Introduction

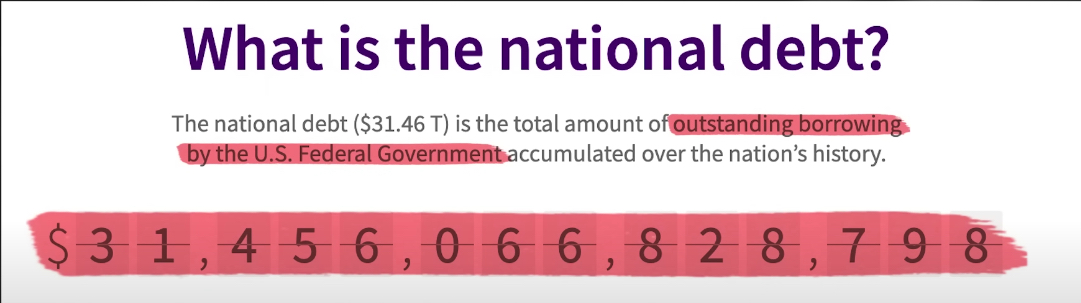

The US national debt has exploded higher and now is over $31 trillion.

And this incredible debt crisis could take the United States straight into the inflation danger zone.

I'm gonna explain this to you in three simple, fast steps.

[ctt template=”3″ link=”Lg5SK” via=”no” ]US debt is ticking up. In fact, the country has officially hit the $31.4 trillion debt ceiling. Republicans and Democrats must raise that $31.4 trillion debt limit by the summer or risk defaulting on debt payments.[/ctt]

The US national debt is the amount of money the US government owes. It has to pay this money back with interest. The US national debt has grown since the early 1980s and currently stands at around $31 trillion. The causes of this growth are complex, but some of the main factors include tax cuts, decreased revenue from taxes, spending on wars, defense programs, Medicare and Social Security benefits, and economic stimulus packages.

Step One – How Dollars Were Created Pre-GFC

Let's discuss how dollars were created before the Great Financial Crisis, not just in the United States but outside of the United States as well.

To understand what will happen regarding future inflation, we must understand how currency units – a major component of consumer price inflation – were created in the past.

