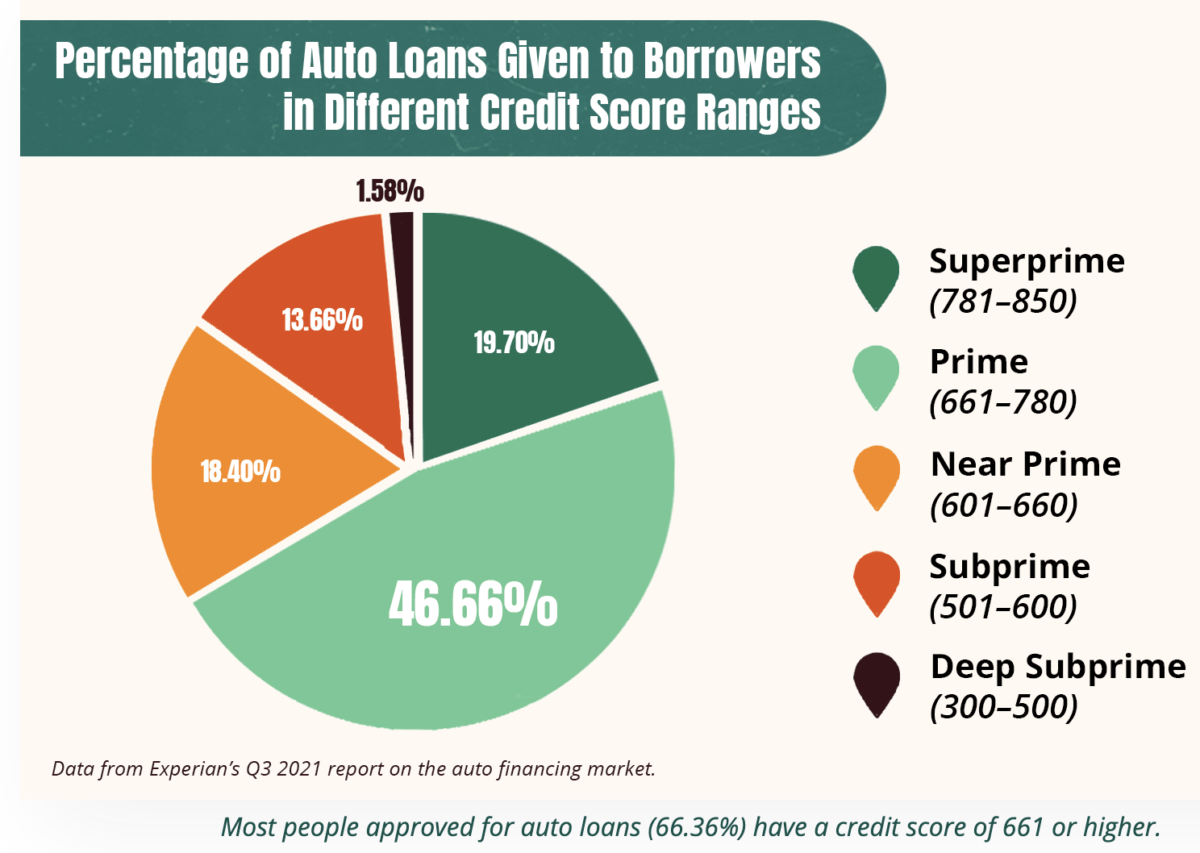

Today, in the auto industry, subprime auto loans make up about 34%.

When you look at how quickly, interest rates have gone up, and how much they have gone up, you also consider that there's a much greater percentage of subprime borrowers in this market. You see very quickly that many metrics are far worse today with the car market than before the GFC in the housing market.

[ctt template=”5″ link=”w7dd4″ via=”no” ]Interest rate hikes and an increase in subprime customers mean tougher times ahead for those in the auto industry and will impact the US economy negatively throughout 2023 ⚠️ #carmarket[/ctt]

Car Market Collapse

We have to look at the risks to the banks. But before we do, I want to cut to a clip from my good buddy Adam Taggart's podcast Wealthion, where he discusses some of the nuances of the problems the car industry is facing right now, in 2023.

Adam Taggart: Between 2020 and 2021, you know, it seemed like lending standards for auto loans just dropped, down into the core of the Earth.

It was like they would give a loan to anybody with a pulse who had a stimulus check to spend, just like we did with housing. My concern is what we're going to see this time around. This market's subprime crisis will be the auto market, like how housing was back in 2008.

Lucky Lopez: Oh, 100%. You hit the nail on the head. When we were starting to go into the pandemic, we were buying cars back-to-book, operating on the same principles.

Then suddenly, we heard multiple banks saying to prime customers, “Hey, you know what? Instead of 110% of loan-to-value (LTV), we'll give you no money down, cover sales tax, add a few bucks of aftermarket products, warranties, etc…”

They were going up to 150-160% loan-to-value.

So I was like, okay, maybe they're doing a little extra because people just didn't want to spend the money, so they're stimulating sales. That's originally how we thought it was, they were just going out of the way to stimulate sales.