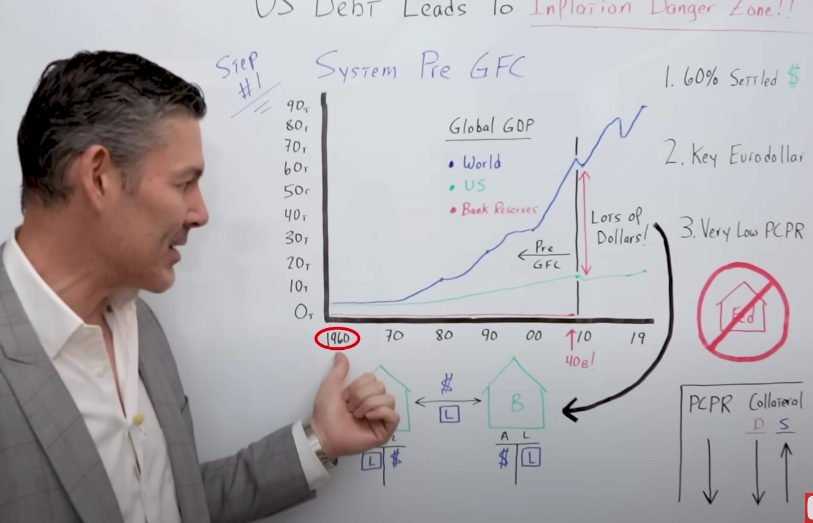

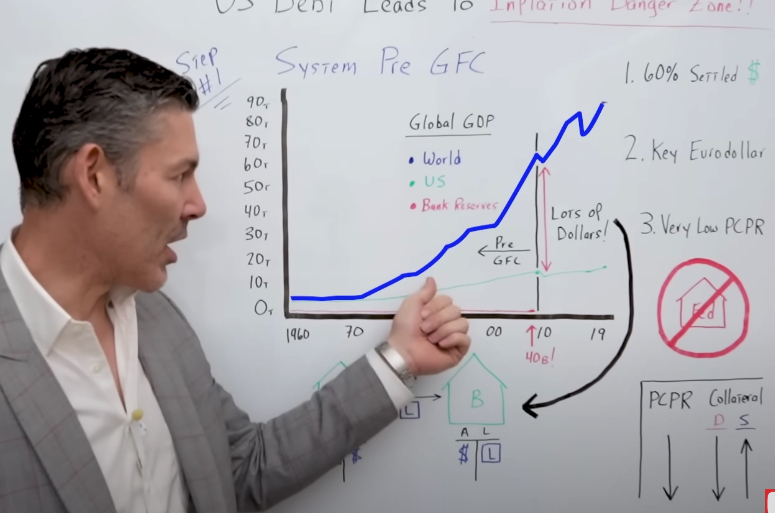

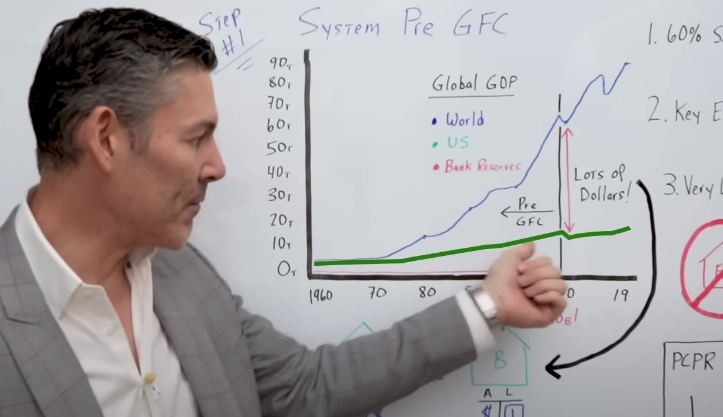

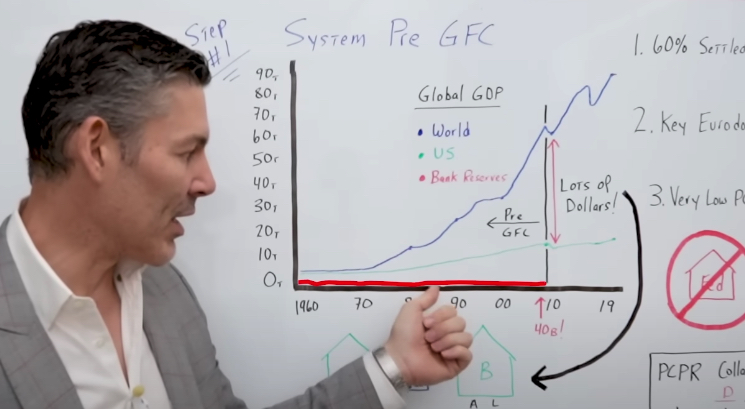

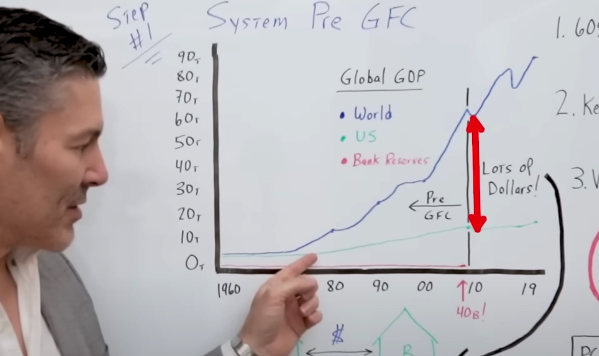

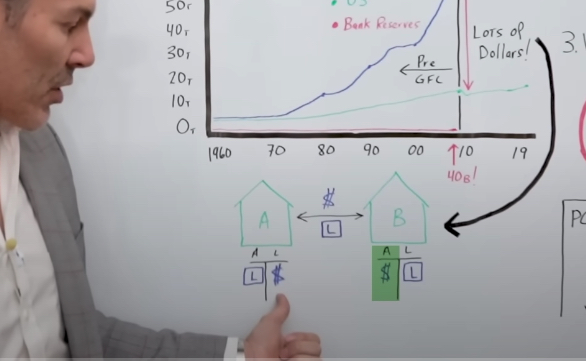

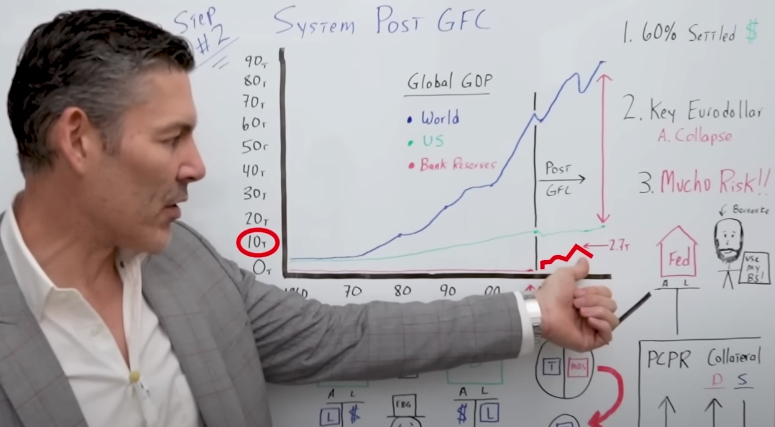

We start with a global GDP chart from 1960 to 2019. On the left, we go from $0 trillion up to $90 trillion.

This blue line represents Global GDP.

The green line represents United States GDP.

The red line is the amount of dollar-denominated bank reserves that were held at the Fed for the US banks.

Getting US-Centric

I'm getting US-centric because it gives you an idea of the balance sheet capacity for the US domestic banks that were being used to create dollars before the GFC.

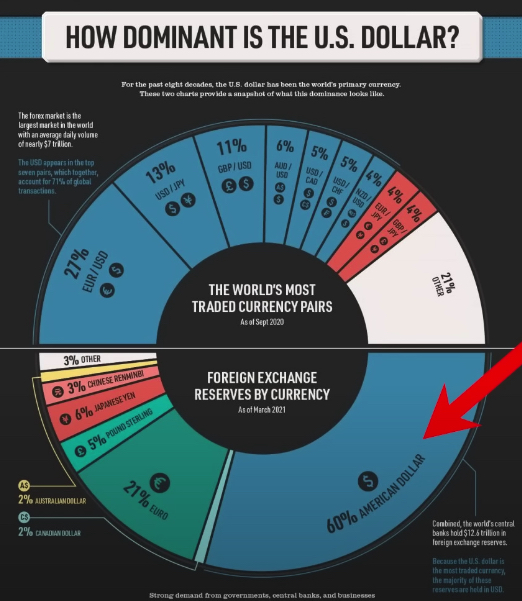

First and foremost, I want you to understand that 60 to 70% of global transactions are settled in dollars. Going all the way back to Bretton Woods when the dollar became the global reserve currency.

The Bretton Woods Conference of 1944 was a pivotal event in the history of international monetary order. It represented a cooperative effort between 44 Allied nations to standardize their currency systems and bring stability and predictability to global markets.

At its core, the conference established the US dollar as the world's primary reserve currency, meaning all other currencies were pegged to it and could be valued against it.

The conference also established the International Monetary Fund and the World Bank, which would help facilitate international trade and provide economic assistance to developing countries.

Focusing on world GDP

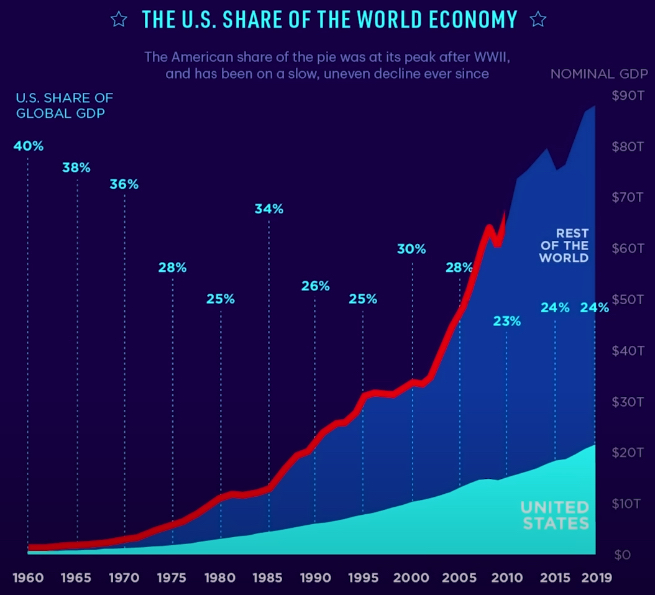

In 1970, world GDP started going up significantly. From 1980 to 2000 it shot up very steeply. Then from 2000 to 2010, it pretty much went parabolic. World GDP skyrocketed up to almost $70 trillion.

At the same time, the US economy went from $8 trillion to $20 trillion.

The main thing I want you to take away from the above chart is the huge gap between the blue and green lines.

Understand that this blue line going up, especially to this degree, requires many dollars because a high percentage of global trade is settled in USD.

You may be asking yourself, “Okay, George, I understand. But what's your point?”

The point is that many dollars were created outside of the US domestic system.

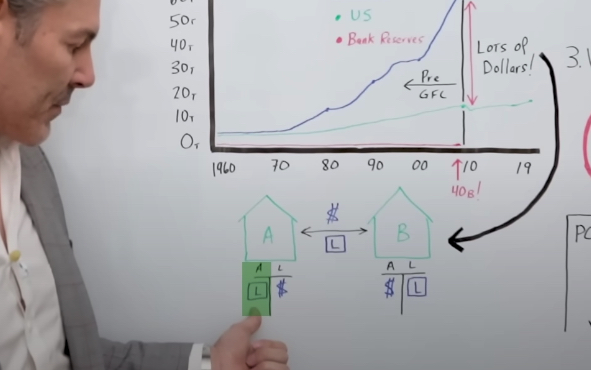

Remember, we've got a $70 trillion economy, and the United States banks only have $40 billion in bank reserves.

How on earth could the United States commercial banks backstop an entire $70 trillion system?

The answer is they couldn't.

The Eurodollar System

The Eurodollar System is a network of banks outside of the United States that, since the 1950s, have been creating US dollars without the Federal Reserve. These are dollars that are created with no reserves to back them up. There's no cash, no green pieces of paper.

You may be scratching your head and saying, “Okay, George, well, how on earth does that work?”

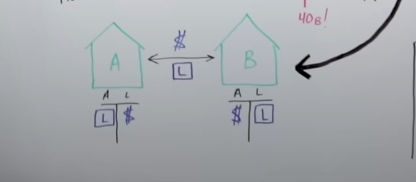

All right, we got Bank A, and we got Bank B. We got the balance sheets, assets on the left, and liabilities on the right.

Bank B needs dollars!

Bank B: “Hey, Bank A, I need a loan.”

Bank A: “Okay, I know you. You're my buddy. There's very low counterparty risk in the system. We'll go ahead and give you that loan.”

Bank A creates dollars out of thin air, since dollars are lent into existence, then gives them to Bank B.

Here's what the balance sheets look like after the transaction

We got Bank A which has the loan they just created on the asset side of their balance sheet. The liability for Bank A is the Eurodollar deposit given to Bank B.

On Bank B's balance sheet, their assets are those newly created Eurodollars. The liability for Bank B is the loan they need to repay to Bank A.

My point in step number one is to illustrate how the above system created trillions and trillions of dollars outside of the United States without the help of the Federal Reserve and the central bank.

What made this system work? Trust!

Trust in the System?

Trust is what made the whole pre-GFC system function properly. In other words, we had perceived counterparty risk because trust was in the system.

If Bank A trusted Bank B and knew they would make a profit, why wouldn't they do the loan? They didn't even need collateral!

They had very low perceived counterparty risk in those days. The demand for pristine collateral was very low, but the supply for pristine collateral was very high.

Why? Because there's actually a collateral multiplier. We will talk about this throughout the rest of this blog post and the video above.

Pristine collateral is a valuable asset in the financial system that carries virtually no risk.