But then, all of a sudden, they brought the subprime markets into it. People we usually would see lent 90% of LTV, were getting 130%, 140%, 150%, loan-to-value, and it blew my mind.

So all of a sudden, there's a rush of all these, we call them “stimulus ballers” on my channel, people that didn't pay their rent, that waited three months and got a big stimulus check from the government with $10,000-$12,000 to spend just showedup to the dealership with stimulus money.

The banks didn't ask for past bank statements, they didn't do a lot of important things. They just saw all this free money coming from the government, so they pumped these loans out, and held onto them for a little bit, then sold them to another bank to see who would take the loss. And so the frenzy began.

Everybody was just buying deals left, and right. The prime banks got into it first, now subprimes are into it. The banks have collected all these auto loans, bundled them up, and they are now selling them off to each other like a deadly game of hot potato.

The Car Market Is In Serious Trouble

But will it lead to a GFC 2.0? My answer is no. And here is why.

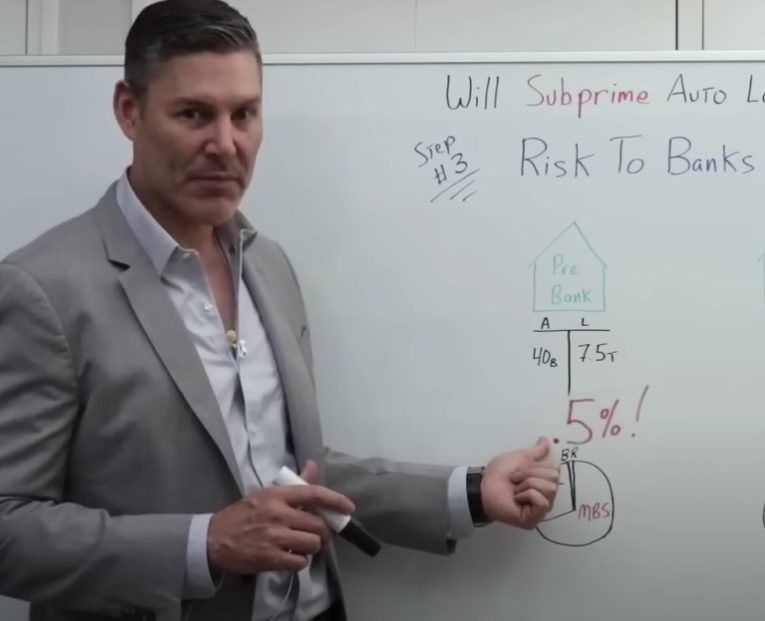

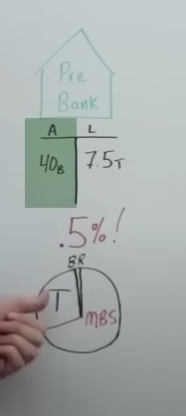

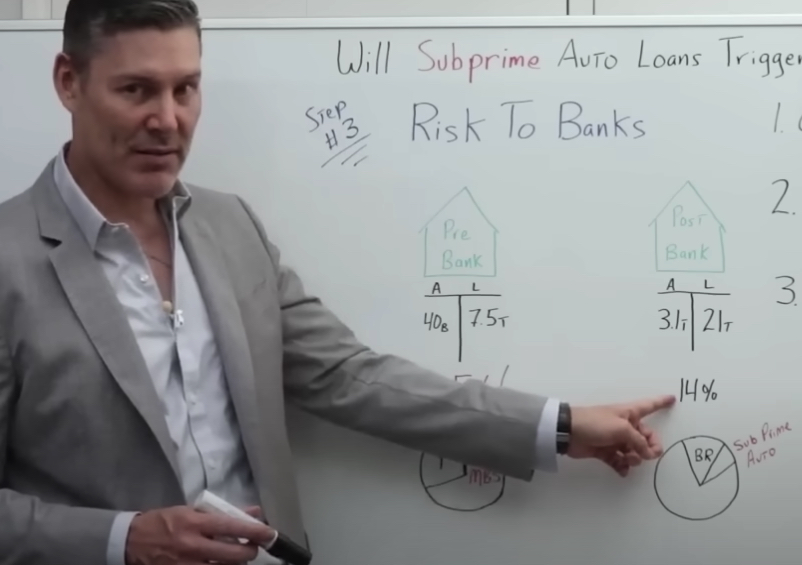

Let's look at the balance sheets of two banks. These banks represent the entire banking system in the United States. So the banking system in aggregate total.

We've got pre-bank (pre-GFC), and post-bank (post-GFC).

Pre-Bank (Pre-GFC)

So before the GFC, if we look at the asset side, the liability side of the banking systems balance sheet, we see that on the liability side, they had about $7.5 trillion in M2 money supply. That M2 money supply would be a liability to the commercial banking system.

Okay, now, they had more liabilities than that, but we're just oversimplifying their balance sheets for the sake of this video and understanding the overall concept. So what did they have to back up that $7.5 trillion?