It is the highest quality type of collateral, with a clean and undisputed title, free from liens or encumbrances. Pristine collateral is often used to secure loans, underwrite transactions and establish credit lines.

Pristine collateral is typically used by financial institutions and other organizations that need to secure a large amount of money or back up another type of agreement.

It can include assets such as cash, securities, real estate, and various forms of investments.

When an institution issues a loan, the borrower typically pledges some form of pristine collateral to guarantee repayment.

What is a collateral multiplier?

If there's very low perceived counterparty risk, then primary dealers and financial institutions will lend the same treasury to multiple parties to use as collateral.

One Treasury can be used for collateral 10, 20…even 30 times. This assumes the perceived counterparty risk is very low, which takes our story straight into the global financial crisis.

Step Two – When The Global Monetary System Changed Forever

in 2008, the world and the global monetary system changed forever.

Let's go into why the world almost ended in 2008, how the system changed, and why it will likely lead the United States straight into the inflation danger zone.

Why The World Almost Ended In 2008

The key is returning to the incredibly fragile global monetary system.

Why was the global monetary system so fragile?

Because it was built on one thing, and one thing only, that was trust. When trust collapses, so does the global economic House of Cards.

Going back to step number one, we know that before 2008, the system was built on trust.

And if we did need some collateral, we had treasuries and everyone's favorite toxic sludge in this saga, mortgage-backed securities.

When the GFC hit, everyone recognized the banks and what they were doing and said,

“We're not going to take your mortgage-backed securities anymore!

Counterparty risk is going through the roof, trust is going down, and we need more pristine collateral. All the system has available are Treasuries”

Treasury securities are debt instruments issued by the United States Department of the Treasury, which is the Federal government's fiscal agency. These securities are issued to finance government spending and borrowing costs.

The most common types of Treasury securities are Treasury bills (T-bills), Treasury notes (T-notes) and Treasury bonds (T-bonds). T-bills are short-term debt instruments with maturities ranging from a few days to 52 weeks. They are auctioned off in weekly and monthly installments. T-notes have intermediate maturities of two to ten years and are auctioned off every two, three, five or ten years. Treasury bonds have a long-term maturity of ten to thirty years and are auctioned off every five, ten or thirty years.

Treasury securities are sold in auctions via the Treasury Direct system, a secure online platform. The competitive bidding process determines the interest rate on these securities at the time of the auction.

So the amount of available collateral went from a large amount straight down to a tiny amount almost overnight.

And this is one of the main reasons why we had the GFC.

If it weren't for the fact that the Eurodollar system was so fragile, it most likely would have just been a real estate crash.

It would have been contained to those countries where the real estate got up to nosebleed levels. It would not have been a global financial crisis.

What happened once the trust evaporated and the amount of collateral basically got sliced in half?

Ben Bernanke, everyone's favorite central banker, came to the rescue.

Ben was out there saying, “Hey, we've got the Federal Reserve here. We will go ahead and use our balance sheet to backstop the entire system.”

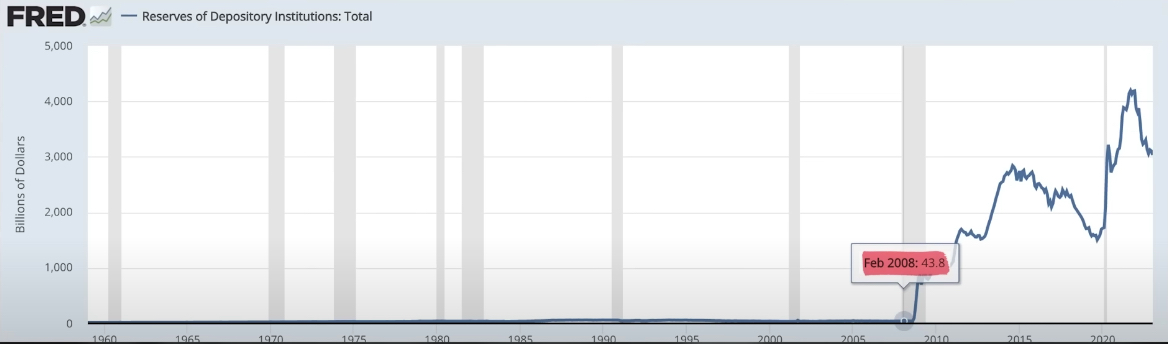

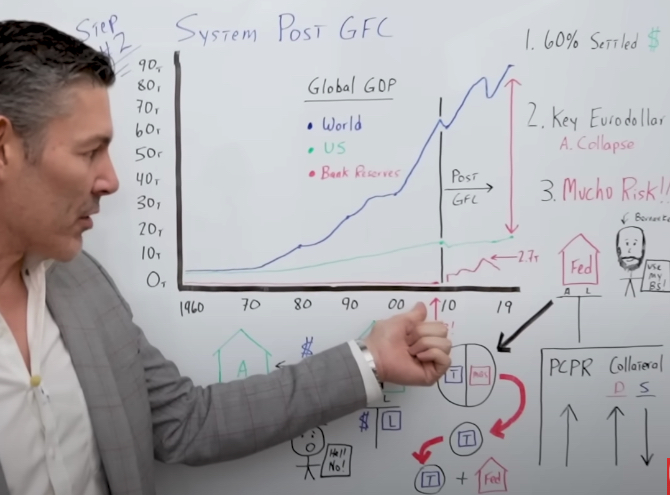

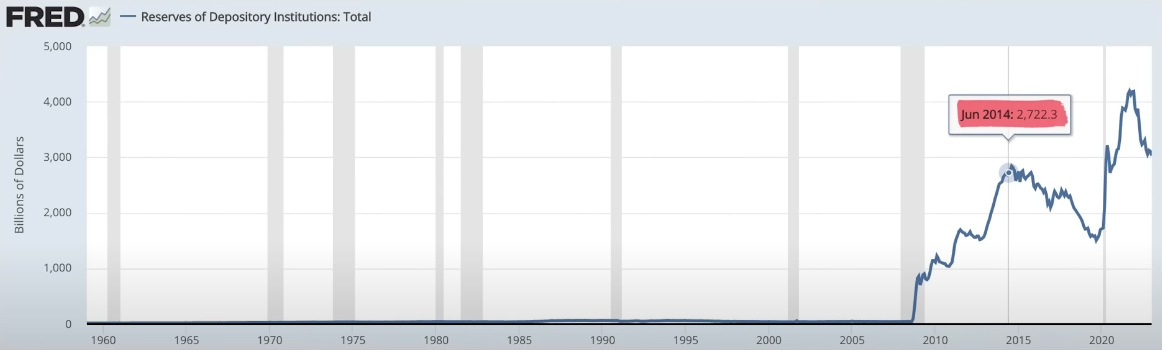

And you can see this happening right here on our chart.

Remember, this chart is not just global GDP, but also this red line indicates the bank reserves on the balance sheets of the US domestic banks at the time.

Quantitative Easing! We All Remember That, Right?

QE1..2..3. Now it's pretty much infinity, although they're currently trying to do Quantitative tightening (QT). More on that at the moment.

Quantitative easing (QE) is an unconventional monetary policy used by central banks in times of economic uncertainty to stimulate the economy. It involves the purchase of financial assets from commercial banks and other private institutions, with the goal of increasing money supply by creating new money and injecting it into the market. This works to reduce interest rates and encourage borrowing and spending, thus stimulating economic activity. QE can also be used to manipulate exchange rates, as it increases the money supply in one country relative to other countries that are not using QE.

We did QE1, QE2, then QE3. Then we started QT heading into 2019 but then reversed course when the covid pandemic hit.

Notice from 2008-2015, Ben Bernanke took the reserves on the Fed's balance sheet from $40 billion to $2.7 trillion.

Now, I know you may be looking closely at my chart below thinking, “George, that's $10 trillion on the left, not $2.7 trillion. You're not even close to accurate on your stupid drawing. Chart crime!”

Yeah, I get that. But if I only brought it up to $2.7 trillion, you wouldn't be able to see it. Forget the left-hand side for now and focus on $40 billion straight up to $2.7 trillion.