Regarding bank reserves, they had a whopping total of $40 billion. So if you do the back of the napkin math, you see that that was 0.5%.

I don't want to go off on a tangent. But if anyone asks you about reserve requirements, and whether or not they impacted the number of dollars circulating in the real economy, then you can point them to this statistic ($40b in assets and $7.5t in liabilities) that clearly shows that reserve requirements had no impact on the amount of M2 money supply.

I drew this little pie chart here, and it's not exact, but again, just gives you the idea of the overall concept.

This would be the assets on the bank's balance sheet in aggregate total backing up that $7.5 trillion in commercial bank deposits, or liabilities.

Let's just assume for a moment that they had this little sliver here of bank reserves, that was the 0.5%. And they had a much bigger portion of this pie chart with mortgage-backed securities. And then they had treasuries.

Okay, well, we know that a large portion of these mortgage-backed securities got a huge haircut. Very rapidly. Meaning that the value of these mortgage-backed securities on their balance sheet went from extremely valuable, down to almost nothing at all, very quickly. I can't make it any easier than that. And this is one of the things that contributed to the GFC.

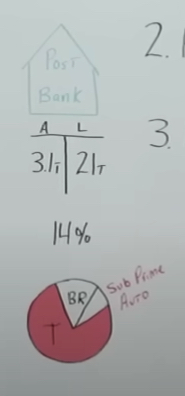

Post-Bank (Post-GFC)

Now let's go ahead and fast forward to post-bank.

On the liability side of their balance sheet, they've got $21 trillion in M2 money supply. On the asset side, though, they've got $3.1 trillion in reserves due to the Fed doing quantitative easing.

So this is 14% in bank reserves to back up that $21 trillion in M2 money supply for commercial bank liabilities.

Now let's go ahead and look at this new and revised pie chart.

This bigger portion is all treasuries. It's not entirely. But let's assume that it's relatively safe.

Okay, so we've got the 14% bank reserves. But now we have a much smaller slice of subprime on the books. We do have some mortgage-backed securities. And you could argue as to whether or not those are, quote-unquote safe.

But focusing on the main topic of this article, the banks of today have a much smaller slice allocated to subprime car loans than they had subprime mortgages back before the Great Financial Crisis.

Why I Don't Think The Collapse In The Car Market Will Lead To The Next Financial Crisis

Reason #1 – Bank Collateral

So the first reason I would give you as to why I don't think the collapse in the car market will lead to the next financial crisis is the collateral on the bank's balance sheet today is much different than it was pre-GFC.

And I would argue, although the bank's balance sheets are far from pristine, they have much less subprime toxic sludge on their balance sheets today than they had in 2007.

Reason #2 – Banks Are Getting Free Money

Another reason I think banks are less risky today is because they are getting free money.

My good friend, and business partner, Lyn Alden, talks about this all the time. So I showed you before how their reserves have gone from $40 billion to $3.1 trillion. But that's not the only thing that changed. Before the GFC, the Federal Reserve did not pay the bank's interest on their reserves after the GFC, they do.

And as the Fed increases interest rates higher and higher, and the Fed funds rate around 4.35% as of this post, the Fed is now paying the banks 4.35% on $3.1 trillion of reserves held on the Fed's balance sheet.

In the past, banks competed for your deposits, for your money, because lending them your dollars, would be a cheaper way of getting those bank reserves, which they need to conduct business. But now they're so flushed with reserves, they don't want your money, they don't even need it.

And this is why you see such a massive discrepancy in what the banks are willing to pay you on a savings account, compared to what they are getting on their savings or checking account held at the Federal Reserve.

The last time I looked, the average interest rate on a savings account was about 25 basis points.

And again, compare that to 4.25% or 425 basis points. The banks are getting paid. They're literally getting a spread of 4%. This is going to dramatically help their profit and loss. And this most likely makes their balance sheet far stronger than before the last crisis.

Reason #3 – Mortgage-Backed Securities

To support my opinion that the plummeting car market will not trigger a financial crisis, I would point out that mortgage-backed securities and mortgages were much higher in nominal terms during the GFC.

[ctt template=”5″ link=”FM_bY” via=”no” ]Mortgage-backed securities were several times larger at the time of the GFC than today’s car market, it's not enough to trigger another GFC.[/ctt]

In 2007, there was about $15 trillion worth of Home Loans. Today, it's about $1.5 trillion in the auto industry. So even if they have a higher percentage of subprime auto loans, in nominal terms, comparing apples to apples, that's a much lower number than the number of subprime mortgages we had before leading up to the GFC.

Let me be very, very clear. The auto industry, right now, is in a massive, massive bubble. And this will impact the US economy negatively throughout 2023. But I don't think it will be the catalyst to a GFC 2.0.

[ctt template=”5″ link=”48GSJ” via=”no” ]The auto industry, right now, is in a massive, massive bubble. And this will impact the US economy negatively throughout 2023. But I don't think it will be the catalyst to a GFC 2.0. #carmarket[/ctt]