The massive increase in reserves indicates what Bernanke was doing. He's going to the global monetary system and saying, “Hey, we realize now that you're short on collateral, the Trust has evaporated. So go ahead and use my balance sheet to backstop the system.”

As a result, perceived counterparty risk and the demand for collateral go straight up. Naturally, said supply of high-demand collateral goes down.

Unfortunately, the system is even more fragile and unstable today, especially if you remove the Federal Reserve from the equation. And as you can imagine, this is when the problems really began.

Sit down, and pour yourself that stiff drink because you'll need it for the rest of this.

Step Three – The Inflation Danger Zone

Now let's talk about how the United States debt will most likely continue to explode higher and how this could take us straight into the inflation danger zone for the rest of the 2020s.

In step one, we discussed the system before the GFC when there wasn't much Federal Reserve involvement. And there wasn't much collateral in the system – which keeps institutions honest – because everyone perceived counterparty risk as very low at the time.

Post-GFC, we transitioned to a system backstopped by the Fed. The system needed lots of pristine collateral because perceived counterparty risk had increased dramatically.

Today, we've gone into a whole new world—a new type of system. Also, Jerome Powell is quantitative tightening, which is the exact opposite of quantitative easing.

Quantitative tightening (QT) is a monetary policy tool central banks use to reduce the money supply in an economy. It involves the sale of government bonds and other financial assets from the central bank's balance sheet, resulting in fewer funds for commercial banks to lend out. This decreases spending and investment in the economy, which reduces inflationary pressures.

QT is typically used when a central bank believes an economy has become overheated and is at risk of inflation or financial instability. It can also be used to help strengthen the local currency in foreign exchange markets by reducing the amount of money available for speculation or investment.

Before, the Fed had its balance sheet backstopping the eurodollar system. Now, they're doing the exact opposite. The Fed is taking its balance sheet out of the equation.

What is this new world that we're moving into?

It's a world where there's no Federal Reserve! This assumes that Jerome Powell continues with quantitative tightening.

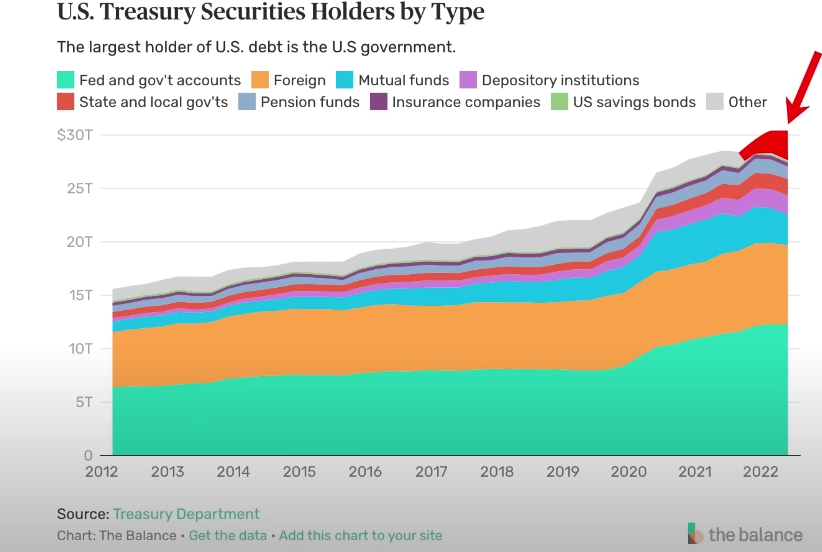

We will need more collateral because if we don't have the Fed's backstop, that void must be filled with something. Most likely, that will be filled by US Treasuries…that pristine collateral.

Let's go back to our examples of Bank A and Bank B.

Bank B needs some dollar liquidity…an extension of credit…dollars…a loan…however you want to rephrase it…from Bank A.

Bank A says, “Okay, we need those treasuries first.”

Bank B has those treasuries on its balance sheet, but if it didn't have those treasuries, it couldn't get the dollar liquidity it needs.

If there's no Fed, there is nothing to backstop Bank B. They will need way more treasuries moving forward to get the dollar liquidity they need.

What is happening to perceived counterparty risk?

We've got this system that has been built on the Fed's balance sheet and collateral since the GFC, and now they're removing the Fed's balance sheet from the equation. Naturally, perceived counterparty risk will likely continue going up.

If perceived counterparty risk increases, the demand for collateral also increases. We're seeing this now, actually. The supply of collateral then goes down because primary dealers and financial institutions are much less likely to re-hypothecate their treasuries. After all, the risks are too high.

Government Deficit Spending And Inflation

Let's think through government deficit spending, how it may impact inflation, and how it creates more currency units in the United States economy, chasing the same amount of goods and services.

When your Drunk and Insolvent Uncle Sam issues treasuries, the cash from buyers (the average Joe, business XYZ or nonbank entities in the real economy) goes back to the government and into the Treasury General Account (TGA).

Janet Yellen then takes those dollars and spends them back into the economy.

Regarding the balance sheets, the average Joe and business XYZ are trading dollars for treasuries.

Okay, that makes sense.

On net balance, has the number of dollars or currency units in the real economy gone up or down?

Trick question, neither!

On net balance, it's a wash. The dollars leave the nonbank entities' bank accounts and enter back into the economy.

However, when the Eurodollar system needs more pristine collateral (treasuries), it will become a significant buyer and likely outbid the average Joe and nonbank entity in the domestic economy. Eurodollar system participants have become significant buyers over the last few years.

This puts the government in a difficult position, almost a Triffins dilemma 2.0.

The Difficult Decision Facing Triffin

And most of you know from watching my videos the original Triffins dilemma, or Triffins paradox story.

Back in 1944, when the United States had the world reserve currency, Triffin came in and said, “Wait a minute, this is probably not going to end well.

The United States is now responsible for supplying the world with all the dollars it needs to grow and function.

If the United States does that, it will have to run massive trade deficits, hollow out its manufacturing base, and do other things that might be counterproductive to the United States economy.

On one hand, you've got the US domestic economy; on the other, you've got the global economy. You have to choose.

They built a system where the United States has outsourced all its manufacturing based on having to export more and more dollars through bigger and bigger trade deficits.

Now, the United States government could be facing a similar paradox. But this time with treasuries and not dollars.

[ctt template=”5″ link=”f93T6″ via=”no” ]They built a system where the United States outsourced all its manufacturing based on having to export more and more dollars through bigger and bigger trade deficits.[/ctt]

They've got to make a choice. Either they continue to create more and more treasuries, which is what the global system demands. Or they could tighten their belt and do what's suitable for the domestic economy. But then, the global system implodes.

And you may be saying yourself, “Okay, George, well, that's a good choice. I prefer, as an American, that we focus and prioritize the US domestic economy.”

Not so fast. You have to understand that now, the United States domestic economy is entirely dependent on the global economy. We can't let it implode.

[ctt template=”5″ link=”64ezq” via=”no” ]You have to understand that now, the United States domestic economy is entirely dependent on the global economy. We can't ignore the global economy and let it implode.[/ctt]

We're between a rock and a hard place where the government might have to deficit spin to greater and greater degrees to give the global system the collateral it needs to avoid imploding.

And you say to yourself, “Okay, George, I get that. But what does that has to do with inflation?”

What you need to know about inflation

Domestically, dollars flow in, and dollars flow out. On net balance, it's a wash.

In the Eurodollar system, however, all these foreign buyers come in and buy US treasuries with eurodollars. These are dollars that were created outside of the United States.

These dollars come into the hands of big government in exchange for treasuries that go out into the system as collateral. Then Janet Yellen spends these newly acquired eurodollars in the domestic system. Since these dollars come from offshore, they become a net increase to the domestic economy.

In other words, we get more dollar-denominated currency units chasing the same number of goods and services. It could take us right into this bizarre situation where the United States CPI continues to skyrocket.

The dollar is losing value against goods and services in the United States. At the same time, the dollar is gaining value against fiat currencies outside of the US domestic economy. This is why the United States debt will most likely increase in the future and how it could take us straight into the inflation danger zone.

[ctt template=”5″ link=”fnjYw” via=”no” ]The United States debt will most likely increase in the future and could take us straight into the inflation danger zone.[/ctt]